Tiger Research: Cryptocurrency Payment Cards Generating $1.5 Billion Monthly in Transactions, Still Stuck in the 1990s

- Core Insight: The current cryptocurrency payment card industry handles approximately $180 billion in annual transaction volume, but users are concentrated in emerging markets. It has not yet established normalized financial account relationships such as payroll direct deposit and automatic bill payments. Its development stage is similar to that of debit cards in the 1990s before commercialization—a supplementary tool rather than a universal financial infrastructure.

- Key Elements:

- High Industry Concentration: The leading service provider, RedotPay, holds over half of the market share. Its users are primarily from underbanked regions such as Bangladesh, India, and Egypt, with the United States accounting for only 4%.

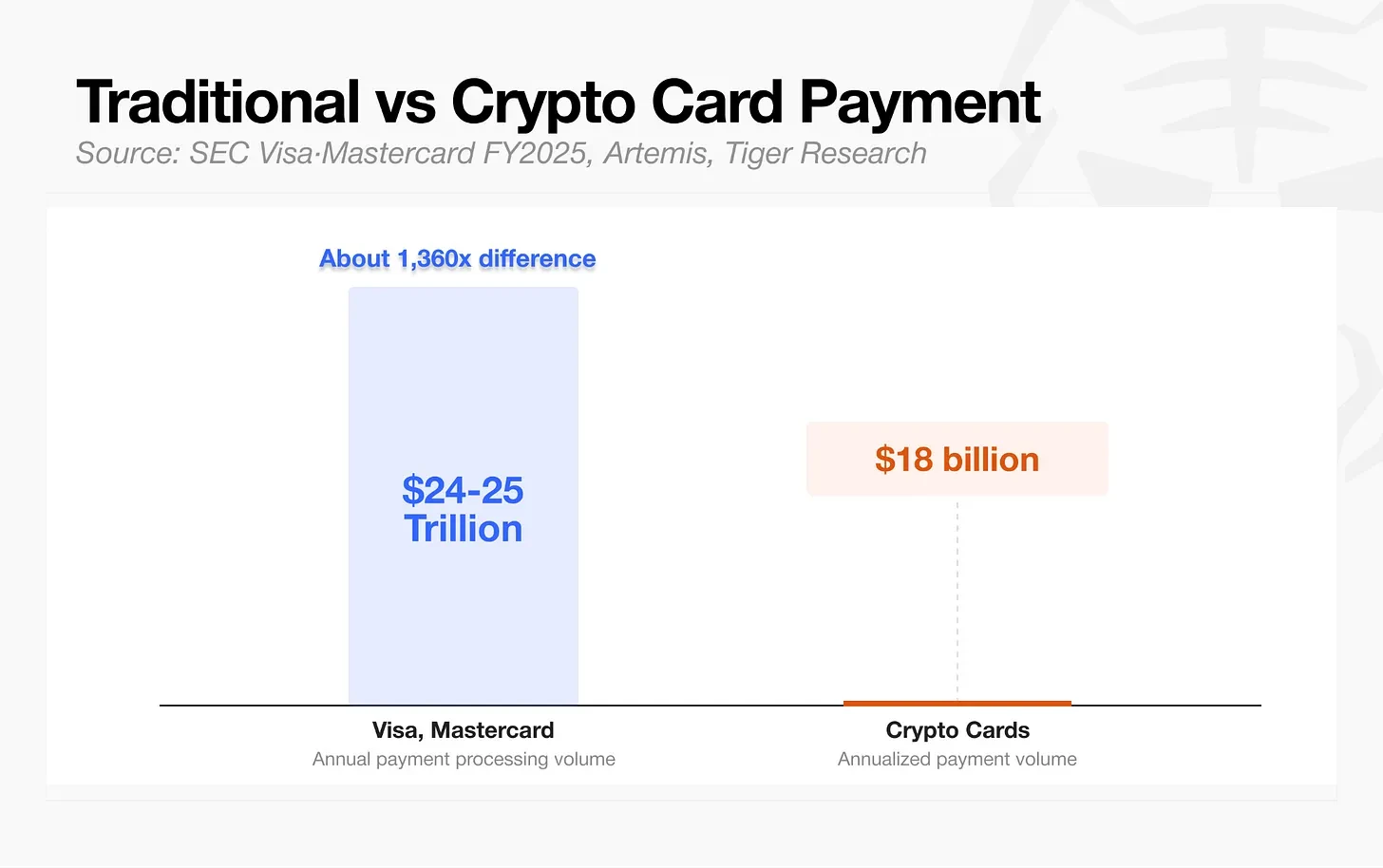

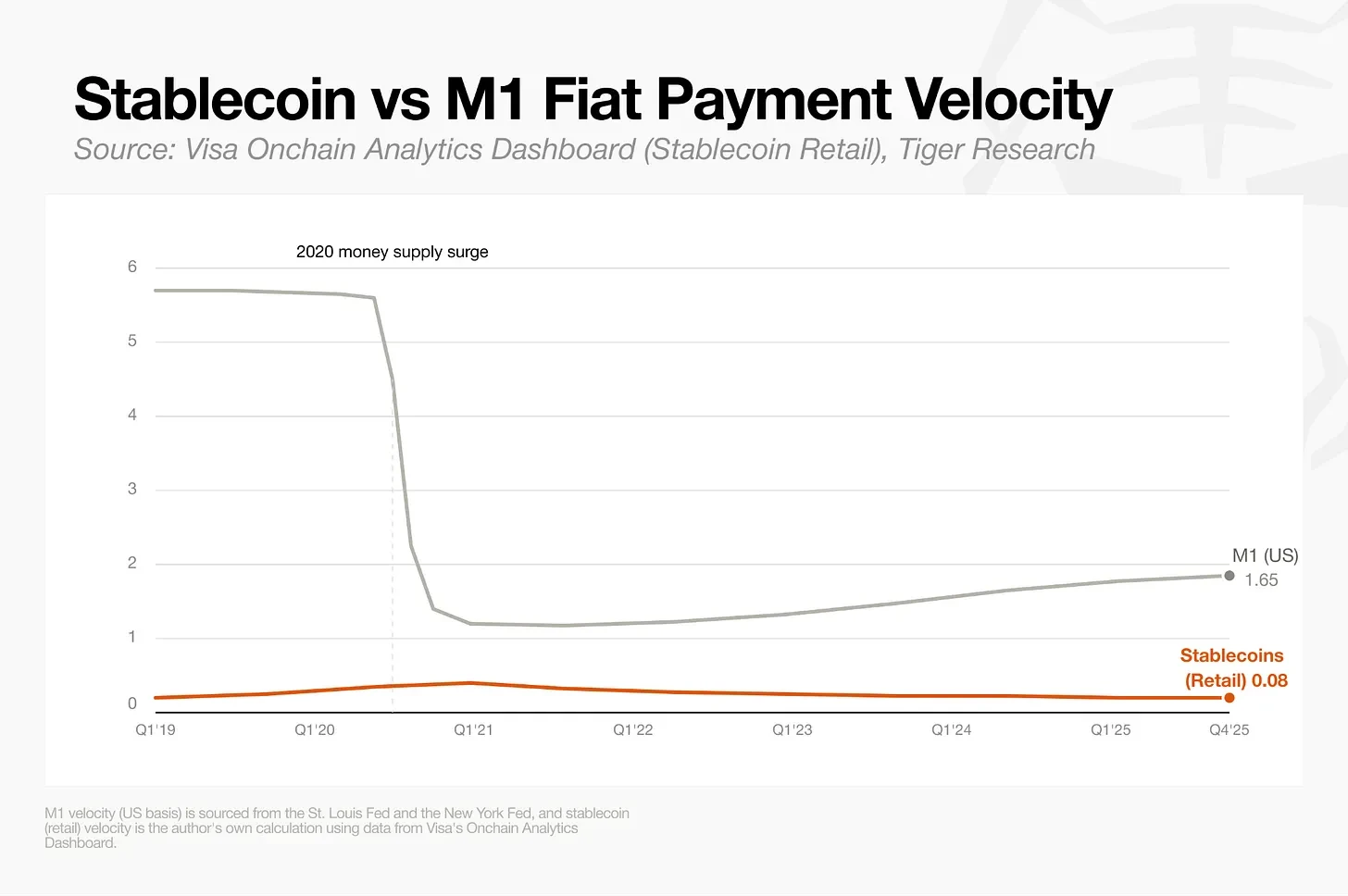

- Huge Gap with Traditional Payment Scale: Visa and Mastercard process annual payment volumes of $24-25 trillion, while cryptocurrency payment cards only account for $180 billion. The retail circulation velocity of stablecoins (0.08) is only one-twentieth that of fiat narrow money (1.65).

