Làm thế nào để xác lập lãi suất cơ bản cho Crypto?

- Quan điểm cốt lõi: Thị trường tiền điện tử thiếu một lãi suất cơ bản thống nhất. Mặc dù tồn tại nhiều ứng cử viên lãi suất (như phí tài trợ hợp đồng vĩnh viễn, lãi suất cho vay), nhưng không có một chỉ số đơn lẻ nào có thể đồng thời đáp ứng các tiêu chuẩn “phạm vi rộng, có cấu trúc kỳ hạn, độc lập về quản trị”, khiến toàn bộ hệ thống tài chính thiếu một điểm neo định giá đáng tin cậy.

- Các yếu tố chính:

- Tăng trưởng bùng nổ của thị trường hợp đồng vĩnh viễn: Báo cáo của BitMEX cho thấy, khối lượng giao dịch hàng tuần trong quý của mảng “tài sản truyền thống vĩnh viễn” đã tăng vọt từ 526 triệu USD lên 30,7 tỷ USD, tương đương mức tăng 5.756%.

- Lãi suất cơ bản đủ tiêu chuẩn cần đáp ứng: Dựa trên giao dịch thực tế, độ sâu thị trường khó bị thao túng, độc lập về quản trị, có cấu trúc kỳ hạn, tương tự như SOFR trong tài chính truyền thống (dựa trên giao dịch repo trái phiếu kho bạc trị giá nghìn tỷ USD).

- LIBOR đã bị bãi bỏ do vụ bê bối thao túng báo giá, chất thay thế SOFR dựa trên dữ liệu giao dịch thực tế, do Cục Dự trữ Liên bang New York quản lý, giải quyết vấn đề xung đột lợi ích.

- FRR (Tỷ lệ hoàn vốn chớp nhoáng) của Bitfinex dựa trên giao dịch tài trợ kỳ hạn thực tế, có cấu trúc kỳ hạn tự nhiên, nhưng được vận hành bởi một sàn giao dịch duy nhất và cùng thuộc công ty mẹ iFinex với Tether, tiềm ẩn rủi ro tập trung và xung đột lợi ích.

- Lợi suất trái phiếu kho bạc được token hóa (ví dụ BUIDL) bám sát lợi suất trái phiếu kho bạc Mỹ, là ứng cử viên cho “lãi suất phi rủi ro tiền điện tử”, định giá trên thị trường thứ cấp chính xác, độ lệch chỉ 2-5 điểm cơ bản.

- Chênh lệch lãi suất hiện tại phản ánh rủi ro cấu trúc: Chênh lệch giữa phí tài trợ hợp đồng vĩnh viễn và lợi suất trái phiếu kho bạc được quy cho biến động đòn bẩy, lãi suất Aave bao gồm rủi ro hợp đồng thông minh, phần bù FRR của Bitfinex thể hiện rủi ro đối tác sàn giao dịch và stablecoin.

Original Author: @BlazingKevin_, Blockbooster Researcher

1. Crypto Has No "Base Rate"

Leverage and financing in the crypto world—trillions of dollars in leveraged positions, collateralized loans, and yield products—operate without a unified benchmark rate curve.

