摩根士丹利解读:上调SIMO目标价至400美元,AI服务器改写NAND周期

- 核心观点:摩根士丹利认为,AI服务器需求正推动NAND市场从消费电子周期转向企业级新周期,预计2026/2027年全球将出现15%/9%的供应短缺,并据此大幅上调Silicon Motion(SIMO)目标价至400美元。

- 关键要素:

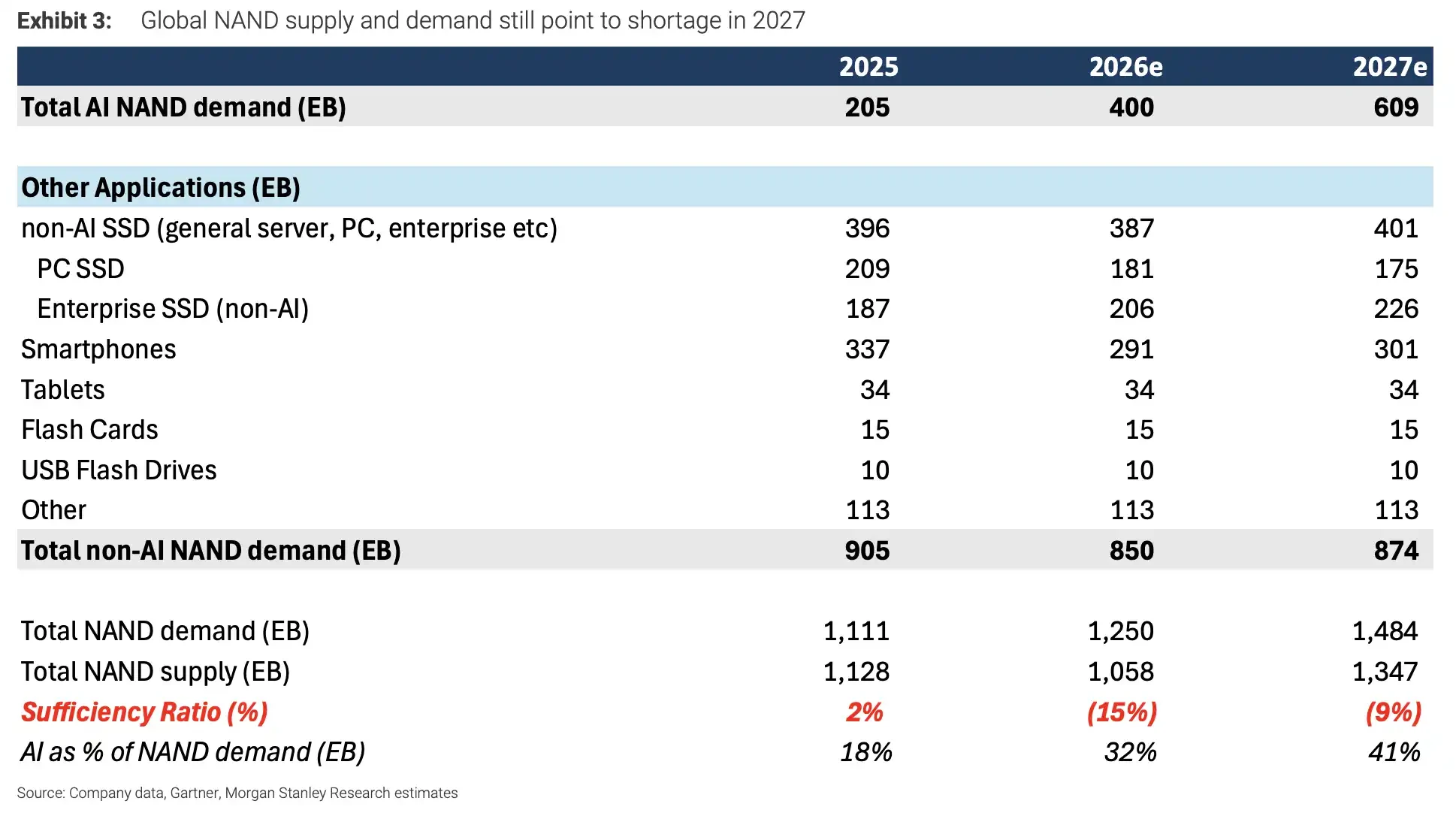

- 供需缺口预测:2025-2027年全球NAND供需比预计分别为2%(过剩)、-15%(短缺)、-9%(短缺),AI需求是核心驱动。

- AI需求占比:预计2027年AI相关NAND需求达609EB,占整体需求的41%,数据中心和云厂商采购成为关键变量。

- 价格分化明显:3Q26企业级SSD定价环比涨约30%,但消费级NAND涨幅有限,因手机/PC客户利润承压。

- SIMO上调逻辑:其企业级SSD控制器(MonTitan)和AI启动盘(boot drive)业务预计2026年贡献营收20%以上,是估值上修的核心。

- 2028年风险:YMTC若扩产至470kwpm或AI资本开支放缓,市场可能从短缺转向过剩,打破乐观预期。

TL;DR

- Morgan Stanley raised its target price for SIMO from $155 to $400, citing accelerated demand for enterprise SSDs and boot drives driven by AI.

- It forecasts a 15% global NAND shortage in 2026 and a 9% shortage in 2027, with AI-related demand reaching 609EB by 2027.

- Suppliers and controller companies benefit more directly, but consumer-side price increases are limited; YMTC's capacity expansion and a slowdown in AI capex could alter the supply-demand balance in 2028.

In its latest report, Morgan Stanley significantly raised target prices for Silicon Motion (SIMO.O) and Longsys, pointing to the NAND demand gap created by AI servers. For investors, this is not just a typical expectation of SSD price increases but a sign that AI data centers are shifting NAND demand from consumer electronics cycles like smartphones and PCs towards a new cycle driven by enterprise SSDs, AI boot drives, and long-term procurement from cloud providers.

The most aggressive adjustment falls on SIMO. Morgan Stanley raised its target price from $155 to $400, corresponding to 23 times the expected 2027 EPS, and anticipates the company's revenue will hit a historical high in 2026. The target price for Longsys was also raised from RMB 300 to RMB 673, and Phison's target price from NT$2,248 to NT$2,588. However, Morgan Stanley maintains an Equal Weight rating for both Longsys and Phison, indicating that not all module makers will benefit equally from this cycle.

The core judgment of this report is that AI's pull on NAND will continue until 2027. In 2025, the lingering inventory overhang still causes a global NAND oversupply of about 2%; by 2026, the market is expected to shift to a 15% shortage; and in 2027, even as supply continues to ramp up, a 9% gap is still possible. The key driver behind this is not smartphones and PCs, but rather demand from AI servers, cloud providers' SSDs, enterprise storage, and boot drives.

