Tiger Research: まずRWAトークン化を海外へ移行せよ

- 核心見解:規制が未成熟な司法管轄区において、金融機関は受動的に自国の法整備を待つのではなく、積極的に海外市場に進出するか、オンチェーンネイティブプラットフォームを活用することで、先行的に運営経験を蓄積すべきです。

- 主要要素:

- 2026年上半期時点で、RWAトークン化市場の規模は250億~360億ドルに達し、効率性は大幅に向上していますが、多くの地域では分散型台帳に法的効力を付与する枠組みが欠如しています。

- 金融機関は3つの戦略的選択肢に直面しています:法整備を待つ(リスクは低いが機会を逃す可能性あり)、規制サンドボックスを利用する(実験範囲が限定的)、海外の成熟市場に進出する(先行者優位を築ける)。

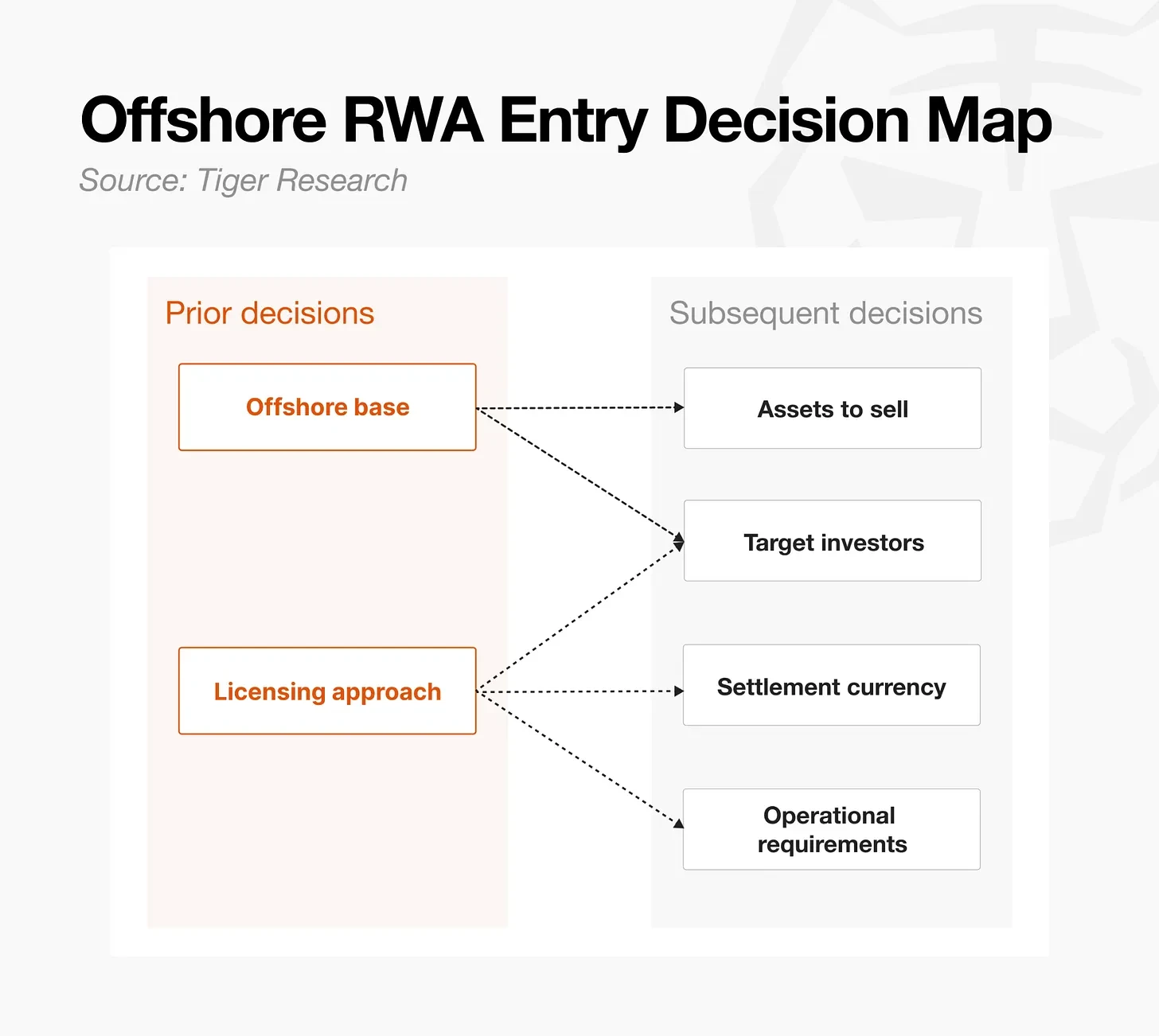

- クロスボーダーRWA業務は6つの側面で準備が必要です:海外拠点の設立、ライセンス・コンプライアンス、資産の定義、投資家の範囲、決済通貨と支払い、運営体制(カストディ、オンチェーンガバナンス等)。

