CLARITY Bill Reshapes the Stablecoin Yield Economy

- Core Thesis: The U.S. CLARITY Act, having passed the Senate Banking Committee, extends the stablecoin yield ban to all digital asset service providers and introduces a legal dichotomy between "passive yield vs. activity-based rewards," compelling the industry to shift from "holding for yield" to "usage for yield." Wall Street asset management giants (Morgan Stanley, BlackRock, JPMorgan Chase) are simultaneously positioning tokenized money market funds to secure their role as the most robust compliant yield infrastructure under this new paradigm.

- Key Elements:

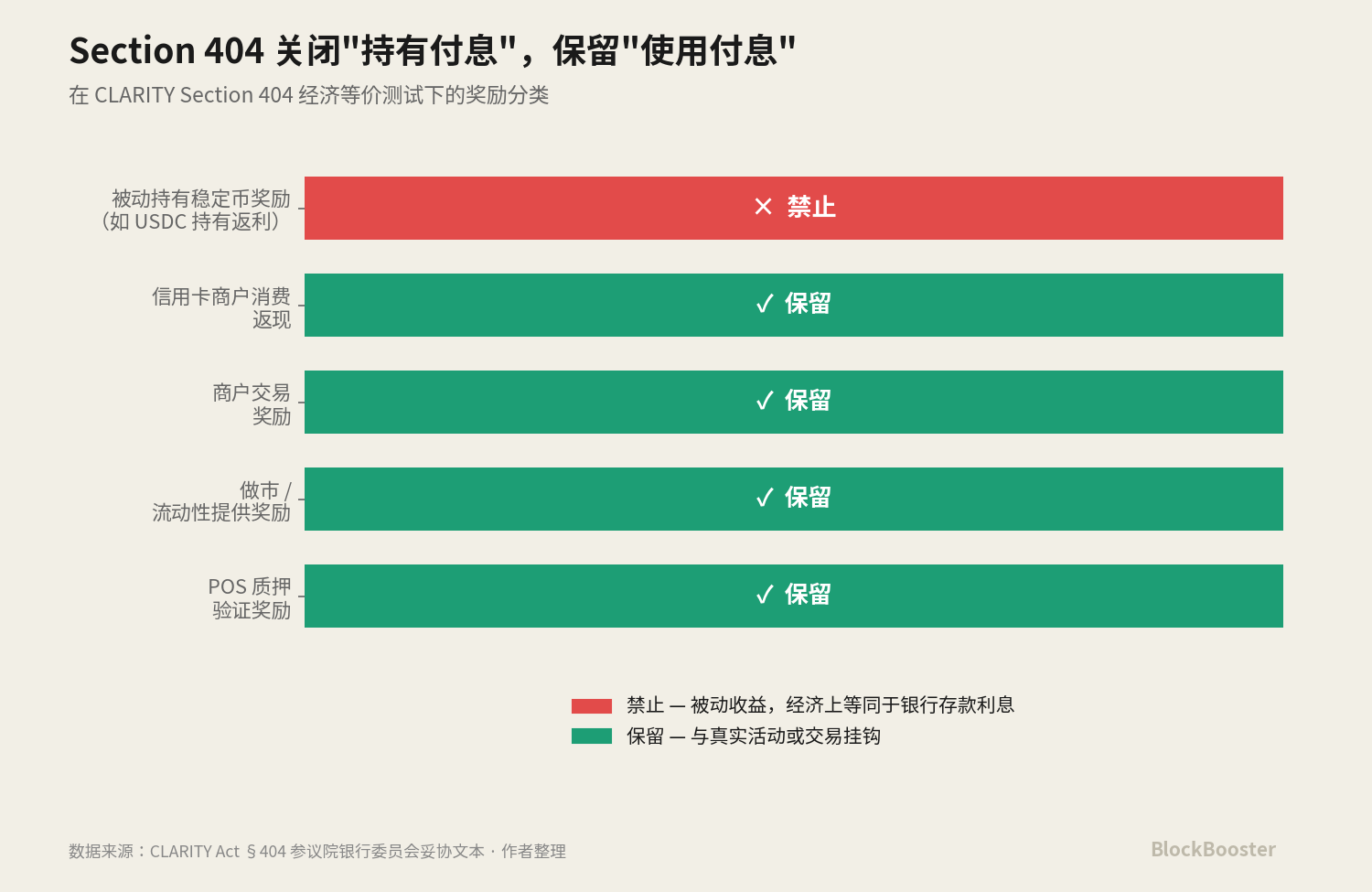

- Section 404 of the CLARITY Act accomplishes two critical things: extending the yield ban from stablecoin issuers to all DASPs (including exchanges, custodians, and their affiliates); and introducing the dichotomy of "passive yield" versus "activity-based rewards," prohibiting interest solely based on holding but preserving rewards tied to genuine activities like staking and trading.

- The Act closes compliance workarounds such as Coinbase's subscription model and Anchorage's affiliate structures for "indirect yield payments," forcing the industry to restructure its yield models.

- Within 28 days prior to the Act's passage, Morgan Stanley (MSNXX), BlackRock (BSTBL/BRSRV), and JPMorgan Chase (JLTXX) nearly simultaneously filed for tokenized money market funds specifically designed for stablecoin reserve needs, indicating market expectations have already realigned around the new paradigm.

