万字解析2026年互联网资本市场:美国结构性转变与亚洲机构的战略窗口

1. The Crypto Industry is Completing Its Transition from Experiment to Industry

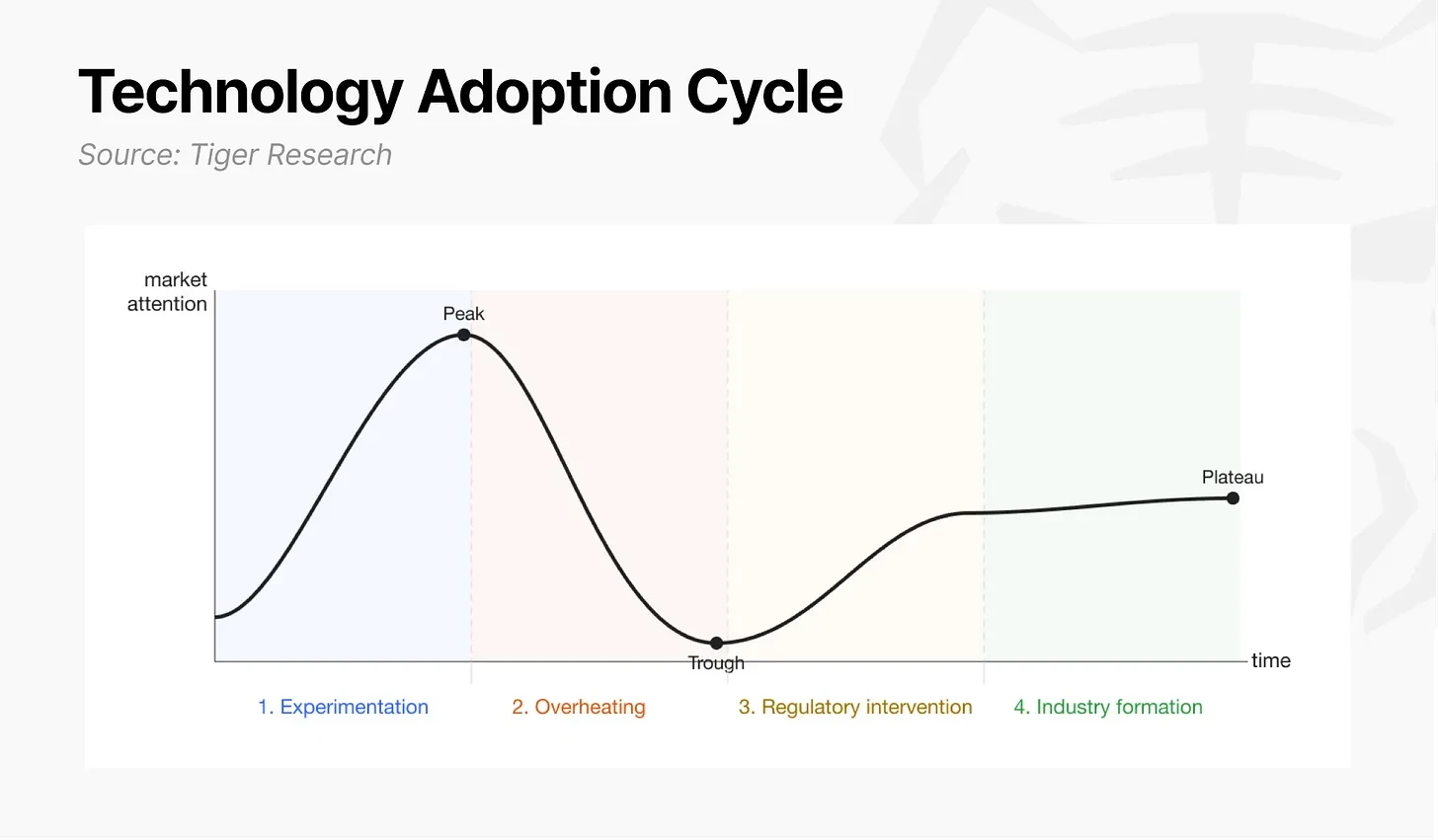

This article is from Tiger Research. The journey of a new technology from experiment to industry typically goes through four phases: the experimental phase, the overheating phase, the regulatory intervention phase, and the industry formation phase. The internet completed its experimental phase in the 1990s, experienced the overheating of the dot-com bubble, and finally evolved into a mature industry after the bubble burst, following the establishment of regulations and standards. Fintech and artificial intelligence are following the same path, albeit with different rhythms and forms.

The crypto industry is currently in the transition zone between the third and fourth phases. After the birth of Bitcoin, a small group of developers verified its potential for payments and settlements (experimental phase). During the ICO boom of 2017 and the DeFi wave of 2021, investors rushed in and out repeatedly (overheating phase). The collapse of FTX in 2022 was both the peak and a turning point. After multiple shakeouts, speculative demand has been filtered out, real-world use cases have been validated, and U.S. regulators have begun to shift towards formalization rather than laissez-faire or suppression (regulatory intervention phase).

Because the crypto industry attempts to directly replace core financial functions like settlement, payments, and issuance, it creates greater friction with traditional financial institutions, thus taking longer to be absorbed. Today, the crypto industry has finally reached the intersection of regulatory intervention and industry formation.

