白天看海力士,晚上炒美股:全球 AI 行情的新「亚盘风向标」?

- Core Thesis: As a leading AI memory stock traded during Asian hours, SK Hynix's stock price fluctuations have become a leading indicator for the US tech sector (especially the Philadelphia Semiconductor Index). This stems from its core position across the entire AI memory supply chain, including HBM, DRAM, NAND, and enterprise SSDs. Furthermore, its US listing is expected to drive a valuation re-rating from a "Korean cyclical stock" to a "global AI infrastructure asset."

- Key Factors:

- Data Validation: When SK Hynix rises by over 1% in a single day, the probability of the Philadelphia Semiconductor Index rising that evening is 77.1%. This correlation is particularly pronounced during the US market's opening gap, indicating its signal has a direct and significant impact on the US market's opening price.

- Industry Position: SK Hynix holds approximately a 58% market share in global HBM, making it a core supplier to NVIDIA. By acquiring Intel's NAND business, it has built a complete AI memory chain spanning HBM, DRAM, NAND, and enterprise SSDs.

- US Listing: SK Hynix plans to list on Nasdaq in July 2025, aiming to raise approximately USD 29.4 billion. This would be one of the largest stock offerings in global history, intended to resolve the "Korea Discount" issue and lower the barrier to entry for international investors.

- Valuation Reset: In the US market, SK Hynix will be directly compared with companies like Micron and could be re-categorized as a "global AI infrastructure asset" rather than a traditional memory cyclical stock, potentially commanding a higher valuation multiple.

- Long-term Challenges: SK Hynix must maintain its technological lead in next-generation HBM (HBM4), prove the sustainability of high HBM profit margins, and successfully develop Solidigm into a second growth engine to support its new narrative.

In the past month, observing the Korean and US stock markets side-by-side reveals a rather interesting phenomenon.

SK Hynix during the Asian trading session increasingly resembles an early preview for the AI sector on Wall Street that night: If it surges during the day, NVIDIA, Micron, and the Philadelphia Semiconductor Index often gap up in the evening; if it pulls back first, US tech stocks are highly likely to cool down in tandem.

This co-movement has become particularly intuitive against the backdrop of recent sharp global tech stock volatility.

The latest example occurred this morning after the US market close. Micron (MU) released blockbuster earnings and guidance that significantly exceeded expectations. When the Korean market opened, SK Hynix quickly absorbed this memory sector sentiment, surging over 10% during intraday trading.

Of course, it would be inaccurate to simply summarize this phenomenon as "SK Hynix up, US stocks up." After all, a trillion-dollar stock alone is unlikely to dictate the direction of a multi-trillion-dollar US capital market.

However, as global capital trades on the same set of AI expectations, an increasingly clear cross-market pricing chain has formed. SK Hynix happens to be the most sensitive 'thermometer' within this chain.

This raises a more pertinent question: Why SK Hynix? How did it become the go-to 'Asian session bellwether' for global AI trading? And with SK Hynix formally advancing its US listing, how will Wall Street re-price it?

1. SK Hynix Up by Day, US Stocks Up by Night: Is It Just Folklore?

From a trading time perspective, the Korean market, operating in the Asian session, naturally sits between the previous night's US market close and the next US market open.

This means that when the Korean market opens, investors have already processed the previous night's US market performance and can simultaneously trade on new post-market earnings reports and macroeconomic developments.

When the Korean market closes, US investors, in turn, reference the performance of Asian semiconductor companies, along with US pre-market trading and equity index futures, to gauge risk appetite for the day ahead.

Therefore, theoretically, a relay pricing chain spanning two trading time zones exists between SK Hynix and US stocks: US stocks first set the baseline sentiment the previous night. SK Hynix confirms or corrects this sentiment during the Asian session. US stocks then absorb the incremental information released by the Asian market at the next opening.

To verify this intuition, MSX Maxton back-tested the co-movement rate, correlation, and conditional hit rate between SK Hynix and major US indices, using common trading days for the Korean and US markets as the sample.

First, looking at the up/down direction over the past month, the co-movement rate between SK Hynix and the Philadelphia Semiconductor Index (SOX) reached 70%. This means that on 14 out of 20 common trading days, they moved in the same direction.

In comparison, the co-movement rate was 65% with the NASDAQ Composite Index, 60% with QQQ, and 55% with the S&P 500 ETF.

