Is the storage cycle reaching its peak? Here's a 'fundamental psychological comfort' from Bank of America

- Core Viewpoint: BofA believes the recent pullback in global memory stocks stems from an overreaction by the market to risks such as Meta's orders, CXMT entering Apple's supply chain, and South Korea's capacity expansion – not a fundamental reversal. The industry remains in a strong cycle, but the trend will shift from broad-based gains to earnings validation and individual stock divergence.

- Key Factors:

- The market fears Meta leasing out computing power will cut memory orders, but BofA points out its demand for HBM, LPDDR5, and enterprise SSDs is still strengthening, viewing this more as an asset monetization move.

- BofA believes it's unlikely Apple will adopt CXMT DRAM on a large scale in the short term; its inclusion might be more of a bargaining chip for Apple against Samsung, SK Hynix, and other suppliers.

- South Korea's 800 trillion won expansion plan spans over a decade, making it difficult to create effective supply in the short term, and thus cannot yet be cited as evidence of a cycle peak.

- Supply chain surveys in Japan indicate DRAM and NAND prices are still expected to rise quarter-over-quarter in Q3 and Q4. The industry might face shortages into 2027, with manufacturers maintaining cautious capital expenditure.

- Capital expenditure from hyperscale cloud providers continues to grow. DRAM and NAND prices remain high, and demand for high-end memory in AI servers and data centers stays robust.

Original report: BofA Global Research - Global Memory Tech, July 2, 2026

Translation & Arrangement: DaiDai, MSX Maitong

Editor: Frank, MSX Maitong

Key Takeaways:

- Bank of America believes the recent concentrated pullback in memory stocks was primarily driven by risk narratives such as Meta's orders, CXMT entering Apple's supply chain, and Korea's capacity expansion, rather than a reversal of industry fundamentals;

- Meta offering data center or cloud services to external parties is more likely a move to monetize computing power and diversify its business, rather than a significant reduction in memory demand. Its demand for HBM, LPDDR5, and enterprise SSDs continues to grow;

- CXMT is unlikely to become a major DRAM supplier for Apple in the short term. Apple is more likely to use it as leverage for price negotiations with Samsung, SK Hynix, and Micron;

- Supply chain surveys in Japan indicate that DRAM and NAND prices are still expected to rise quarter-over-quarter in Q3 and Q4, with the industry potentially remaining in shortage through 2027. Manufacturer CapEx and wafer output remain relatively restrained;

- The memory industry is still in a strong cycle, but following significant increases in product prices and related stocks, future performance will depend more on earnings realization. Sector volatility and stock divergence may increase significantly;

Over the past week, global memory stocks have experienced a notable correction.

The market quickly found three seemingly plausible explanations for this decline: Meta's plan to sell some of its computing power to external parties, potentially indicating an oversupply of data centers constructed earlier; Apple evaluating CXMT's DRAM, which could disrupt the supply structure dominated by Samsung Electronics, SK Hynix, and Micron; and South Korea's announcement of another large-scale semiconductor cluster plan, further fueling concerns about future oversupply.

All three narratives point to the same conclusion: Demand may be peaking, supply is poised to expand, and the memory super-cycle may be nearing its end.

However, Bank of America's judgment in its latest "Global Memory Tech" report is quite the opposite.

From its perspective, while the aforementioned risks are not entirely non-existent, the market has significantly overestimated their impact on the short-term supply-demand balance. Cloud CapEx, Korean semiconductor exports, and spot and contract prices for DRAM and NAND have yet to show a directional reversal in the memory cycle.

What has genuinely changed is not that fundamentals have shifted from strong to weak, but that the industry, after experiencing substantial price increases and stock revaluation, has entered a new phase where fundamentals remain strong, but the difficulty of trading has increased significantly.

I. Analyzing the Market's Concerns: Are They Valid?

1. Meta Selling Computing Power ≠ Cutting Memory Orders

The market's concern over Meta stems from a seemingly logical deduction: If Meta begins opening its data centers or selling cloud services to external customers, does this mean the company previously purchased too many servers, and its internal business can no longer absorb the existing computing power?

If the answer is yes, demand for AI hardware like GPUs, HBM, server DRAM, and enterprise SSDs might subsequently decline.