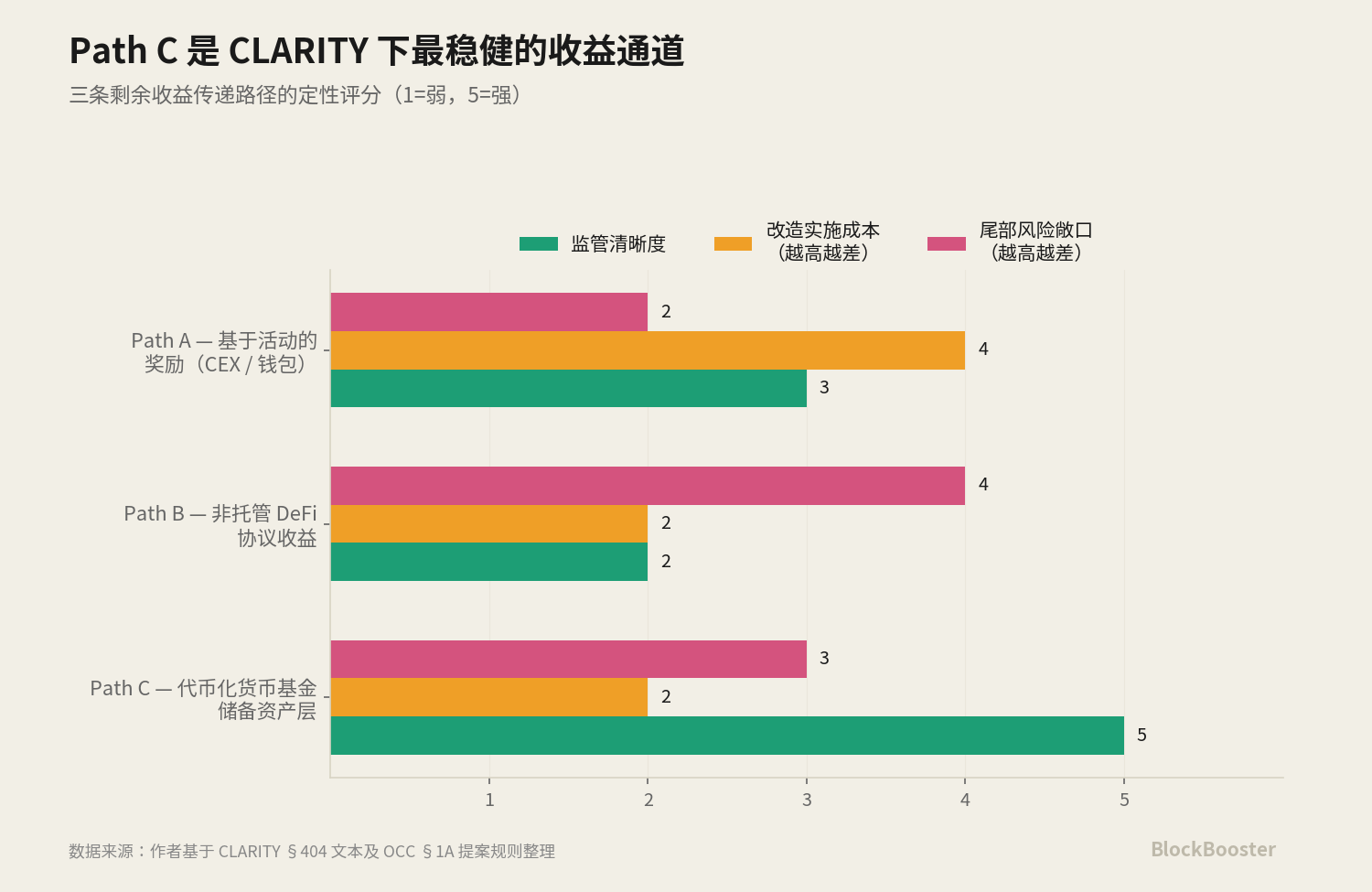

- Under the new paradigm, three pathways for yield transmission exist: Path A (exchanges redesigning activity rewards), Path B (non-custodial yield at the DeFi protocol layer), and Path C (tokenized money market funds paying yield as reserve assets), with Path C facing the most minor direct regulatory threat and offering the strongest risk-adjusted appeal.

- The OCC's proposed "20% cap on tokenized reserve assets" is the key determinant for Path C's scalability. The CLARITY Act grants legal status to tokenized securities, weakening the OCC's rationale for the restriction, which may lead to the cap being loosened.

- BlackRock has constructed a three-tier product matrix (BUIDL, BSTBL, BRSRV) covering DeFi collateral, traditional institutional cash management, and stablecoin reserve assets, forming a complete ecosystem.

- Concentration risk is prominent in BUIDL: a single fund backs approximately 90% of USDtb reserves and about 81% of JupUSD reserves. Should the OCC cap be relaxed, this single point of failure risk will be amplified, potentially triggering systemic risks.

Original author: @BlazingKevin_, Blockbooster Researcher

On May 14, 2026, the U.S. Senate Banking Committee passed the CLARITY Act with a bipartisan vote of 15-9.

The most important content in this "legislative progress" is Section 404 of the bill text. This section, redrafted in a compromise text released on May 1 by Senators Thom Tillis and Angela Alsobrooks, does two things that the GENIUS Act did not:

First, it expands the stablecoin yield prohibition to all Digital Asset Service Providers (DASPs) and their affiliated parties—including centralized exchanges, brokers, dealers, and custodians. When the GENIUS Act was signed in July 2025, it only constrained "stablecoin issuers" (PPSI/FPSI). The compliance workarounds used by Coinbase, Anchorage Digital Neo Ltd., etc.—providing 3.5%-5% yields to users via a "non-issuer interest payment" path—are all shut down by Section 404.

Second, it explicitly introduces the legal dichotomy of "passive yield vs. activity-based rewards". Section 404 prohibits rewards that are "functionally or economically equivalent to bank deposit interest"—i.e., yield that accrues automatically based solely on holding—but preserves rewards based on "real activity or transactions," such as staking, market making, credit card cashback, and merchant transaction rewards.

Together, these two changes constitute a paradigm shift. The stablecoin industry is moving from a market where holding earns yield to one where usage earns yield.