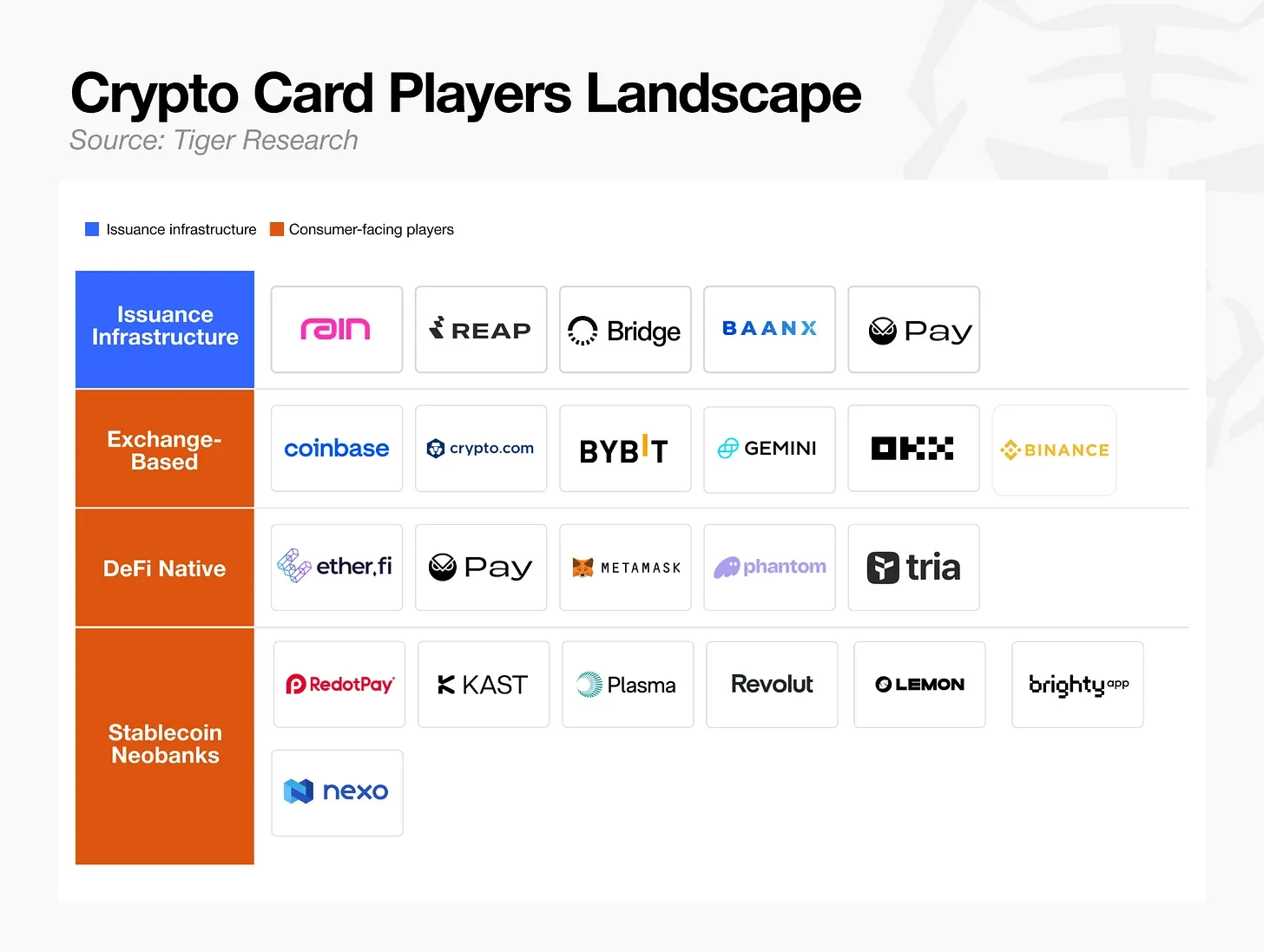

- Four Types of Business Models: Card issuance infrastructure (e.g., Rain), exchange-affiliated cards, decentralized wallet cards (e.g., MetaMask Card), and stablecoin digital banks (e.g., RedotPay). Each model faces different challenges.

- Regulatory Constraints on Development: The U.S. GENIUS Stablecoin Act prohibits interest-bearing stablecoin businesses, while regulations like the EU's MiCA restrict asset management, hindering the industry from breaking through the pure payment profit ceiling.

- Key to Industry Success: Companies need to directly control the flow of funds, secure unique use cases in emerging markets, and build their own user account systems, rather than merely competing on card issuance volume or transaction volume.

Key Takeaways

- This article from Tiger Research suggests that the current state of crypto payment cards is analogous to debit cards in the early 1990s, just before commercialization: both leverage existing payment networks to bypass merchant acceptance. However, the daily financial relationships built around primary bank accounts (e.g., payroll deposits, recurring payments) have yet to be formed.