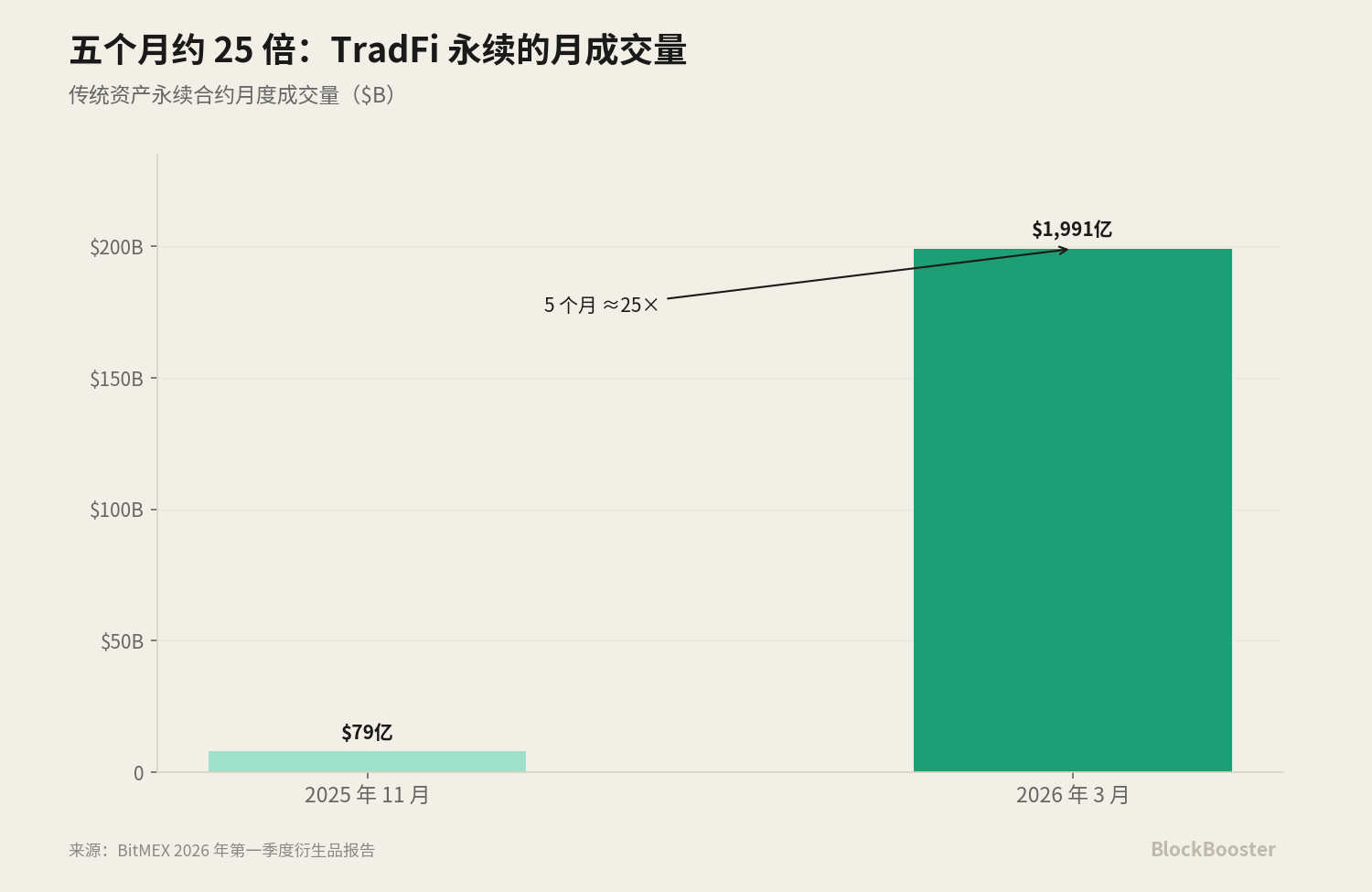

According to BitMEX's Q1 2026 derivatives report, the single-quarter weekly trading volume for the nascent "traditional asset perpetuals" track surged from approximately $525.8 million at the end of 2025 to $30.7 billion by mid-March 2026, a quarterly increase of about 5,756%. Its monthly trading volume soared from $7.9 billion in November 2025 to $199.1 billion in March 2026, growing roughly 25 times in five months.