However, citing feedback from the supply chain, Bank of America's report states that memory chip manufacturers believe Meta will continue to more aggressively adopt high-performance memory products like HBM, LPDDR5, and enterprise SSDs in its AI data centers. Therefore, market speculation about Meta leasing out previously over-invested AI servers or cloud infrastructure lacks sufficient basis.

Furthermore, some NAND controller chip and packaging substrate manufacturers actually indicated that Meta's chip and component orders are still strengthening. Thus, Meta opening its data centers to external customers is more likely an attempt at asset monetization and business diversification, rather than being forced to deal with severely excess computing capacity.

2. CXMT Entering Apple's Supply Chain: More Like a Bargaining Chip

Bank of America's report predicts that the probability of Apple adopting CXMT's DRAM on a large scale in the short term remains low.

Several constraints exist:

- Policy and Supply Chain Restrictions: Apple must consider US restrictions related to China's semiconductor industry and the associated compliance and supply chain risks;

- Technical Specifications: Apple has high requirements for mobile DRAM regarding transfer speed, power consumption, and reliability, including transfer speeds exceeding 10Gbps, low power consumption design around 1.1V, and ECC error correction capability. Whether CXMT can consistently and massively meet these requirements over the long term requires further validation;

- Intellectual Property Risks: Core DRAM patents have long been concentrated among leading manufacturers like Samsung, SK Hynix, and Micron. If Apple were to adopt products with insufficient patent coverage on a large scale, it could face potential lawsuits and supply disruption risks;

Theoretically, CXMT could compete for orders for the low-end iPhone 18e, but considering the scale of such models in the Chinese market, the actual procurement volume is expected to be limited.

Rather than truly restructuring its supply chain, Apple is more likely using this to enhance its bargaining power in contract price negotiations for the second half of 2026 or 2027. Therefore, this event is more likely to impact the pricing expectations of Samsung, SK Hynix, and Micron in the short term, rather than immediately changing the global DRAM supply-demand balance.

3. Large-Scale Expansion in South Korea ≠ Uncontrolled Short-Term Supply

Another recent concern stems from South Korea's new semiconductor industry cluster plan.

Some investors believe the South Korean government's plan to invest approximately 800 trillion won in a new memory fab cluster in the southwestern region might indicate the memory cycle is nearing its peak. However, Bank of America's report dismisses this and predicts that the project will be difficult to generate significant effective supply before the early 2030s. Currently, priority must still be given to the expansion of the Yongin and Pyeongtaek clusters from 2026 to 2035.

Therefore, an industrial plan spanning over a decade cannot be directly equated with uncontrolled supply in the next two to three years. Long-term capacity expansion warrants continuous tracking but is not yet a direct basis for judging the peak of the current memory cycle.

4. Japan Supply Chain Surveys Remain Relatively Optimistic

Bank of America's recent supply chain survey in Japan also reinforces an optimistic outlook for the memory industry.

Japanese investors generally acknowledge the current industry prosperity. However, with the rapid price increases of products and related stocks, the market is also paying more attention to the potential downside cycle. Compared to investors' caution, management across the supply chain remains relatively positive:

- Q2 memory ASPs performed strongly, especially for NAND;

- Q3 and Q4 ASPs are expected to be higher than Q2;

- DRAM and NAND may remain in shortage in 2027;

- The number of Long-Term Supply Agreements (LTSAs) is increasing, but they mainly focus on volume commitments;

- CapEx and wafer output remain restrained, particularly among Japanese NAND manufacturers;

This means that although the market has started to discuss the next supply cycle early, based on actual manufacturer expansion and customer procurement behavior, the industry has not yet entered a phase of obvious uncontrolled supply.

5. Samsung's Memory Business May Still Exceed Expectations

In a report published on July 2, Bank of America predicted that due to special bonus expenses and margin pressure in the smartphone business, Samsung Electronics' overall Q2 operating profit might slightly miss the market's more optimistic expectations. However, driven by strong average selling prices (ASPs) for DRAM and NAND, the memory business's standalone operating profit was still expected to exceed market expectations.