- The annual transaction volume of crypto payment cards is approximately $18 billion, with RedotPay alone holding over half of the market share, and users concentrated in emerging markets. At this stage, crypto payment cards are merely supplementary tools in regions lacking access to the US dollar, far from becoming a universal financial infrastructure.

- Infrastructure status for crypto payment cards cannot be established by transaction volume growth alone. The market landscape will ultimately be determined by three types of players: platforms controlling capital flow, service providers covering areas underserved by traditional finance, and enterprises building core daily account relationships on top of underlying payment systems.

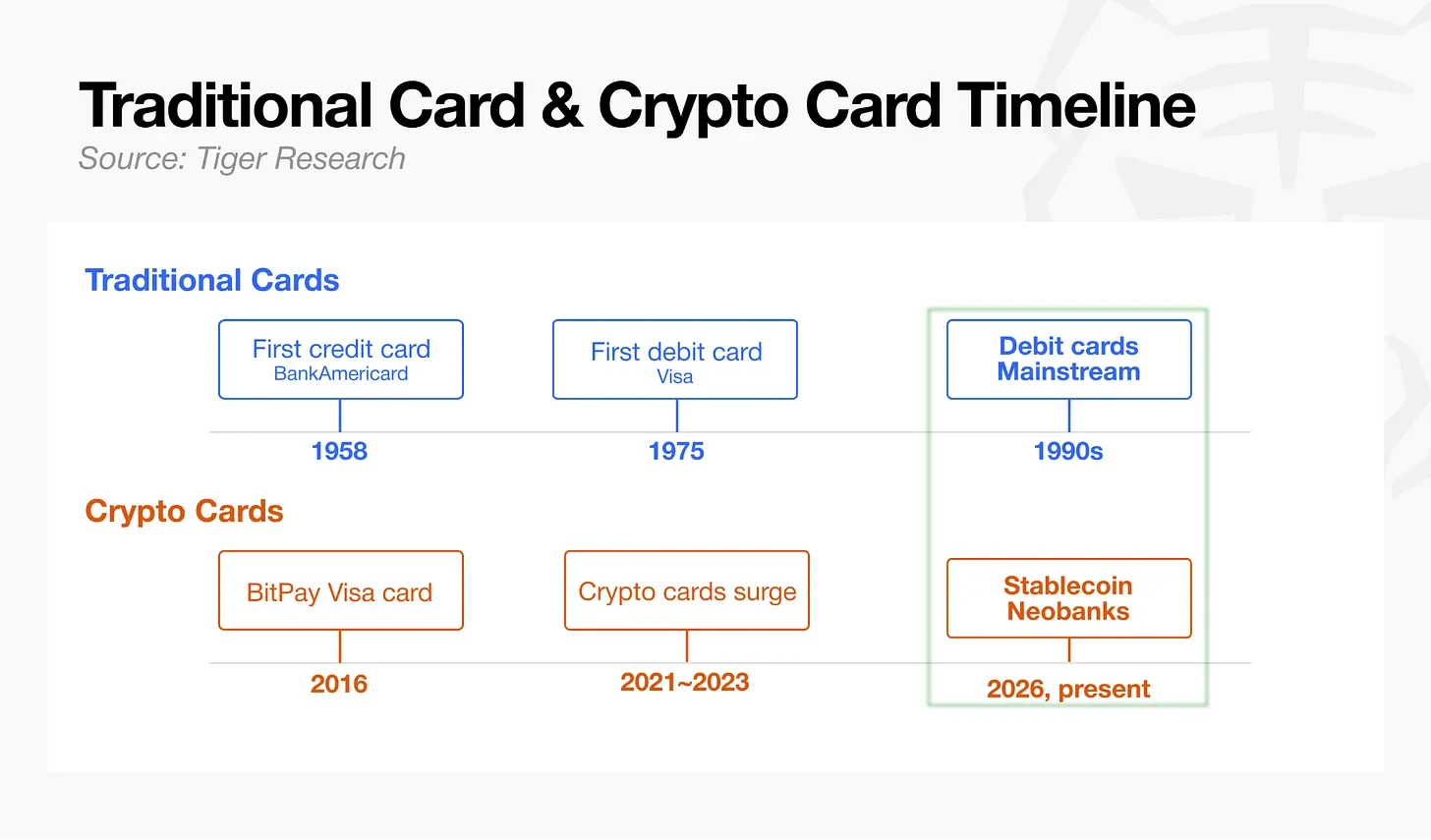

A Parallel Universe to the 1990s Debit Card

In September 1958, Bank of America mass-mailed credit cards to 65,000 residents of Fresno, California, marking the first payment card without underlying infrastructure. A year after launch, business was sluggish, with a 22% delinquency rate and losses reaching $20 million. The industry took 15 years to build an electronic clearing system, debit cards didn't officially appear until 17 years later, and Visa spent a full 20 years establishing a global universal payment standard.