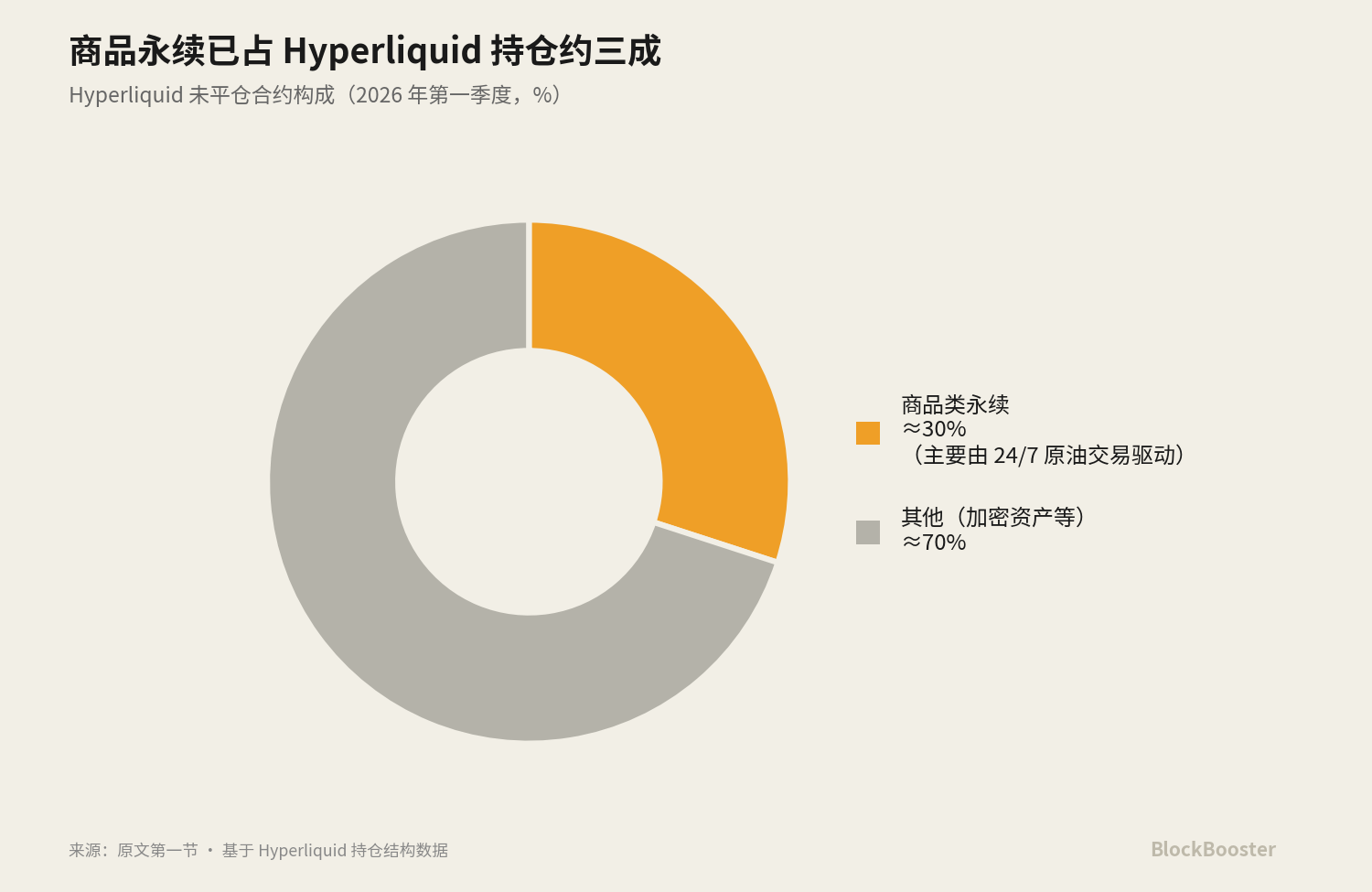

Based on DefiLlama's 30-day snapshot, Hyperliquid processed approximately $172.63 billion in perpetual volume, with open interest around $9.13 billion. In Q1 2026, commodity perpetuals accounted for about 30% of Hyperliquid's open interest, primarily driven by demand for 24/7 crude oil trading.