Five days after the report, on July 7, Samsung announced its preliminary Q2 results: consolidated sales of approximately 171 trillion won and operating profit of approximately 89.4 trillion won, representing year-over-year increases of 129.3% and 1810.3%, respectively. The operating profit exceeded the market's prior estimate of around 86 trillion won, meaning Bank of America's judgment that the group's overall profit might slightly miss optimistic expectations did not materialize.

However, Samsung's disclosure only covers group-level preliminary results. Detailed profit figures for memory, foundry, and mobile businesses have not yet been released. Whether the memory division alone exceeded expectations awaits confirmation in the full financial report. Considering the Q2 price increases for DRAM and NAND, along with significant growth in South Korean semiconductor exports, the memory business is highly likely the core driver of Samsung's profit surge this cycle.

II. What Do Export Data, ASPs, and Product Prices Signal?

1. Surge in South Korean Semiconductor Exports

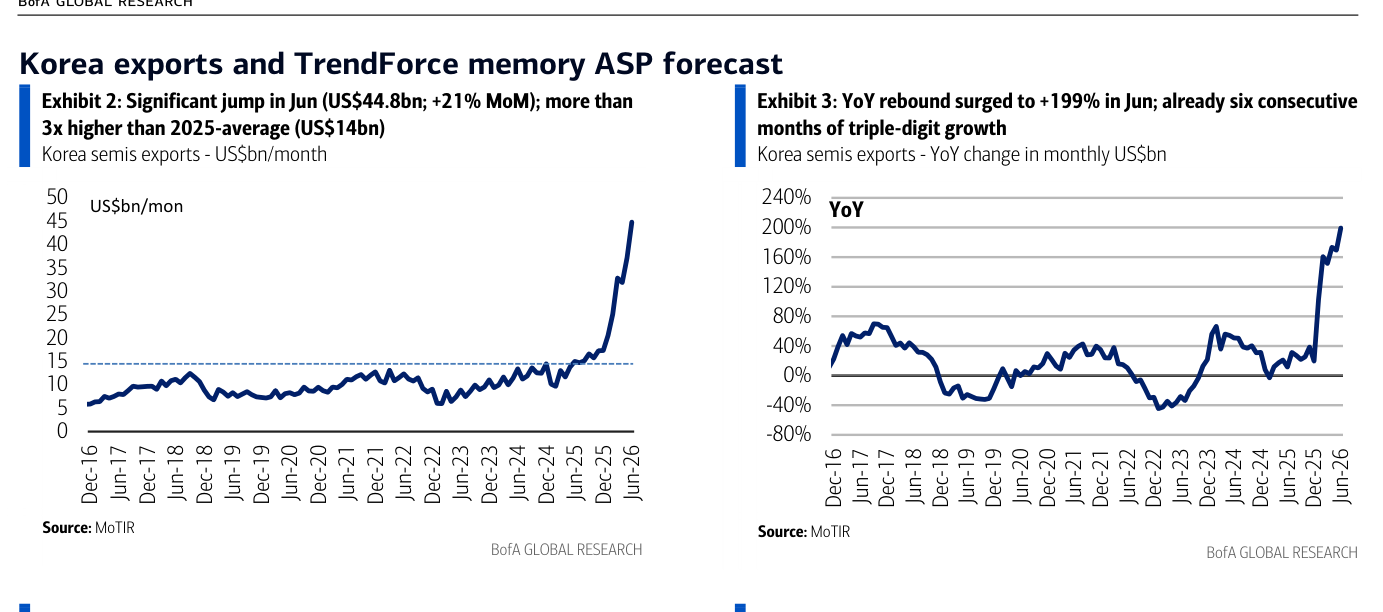

In June 2026, South Korea's semiconductor exports reached $44.8 billion, a month-over-month increase of 21% and a year-over-year increase of 199%. This marks the sixth consecutive month of triple-digit year-over-year growth.

This figure is approximately three times the average monthly export value of $14 billion in 2025, clearly indicating that the current memory price increases are being transmitted significantly to export revenue and corporate profits.

Of course, rising export value does not entirely equate to a simultaneous increase in shipment volume. A large part of the increase comes from rapidly rising product ASPs. However, this precisely illustrates that the core contradiction in the current supply chain remains price increases and tight supply, rather than inventory buildup or a significant contraction in demand.