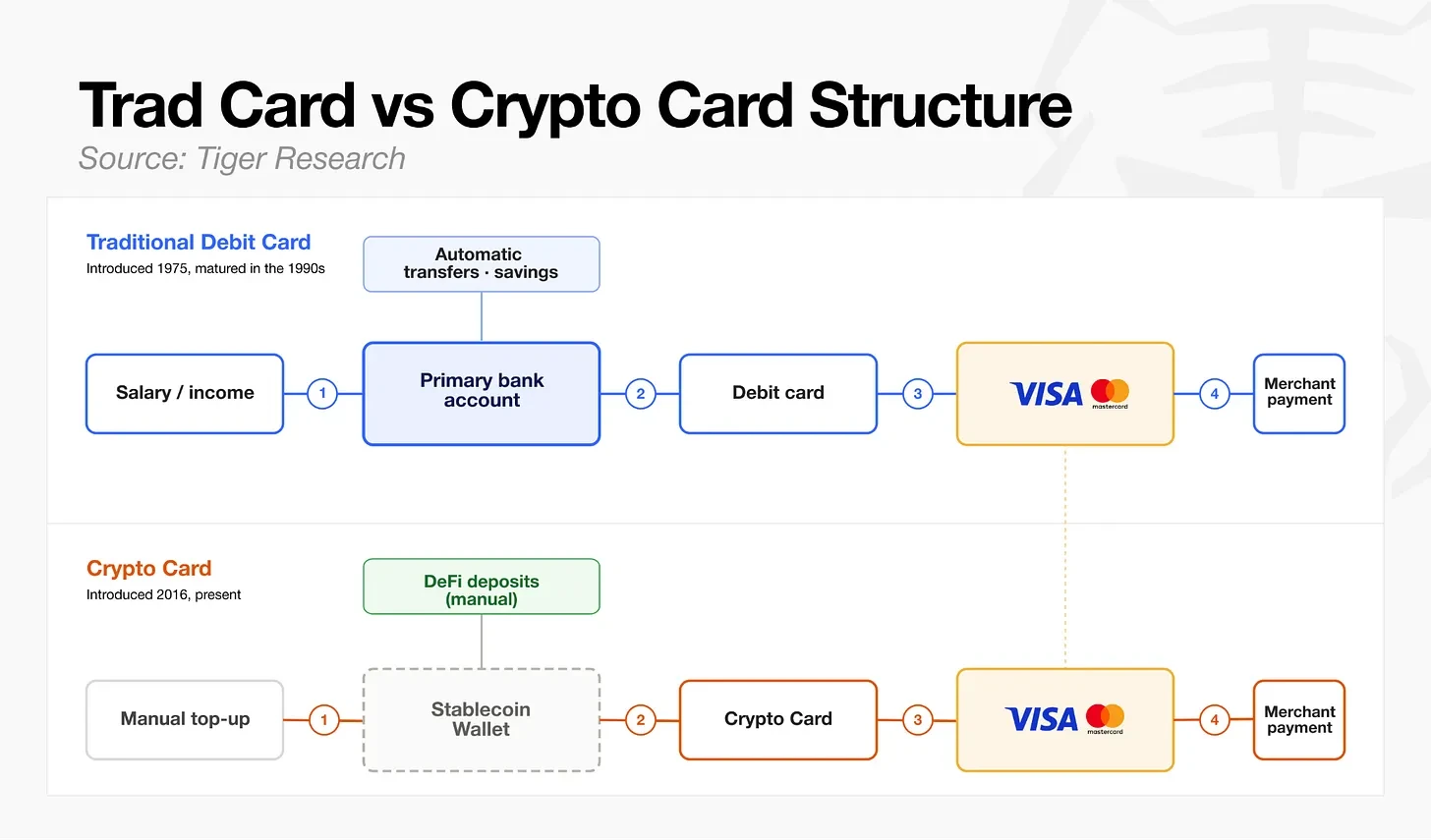

The biggest watershed between traditional payments and crypto payments lies in whether a normalized user financial account relationship is established. Debit cards were born in 1975, but only became a standard tool for personal primary bank accounts with the普及 of payroll direct deposit in the 1990s. In contrast, today's crypto payment cards primarily rely on users self-funding with stablecoins; the vast majority of crypto wallets cannot handle routine financial flows like salary deposits and recurring deductions. The overall development stage of the industry is roughly equivalent to that of debit cards around 1990.

The future leader in the crypto payment card space won't be determined by the number of cards issued, but by who first builds a core account truly serving daily income and expenses, or finds a growth fulcrum driving long-term user retention.

$1.5 Billion in Monthly Transactions Doesn't Mean Industry Maturity

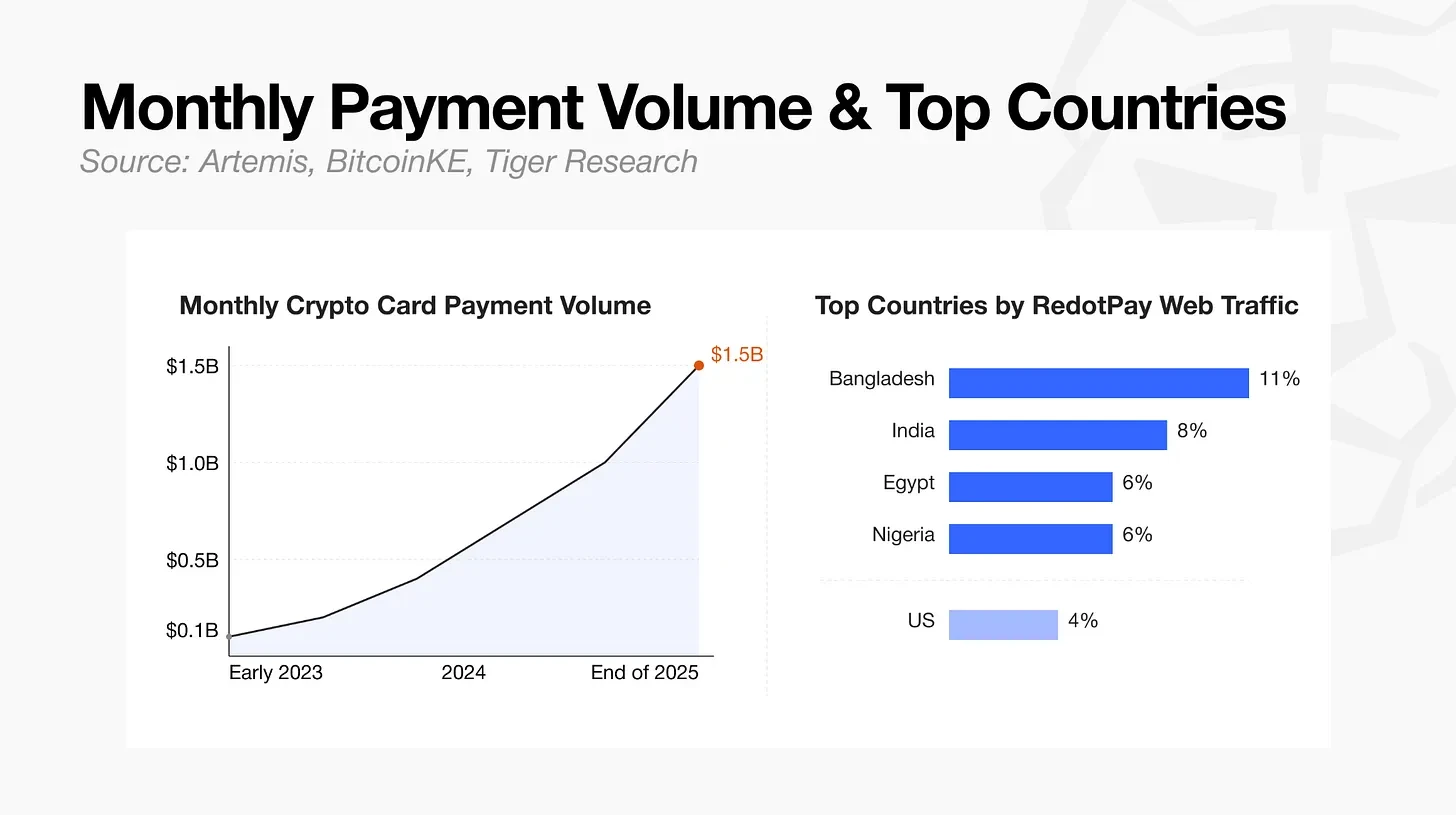

Data from Artemis shows that the monthly transaction volume of crypto payment cards grew from $100 million in early 2023 to $1.5 billion by the end of 2025, with an annualized scale of approximately $18 billion. Due to on-chain data measurement differences, the actual annualized figure may fluctuate slightly, but the explosive growth in transaction volume is a fact.