Global NAND supply-demand still points to a shortage in 2027. Total demand for 2025-2027e is 1111/1250/1484 EB, with supply at 1128/1058/1347 EB, shifting the supply-demand balance from 2% surplus to -15% and -9%.

AI Shifts NAND Demand重心 from Consumer Electronics to Data Centers

In the past, NAND was more easily swayed by the inventory cycles of smartphones, PCs, and consumer-grade SSDs. The change now is that AI servers require not just GPUs and HBM, but also substantial local storage, enterprise SSDs, and boot drives. Once cloud providers' procurement shifts into long-term agreements, the dynamics of NAND price and supply-demand balance will also change.

Morgan Stanley estimates that AI-related NAND demand in 2027 will grow 60% year-over-year, reaching 609EB, accounting for 41% of total NAND demand. That same year, global NAND total demand is expected to be 1484EB, compared to a supply of 1347EB, corresponding to roughly a 9% shortage. In contrast, the assumptions for smartphones and PCs are not aggressive: per-device NAND content is roughly flat, and terminal shipments are modeled to decline based on hardware team projections.

This means that the report's judgment of a shortage is not built on a broad consumer electronics recovery, but on the continued expansion of AI servers and cloud capital expenditure. The greater the contribution from AI demand, the higher the sensitivity of the NAND cycle to CSP procurement, server configurations, and enterprise SSD supply.

Channel prices are already starting to diverge. 3Q26 channel checks show that TLC enterprise SSD pricing is up roughly 30% quarter-over-quarter, server-grade DRAM up 20%, and legacy DRAM like DDR3/DDR4 up 30%-40%. However, consumer-grade NAND price increases are significantly smaller, as smartphone and PC customers face greater profit pressure and cannot bear the same magnitude of price hikes.

In other words, price increases are indeed happening, but the strongest gains are in data center-related products, not all NAND categories.

Why Was SIMO Upgraded the Most?

The core reason for the raised target price on SIMO is that its business exactly taps into two segments of AI storage growth: enterprise SSD controllers and AI boot drive modules.