South Korean Semiconductor Exports (Value & YoY Growth): Notable surge in June 2026 (Original Report, Page 2)

2. DRAM Remains the Strongest Memory Category

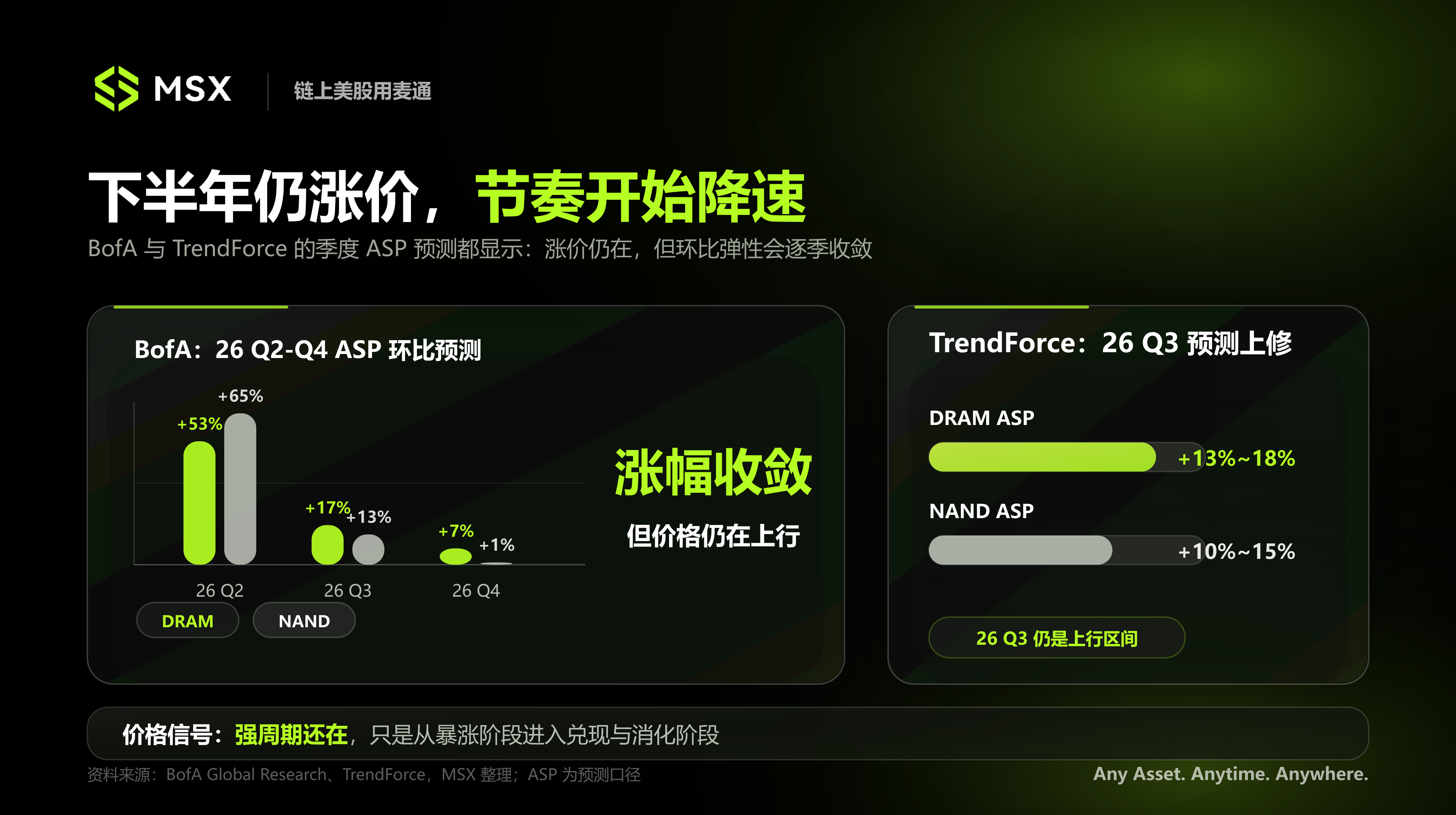

TrendForce has revised its Q3 2026 DRAM ASP forecast from a QoQ increase of 3%–8% up to 13%–18%. Bank of America estimates Q2 to Q4 2026 DRAM ASPs will increase QoQ by 53%, 17%, and 7%, respectively.