This result primarily indicates that SK Hynix is not a broad-based signal equally effective for all US stocks. Instead, it exhibits a clear industry gradient. For instance, the strongest co-movement is with the SOX, followed by tech-heavy indices like the NASDAQ and QQQ, and finally, the spillover effect reaches the broader-market S&P 500.

This aligns perfectly with SK Hynix's industrial characteristics.

Capital first trades memory and semiconductor sentiment through SK Hynix. This risk appetite then transmits to the entire AI tech sector. Only when the market trend is strong enough and the impact broad enough does it further spill over to the broader US market.

In other words, SK Hynix acts more like a semiconductor sentiment outpost than a macro-level predictor for the broad US market.

Examining the daily return correlation over the past three months reveals this same industry gradient. The correlation coefficient between SK Hynix and the SOX is 0.363, with QQQ it's 0.344, and with the NASDAQ Composite Index it's 0.313.

It's crucial to clarify that these numbers do not mean a 1% rise in SK Hynix will mechanically trigger a 0.363% rise in the SOX. Rather, they measure the degree to which the two return series move in the same direction over the sample period – a value closer to 1 indicates they are more likely to rise or fall together; closer to 0 indicates a weaker linear relationship.

Realistically, a value between 0.3 and 0.4 is only a moderate positive correlation. However, considering the significant noise in daily financial market data, this is already a strong and highly valuable signal.