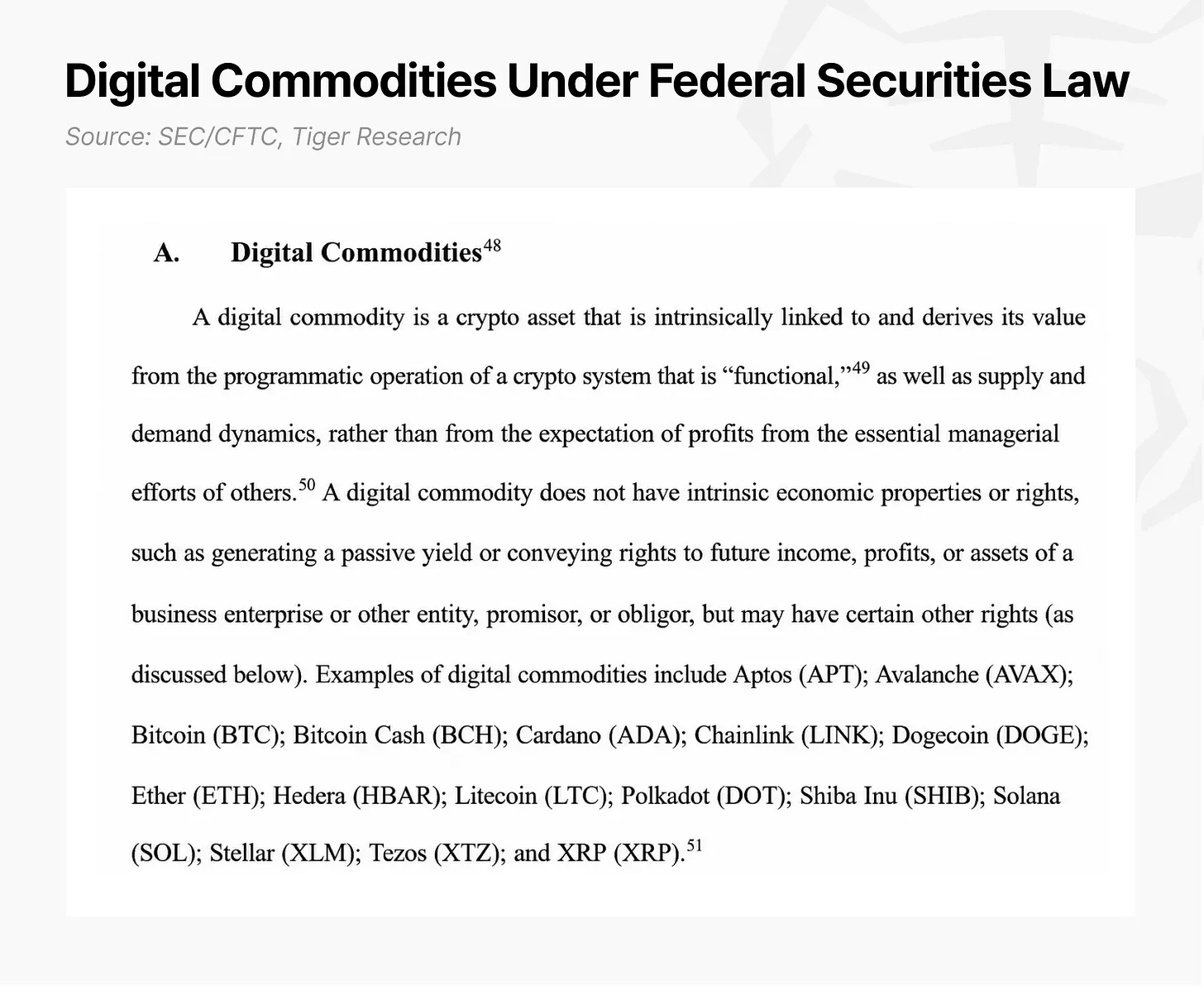

Progress on the regulatory front is significant. The U.S. Congress passed the GENIUS Act, clarifying the legal status of stablecoins. In March 2026, the SEC and CFTC issued joint interpretive guidance, recognizing 16 assets, including Solana (SOL), as digital commodities. This guidance classifies assets into five categories, discarding the old binary "security/non-security" classification, and formally excludes protocol staking from securities law oversight.

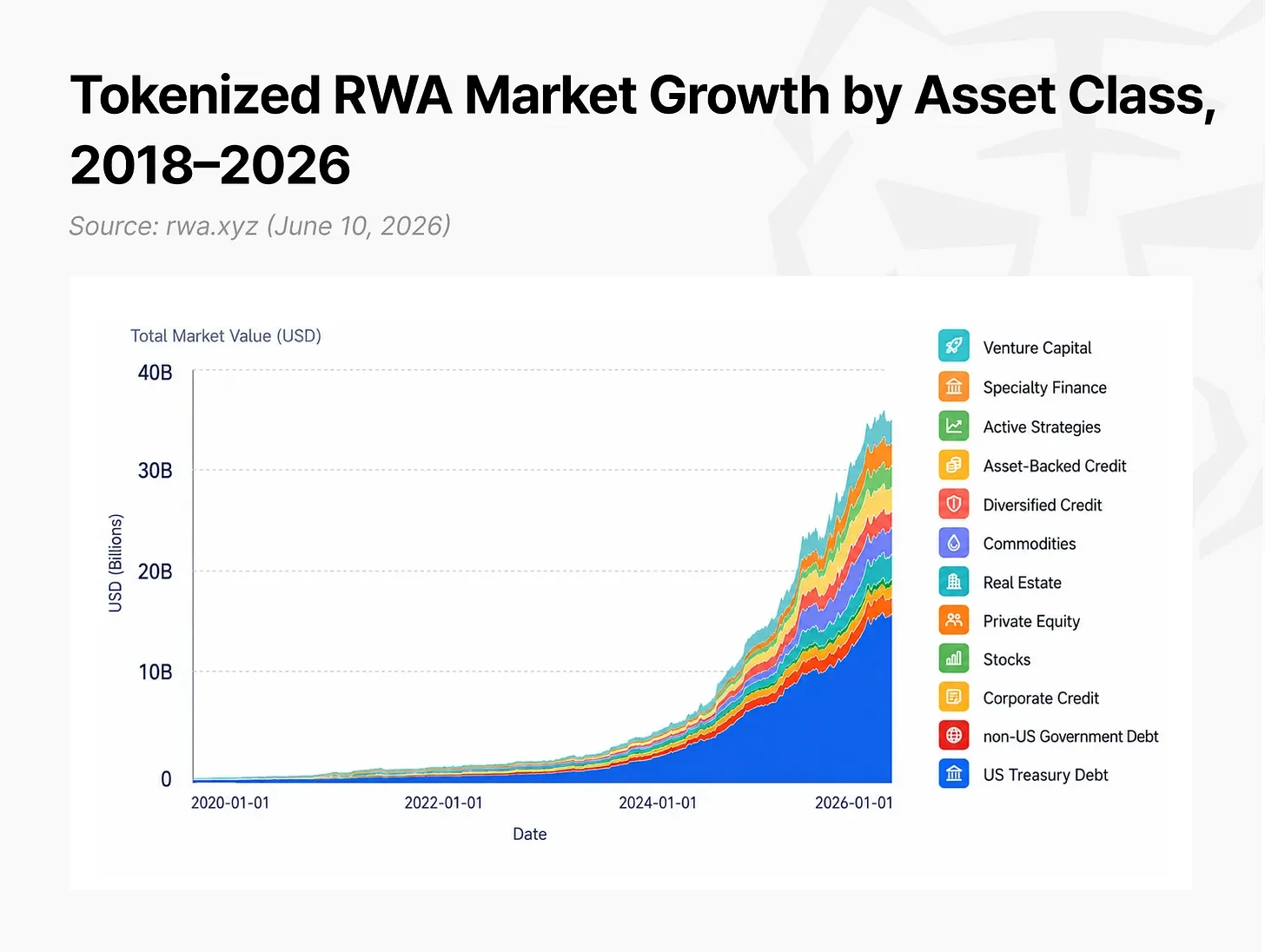

Institutional adoption continues to accelerate. The tokenized real-world asset (RWA) market grew by approximately 257% in 15 months, from $5.4 billion at the start of 2025 to $19.3 billion by the end of March 2026. If stablecoins are included, the total value of on-chain assets has approached $300 billion.

This is not yet enough to call it a mature industry, but industry formation has already begun in tandem with regulatory development.

2. Internet Capital Markets: The Endgame for the Crypto Industry

The future the crypto industry points to as it enters the industrial phase is a restructuring of capital markets themselves. This future can be defined as "Internet Capital Markets" (ICM): a capital market where the issuance, trading, and settlement of assets all occur on a single public blockchain.