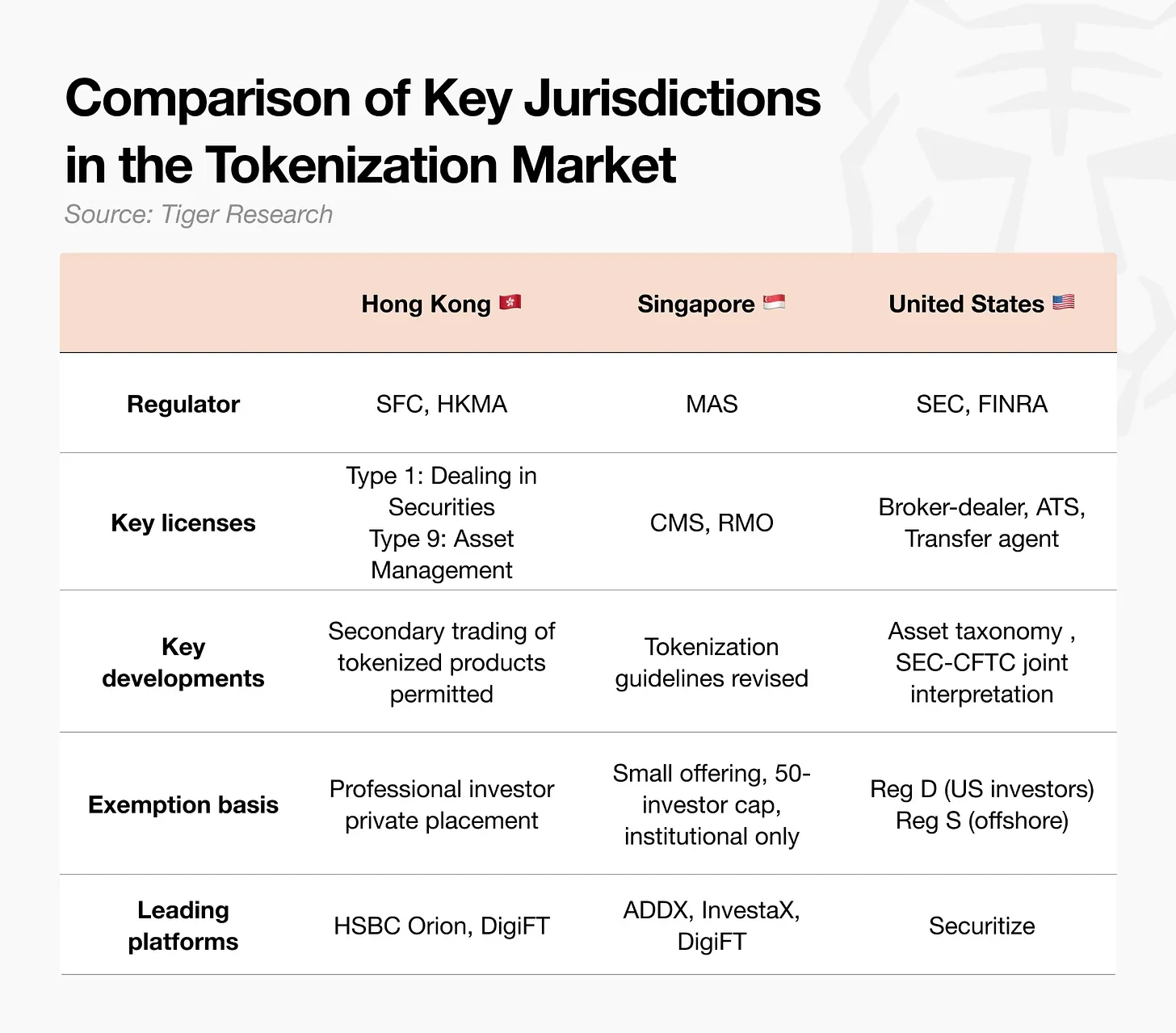

- 香港、シンガポール、米国が主要な先行市場です:香港は完全な規制チェーンと政策補助金を提供し、シンガポールは規制が厳格ながら明確であり、米国ではSecuritizeなどのプラットフォームを通じて効率的に発行できます。

- オンチェーンネイティブの経路(Ondo、Plumeなど)により、機関投資家は司法管轄区を回避し、コンプライアンス対応済みのプラットフォームを通じて迅速に市場にアクセスできますが、構造設計はより複雑で、プラットフォームごとの差異に依存します。

- 香港を例にとると、中堅証券会社は既存子会社を活用し、DigiFTプラットフォームを選択し、Regulation Sの適用除外を利用することで、評価から発行までの全プロセスを6~12ヶ月で完了できます。

Core Points

This article is from Tiger Research. The RWA market is growing rapidly, but many jurisdictions still lack a supporting regulatory framework. Financial institutions in these regions face a strategic choice between three options: waiting for domestic legislation, using regulatory sandboxes, or directly entering overseas markets.

Cross-border RWA business requires extremely high precision. Before entry, full preparation must be completed across six core areas, encompassing jurisdiction selection, licensing, asset definition, investor scope, and the design of settlement and operational arrangements.

The core goal is to accumulate real operational experience by choosing a path that suits one's own situation. The two main paths are: directly entering jurisdictions where regulations are already mature, and adopting the technological path of an on-chain native platform.

1. Wait, Experiment, or Go Global

As of the first half of 2026, the Real World Asset (RWA) tokenization market has grown to approximately $25-36 billion. The clear efficiency improvements it demonstrates, including automated interest payments and redemptions, shorter settlement cycles, and broader customer coverage, continue to attract the attention of institutional investors.

However, financial institutions still face real obstacles within regulatory vacuums. While tokenization is not explicitly prohibited, the legal framework needed to give legal effect to distributed ledger records has not yet been established, thus lacking sufficient protection for investor rights. In response, financial institutions choose between three broad directions: Waiting for domestic legislation favors risk management but carries significant risk of missing early market positions; Using regulatory sandboxes allows for limited experimentation but is restricted to areas like fragmented investments, not scalable to standard securities issuance; Entering overseas markets first means issuing digital bonds in jurisdictions where regulations are already in place, building a track record locally and using the experience gained overseas to secure an early competitive position.