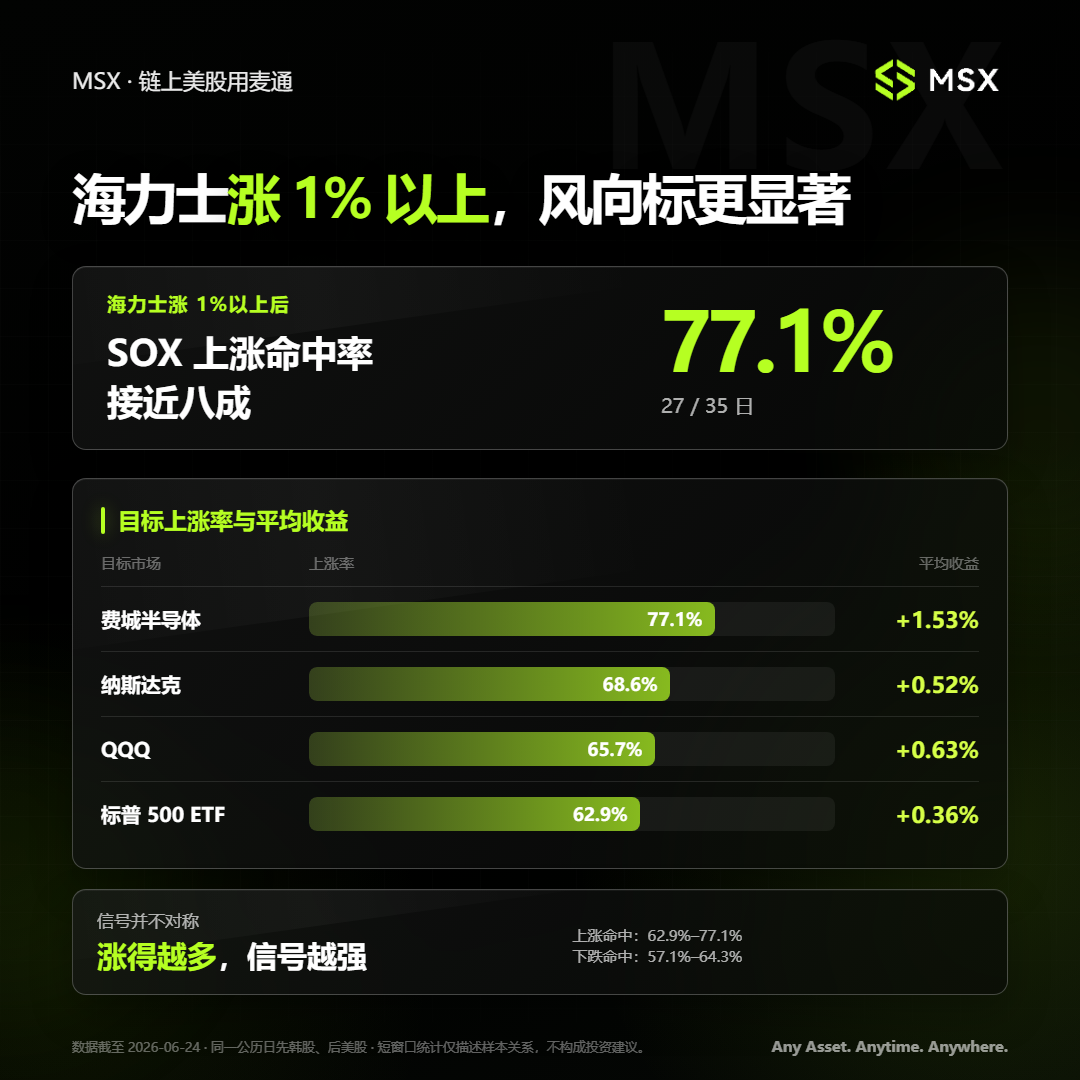

For this reason, MSX further cleaned and filtered the data, discovering a distinct "strong volatility trigger" characteristic. When SK Hynix rose more than 1% in a single day, the probability of the SOX rising that night reached 77.1%. In 27 out of 35 qualifying instances, the SOX recorded a gain, with an average return of 1.53%.

Under the same condition:

- The NASDAQ Composite Index's probability of rising was 68.6%, with an average return of 0.52%;

- QQQ's probability of rising was 65.7%, with an average return of 0.63%;

- The S&P 500 ETF's probability of rising was 62.9%, with an average return of 0.36%;

These results are undoubtedly more explanatory than simple directional co-movement rates.

When SK Hynix only fluctuates slightly, the movement may be mixed with significant noise from domestic Korean capital, currency fluctuations, and index weight adjustments. However, when it surges over 1% in a single day, it often means the market is focusing on a clearer, more substantial industry signal.

More interestingly, this signal is not perfectly symmetrical. In the current sample period, when SK Hynix significantly rose, the probability of subsequent US index gains ranged from 62.9% to 77.1%. In contrast, when SK Hynix significantly fell, the probability of US index declines was only between 57.1% and 64.3%.

This suggests that, at least in the current sample period, SK Hynix's upward signal is temporarily more stable than its downward signal.

This could be related to the sample period coinciding with an upward phase in the AI memory cycle. In a market where capital seeks long opportunities in AI, a strong rise in SK Hynix is more easily interpreted as reconfirmed industrial demand, similar to the direct catalyst of Micron's earnings today.

A decline in SK Hynix, however, could stem from short-term profit-taking, technical adjustments in the Korean market, or stock-specific capital flows, not necessarily signaling a synchronous deterioration in global AI fundamentals.

The third set of data further reveals the specific timing when the SK Hynix signal plays its role.

If we decompose the daily US stock returns into two components:

- Opening Gap: The change from the previous day's closing price to the current day's opening price;

- Intraday Return after Open: The change from the current day's opening price to the closing price;

We find that the correlation between SK Hynix and US stocks is almost entirely concentrated in the opening gap phase.

Specifically, the correlation coefficient between SK Hynix's daily return and the SOX's opening gap is 0.497. With QQQ it's 0.483, with the NASDAQ Composite Index it's 0.435, and with the S&P 500 ETF it's 0.405.

As mentioned earlier, a correlation coefficient close to 0.5 in noisy daily cross-market returns implies that the stronger SK Hynix's performance during the day, the higher the probability that the SOX and QQQ will open higher that night. The weaker SK Hynix's performance, the more likely US semiconductor and tech stocks will open lower.

However, once the US market truly opens, this connection almost instantly dissipates. The correlation between SK Hynix's daily return and the SOX's intraday return is only 0.051. With QQQ it's 0.055, with the NASDAQ Composite Index it's 0.054, and with the S&P 500 ETF it's 0.081 – essentially near zero.

The stark contrast between these two phases indicates that the information revealed by SK Hynix during the Asian session is primarily absorbed by the US market in one go at the opening price. Once the US market opens, domestic data, news, and intraday liquidity take over the pricing process, and SK Hynix's explanatory power rapidly diminishes.

Combining these three sets of data, we can construct a relatively complete transmission chain:

SK Hynix first confirms memory and semiconductor sentiment. The SOX most directly inherits this at the US market open. This influence then diffuses to QQQ and the NASDAQ. Finally, it may transmit to the S&P 500. In this chain, the SOX verifies the industry-specific nature of the signal, QQQ and the NASDAQ observe whether it has spread to the main AI narrative of the US market, and the S&P 500 serves as a broad-market benchmark for comparison.

From this perspective, the co-movement between SK Hynix and the US AI sector doesn't imply the former unilaterally "drives" the latter. Instead, it seems like two markets continuously pricing the same set of industrial variables across different timeframes.