Examining these indicators closely reveals a clear concentration of services and geographic regions. The leading provider, RedotPay, accounts for over half of the industry's total transaction traffic; platform user access is highly concentrated in emerging markets, with Bangladesh at 11%, India 8%, Egypt 6%, Nigeria 6%, and the US only 4%.

Thus, the real demand for crypto payment cards doesn't come from developed mainstream markets, but from developing regions with inadequate financial services and limited access to US dollars.

Compared to mature financial networks, the scale gap for cryptocurrencies remains enormous. Visa and Mastercard handle a total annual payment volume of $24 to $25 trillion, while crypto payment cards have an annualized transaction volume of just $18 billion – the two are not on the same magnitude at all.

The velocity indicator, measuring the普及程度 of daily payments, is also relatively low. Visa's data shows the retail velocity of on-chain stablecoins is only 0.08, one-twentieth of the narrow money M1 velocity (1.65). Users' pattern of using stablecoins is not a normalized process of payroll deposit, daily spending, and top-up, but rather sporadic card usage after a one-time top-up.

Growth in transaction volume figures does not equal a mature, universal clearing system in the market. Currently, a large portion of crypto payment card transactions come from users in emerging markets who cannot easily open USD bank accounts. For these users, crypto cards indeed offer practical financial value.

However, in developed markets, crypto payment cards have yet to find a stable product-market fit, nor have they established the deep account binding relationships brought by payroll deposits and automatic bill payments.

Considering the channels of capital inflow and spending scenarios holistically, today's crypto payment cards are more suited to specific country-level niche demands. They are supplementary tools, not universal financial infrastructure. Nevertheless, amid the industry's rapid growth, the top players across four main business models are simultaneously improving the value chain across various stages.

Four Main Business Models for Crypto Payment Cards

The crypto card industry can be broadly categorized into four business models, with various participants competing for an edge at different levels. These models vary in form, from companies focused on providing backend infrastructure to those that only use the card form factor but have completely different underlying structures.