The RWA market is fundamentally a global business, making it crucial to build operational capabilities across different regulatory environments. While overseas expansion has real constraints, it is precisely those financial institutions whose domestic regulations are still lacking that have more reason to gain first-hand experience in overseas markets ahead of their peers.

2. Tokenization is Not Magic

Cross-border RWA business is not the product of a series of isolated decisions. The choices involved are interconnected, with the outcome of each step determining the available options for the next. Tokenization is not magic; it is the process of migrating existing financial instruments to a new type of infrastructure, a process that demands higher, not lower, precision than traditional issuance.

Before deciding to enter, financial institutions should honestly assess their readiness against the following six requirements.

First, Establish an Overseas Base. Institutions must determine how to utilize key jurisdictions like Hong Kong, Singapore, or the US, and the specific path: via existing entities, new entities, or partnerships with local institutions. New entities offer greater control but require significant resources; partnerships allow faster market entry but limit the depth of internalizing core capabilities.

Second, Licensing. Institutions must meet the licensing requirements of the target sales jurisdiction. The choice is typically between obtaining a license directly (time-consuming and costly) and using the license of an existing platform (faster, but requires structuring the issuance according to the platform's specifications).

Third, Asset Definition. Choosing which assets to tokenize directly determines the entry barrier. Standardized securities like bonds have mature structures and are relatively easier to bring to market; non-standard assets like real estate or trade receivables require significantly more time for legal review and structural design.