SK Hynix gains its temporal lead by opening first. Due to its central position in the AI memory supply chain, it possesses a higher information density than average Asian tech stocks.

This brings us to the core question: Why is SK Hynix the one capable of playing this role?

2. Why SK Hynix Specifically?

The fundamental reason SK Hynix can hold this market position is not merely that the Korean market opens earlier. It has effectively become one of the 'critical few' that is hard to bypass in the AI infrastructure landscape.

As is well known, over the past few years, market discussions about AI typically started with GPUs.

NVIDIA provides the computing power, cloud providers build data centers, and power, networking, optical communications, and liquid cooling ensure the stable operation of computing clusters. Within this narrative, memory, though equally important, was long viewed as a relatively traditional cyclical component.

But as model scale, training data, and inference demands continue to grow, the problem facing AI systems is no longer simply 'having enough GPUs,' which led to the redefinition of memory's role in AI:

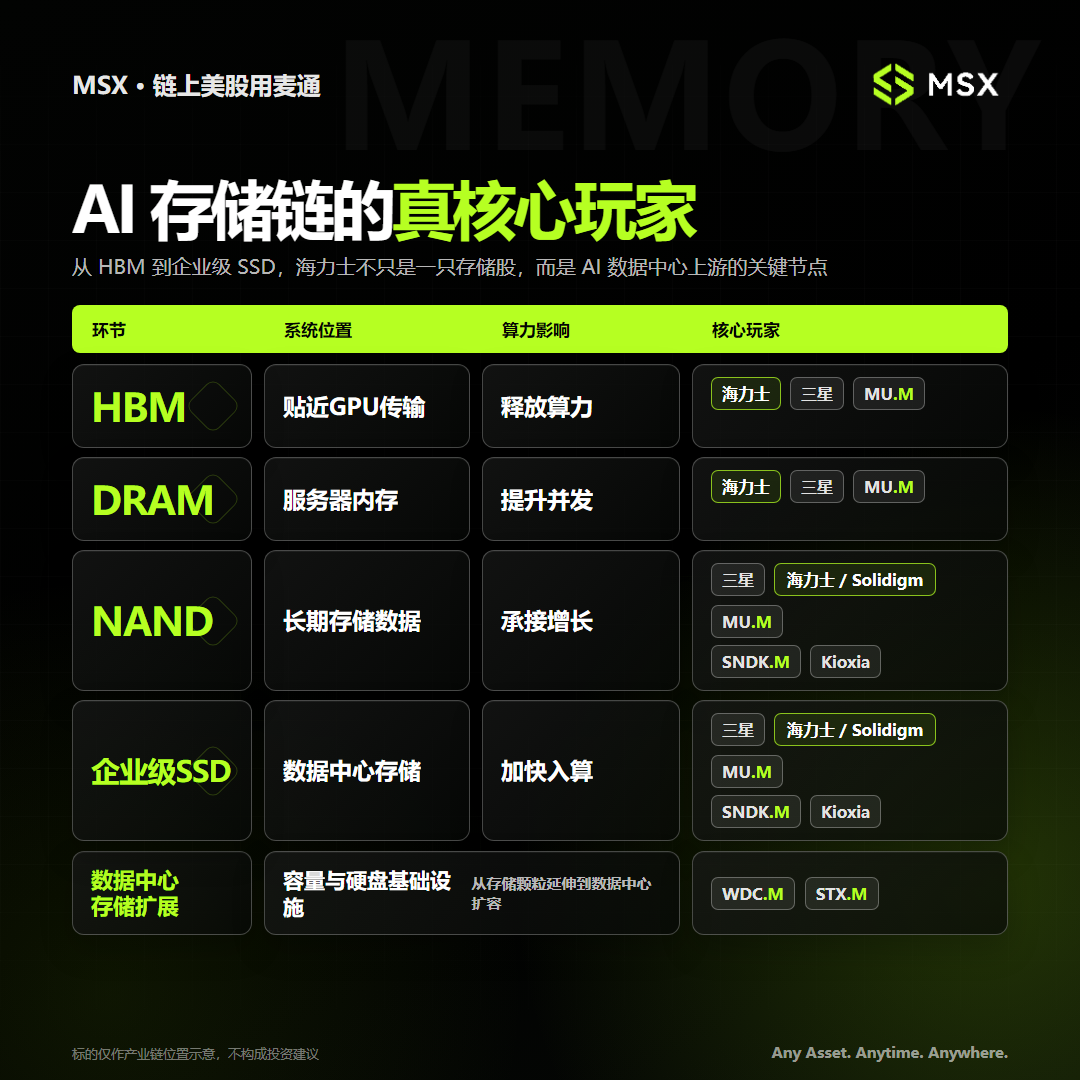

- HBM sits right next to the GPU, responsible for high-speed data transfer, determining whether expensive AI chips can fully unleash their computing power;