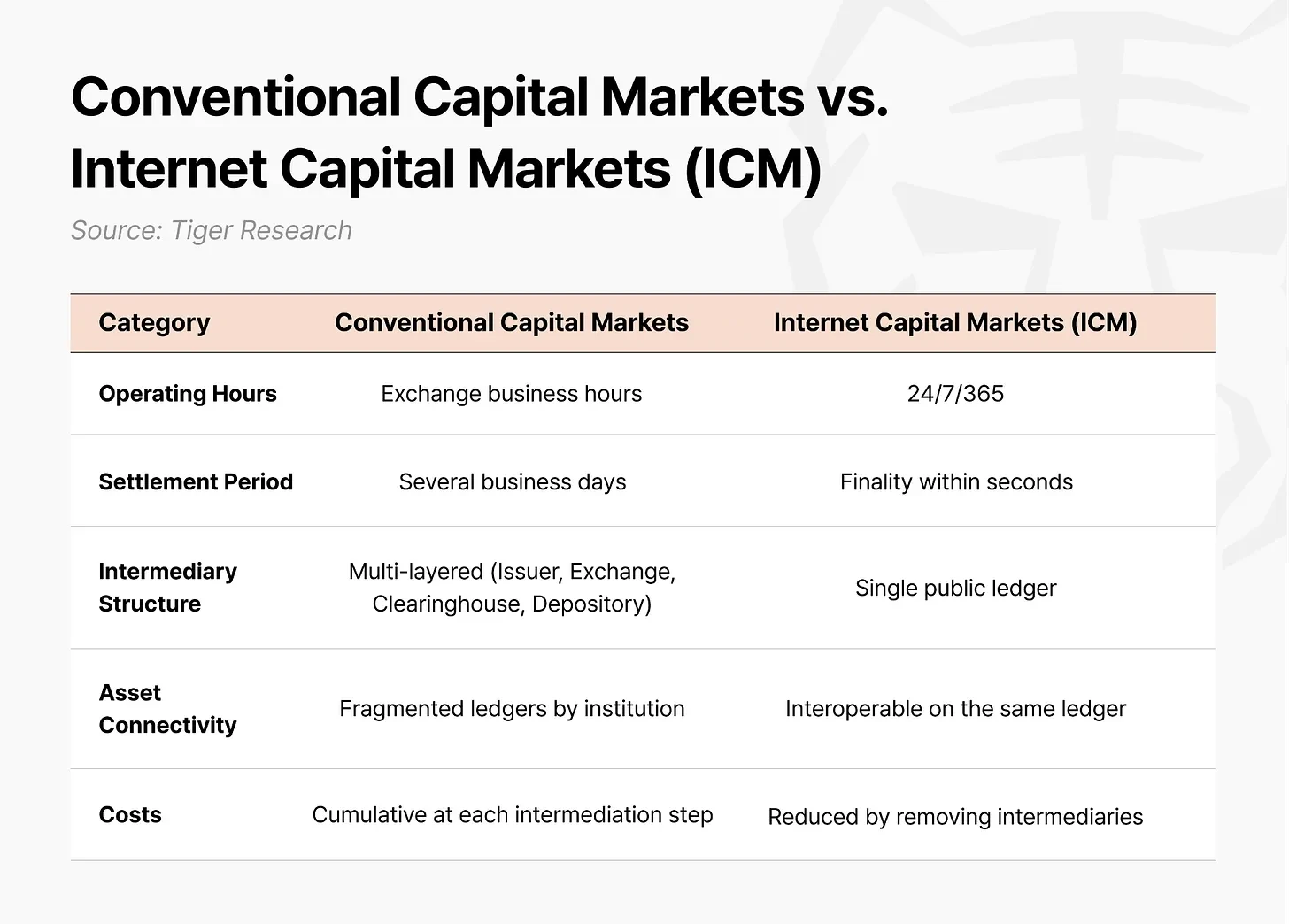

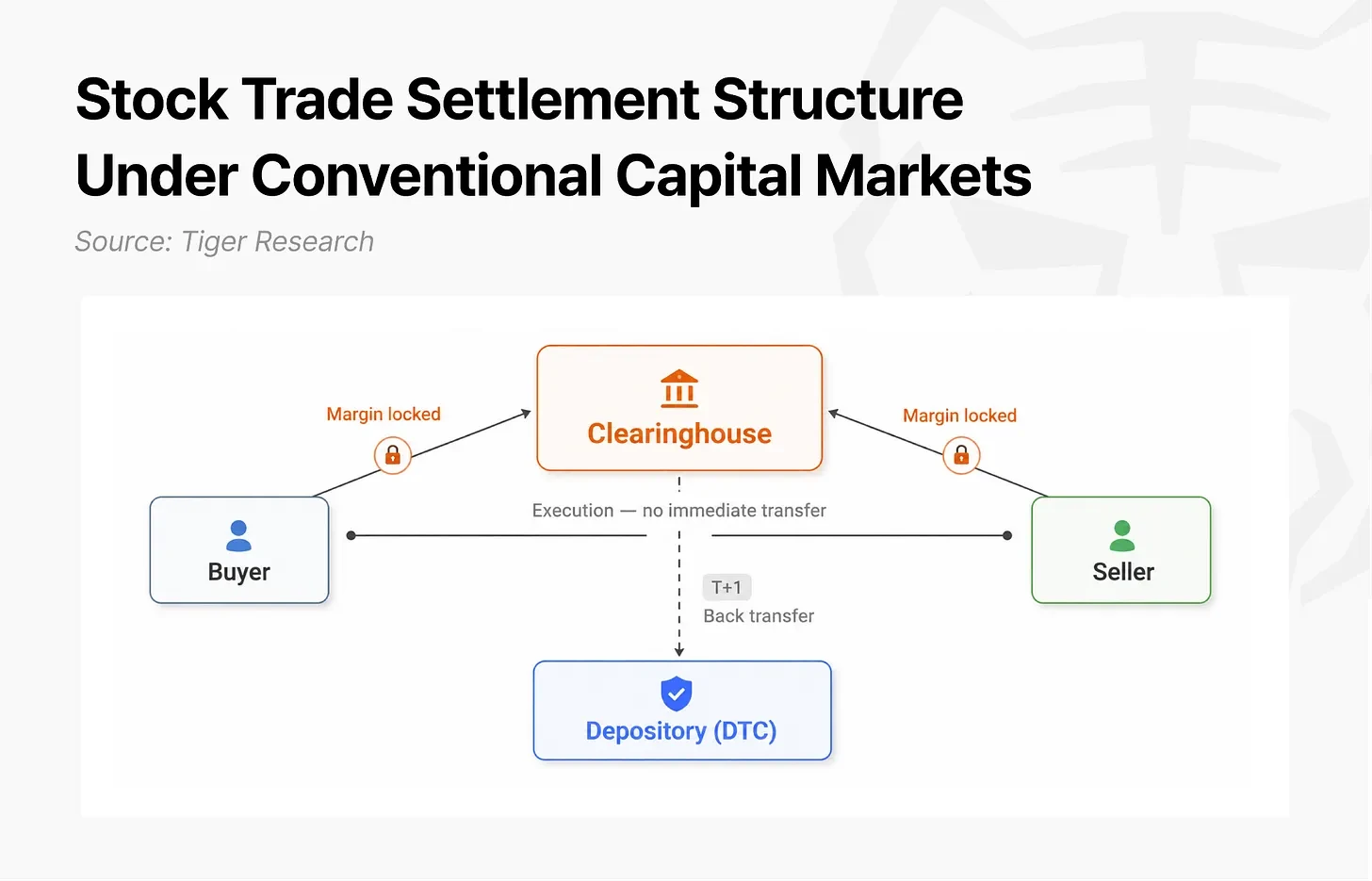

Today's capital markets operate on an architecture designed before the internet was born. When buying and selling a stock, the assets and funds do not settle at the moment of execution. A clearing house sits between buyers and sellers, assuming settlement risk and requiring margin from both parties. This capital is locked up until settlement is complete. In the U.S. market, the transfer of securities at the depository doesn't occur until the business day after execution. Because brokers, exchanges, clearing houses, and depositories each maintain separate ledgers, they must reconcile with each other daily; any discrepancy delays settlement. Cross-border transactions add currency conversion and foreign depositories, extending settlement times to T+3 or longer. This architecture, designed for an era of mutual distrust between counterparties, has itself become a cost.

In the Internet Capital Markets, code takes over the role of the clearing house. The buyer's payment and the seller's asset are placed into a smart contract simultaneously, executing both transfers as a single transaction. If either party's conditions are not met, the entire transaction automatically cancels, eliminating the scenario of one-sided fund flow. Since settlement risk is eliminated at the code level, the clearing house's margin requirements are no longer needed. And because all participants share the same real-time ledger, inter-institutional reconciliation disappears. Execution and settlement are completed synchronously within seconds.

The entities driving this change are expanding from crypto startups to traditional financial institutions. Institutions that once earned revenue from multi-layered intermediary structures are now themselves participating in this transformation. History repeatedly shows that at every inflection point of infrastructure change, institutions