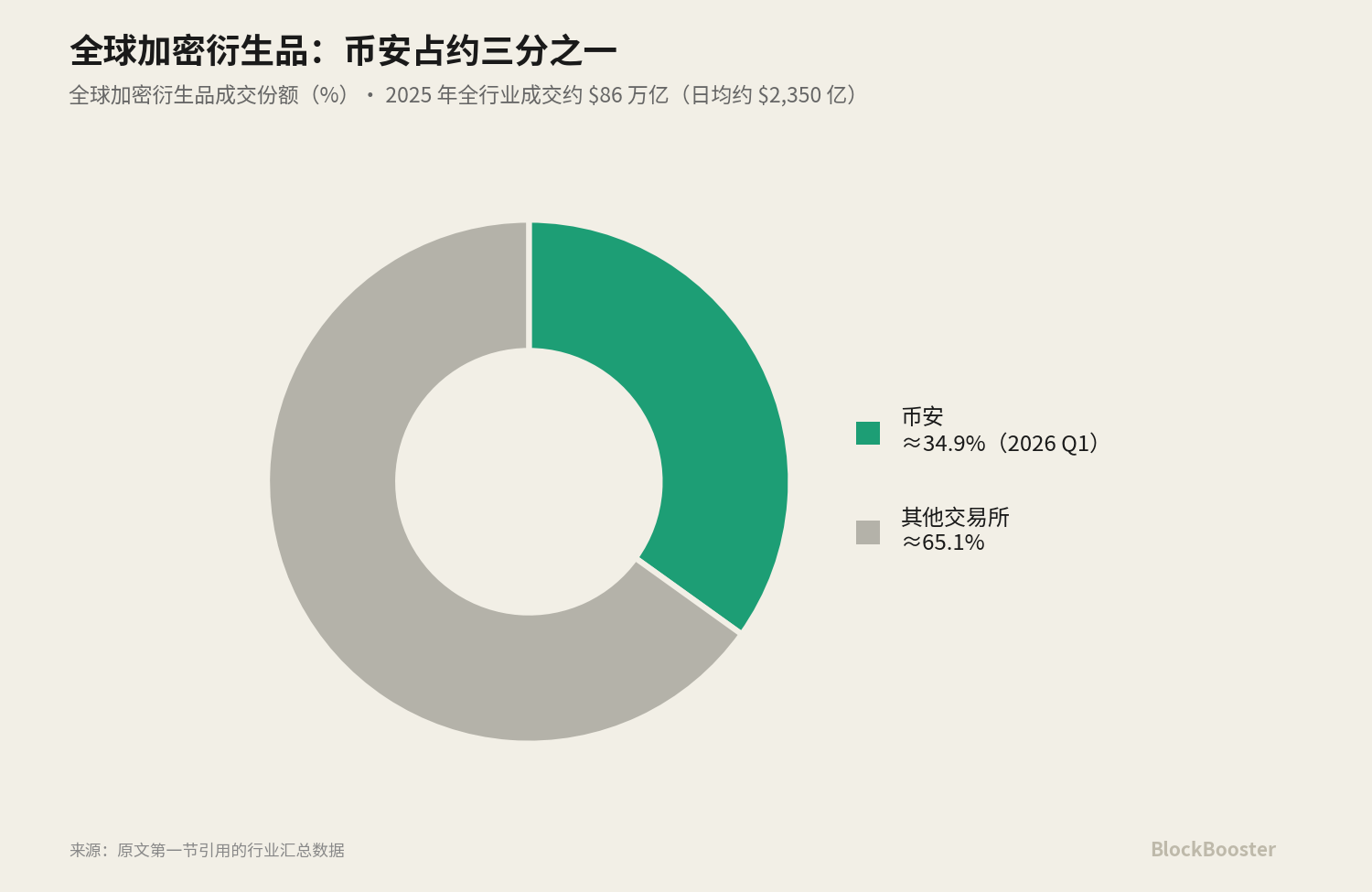

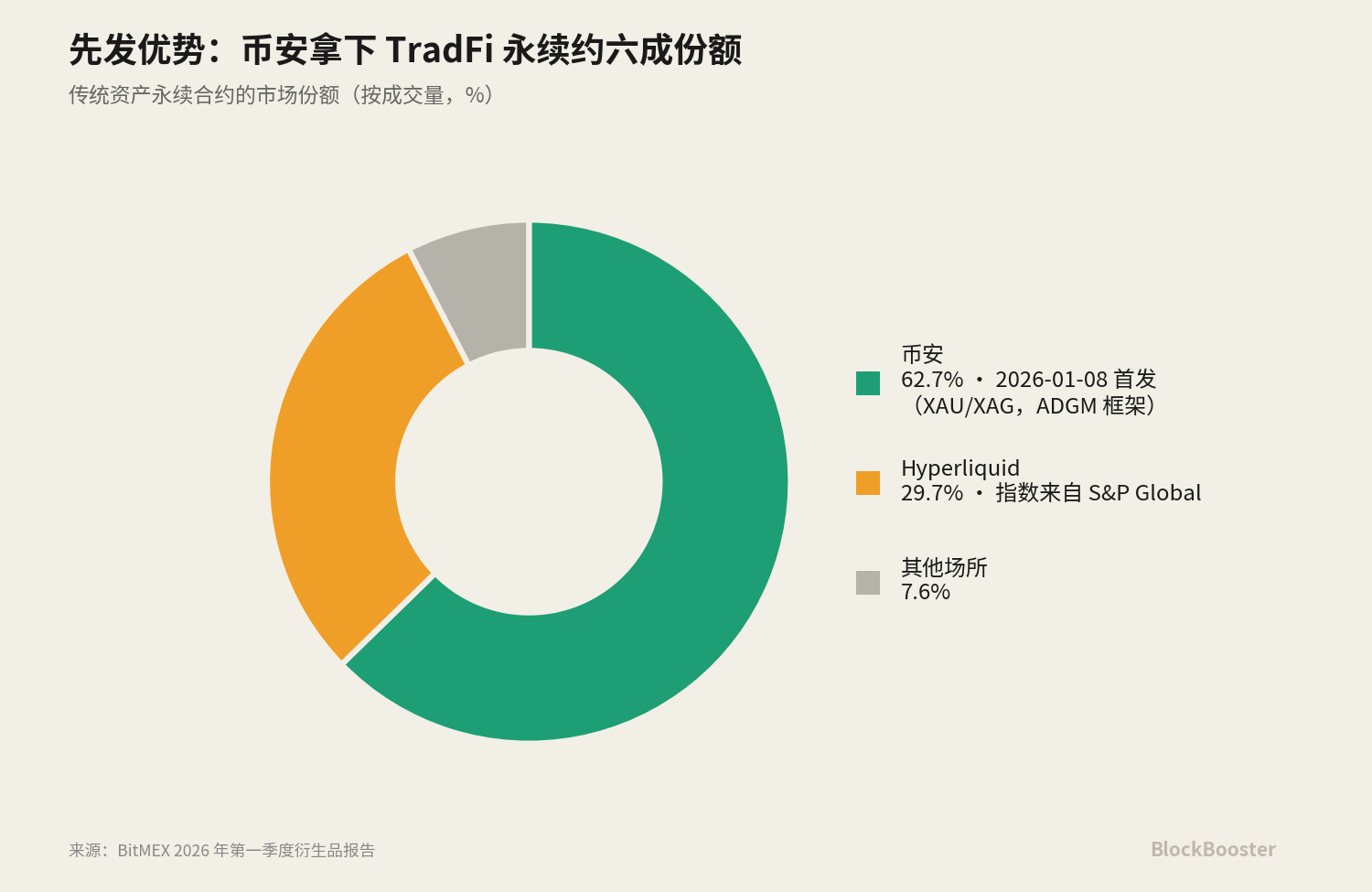

For the "traditional asset perpetuals" track, Binance listed TradFi perpetual contracts on January 8, 2026, starting with gold (XAUUSDT) and silver (XAGUSDT). Leveraging its first-mover advantage, Binance captured roughly 62.7% of the TradFi perpetual market share, with Hyperliquid following at 29.7%.

Hyperliquid's index data for these traditional asset perpetuals comes from its partnership with S&P Global. This collaboration—linking crypto perpetuals directly to traditional indices—is drawing regulatory scrutiny from the US CFTC.

Meanwhile, Ethena's USDe market cap was in the range of approximately $4.5 billion to $5.9 billion in early June 2026.

Each of these products quotes a "rate" or "yield"—perpetuals have funding rates, lending protocols have lending APRs, sUSDe has a staking yield, and tokenized treasuries have coupons. Yet, crypto still lacks its own SOFR. There is no widely accepted benchmark curve that can serve as an anchor for pricing. Every exchange and every protocol becomes a micro financing market, quoting its own price, yet without a public, trusted reference system between them.

2. What Qualifies as a Crypto "Base Rate"?

Let's first look at three different sets of rate comparisons:

- **Set 1: Base Funding Rate vs. Product Yield vs. Derivatives Implied Rate.** The APY of sUSDe is a product yield—the return to holders. The perpetual funding rate is a derivatives implied rate—the fee paid between longs and shorts to keep the perpetual price anchored to the spot price. A benchmark funding rate, however, should be a public reference that countless other products can cite for pricing. **Product yields and derivatives implied rates are not benchmarks—they are "downstream" of a benchmark**, resulting from stacking various premiums and structures on top of a base rate.