The specific metrics differ between the two sets of forecasts, but they both point to the same trend: DRAM prices will continue to rise in the second half of the year, but as the price base increases, the QoQ growth rate may slow sequentially.

As of early July 2026, the spot price for 16Gb DDR5 is approximately $47, and for 16Gb DDR4, it is around $75. Both are significantly higher than the price peaks of the previous memory cycle. The core reason is not just customer inventory restocking, but memory manufacturers consistently shifting wafer capacity towards higher-margin HBM and server DRAM.

After advanced capacity is absorbed by AI-related products, the supply available for traditional DDR4 and standard DDR5 decreases simultaneously.

This is particularly evident for DDR4. As leading manufacturers gradually phase out mature products, DDR4 faces a notable structural shortage. Contract prices for both 16Gb DDR4 and DDR5 have risen to the $35–$40 range, effectively eliminating the long-standing technical premium of DDR5 over DDR4.

This does not mean the market prefers the older DDR4 generation. Rather, manufacturers are exiting faster than customers can complete product transitions, making the mature product scarcer.

3. NAND Price Increases Slow, but Absolute Prices Remain High

Compared to DRAM, the marginal change in NAND prices is more apparent.

After hitting a cyclical high in March 2026, the spot price of 512Gb NAND wafers stabilized or slightly declined from April to June, but it is still up over 50% for the year and approximately eight times the low point from February 2025.

The NAND contract price is around $25, roughly ten times the low of $2.5 in February 2025. Following substantial increases in Q4 2025 and Q1 2026, the monthly growth rate of NAND contract prices from April to June has slowed to around 1%–5%.

This does not signify a reversal in NAND prices but rather indicates that customer tolerance for high prices is gradually approaching its limit, and the pace of price increases is returning to normal.

The change in client SSD prices is particularly direct. As of June 2026, the price of a 512GB client SSD has risen from $73.1 at the end of 2025 to $137.5, nearly doubling. This reflects that upstream NAND price increases are continuously being transmitted to end products.

Therefore, a more accurate description of NAND's current state is that absolute prices remain very high, but the QoQ rate of increase is decelerating.

4. Server Memory Continues to Hit Highs

Server memory also maintains its strong momentum.

Prices for 64GB server DRAM modules have hit all-time highs, with DDR5 around $1,400 and DDR4 around $1,100. In June 2026, DDR5 server DRAM contract prices rose again, while DDR4 prices remained largely flat.

This indicates that even as price increases for some consumer-grade memory products begin to slow, demand for high-end memory related to AI servers and data centers remains robust.