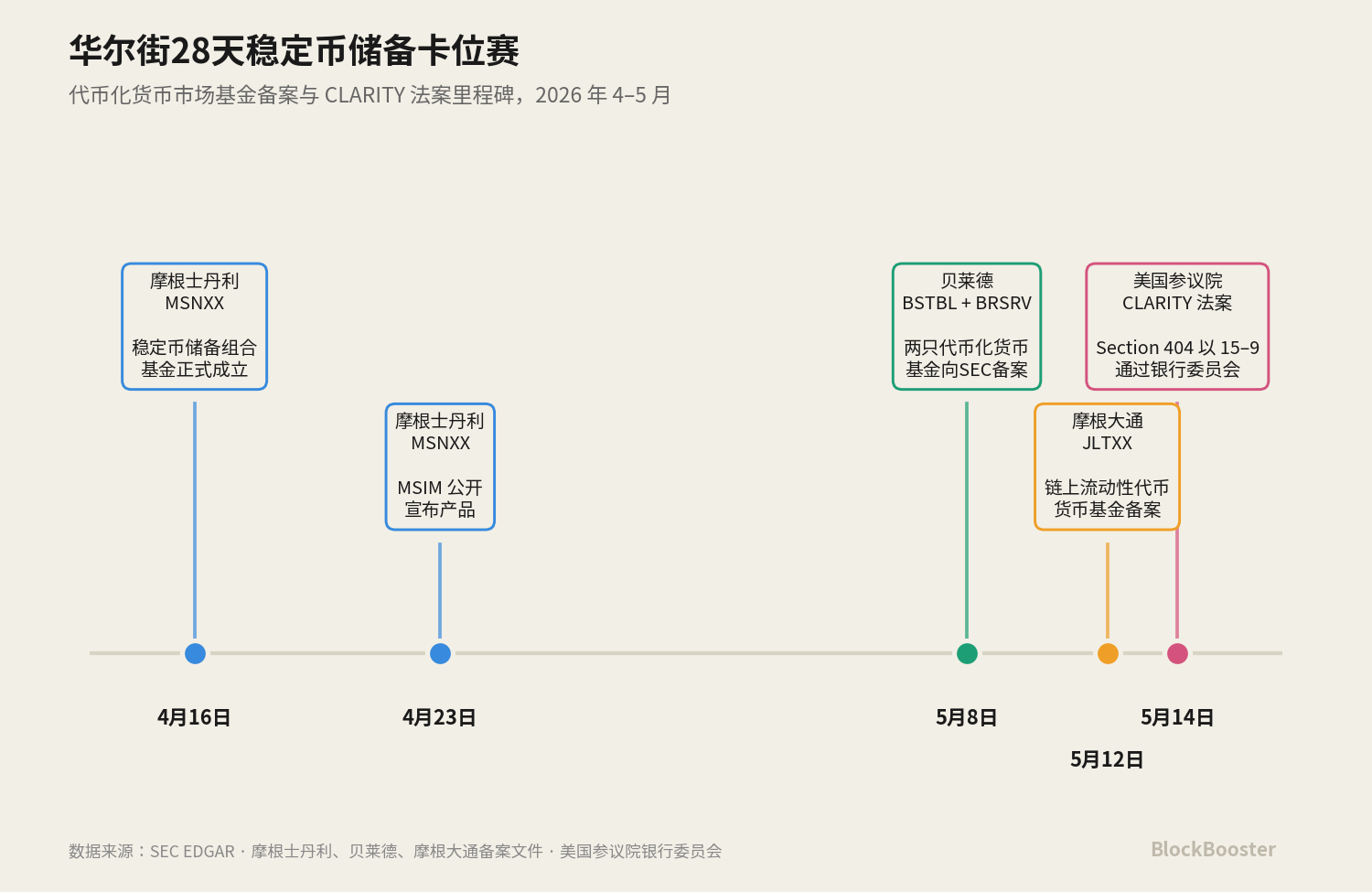

Meanwhile, over the past month, the three largest asset management firms on Wall Street (Morgan Stanley, BlackRock, JPMorgan) have almost simultaneously launched money market fund products tailored for stablecoin reserve requirements. Morgan Stanley's MSNXX was established on April 16 and publicly announced on April 23; BlackRock filed for two tokenized funds, BSTBL and BRSRV, on May 8; JPMorgan filed for JLTXX on May 12. All three launched highly similar products within a 28-day window.

This timing is certainly no coincidence. We believe: The expectation that CLARITY Section 404 will soon pass is pushing the stablecoin yield economy towards a new paradigm—the hold-to-earn path is narrowing, the use-to-earn path is preserved, and tokenized money market funds, serving as compliant yield-bearing instruments for stablecoin reserves, become the most robustly benefiting compliant yield layer in this new paradigm.