- **Set 2: Overnight Rate vs. Term Rate.** Perpetual funding rates settle every 1 or 8 hours, which is essentially an overnight rate—it only reflects the cost of capital "from now until the next settlement point" without a term structure. It cannot tell you the price difference between "borrowing for 30 days" and "borrowing for 90 days." Just as SOFR itself is an overnight rate and relies on the futures market to construct a Term SOFR with a term structure, **a rate without a term structure cannot support any medium to long-term fixed-income market.**

- Set 3: Real Lending Rate vs. Algorithmic/Implied Rate. Real bilateral lending transactions (e.g., Bitfinex's margin funding book, where real lenders and borrowers are matched) and algorithmic utilization pricing (e.g., Aave, where the rate is automatically calculated by the pool's utilization via a formula) are two fundamentally different price generation mechanisms. The former is voted on by market participants with real money; the latter is a curve written into the code by the protocol designer.

From these three distinctions, we can extract the criteria a "qualified benchmark" should meet:

Based on real transactions, underlying market is sufficiently broad and deep (hard to be manipulated by a single participant), independent governance (no conflict of interest between the administrator and the market being priced), and ideally possesses a term structure (to support medium and long-term pricing).

(SOFR's underlying is real overnight repo transactions collateralized by US Treasuries, with average daily volume "often exceeding $1 trillion." This is the real trading volume of overnight repos, distinct from the notional volume of SOFR futures supporting Term SOFR.)