that follow later either pay higher costs or lose their leadership position. The transition to electronic trading in the 1990s is a classic example: large institutions reliant on floor trading initially resisted electronic platforms like Island ECN and Instinet, only passively following through acquisitions and adoption after these platforms became the standard. The fintech transition is unfolding similarly.

This transformation is progressing fastest in the United States. After the dollar became the reserve currency under the Bretton Woods system in 1944, global trade and financial transactions are denominated and settled in dollars. CHIPS processes over $2.2 trillion in payments every business day. The SEC's disclosure standards serve as a reference for the capital market systems of other countries. Over 99% of stablecoins are dollar-denominated. The U.S. is replicating this same model within the Internet Capital Markets.

3. The Specific Implementation of Internet Capital Markets

For example, within the landscape of U.S. Internet Capital Markets, Solana is the public chain network that integrates the technical foundation, institutional practice, and regulatory design into one.

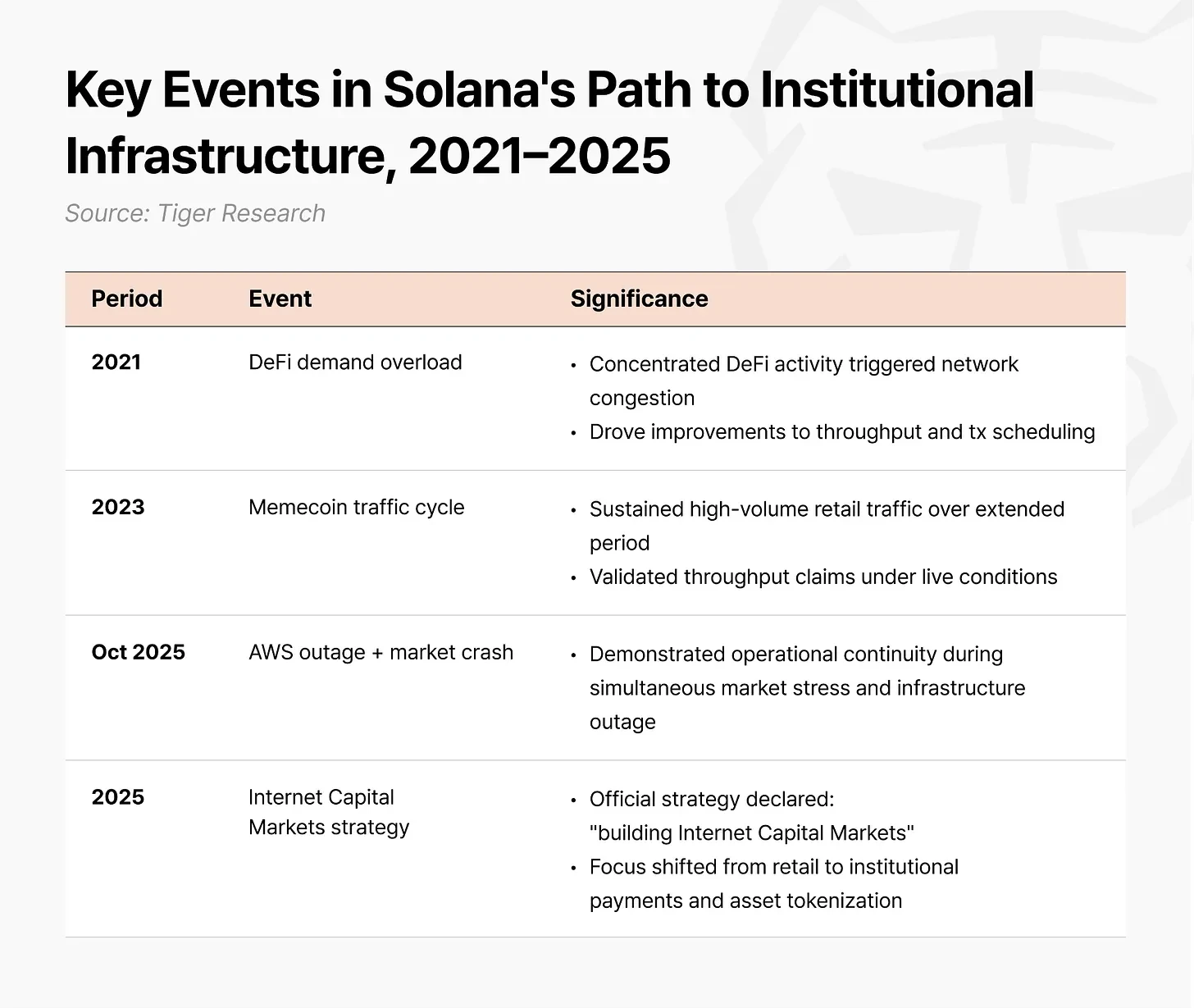

Solana's technical foundation has been tempered in the retail market. The surge in DeFi demand in 2021 caused network overload, which Solana treated as an opportunity to improve throughput and transaction scheduling. During the meme coin cycle in 2023, it validated its throughput claims by sustaining high-intensity retail traffic for an extended period. In October 2025, a market crash coincided with an AWS outage; transaction fees on other chains soared to $100 per transaction, while Solana continued operating at a cost of $0.0013 per transaction without interruption. The infrastructure stability required for institutional finance was first validated through stress tests in the retail environment.