The products concentratedly filed by Wall Street asset management giants in April-May represent an industrial positioning for this paradigm shift. It's important to clarify: CLARITY has currently only passed the Senate Banking Committee; there is still some distance from the President's signature, but market expectations are already reorganizing in this direction.

This article will start by reconstructing the timeline, deconstructing the relay of legal structures between GENIUS and CLARITY, and analyze why the tokenized reserve asset layer emerges as the most robust compliant yield channel in the new paradigm.

1. 30 Days of Industrial Positioning

1.1 April 16: Morgan Stanley's Opening Move

Let's go back to the earliest event first.

On April 16, 2026, Morgan Stanley's Stablecoin Reserves Portfolio (ticker: MSNXX) was officially established.

MSIM publicly announced this product on April 23.

MSNXX's product positioning is very precise. The official statement reads: "The Fund offers compliant stablecoin issuers a qualified money market fund option to invest the reserve assets needed to back their circulating stablecoins."

MSNXX is a product tailored for reserve asset requirements—investing in cash, U.S. Treasury securities with maturities of 93 days or less, and overnight repurchase agreements collateralized by Treasuries.

However, MSNXX is not a tokenized product and does not trade on-chain. Morgan Stanley's product strategy is conservative—offering only a traditional MMF wrapper for stablecoin issuers to invest through traditional financial channels.

This is the first publicly announced product "specifically designed for stablecoin reserve needs" among Wall Street asset management giants. It isn't revolutionary in itself, but it sends a clear signal: the demand for stablecoin reserves has grown large enough that asset managers are willing to create a dedicated fund for it.

1.2 May 8: BlackRock's "Dual Filing"

22 days later, BlackRock filed two registration statements with the SEC simultaneously: the BlackRock Select Treasury Based Liquidity Fund tokenized version (BSTBL) and the BlackRock Daily Reinvestment Stablecoin Reserve Vehicle (BRSRV).

The design of these two products contrasts sharply with MSNXX. BSTBL is a tokenized version of BlackRock's existing Select Treasury Based Liquidity Fund, serving traditional institutional cash managers—clients who already invest in this fund, now with an additional on-chain distribution channel.

BRSRV, on the other hand, is a newly created tokenized money market fund, distributed across multiple chains by Securitize, targeting a single customer group: stablecoin issuers.

The key difference between BlackRock and Morgan Stanley lies in tokenization. BlackRock chose to issue on-chain shares of the same underlying assets (short-term Treasuries + cash + overnight repos) to stablecoin issuers, granting the reserve assets themselves on-chain composability, 24/7 transferability, and integration potential with DeFi protocols. This is a product form tailored for crypto-native clients like Ethena, Jupiter.

The BSTBL + BRSRV filing expands BlackRock's existing product matrix, extending the tokenization infrastructure from BUIDL's "DeFi collateral" use case to BRSRV's "stablecoin reserve asset" use case.

1.3 May 12: JPMorgan's Second Entry

Four days later, JPMorgan filed a registration with the SEC for the JPMorgan OnChain Liquidity-Token Money Market Fund (JLTXX).

The fund itself invests in U.S. Treasury securities and overnight repurchase agreements collateralized by Treasuries or cash, with underlying assets identical to BUIDL, BSTBL, and BRSRV. The Token Class Shares are dated May 13.

LTXX is not JPMorgan's first on-chain MMF. As early as December 15, 2025, JPMorgan Asset Management had already launched My OnChain Net Yield Fund (MONY) on Ethereum. MONY is a 506(c) private fund, open only to qualified investors.

This means JPMorgan already has nearly 5 months of operational experience in the tokenized MMF track. JLTXX is not a catch-up product but JPMorgan's second step in its on-chain MMF strategy—extending a product previously limited to 506(c) qualified investors into a registered fund accessible to a broader client base, specifically targeting the stablecoin reserve use case.