III. Cloud CapEx Remains the Demand Anchor, but the Investment Logic is Changing

1. Hyperscalers Continue to Expand

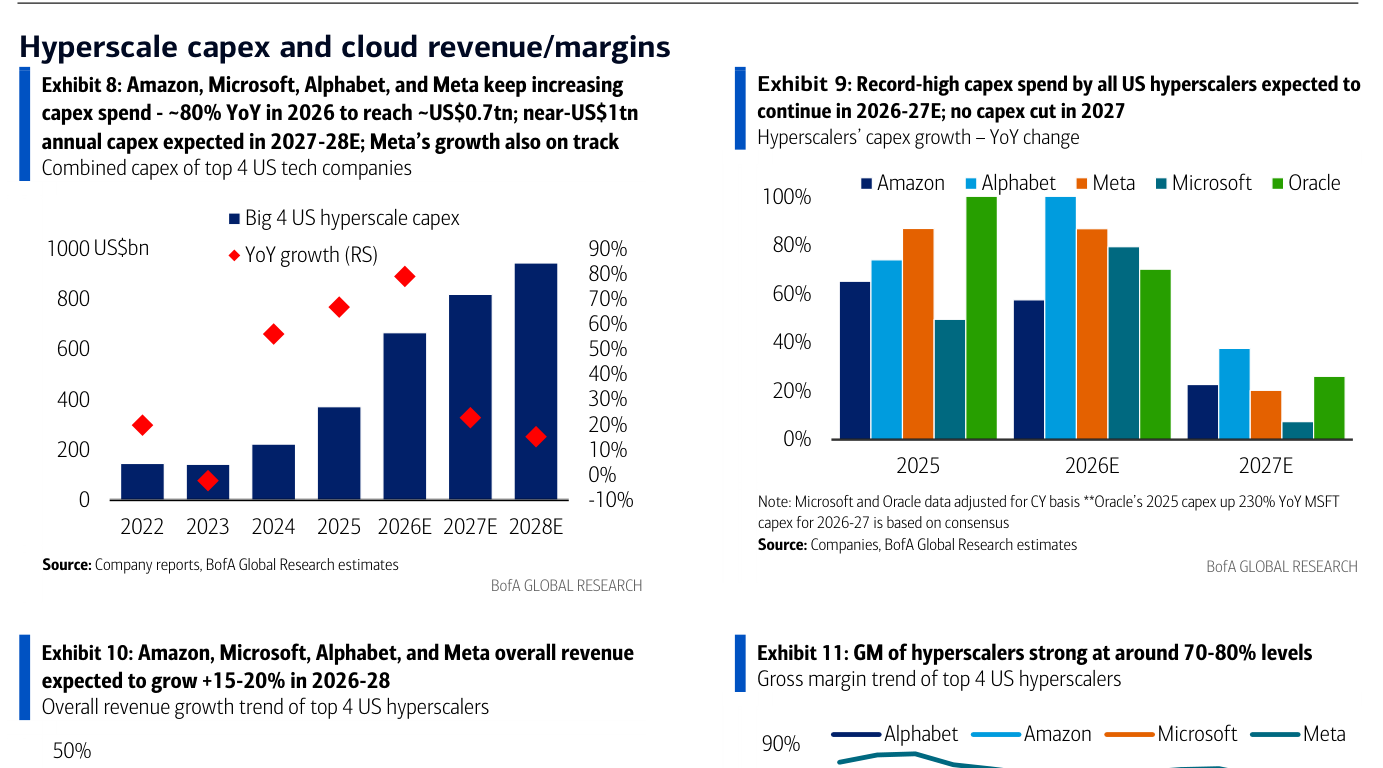

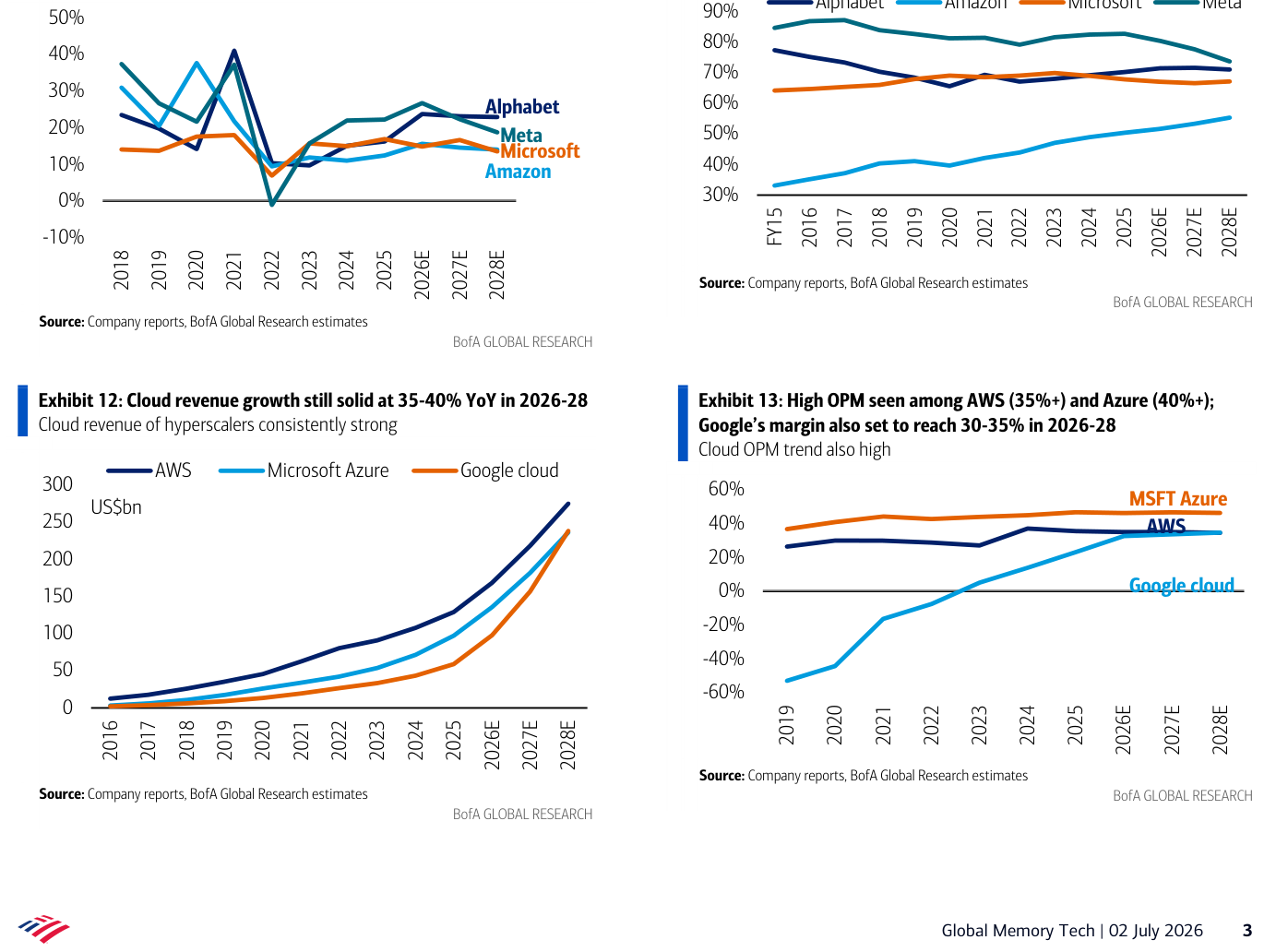

Hyperscale cloud providers like Amazon, Microsoft, Alphabet, and Meta are becoming the most important sources of incremental memory demand. The report estimates that the combined CapEx of these four companies will be approximately $700 billion in 2026, a YoY increase of about 80%. By 2027–2028, annual CapEx could approach $1 trillion.

Furthermore, Bank of America sees no signs of major cloud providers significantly cutting CapEx in 2027, meaning these investments will ultimately translate into more AI accelerators and HBM, more server DRAM, more enterprise SSDs, and more data center and AI inference infrastructure.

CapEx, Revenue & Gross Margin Trends for Major US Hyperscale Cloud Providers (Original Report, Page 3)

The report estimates that from 2026 to 2028, the combined revenue of the four major tech companies could grow by 15%–20%, with cloud segment revenue possibly growing 35%–40% YoY.

Among them, AWS's operating margin is expected to remain above 35%, Azure could exceed 40%, and Google Cloud is projected to reach 30%–35%.

As long as cloud businesses can sustain high revenue growth and profit margins, tech giants will maintain the commercial incentive to continue expanding AI infrastructure investment.

Cloud Revenue & Cloud Business Operating Margin Trends (Original Report, Page 3)

2. This Cycle is No Longer Just about Consumer Electronics Restocking

The biggest difference between this memory cycle and past cycles is that demand is no longer primarily dependent on smartphone and PC restocking.

Past memory cycles were often driven mainly by PC and smartphone inventory changes, creating typical cyclical patterns: end-demand rises → customers restock → memory prices increase → manufacturers expand capacity → inventories gradually build up → prices enter a downtrend.

However, the current cycle has a more complex structure. Demand has long since expanded from simple consumer electronics restocking to include:

- HBM;

- Server DRAM;

- Enterprise SSDs;

- AI Inference Infrastructure;

- Hyperscaler Cloud CapEx;

- Structural shortage from DDR4 capacity retirement.

This means that only observing PC and smartphone sales is insufficient to judge the entire memory cycle. Even if some consumer electronics demand weakens due to high prices, AI servers and data centers can continue absorbing high-end capacity, keeping overall supply relatively tight.

But this also implies that divergence within the sector will become increasingly apparent. In short, companies focused on HBM, server DRAM, enterprise SSDs, and advanced packaging may continue to benefit from stronger orders and margins; manufacturers overly reliant on client, mobile, and consumer-grade NAND might