Card Issuing Infrastructure

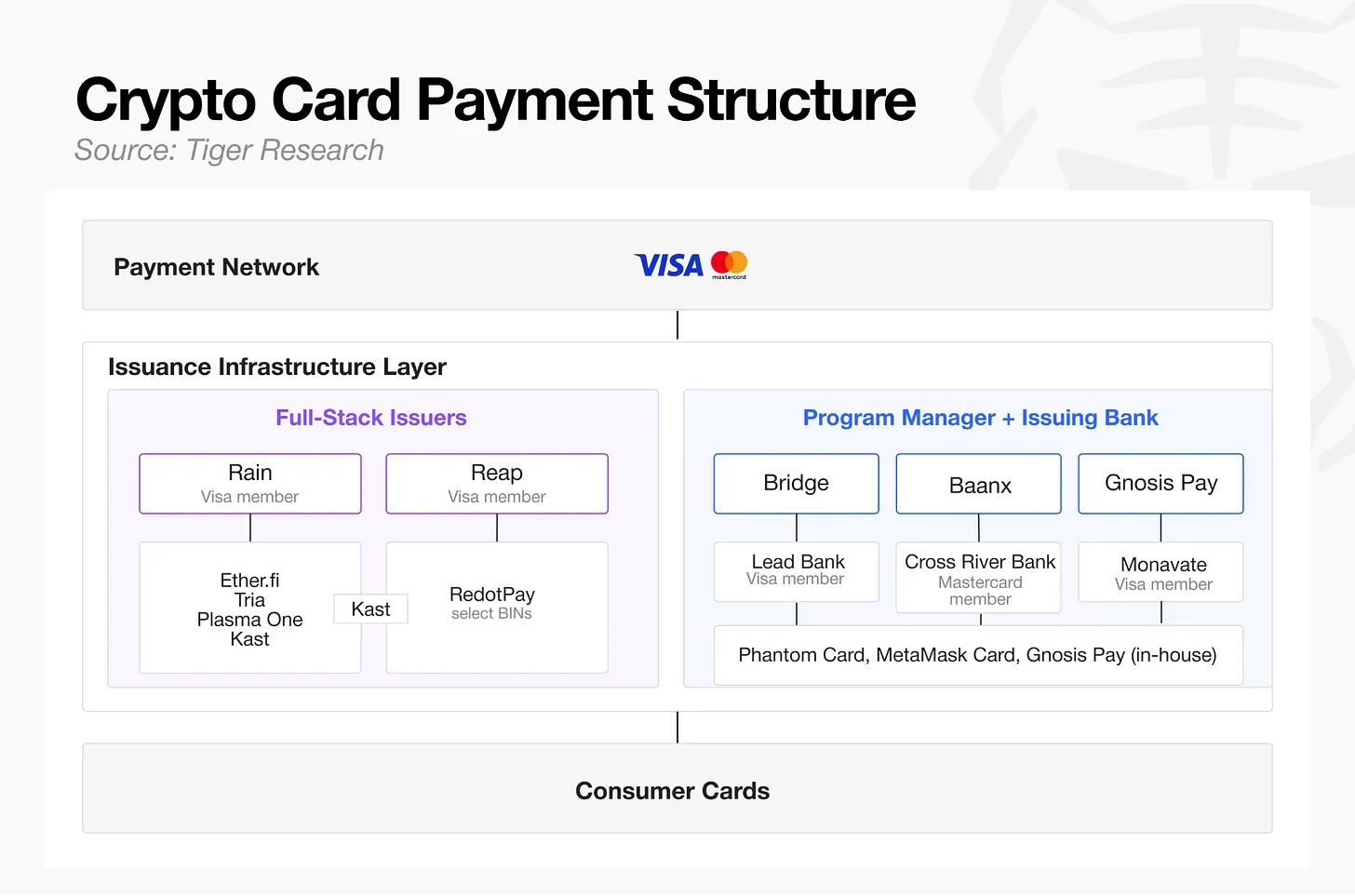

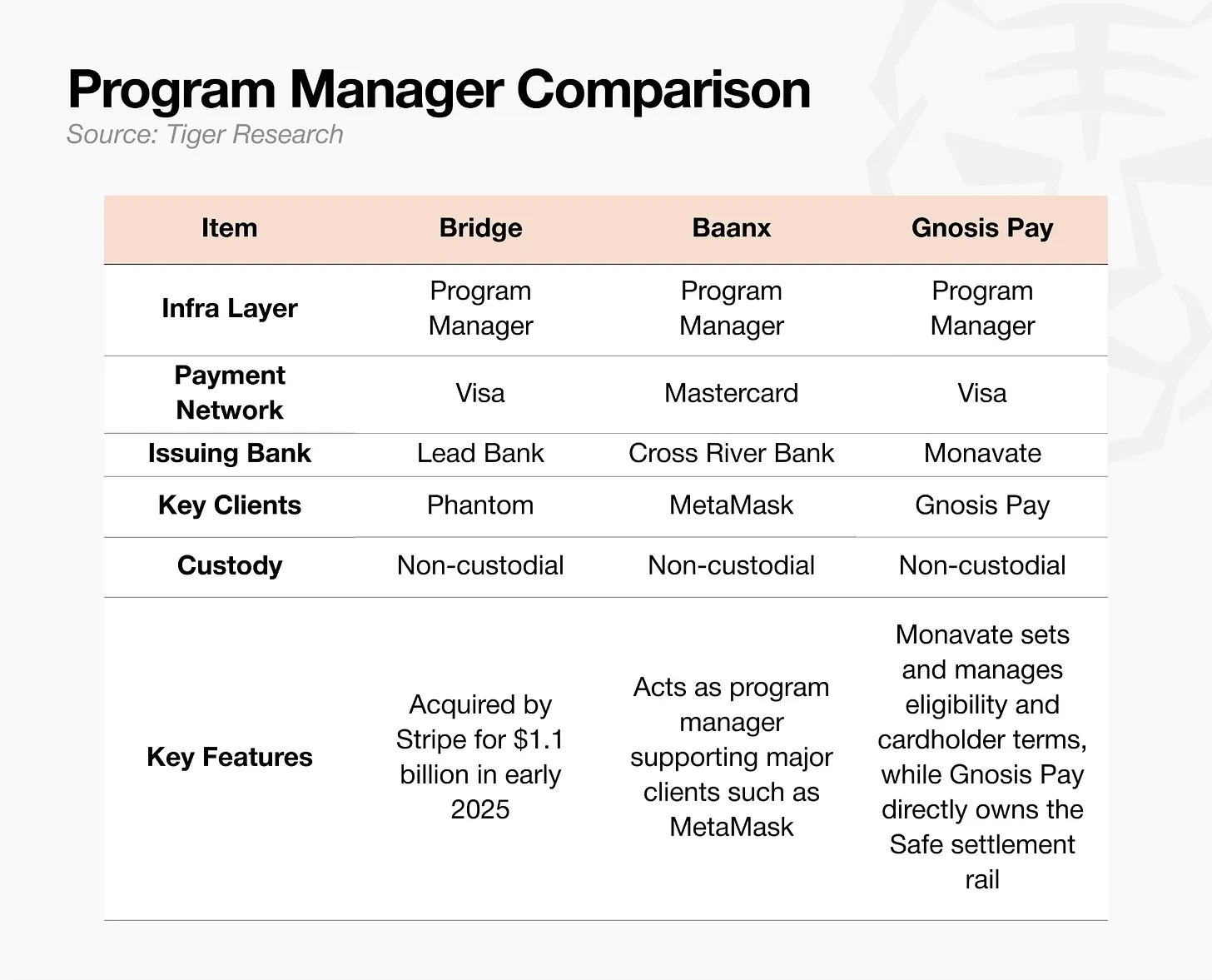

Visa and Mastercard, the two prominent payment networks, also underpin the cryptocurrency card ecosystem. Below them lies the card issuing infrastructure layer, which ultimately connects to consumer cards. As shown in the diagram above, there are two structures within the issuing infrastructure layer. The first is a traditional two-tier structure, where the project manager handling operations is separate from the issuing bank responsible for member management and settlement. The second is a full-stack issuing institution, like Rain and Reap, which combines these two roles into one.

Many seemingly independent payment card brands rely on just a few project service providers at the backend. Phantom Card, MetaMask Card, and Gnosis Pay are typical examples.

Seemingly independent payment card products like Kast, Ether.fi, Tria, and Plasma One also share a small number of backend infrastructure providers. Rain handles the vast majority of consumer-level card business.

The highly concentrated nature of card issuing infrastructure has attracted traditional digital banks with mature experience to enter the space. In March 2026, Nium launched a stablecoin card issuing platform supporting both Visa and Mastercard networks. Other traditional financial infrastructure players include Bridge, acquired by Stripe for $1.1 billion in early 2025, and BVNK, whose acquisition by Mastercard for up to $1.8 billion was announced in March 2026.

With competition in the card issuing space intensifying, full-stack issuers, established project service providers, and new fintech companies are all competing on the same stage. Simple card issuing services are no longer a high barrier to entry.

Rain differentiates itself through daily stablecoin settlement. Traditional card settlement cycles can take days. Rain, through Visa, enables T+0 stablecoin settlement, significantly improving capital turnover efficiency for partner platforms like Ether.fi. Recently, the platform launched an AI agent control layer, supporting the automated generation of single-use virtual cards, moving beyond basic card issuing infrastructure.

Card issuers that can break away must offer more than basic payment rails; they need to rapidly implement differentiated value-added functions that traditional infrastructure cannot achieve.