Applying SOFR's logic to crypto reveals structural isomorphism. The Bank for International Settlements, in its research, likens the on-chain collateralized lending market to a "crypto-native money market," whose operational mechanism is similar to traditional tri-party repos—over-collateralized, marked-to-market, and overnight rollover. Since on-chain lending is structurally a repo-style secured financing, using SOFR's design—a benchmark built on real repo transactions—to evaluate a crypto benchmark is an appropriate isomorphic reference.

3. What are SOFR's Characteristics? Why was LIBOR Discontinued?

LIBOR (London Interbank Offered Rate) was once the cornerstone of global finance. At its peak, approximately $300 trillion in financial contracts (including interest rate swaps, mortgages, student loans, corporate bonds, etc.) relied on LIBOR across five currency zones. However, LIBOR had a fatal design flaw: it was not based on real transactions, but on daily "self-reported" estimates of borrowing costs from a small panel of banks.

This flaw was fully exposed after the 2008 financial crisis. Regulatory investigations revealed that traders at several major global banks systematically manipulated LIBOR quotes to benefit their own derivatives positions.

The manipulation scandal directly led to LIBOR's abolition.

Its replacement is SOFR (Secured Overnight Financing Rate). SOFR's design is almost a "reverse engineering" of every LIBOR flaw: It uses no self-reported estimates but is based on real transactions in the US Treasury repo market. It takes the volume-weighted median of transactions from three repo markets (tri-party repo, GCF repo, and bilateral repo cleared through FICC's DVP service), a broad and deep gauge that is hard for any single participant to manipulate. It is administered by the New York Fed, adhering to IOSCO benchmark principles, ensuring no conflict of interest between the administrator and the priced market.

However, SOFR has an "inherent shortcoming": it is an overnight rate with no term structure. The market needs not only "today's overnight cost" but also the "expected cost of funding over the next three months" to price medium and long-term loans. Thus, CME launched CME Term SOFR—a set of forward-looking rates covering four tenors: 1-month, 3-month, 6-month, and 12-month.

It uses trading data from SOFR futures to infer the market's expectation of the future SOFR path, thereby constructing a forward-looking term curve. (The representative notional volume of SOFR futures used to construct Term SOFR was approximately $2.3 trillion per day in Q4 2023.)

4. Discussing Some Candidate Rates

Many candidates are currently being referred to as "rates" or "yields" in the market. Let's break them down one by one to discuss why some are clearly unsuitable as benchmark rates and which may have room for evolution.

A key theme running through all analyses is—"who has the power to decide": is it market weighting, algorithmic utilization, or governance setting?

4.1 Perpetual Funding Rate (Hyperliquid / Binance)

The perpetual funding rate is the implied price of leverage, driven by the basis between the spot and perpetual prices: essentially an overnight rate, with no term structure.

When the spot market for TradFi underlying assets is closed (e.g., stocks, precious metals on weekends), exchanges cannot obtain a real spot price to calculate the funding rate. Binance freezes the index price at the last spot price and uses an EWMA mark price with a ±3% cap. Hyperliquid also switches to EWMA on weekends with volatility caps per product. During closed market hours, the "anchor" for the perpetual price is actually a predicted value, not a real transaction price. When the market reopens and the real price gaps beyond this cap, it triggers limit-up/limit-down situations. Therefore, prices during closed market hours are predictions, not real, arbitrageable anchors.

On May 29, 2026, the US CFTC approved KalshiEX's Bitcoin perpetual contract (BTCPERP), the first truly non-expiring regulated Bitcoin perpetual in the US. Concurrently, it issued a policy statement on perpetual contracts, a staff guidance on 24/7 trading and clearing, and a no-action position regarding Coinbase offering perpetuals through Deribit. The significance is that a regulated, centrally cleared perpetual means its funding rate and basis are generated in a compliant environment with clearing safeguards—positioning it as a potential future candidate for a "crypto SOFR." This, along with the CFTC's scrutiny of the Hyperliquid–S&P Global index partnership, forms a signal that "regulation is approaching crypto benchmarks."

4.2 Bitfinex Margin Funding + FRR

This is crypto's native USD term funding market.

Here's the mechanism: Bitfinex operates a peer-to-peer margin funding market where lenders lend funds to margin traders to earn interest. The key design feature is that funding durations range from 2 to 120 days (common: 2, 7, 30 days), and matching requires both the rate and duration to align. This means Bitfinex's funding book naturally constitutes a real lending curve from the short to the long end: 30-day money and 120-day money have different prices, determined by real supply and demand matching. It is one of the very few markets in the crypto world that inherently possesses a term structure.