In 2025, Solana established "building Internet Capital Markets" as its official strategy, shifting its focus towards institutional payments and asset tokenization. The Token-2022 standard introduced for this purpose embeds functions like freezing, confiscation, whitelist management, and confidential balances directly into the token code itself. Issuers can achieve compliance requirements within the token itself without needing external systems, addressing the core financial needs for asset holding and transaction eligibility at the protocol level.

On this infrastructure, seven major U.S. financial institutions have initiated proof-of-concepts or completed real transactions on Solana: J.P. Morgan, State Street, Citi, Franklin Templeton, Visa, PayPal, and Western Union. Three of these are among the eight U.S. Global Systemically Important Banks (G-SIBs).

Concurrently, the Solana Policy Institute (SPI) was established in Washington, D.C., in the spring of 2025, recruiting the former CEO of the DeFi Education Fund and the former CEO of the Blockchain Association. Rather than waiting for legislation to pass before reacting, it proactively submitted a pilot framework called "Project Open" to the SEC's Crypto Task Force, attempting to set regulatory precedents first, while simultaneously advancing business diversification and regulatory development.

4. Institutional Practice: Case Studies in Four Key Areas

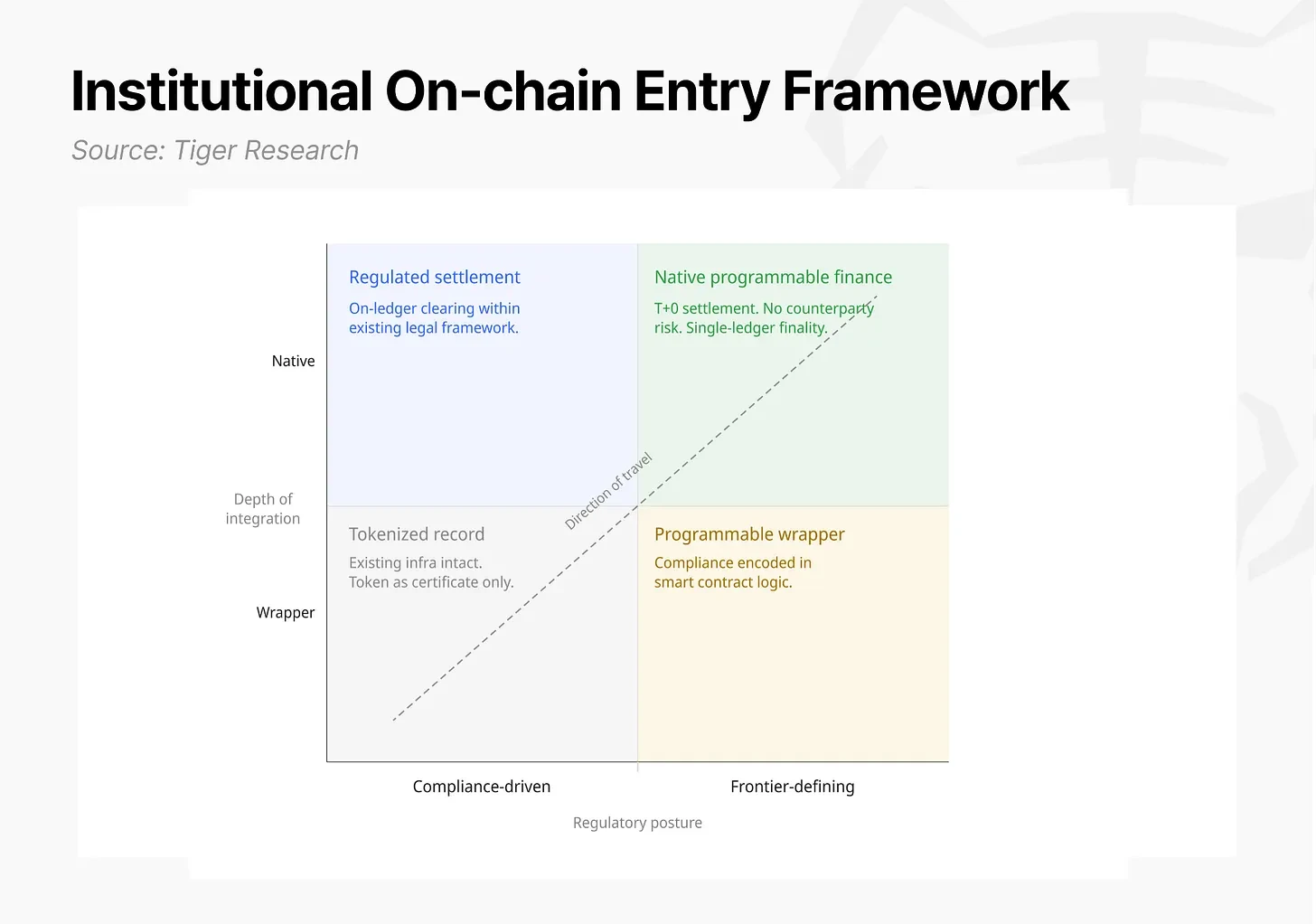

Institutional participation in Solana's Internet Capital Markets is unfolding across multiple fronts, but not all participants share the same goals. Understanding this layered activity requires an analytical framework built around two core axes: regulatory posture (Compliance-Driven vs. Frontier-Defining) and the depth of value chain integration (Wrapper Layer vs. Native Layer).

4.1 Banking and Capital Markets: The Hidden Cost of Settlement Delays

The banking and capital markets sector, encompassing bond issuance, trade finance, and treasury management, is the core revenue source for traditional financial institutions and the area where the cost advantages of Internet Capital Markets are most directly apparent. Three sub-areas share a key issue: the time lag between trade execution and the actual movement of funds.

According to estimates by Tiger Research, in the U.S. Treasury market alone, the annual opportunity cost of capital idling due to settlement delays is approximately $32 billion. If extended to the entire U.S. fixed-income market, the annual opportunity cost exceeds $45 billion. The speed limitations of the existing financial system are imposing significant hidden costs on market participants.

On the Internet Capital Markets infrastructure, this chronic time lag disappears. Atomic settlement (DvP) bundles asset transfer and payment into a single transaction processed in real-time. The clearing house is no longer needed, and the separate reconciliation processes run by each institution are eliminated. Execution and settlement are completed within seconds.