On one hand, JPMorgan explored issuing a joint syndicated stablecoin with Bank of America, Wells Fargo, and Citigroup in 2025; on the other, it deeply positioned itself in the tokenized reserve asset track through the MONY → JLTXX product matrix. Whatever the OCC ultimately decides, JPMorgan has a product in place—this "betting on both sides" reflects JPMorgan's unique strategic space as a GSIB bank and asset manager.

1.4 May 14: CLARITY Act Stamps the Entire Track

On May 14, the Senate Banking Committee passed the CLARITY Act with a bipartisan vote of 15-9.

It's worth noting carefully: Morgan Stanley's MSNXX, BlackRock's BSTBL/BRSRV, and JPMorgan's JLTXX—these products were all prepared before the CLARITY Section 404 compromise text was made public.

In fact, since CLARITY was first shelved in January 2026, the asset management industry has been clear on two things: First, the "hold-to-earn" stablecoin reward path would eventually be closed. Second, stablecoin reserve assets must exist, must be compliant, and will inevitably bear yield.

Combining these two points: When the hold-to-earn path narrows, one of the most robust "indirect yield" transmission routes is through the reserve asset layer—the stablecoin issuer itself doesn't pay yield, but its reserves held in tokenized money market funds legally pay yield to the issuer, who then decides how to pass this yield on to users within a compliant framework.

The asset management giants' products are the infrastructure prepared for this "most robust compliant yield channel."

2. Why CLARITY is Much More Important Than GENIUS

2.1 The Limited Scope of the GENIUS Act

To understand the paradigm-shifting effect of Section 404, one must first precisely understand what it expands upon—Section 4(a)(11) of the GENIUS Act.

The GENIUS Act, signed into law in July 2025, stipulates that a compliant stablecoin issuer or foreign stablecoin issuer shall not pay any form of interest or yield to stablecoin holders.

This means the GENIUS Act itself does not distinguish between "passive yield" and "activity-based rewards." All forms of interest or yield paid by the issuer to the holder are prohibited.

Second, its constraint applies only to the issuer itself, not including third parties like exchanges, wallets, custodians, or affiliated entities.

This second limitation created a regulatory loophole—what the industry calls "pass-through evasion." The entire stablecoin industry in 2025-2026 was essentially seeking compliant innovation space within this loophole:

- Coinbase / Kraken Model: Exchanges distribute rewards. USDC is issued by Circle, but Coinbase provides approximately 4% rewards to USDC holders through the Coinbase One subscription model.

- Gemini Credit Card Model: Rewards triggered via external merchant transactions. GUSD is issued by Gemini Trust Company, but Gemini credit card holders receive GUSD cashback when spending at merchants.

- Anchorage Digital Neo Model: Rewards paid through an independent affiliated legal entity. USDtb is issued by Anchorage Digital Bank, but Anchorage Digital Neo Ltd. (a separate legal entity) pays the rewards.

These three models together formed the "indirect yield" ecology of the GENIUS era.

But the compliance basis for all this was the limited scope of the GENIUS Act constraining only the issuer.

2.2 The Substantive Expansion of CLARITY Section 404

CLARITY Act Section 404 does two things the GENIUS Act did not.

First: Expansion to DASPs and Affiliated Parties

The scope of Section 404 is no longer limited to stablecoin issuers but extends to "covered digital asset service providers and their affiliated parties." This scope explicitly covers centralized exchanges, brokers, dealers, and custodians.

This expansion immediately closes all the "non-issuer interest payment" compliance paths used by Coinbase, Kraken, Gemini, Anchorage Digital Neo, etc. Coinbase, as a DASP, can no longer distribute hold-only USDC rewards; Anchorage Digital Neo can no longer pay USDtb rewards.

Second: Introducing the "Passive vs. Activity" Dichotomy

Section 404 prohibits DASPs from providing rewards that are "functionally or economically equivalent to bank deposit interest" but preserves rewards based on "real activity or transactions."

This means any reward tied to "spending, trading, staking, or transferring" can survive, while any reward that grows linearly with an idle balance cannot.

Together, these two things constitute a complete paradigm shift. All the "indirect yield" templates of the GENIUS era are either shut down or require redesign in the CLARITY era.