The FRR (Flash Return Rate) is the reference rate for this market. FRR is the average rate of all active fixed-rate funding weighted by their size, updated hourly. Essentially, it is a "Bitfinex version benchmark reference rate"—an index reflecting the current average market borrowing cost. Lenders can choose to lend at the FRR, allowing their rate to automatically track the market.

Bitfinex charges lenders approximately 15% of the lending revenue (18% for hidden orders). The minimum order is $150. FRR is quoted as a daily rate, annualized: Bitfinex USD FRR is approximately 0.0136%/day, annualized around 5.1%—comparable to tokenized treasuries, Aave, SSR, and other candidates.

Its crucial characteristic is its volatility: USD lending rates have historically fluctuated wildly, roughly between 3%–20% APR, strongly correlated with leverage demand.

This daily rate curve unfolds across different tenors from 2 to 120 days, forming a native USD funding curve with a real term structure in crypto.

Bitfinex and Tether are under the same parent company, iFinex, with overlapping management. This gives Bitfinex the deepest USDT liquidity in the entire crypto world—one reason its funding market is so deep. However, it also concentrates counterparty risk and stablecoin issuer risk within the same entity. Borrowing Bitfinex money, using Bitfinex matching, denominated in Tether, with the same parent company backstopping in extreme scenarios—this is a highly self-contained structure.

Although Bitfinex's funding market is the oldest and deepest native USD term funding market in crypto, its absolute size (stock of funding offers and daily matching volume) is still much smaller compared to the trillions of dollars in perpetual trading volume mentioned earlier.

Comparing FRR with LIBOR and SOFR, on the dimension of "being based on real transactions," FRR is actually cleaner than LIBOR. FRR is calculated from real, executed fixed-rate funding weighted by size; it reflects genuine market behavior. However, FRR comes from a single exchange's order book (concentration), is operated by the same parent company iFinex that controls the largest stablecoin Tether (conflict of interest), and this operator is also the lender of last resort for existing positions in this market (further concentration and conflict). Therefore, FRR hits on the concentration and conflict of interest issues that SOFR was designed to eliminate.

4.3 DeFi Lending Rates (Aave / Morpho)

This represents algorithmic utilization pricing: the rate is not determined by bilateral matching but automatically calculated from the pool's utilization via a preset formula—the higher the utilization, the higher the rate. It fluctuates in real-time with borrowing demand.

Aave's mainnet USDC deposit rate fluctuates between roughly 3.5%–6% depending on utilization. Morpho's curated USDC vaults offer around 5%–7% after curator fees.

4.4 MakerDAO / Sky Savings Rate (DAI's DSR / USDS's SSR)

This is a "policy-like rate" directly set by protocol governance. DAI's DSR (Dai Savings Rate) and USDS's SSR (Sky Savings Rate) are widely cited and function similarly to a central bank's policy rate—not determined by market matching or algorithmic utilization triggers, but by Sky's governance vote.

The governance-set DSR/SSR, market-weighted FRR, and Aave's algorithmic utilization represent a stark contrast among three different rate generation mechanisms.

Governance setting vs. market weighting vs. algorithmic utilization—each mechanism has its own credibility issues and manipulation risks. A mature market benchmark should ideally come from the one least susceptible to manipulation (market-weighted real transactions with sufficient breadth and depth). In terms of current value, SSR was lowered by governance from 4.75% at the end of April 2026 to approximately 3.6%–3.75% by early June (the "governance setting" mechanism moves with the Fed's path). USDS circulating supply is around $11 billion.

4.5 Tokenized Treasury Yields (BUIDL / BENJI, etc.)

This is the ~4–5% "risk-free leg," a candidate for the "crypto risk-free benchmark." BlackRock's BUIDL, Franklin Templeton's BENJI, etc., bring US Treasury coupon yields on-chain. In terms of current value, major tokenized treasury tokens (BUIDL, USDY, USDM, USYC, etc.) were paying approximately 4.1%–4.7% APY in April 2026, closely tracking the 3-month Treasury yield. Its yield can almost directly proxy the traditional risk-free rate.