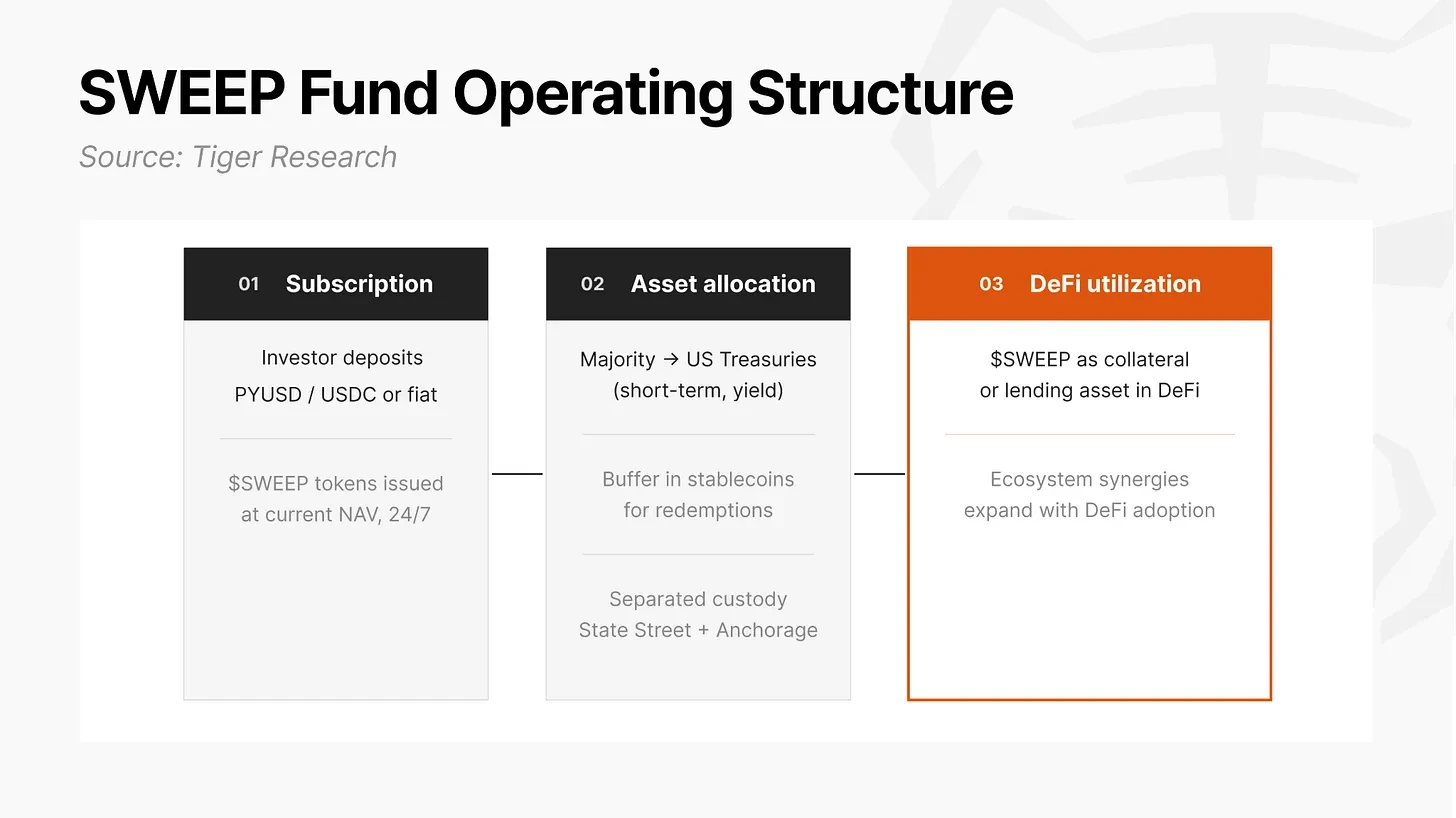

State Street × Galaxy: On-Chain Treasury Management (SWEEP). Launched on Solana in May 2026, SWEEP is an on-chain fund for institutional investors that accepts stablecoin (PYUSD, USDC) or fiat deposits and invests in short-term U.S. Treasuries to generate yield. It implements the traditional finance concept of a "sweep account" as an on-chain fund. For Web3 foundations holding large amounts of stablecoins, accessing traditional financial services under the existing infrastructure requires first converting stablecoins to USD, incurring conversion fees and time delays. SWEEP allows institutions to deposit into and redeem from a Treasury yield asset directly from their wallet. Ondo Finance's flagship fund, OUSG, made an anchor investment of approximately $200 million at the launch of SWEEP, representing about 26% of its total TVL at the time.