Fourth, Defining Target Investors. A typical approach is to cover all jurisdictions except the US. Selling only to non-US investors can rely on Regulation S's offshore exemption; including US investors triggers additional requirements like Regulation D, significantly increasing structural complexity. Furthermore, many STO and RWA platforms restrict sales to accredited or institutional investors, so the sales strategy must be determined concurrently with the investor scope.

Fifth, Settlement Currency and Payment Process. Institutions must decide whether to accept local currency, USD, stablecoins, or wholesale CBDCs for settlement. This is not just a currency choice but a key variable determining investor accessibility, custody structure, and ultimately, revenue. For example, accepting stablecoins introduces exchange needs and potential additional costs.

Sixth, Other Operational Requirements. Depending on the structure, there are further considerations including blockchain choice, custody, on-chain operations, and post-issuance governance. Institutions must specifically confirm who controls interest payments and redemptions, register management, and the ability to force transfer or freeze tokens in the event of an event. These matters correspond to the operational requirements of traditional financial instruments.

Tokenization is not magic. Work is not finished once the structure is designed; the business truly materializes only when the securities are sold and investors are onboard.

3. Where to Operate

Jurisdiction selection is a strategic decision that requires balancing regulatory fit with operational efficiency.

For institutions with existing overseas presence, the most efficient starting point is to evaluate their current jurisdictions. If the primary goal of an overseas tokenization strategy is to gain early first-hand experience, establishing a new base in a completely new jurisdiction presents a significant barrier in terms of time and capital.

Hong Kong: Regulatory Completeness and Enforceability

Hong Kong is the most advanced first-mover market. Security tokens are regulated under the existing Securities and Futures Ordinance. A circular from the Securities and Futures Commission (SFC) in April 2026 allowed licensed virtual asset exchanges to conduct secondary trading, completing the full chain from issuance to circulation. Infrastructure like HSBC Orion is live, and policy support is substantial, including subsidies from the Hong Kong Monetary Authority (HKMA) for issuance costs. Institutions should be aware that if legislation introducing new licenses for virtual asset dealers and custodians progresses as planned in 2026, attention must be paid to compliance with transitional provisions.

Singapore: Precise Framework and Regulatory Clarity

Singapore strictly applies the Securities and Futures Act under the principle of "same activity, same risk, same regulation". The Monetary Authority of Singapore (MAS) revised its tokenization guidance in December 2025, providing clearer direction. The Variable Capital Company (VCC) structure simplifies asset segregation, making it particularly suitable for fund structures. However, Singapore imposes strict licensing requirements even for services targeting overseas clients, making the entry barrier high.

United States: Regulatory Clarity and Efficient Listing Paths

A joint interpretation released by the SEC and CFTC in 2026 clarified the asset classification framework. While the cost of directly applying for a license as an issuer remains high, efficient issuance is possible through vertically integrated platforms like Securitize: using Regulation D exemption for US qualified investors and Regulation S exemption for overseas investors. BlackRock's BUIDL fund is the most representative example of this path.

Each of these jurisdictions has mature platforms that can accelerate local entry. These platforms are licensed operators offering a one-stop service, including regulatory coordination, access to investor networks within the platform for fundraising, and operational infrastructure covering the entire lifecycle from issuance to settlement. When evaluating entry into a specific jurisdiction, engaging directly with leading local platforms to test business feasibility is strategically more efficient than reviewing a large amount of regulatory documents first.

4. Bypassing Jurisdictions

The previous section discussed the direct path: establishing legal and physical presence and obtaining necessary licenses within a specific jurisdiction. This section discusses a fundamentally different approach: the on-chain native path, which designs issuance and circulation around the on-chain environment from the outset.

Instead of investing the time and capital required to establish a physical base, this path partners with on-chain platforms that have built-in compliance capabilities or borrows their structural logic, lowering the entry barrier through such infrastructure. The location-based path of the previous section answers "where to operate," while the on-chain native path answers "how to structure the transaction."