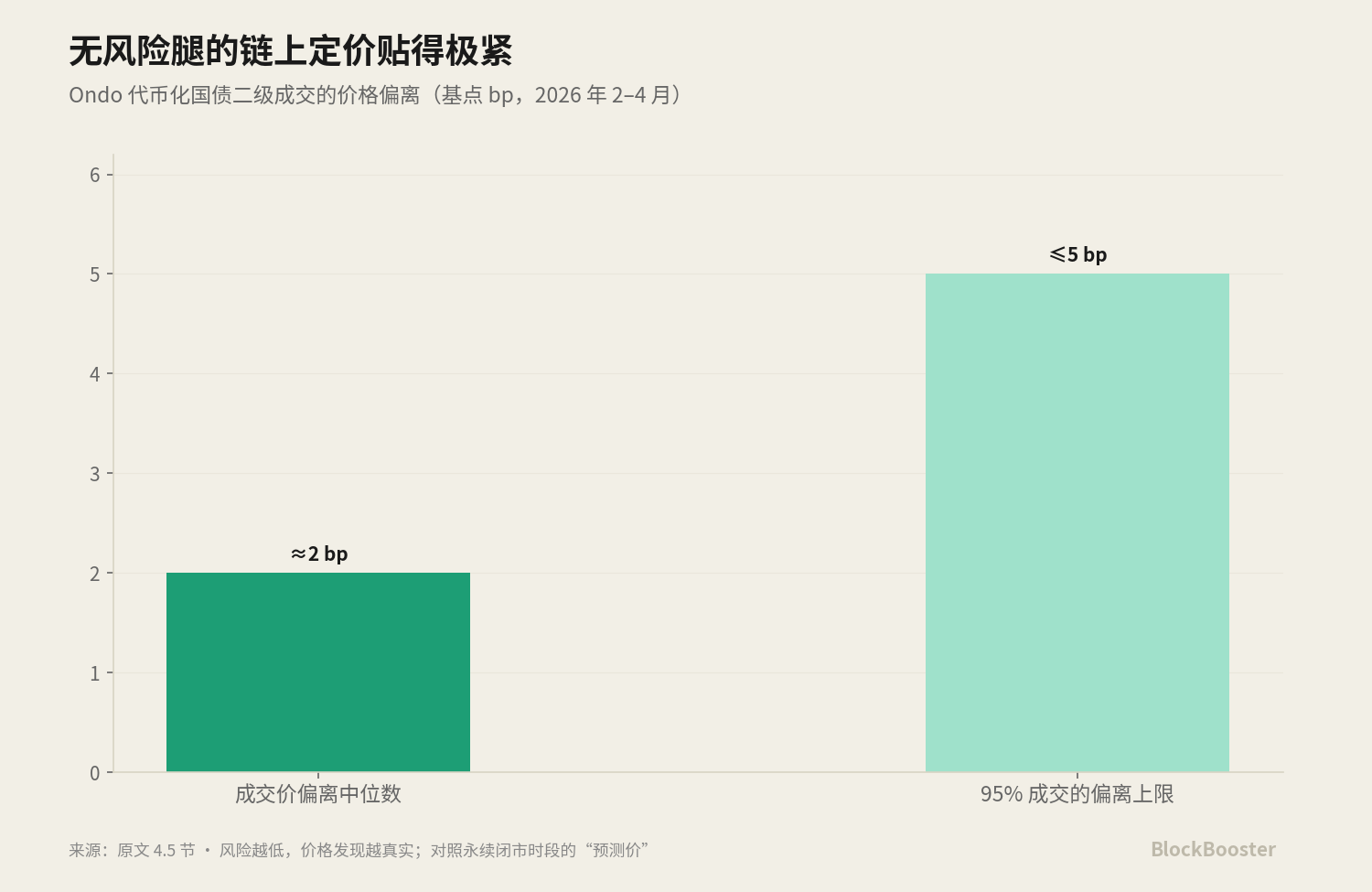

The secondary market pricing for this "risk-free leg" of tokenized treasuries is very tight. For example, with Ondo's tokenized treasury, between February and April 2026, the deviation of its transaction prices from the median was only about 2 basis points, with 95% of transactions falling within 5 basis points. This shows that when the underlying asset is sufficiently standard and risk-free, on-chain price discovery can be very precise. In contrast, the "prices" of high-risk varieties like perpetuals during closed market hours are full of speculative components—the lower the risk, the more real the price; the higher the risk, the more the pricing resembles guesswork.

4.6 Ethena sUSDe

This is a securitized product of perpetual funding rates plus collateral yield. Its APY is highly dependent on the funding rate levels in the perpetual market. Therefore, it is essentially a repackaging of implied rates, not the benchmark itself.

Putting the seven candidates together: they measure different things (leverage sentiment, real lending, algorithmic utilization, governance policy, risk-free coupon, institutional arbitrage), each embedded with different risks (liquidation, counterparty, smart contract, governance, credit), and priced by different entities.

None simultaneously meets the three conditions of "broad gauge + term structure + independent governance."

This is the current state of the crypto benchmark