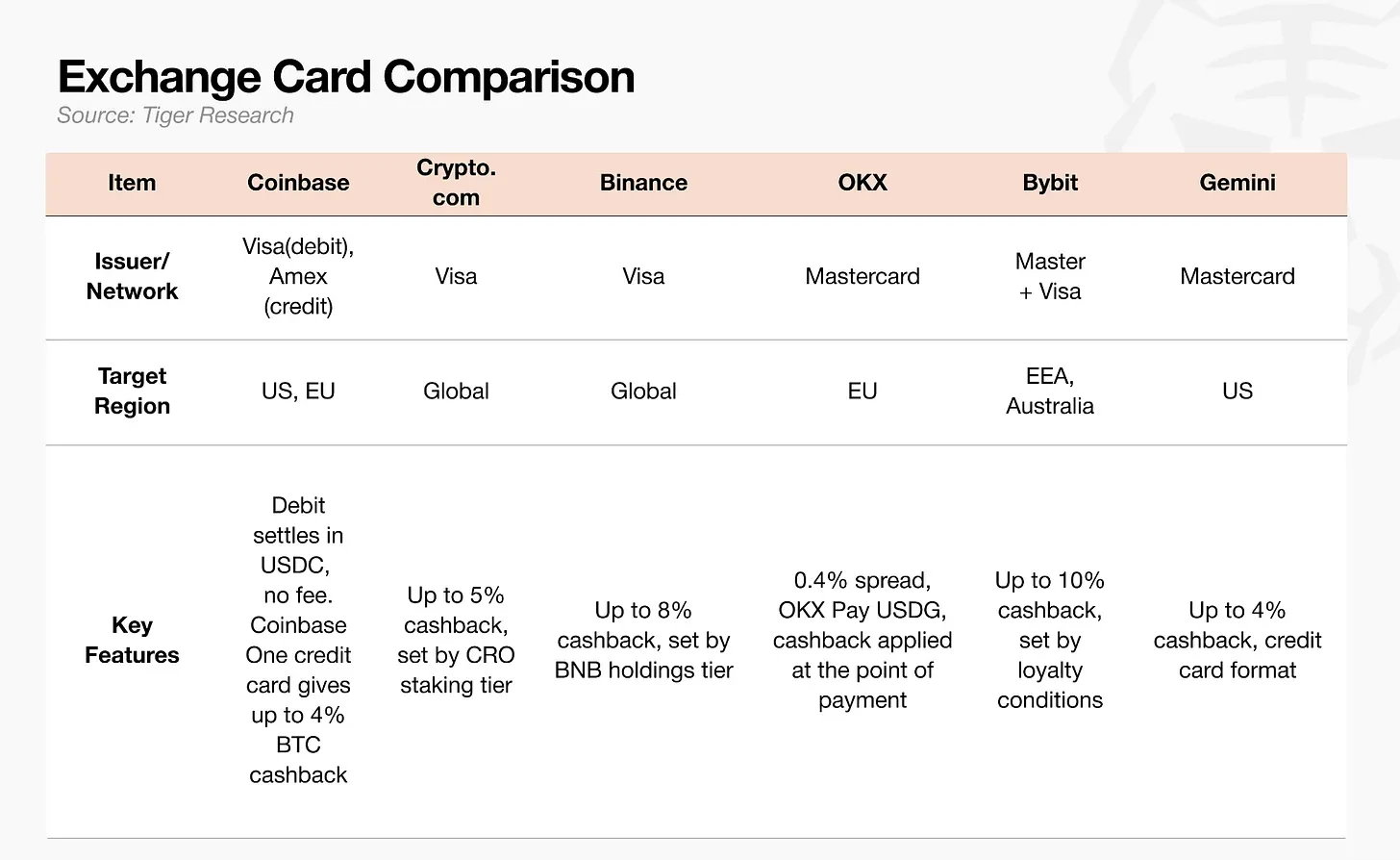

Exchange-Affiliated Payment Cards

For exchanges, payment cards are not a core revenue source; their primary role is to retain existing users. By integrating card functionality with the platform's existing user base, assets, and trading data, exchanges aim to prevent user churn. The platform's real revenue comes from trading fees, lending services, and asset custody, not from card spending itself.

Exchanges view payment cards as a traffic entrance for building a financial super-app. However, the practice of offering cashback in the platform's native token carries risks: token price volatility can lead to unstable effective cashback rates.

Alternative industry proposals include stablecoin cashback or interest-bearing balances, but the US GENIUS Stablecoin Act prohibits interest on stablecoins, posing an obstacle to market expansion.

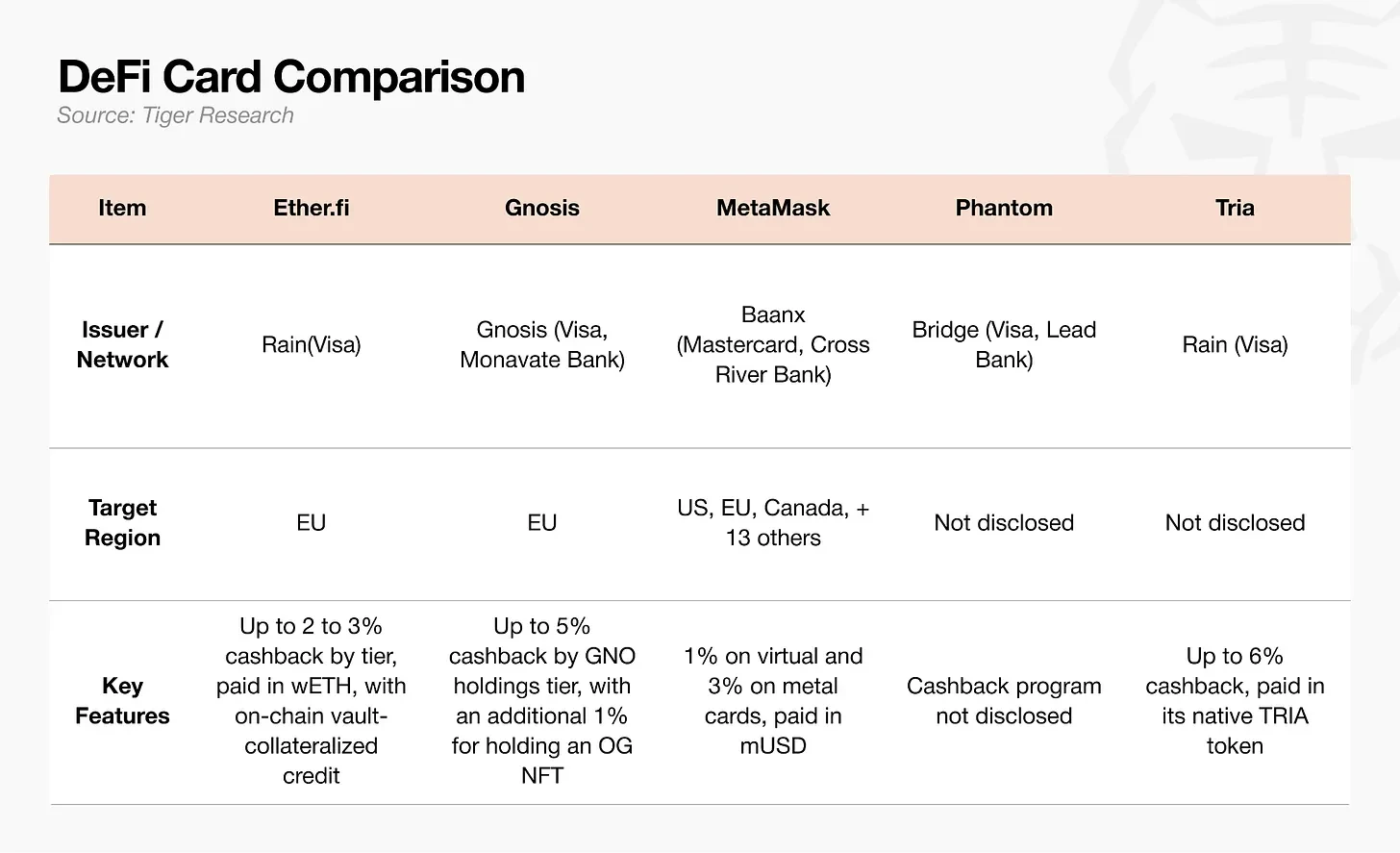

Decentralized Wallets & DeFi

The core logic of this model is that the wallet itself acts as the user's account. Assets are self-custodied on-chain, not held by a centralized exchange, and card spending settles directly from on-chain assets. Additionally, it offers credit lines, where assets can be staked as collateral.

However, users must self-manage vaults, collateral, and monitor liquidation risks, creating a high operational barrier. This results in a limited user base for this model.