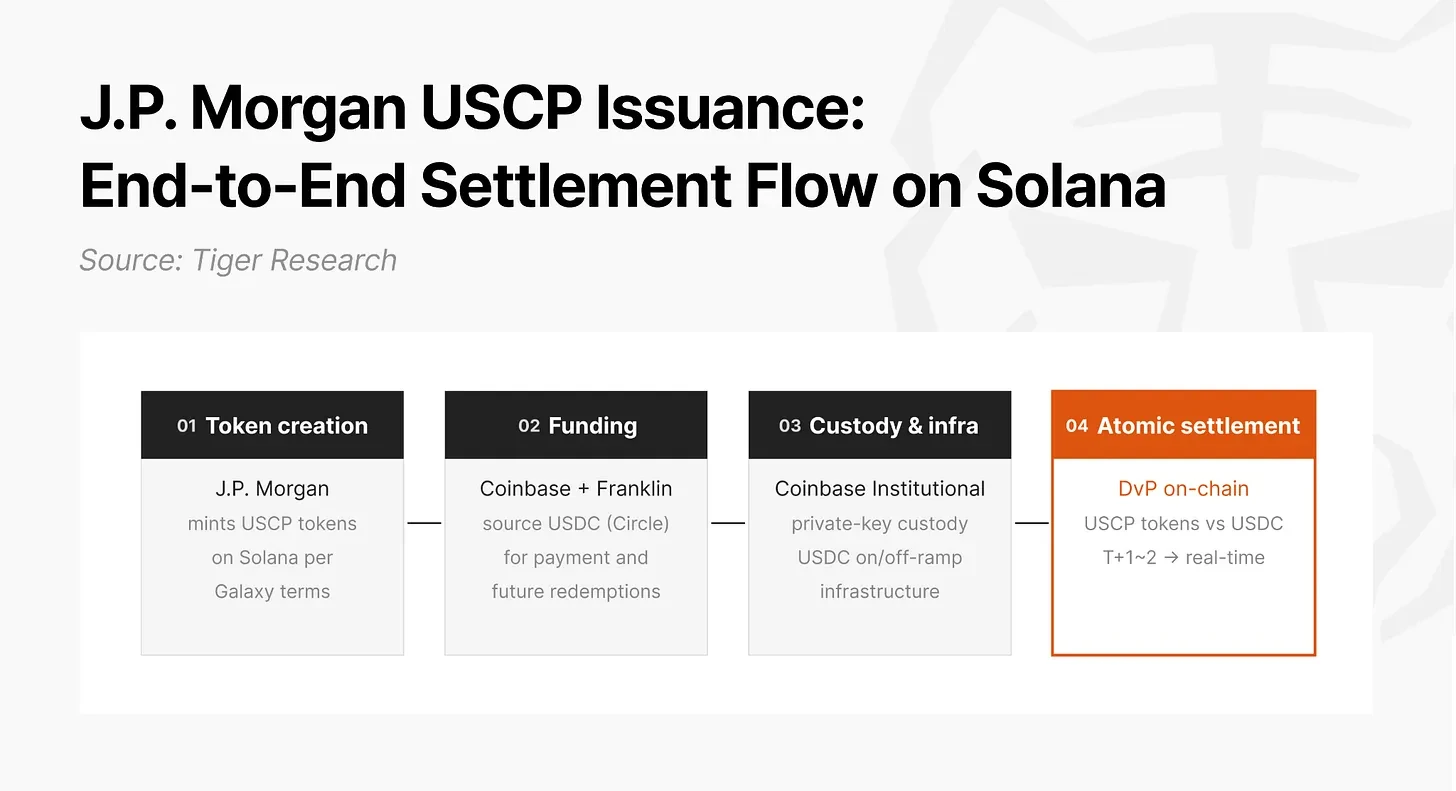

J.P. Morgan × Galaxy: Commercial Paper Issuance (USCP). In December 2025, J.P. Morgan arranged a $50 million U.S. commercial paper issuance on the Solana public chain. This was not a simulation test but one of the earliest real debt security transactions on a public blockchain. J.P. Morgan acted as the arranger, creating USCP tokens directly on the Solana blockchain. Coinbase and Franklin Templeton acted as primary investors and buyers, paying with USDC (issued by Circle). Coinbase provided private key custody and USDC on/off-ramp infrastructure. By combining the stablecoin payment network with on-chain atomic settlement (DvP), the corporate financing cycle—which previously required T+1 to T+2 and multiple intermediaries—was compressed to real-time completion.

Citi × PwC: Trade Finance Tokenisation (Bill of Exchange). Citi and PwC completed an internal proof-of-concept on Solana, transforming traditional bills of exchange into tokenized digital assets. In a simulated environment, the entire lifecycle of a bill of exchange (issuance, financing, circulation, settlement) was automated via smart contracts, reducing settlement time from days to minutes and eliminating manual reconciliation costs. This case study holds strong relevance for Asian financial markets, given that global trade hubs are highly concentrated in Asia.

4.2 Payments and Stablecoins: Redesigning the Settlement Paradigm

Western Union: Global Remittances (USDPT). In May 2026, this 175-year-old company, which processes approximately $150 billion in cross-border remittances annually across over 200 countries, issued a USD payment token, USDPT, on Solana. In the traditional correspondent banking system, each intermediary bank processes transactions only within its own systems and working hours. Settlement typically takes one to two business days, stopping entirely on weekends and holidays. To respond instantly to real-time payment requests from destination countries, Western Union must pre-lock significant USD amounts in local bank accounts across various countries. These pre-deposited correspondent account balances remain locked and yield nothing before the transfers occur.

USDPT fundamentally redesigns this settlement process, shifting the paradigm from "pre-funded reserves" to "real-time on-demand supply." When a local agent's cash inventory falls below a threshold, the U.S. headquarters treasury team immediately sends funds, via USDPT issued by Anchorage Digital, to the agent's institutional on-chain wallet. Regardless of weekends, nights, or holidays, final settlement is rapidly completed based on Solana's 0.4-second block time. Western Union is also building a Digital Asset Network (DAN) and plans to roll out its consumer-facing stablecoin payment service, "Stable by Western Union," to over 40 countries within 2026.