- Server DRAM acts as working memory, impacting server concurrency capacity and task throughput;

- NAND handles the long-term storage of models, training data, and inference data, absorbing the overall growth in data volume driven by AI;

- Enterprise SSDs reside in the data center storage layer, accelerating data transfer into computing systems through higher capacity and faster read speeds;

To put it more directly: GPUs determine 'whether you can compute,' HBM determines 'whether computing power can be fully utilized,' DRAM determines 'how many tasks can be processed simultaneously,' and NAND and enterprise SSDs determine 'where massive data is stored and how quickly it can be accessed.'

And SK Hynix runs through virtually every layer of this AI memory chain, achieving a 'grand slam.'

In the HBM field, SK Hynix remains one of the world's most critical suppliers. As of Q1 2026, SK Hynix held approximately a 58% share of the global HBM market, with Samsung and Micron each accounting for about 21%. It is also one of NVIDIA's most important HBM suppliers for its AI accelerators.

The biggest difference between HBM and traditional standardized memory is that HBM is difficult for customers to easily substitute.

At the same time, SK Hynix is more than just an HBM company. Back in 2020, it announced the acquisition of Intel's NAND and SSD business for approximately $9 billion. It completed the first phase of the transaction in 2021, establishing Solidigm, a US-based company focused on enterprise SSDs and data center storage. In March 2025, both parties completed the second phase, with the remaining Intel NAND technology, intellectual property, and related personnel officially transferring, finally closing the multi-year acquisition.

This deal not only filled a critical gap in SK Hynix's enterprise storage capabilities but also gave it two interconnected yet distinct growth trajectories:

- One trajectory revolves around HBM and server DRAM, participating in the expansion of AI accelerators and servers;

- The other revolves around NAND and enterprise SSDs, capturing demand from training data, model weights, inference caching, and data center storage;

Essentially, SK Hynix today is like a high-purity AI memory asset. Its profits, capital expenditures, and market expectations are all tightly coupled with the memory cycle's momentum.

This business concentration undoubtedly maximizes its stock price sensitivity. Thus, the three conditions for SK Hynix becoming the Asian session bellwether form a closed loop:

- First, it holds the time advantage by opening earlier, absorbing Asian session information before the US market opens;

- Second, it is sufficiently central to the industry, spanning the four-layer memory chain of HBM, DRAM, NAND, and enterprise SSDs;

- Third, the purity of its business and the high elasticity of its stock price allow it to quickly amplify global capital's assessment of the AI memory cycle;

Therefore, when SK Hynix experiences significant volatility, the market is not just trading the rise or fall of a single Korean company. It is trading on whether AI server shipments can continue to grow, whether memory supply remains tight, and whether global capital is willing to pay higher valuations for AI hardware.

However, the crux of the issue is that SK Hynix's past capital identity, largely confined to the Korean market, has not quite kept pace with its evolving global industrial status.

Its latest push for a US listing is precisely an attempt to change this.