During payment, the system converts on-chain assets into fiat in real-time for settlement, incurring on-chain gas fees for each transaction. When public chain throughput is low or the network is congested, gas fees could exceed the transaction amount, leading to frequent transaction authorization delays.

MetaMask Card opted for its self-developed Layer 2 network, Linea, to reduce single transaction gas fees to around $0.01, alleviating pain points related to fees and latency for small payments. Tria employs a gas-free top-up scheme, where the platform covers the gas fee for top-ups, eliminating the user's need to choose a blockchain or calculate fees.

Until the interaction experience balancing asset self-custody with the convenience of card swiping reaches the level of traditional debit cards, this model will remain limited to native crypto users.

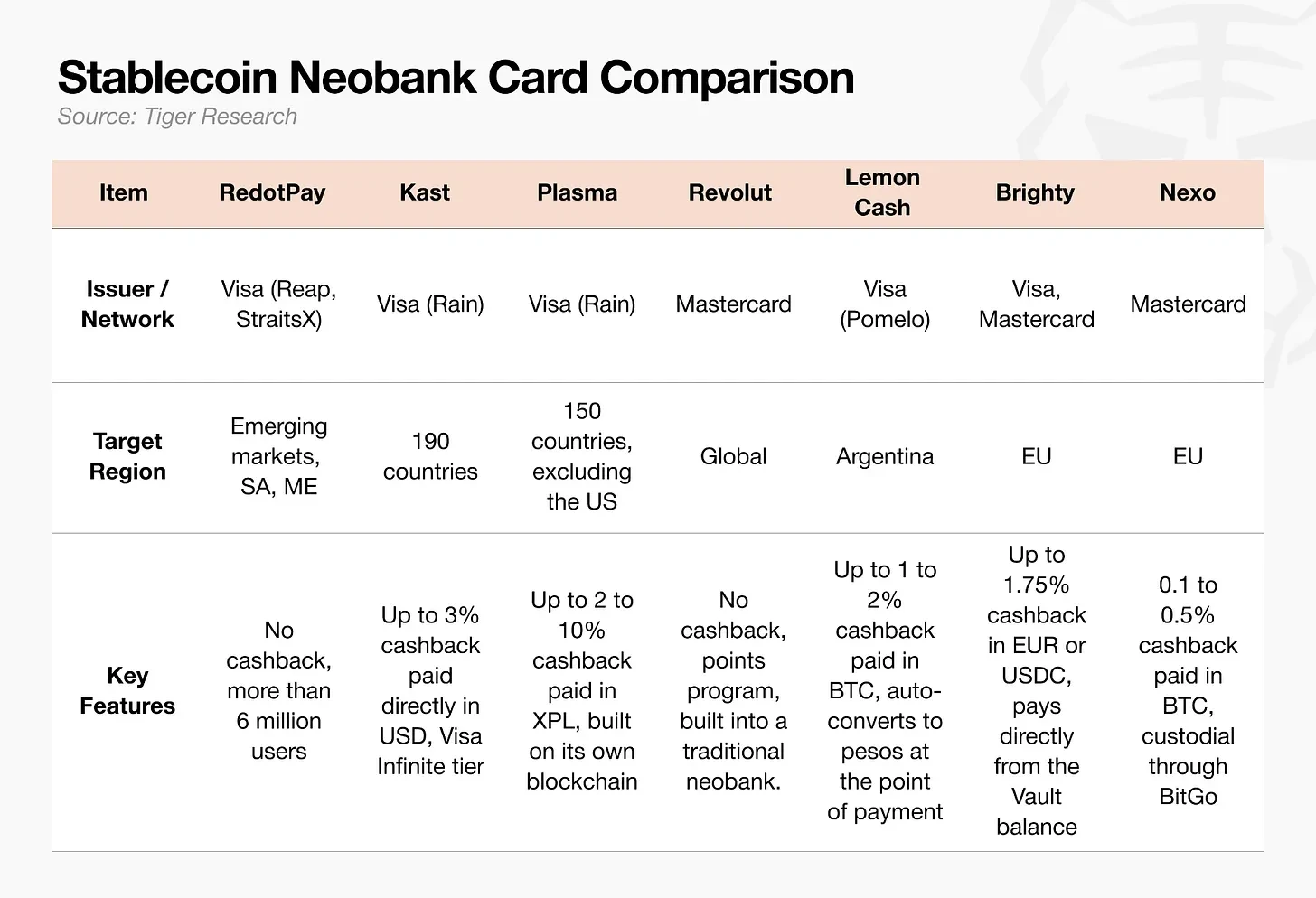

Stablecoin Digital Banks

This track currently accounts for the largest share of market transaction volume. The emphasis is on account functionality rather than the card itself. Stablecoin balances integrate foreign exchange, cross-border remittance, and wealth management features, with the payment card serving merely as the top-tier spending vehicle. This model holds immense competitive strength in emerging markets characterized by volatile local currencies, high cross-border remittance costs, and difficulty accessing US dollars.

For sustainable growth, this track must move beyond the singular "prepaid card" model, where users buy stablecoins and transfer them into their balance.

Cashback strategies vary across platforms based on market positioning. Industry leader RedotPay and traditional fintech veteran Revolut offer no cashback at all, while later entrants like Kast and Plasma One heavily promote cashback in USD or platform tokens to attract users.

However, subsidies and rewards alone cannot drive the deep integration of crypto payment cards into users' daily spending habits.

Single Payment Function Cannot Sustain Long-Term Development

The history of traditional bank cards and digital banks proves that the profit ceiling for pure payment services is extremely low. These enterprises only achieved profitability after incorporating the concept of primary accounts and structural elements like deposit and loan margins into their business models. The crypto payment card industry now stands at a similar development inflection point. However, global regulatory frameworks like the US GENIUS Act and the EU's MiCA impose constraints on developing stablecoin interest-bearing and asset management services, making the path forward challenging.

Under these macro-regulatory constraints, industry players aiming for long-term survival must focus on three core strategies:

- Directly controlling the capital flow chain;

- Securing unique application scenarios in emerging markets;

- Building proprietary user account systems that cannot be easily replaced by underlying infrastructure providers.

Once industry standards solidify, companies failing to achieve these three points will gradually fall behind.

Looking back at the history of debit cards, the ultimate market dominators were not the ones issuing the most cards, but the enterprises that first controlled users' primary bank accounts. The crypto payment card industry faces the exact same challenge today.

Crypto card operators need to directly control capital flow upstream of the Visa payment rails, seize the lead in niche markets, and, akin to the rise of bank accounts in traditional finance, take control of the consumer infrastructure layer. This means establishing a global standard without any precedent to follow.

Crypto payment cards that cannot achieve the above will never become essential tools integrated into daily life. They will remain niche prepaid cards used by specific groups for minimal cashback rewards.