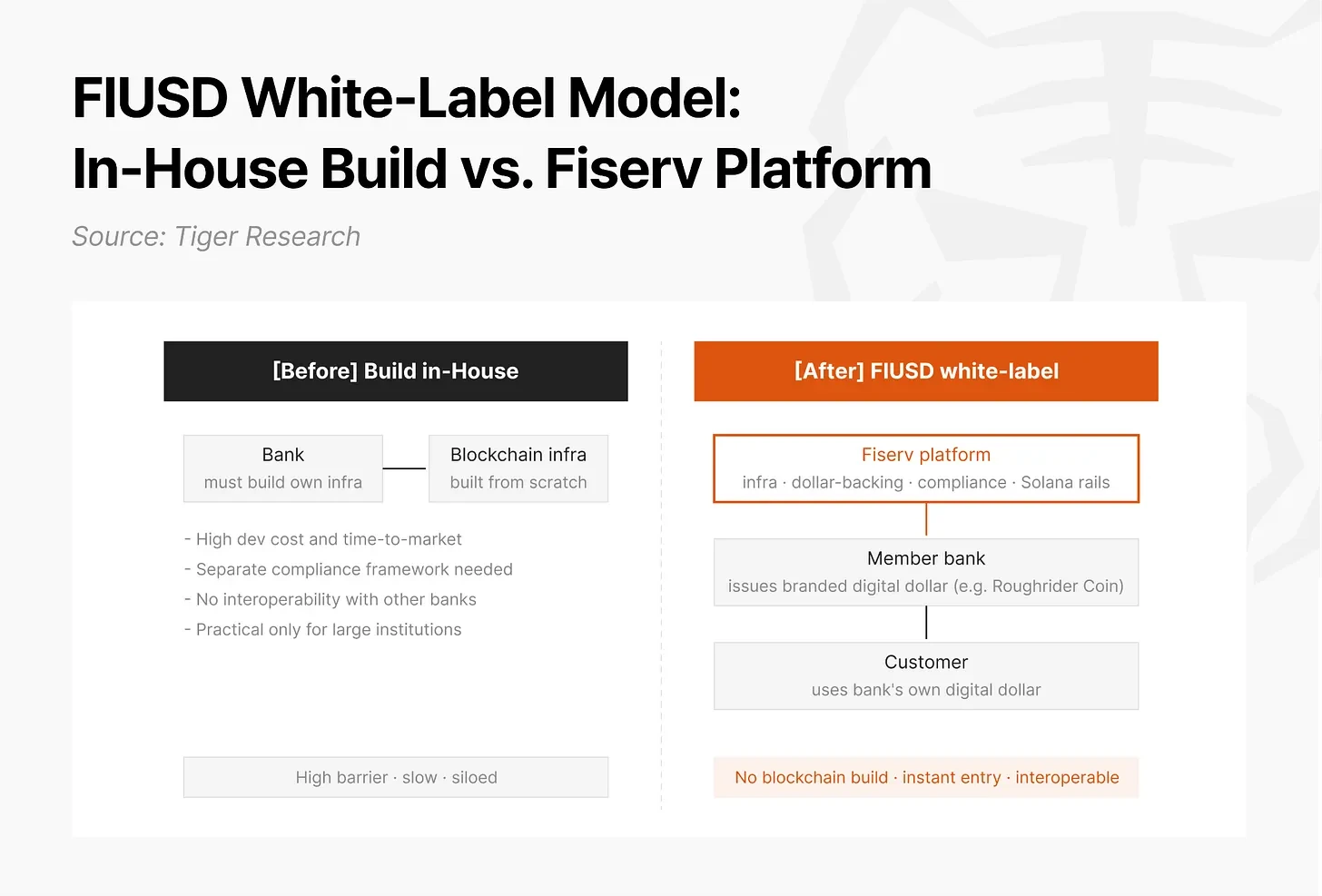

Fiserv: White-Label Stablecoin for Financial Institutions (FIUSD). Fiserv announced the launch of its FIUSD white-label stablecoin platform, scheduled to go live on Solana in July 2026. Under the white-label structure, Fiserv provides the technical infrastructure and USD backing, while individual financial institutions issue and offer stablecoins under their own brands. Banks can offer their own digital dollar to customers without building blockchain infrastructure from scratch. The Bank of North Dakota (the only state-owned bank in the U.S.) has already announced it will launch a "Roughrider Coin" on this platform. Fiserv's multi-sided network covers approximately 10,000 financial institution clients and 6 million merchants, processing 90 billion transactions annually. It plans to offer FIUSD for free to its member financial institution clients using existing technology.

This structure can be directly adopted by Asian financial institutions. For South Korea, the white-label model perfectly maps onto the current debate about whether banks or non-bank institutions can issue stablecoins. Once the Financial Services Commission (FSC) defines the boundaries and establishes Korean Won-denominated rules, this model is immediately transferable.

4.3 Real-World Asset Tokenization: A Closed Loop from Issuance to Circulation

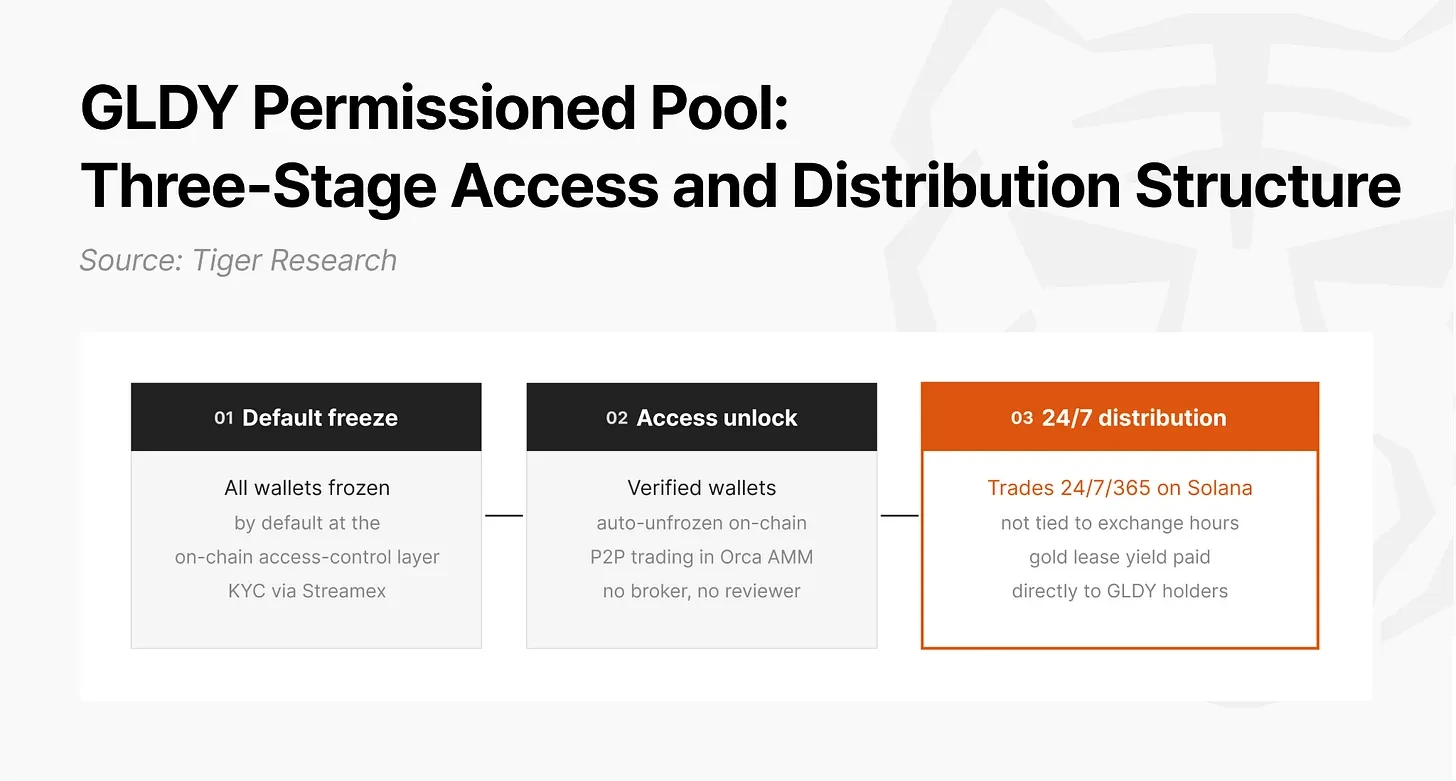

Orca × Streamex: Compliant RWA Distribution (GLDY). The tokenized public stock market has long faced a disconnect between issuance and distribution. Several exchanges offer secondary trading venues for tokenized public equities, but non-equity tokenized securities like bonds, commodities, and private loans lack a liquidity infrastructure post-issuance that is controlled by the issuer and accessible based on eligibility criteria. Issuance technology has improved, but distribution infrastructure has not kept pace.

In May 2026, Orca launched a permissionless AMM infrastructure, allowing issuers to create customizable permission pools according to their regulated asset requirements. Nasdaq-listed Streamex, acting as the first issuer, utilized this solution to provide secondary liquidity for its gold yield token, GLDY. The GLDY permission pool operates in three stages: All investor wallets are frozen by default; only wallets that pass Streamex's KYC verification are automatically thawed by the on-chain access control layer; thawed wallets then engage in peer-to-peer real-time trading within the Orca AMM pool, requiring no broker or manual review. Unlike traditional gold investment products limited by exchange trading hours, GLDY trades 24/7 on Solana, with yield from Monetary Metals' gold leasing contracts paid directly to GLDY holders.

This token-level freeze/thaw control mechanism is not limited to gold. It is directly applicable to any regulated asset, such as Treasuries, corporate bonds, and private credit. This is precisely why Orca proposed this structure as the trading infrastructure proposition for the Project Open pilot framework.

Apollo: Private Credit Tokenization (ACRED). Despite high yields, the traditional private loan market has two major structural barriers: high minimum investment amounts limiting access to institutions and ultra-high-net-worth individuals, and illiquidity, as capital is locked in until maturity. In January