3. US Listing: Changing More Than Just the Trading Venue

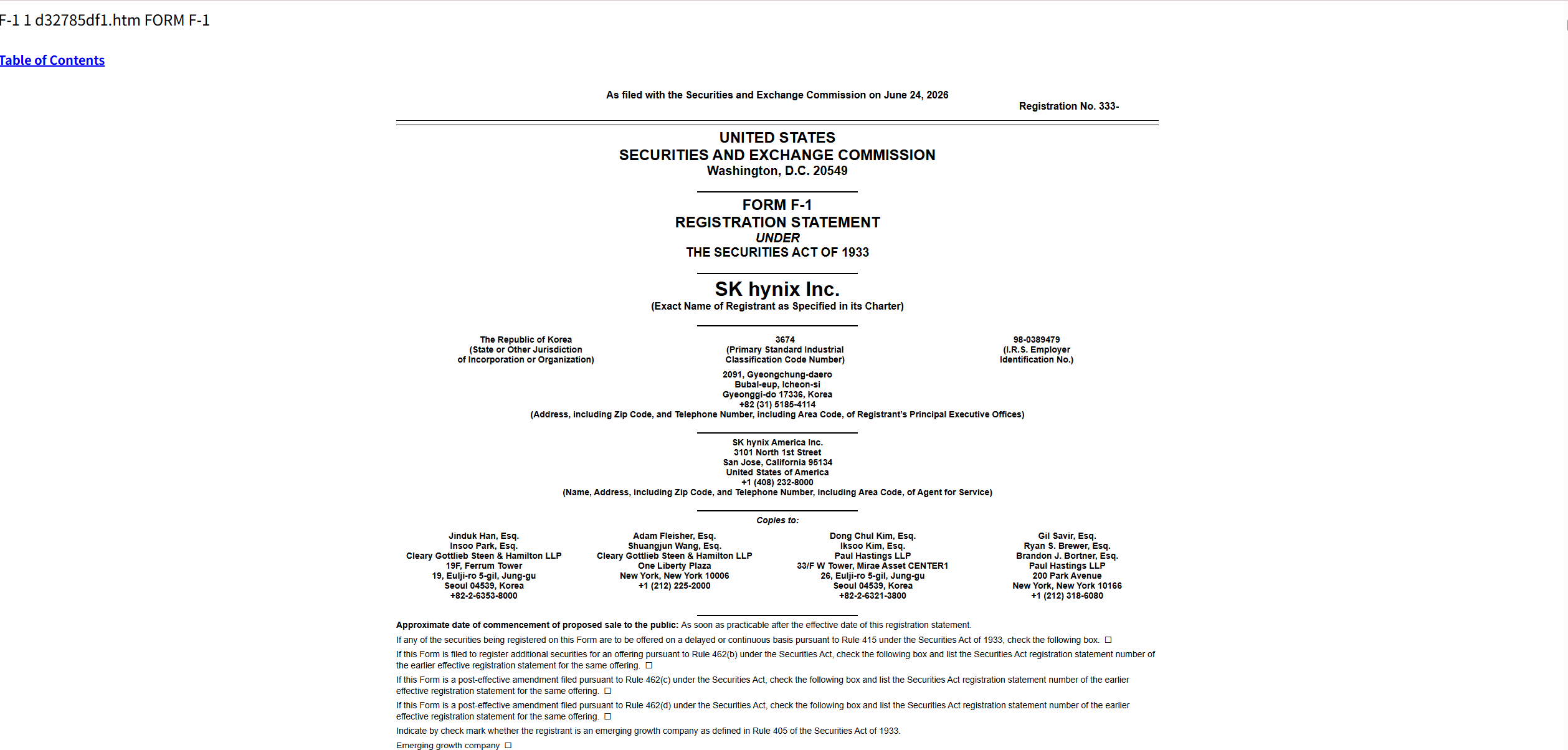

Coincidentally, on June 24, SK Hynix publicly filed an F-1 registration statement with the U.S. Securities and Exchange Commission (SEC), formally advancing its NASDAQ ADR listing under the proposed ticker symbol "SKHY."

According to the currently disclosed plan, SK Hynix aims to issue up to 17.79 million new common shares. The potential fundraising size is estimated at approximately $29.4 billion, with a planned listing on NASDAQ as early as July 10.

If completed at the current indicative price, this would become one of the largest stock issuances in the history of global capital markets – surpassing the approximately $25.6 billion issuances of Alibaba in 2014 and Saudi Aramco in 2019. It would rank second only to SpaceX's record of $85.7 billion set in mid-June.

In other words, had SpaceX not set a new record earlier in June, SK Hynix itself would have had the chance to become the world's largest stock issuance.

It's important to note that SK Hynix's US listing is not a traditional IPO for a company that has never been public. SK Hynix is already listed in South Korea and is conducting a secondary listing in the US via ADRs while issuing new shares.

Theoretically, changing the trading venue does not magically create new revenue or profit. Beyond raising capital, the business itself seems unlikely to change immediately.

However, capital markets don't just price current profits. What the US listing could truly change is the scope of its investor base, its liquidity, its ability to raise capital, and the narrative framework the market applies to it.

The most direct change is that SK Hynix may undergo a transformation in identity from a 'Korean memory cycle stock' to a 'global AI infrastructure asset.'

Historically, many large South Korean companies, including SK Hynix, have been subject to the so-called 'Korea Discount.' Factors like complex conglomerate governance structures, foreign exchange risk, limited market liquidity, and barriers for international capital entry mean that even globally competitive Korean companies often struggle to achieve valuations comparable to their US counterparts