The MonTitan enterprise SSD business is considered the most important new growth driver for the company in the coming years. Morgan Stanley expects this business to contribute 5%, 13%, and 19% to SIMO's revenue in 2026, 2027, and 2028, respectively. Meanwhile, the boot drive module is also expected to ramp up, contributing an estimated 15% and 21% of the company's total revenue in 2026 and 2027.

For AI servers, the boot drive is not the most prominent component, but it is an indispensable storage configuration for system startup, management, and operation. As AI server shipments increase, demand for related controllers and modules will also rise. SIMO was previously seen more easily by the market as a consumer-grade controller company; the key to its valuation upgrade now is the potential for its enterprise and AI-related revenue share to increase rapidly.

However, this is still a projection, not already realized profits. The $400 target price given by Morgan Stanley corresponds to 23 times the expected 2027 EPS, implicitly assuming smooth volume ramp-up for enterprise SSDs and boot drives, continued customer adoption, and no significant slowdown in AI server demand. Any of these links falling short of expectations could affect whether the valuation holds.

Module Makers Get Target Price Hikes, But May Not Capture the Biggest Slice

Longsys and Phison also benefit from memory price increases and AI server demand, but the report did not upgrade their ratings to a more aggressive level. The reason is that module makers face a practical constraint in this cycle: when NAND supply is tight, original manufacturers are more likely to prioritize capacity allocation to large cloud vendors and core CSP customers, meaning the incremental supply available to module makers may not be sufficient.

This is also why target prices can be raised, but ratings remain at Equal Weight. Price increases benefit inventory and ASP, and an improved enterprise product mix can support margins. However, if volume is locked in by upstream suppliers and major customers, the revenue elasticity for module makers becomes limited.

Long-Term Agreements (LTAs) are another important clue. Suppliers can gain some downside price protection through LTAs; Kioxia's LTA coverage for 2027 is expected to exceed 50%. However, these agreements are not a one-way benefit. Micron has also indicated that LTAs often include both price ceilings and floors. While they can reduce the risk of a price crash, they may also limit suppliers' ability to raise prices during extreme shortages.

Module makers, on the other hand, hope to use models like TCM to transfer more inventory pressure to customers, aiming for long-term gross margins in the 25%-35% range. This, however, also depends on customer acceptance, the degree of supply tightness, and whether the products are sufficiently high-end.

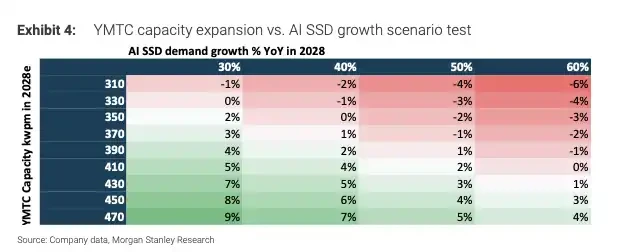

The Risk for 2028 Lies in Supply and AI Spending

The biggest boundary for this optimistic forecast lies in 2028.

In Morgan Stanley's baseline scenario, even by 2028, if AI NAND demand still grows 60% year-over-year and YMTC capacity stays around 310kwpm, the market could still see a shortage of about 5%. However, if YMTC capacity rises to 470kwpm while AI growth slows down, the NAND market could shift from shortage to oversupply.

Scenario analysis: YMTC 2028 capacity expansion vs. AI SSD growth. The matrix shows that with YMTC capacity at 310-470kwpm and AI growth at 30%-60%, the supply-demand balance could shift from shortage towards equilibrium or even oversupply.

This is also the most challenging part of judging the memory cycle: short-term price increases and low inventory levels can easily reinforce optimistic expectations, but once supply discipline loosens in semiconductor memory, oversupply can return quickly. On the consumer side, some order reductions have already appeared; smartphone and PC customers have limited tolerance for price increases, and the price ceiling for consumer-grade NAND may be reached earlier than for enterprise products.

Therefore, the real question this report poses to the market is not "will SSDs get more expensive," but whether AI demand is strong enough to absorb the new supply in the next two years. For companies like SIMO on the NAND controller and AI storage chain, 2026 could be the starting point for significant volume in enterprise and AI businesses. For the overall NAND cycle, the expansion pace of manufacturers like YMTC in 2028, the intensity of CSP capital spending, and supplier discipline will be the key factors determining whether the shortage can persist.