Representative examples are as follows. Ondo Global tokenizes US securities through a bankruptcy-remote Special Purpose Vehicle (SPV) domiciled in the British Virgin Islands, using Regulation S's offshore exemption to minimize friction with US securities regulations. Ondo also operates its own secondary market, Ondo Global Markets, directly handling trading of issued tokens. Plume Nest holds a Class M DABA license from the Bermuda Monetary Authority through Plume's Bermuda subsidiary, KDAB (Kimber Digital Assets Bermuda), operating a regulated on-chain vault. Access to the Plume Nest platform is limited to investors who have passed KYB and KYC checks. Furthermore, an affiliated company registered as a transfer agent with the US SEC provides a second layer of assurance for ownership record management and distribution. Due to the platform's decentralized design, tokenization outside this regulated structure is also possible, but this path is not suitable for regulated financial institutions.

The on-chain native strategy is essentially similar to location-based tokenization but differs significantly in execution. Its primary advantages are speed to market and breadth of coverage: institutions are no longer limited to a specific base but can leverage proven infrastructure to reach the market faster. Another advantage is particularly evident when compared to location-based platforms: the closed ecosystem of location-based platforms might limit secondary market liquidity, whereas on-chain native platforms designed for scalability can organically connect with DeFi liquidity pools.

However, the complexity of structural design is a risk that requires careful consideration. The open nature of such platforms allows for a wider range of products, but lacks the mature regulatory guidance of the location-based path for core structural decisions like issuance design. The structural differences vary by platform rather than by jurisdiction, which can create operational burdens for traditional financial institutions. Therefore, assessing whether there are local counterparts to these platforms within the target region is a necessary preparatory step.

5. Don't Wait for Regulation; the Market Won't Wait

Large financial institutions in the US are already leading the market, either building their own platforms or gaining direct experience on Canton, Solana, and Ethereum. For financial institutions still in regulatory gray areas, launching an overseas RWA business means redesigning the entire value chain locally, from establishing a base to issuance and distribution, with a preparation period typically ranging from six months to over a year.

The following uses a hypothetical case to illustrate the process: A medium-sized securities firm, "Company A," which already has a presence in Hong Kong, tokenizes short-term investment-grade bonds for sale to overseas institutional investors.

Step 1: Assess Existing Base and License Status. Company A uses its existing entity (its Hong Kong subsidiary) to avoid the time and cost of setting up a new one. Whether the existing license covers tokenization is a separate issue. Local legal counsel assesses the scope of the existing authorization. If necessary, Company A makes a preliminary enquiry to the regulator (here, the SFC) to confirm whether a change in license conditions or additional filing is required.

Step 2: Choose Platform and Infrastructure. To reduce the time required for its own license application, Company A considers using mature platforms like DigiFT. Vendor due diligence covers the platform's license validity, supported asset types, custody partners, and investor restrictions. During the contract phase, legal review covers the issuance structure designed to fit the platform's specifications, allocation of responsibilities, and governing law.

Step 3: Compliance and Product Design. This phase finalizes the product structure of the bonds to be tokenized, including the underlying asset, investor rights, and governing law. The standard approach is to use the Regulation S exemption for sales to overseas institutional investors outside the US. Legal opinions on local securities law compliance are obtained for each target jurisdiction. Company A must also confirm that its logic for excluding domestic investors is legally sound under securities law before proceeding to the drafting and approval of issuance documents.

Step 4: Design Custody Structure and On-Chain Operations. Company A establishes a dual custody arrangement, with a global custodian bank holding the underlying assets and professional infrastructure hosting the on-chain tokens, with relevant legal opinions obtained from external counsel. Operational details are also finalized, including the interest payment schedule, settlement currency (USD or stablecoins), and redemption mechanism.

Step 5: Issuance, Execution, and Verification. Company A executes the actual issuance and sale according to the finalized structure, and subsequently confirms that operational processes like interest payments and redemptions function as designed. Structure design is merely the starting point; the business is completed only when investors are onboarded and sales are finalized.

The above overseas tokenization strategy is not limited to the direct path of "establishing a base in a specific jurisdiction." Paths like the on-chain native approach, which offer more flexibility to bypass jurisdictional boundaries, effectively keep the space of feasible solutions open. Legal review will be the most time-consuming and costly hurdle in any path. However, waiting for a complete regulatory framework is not the only answer. The ability to quickly outline a feasible path and accumulate experience through execution is more critical than any other factor. The reason is simple: the essence of a tokenization business lies not in technical design, but in the ultimate completion of the full sales process.

No one can predict when regulations will finally be established, and the market will not wait. The time to act is now.