The stablecoin industry is moving from a market where holding earns yield to one where usage earns yield.

2.3 Winning Paths in the Paradigm Shift

In the use-to-earn paradigm, there are three possible paths to pass yield to users.

Path A: Redesign rewards as activity-based rewards

Target: Exchanges, wallets, credit cards. Coinbase could change its USDC rewards from "hold-based" to "based on transaction frequency/consumption amount." Gemini is already using the credit card cashback model.

The key issue for Path A isn't whether it can retain users, but its design cost—Coinbase would need to restructure the entire legal framework and product UI of its reward system. Each active design would require a "facts and circumstances" test by the SEC/CFTC. This restructuring could take 6-12 months, during which user churn is a real risk. However, medium-term, Path A could potentially recover and even surpass the appeal of the hold-to-earn era.

Path B: Keep yield at the protocol layer, pass it to users via activity-based operations

Target: DeFi protocols. The definition of "covered digital asset service provider" in Section 404 is clearly built around centralized intermediaries—yield generated by non-custodial smart contracts, such as supplying USDC to Aave for variable rate lending, arguably falls outside this definition.

This means a user depositing USDC into the Aave lending pool to earn a variable rate is currently interpreted by most legal scholars as compliant—CLARITY seemingly inadvertently leaves a yield channel open for non-custodial DeFi.

However, this exemption carries significant uncertainty. If final rules extend the "economically equivalent" concept to non-custodial DeFi, or define DeFi frontends as affiliated parties, the exemption for Path B could be substantially narrowed.

Path C: Pay yield through the reserve asset layer

This is the path Wall Street asset management giants are betting on. Specific mechanism: The stablecoin issuer itself doesn't pay yield, DASPs don't pay yield, but the stablecoin's reserve asset is a tokenized money market fund. The fund legally pays yield to its holders (i.e., the stablecoin issuer). The stablecoin issuer receives the distributed yield from the fund and retains it as company profit—or partially passes it to users via designed active behavior rewards.

The key compliance advantage of this path: Its yield layer is not at the stablecoin layer, nor at the DASP layer, but at the underlying fund layer—unrelated to the stablecoin regulatory framework.

These three paths are not mutually exclusive; they will evolve simultaneously.

Path A may find new life with players like Coinbase who have retail brands and distribution channels;

Path B may receive an unexpected boost for protocols like Aave, Pendle (albeit with tail risk of regulatory tightening over the next 12 months);

Path C is the one least directly threatened by Section 404, but requires the OCC's 20% cap not being enacted as a prerequisite.

Path C is the "most robustly benefiting" compliant yield layer, but not the "sole beneficiary."

This is why Wall Street asset management giants concentratedly filed for tokenized money market funds in April-May. They are providing one piece of compliant yield infrastructure for the use-to-earn paradigm about to be finalized by CLARITY Section 404. Considering the implementation costs and regulatory uncertainties of Paths A and B, Path C offers the strongest risk-adjusted appeal—this is the industry judgment of the BlackRocks of the world.

2.4 The Collaborative Relationship Between Path B and Path C

There seems to be collaborative potential between Path B and Path C. A complete on-chain yield system could utilize both paths simultaneously:

- The reserve asset layer uses BUIDL—ensuring a source of compliant yield

- The user layer uses Aave lending or Pendle yield splitting—ensuring the "yield" perceived by the user originates from active operations

This two-layer structure, "BUIDL at the base, DeFi protocol on the surface," could theoretically build a use-to-earn system that is both compliant and user-friendly. BlackRock likely didn't specifically foresee Section 404 when launching BUIDL, but this product perfectly serves as the optimal base layer for the use-to-earn system under the new paradigm.

3. BlackRock's Three-Layer Product Matrix—Infrastructure Built for the New Paradigm

3.1 Three Products, Three Customer Groups

To understand BlackRock's strategy, its three tokenized fund products must be compared side-by-side:

BUIDL: Launched March 2024, natively built on Ethereum. Legal structure is a BVI fund, custody provided by Securitize.

Target Clients: DeFi protocols, crypto-native institutions, on-chain scenarios needing BUIDL as collateral