Gate 기관 주간 보고서: WTI 원유 70달러 붕괴, LST 섹터 다시 하락

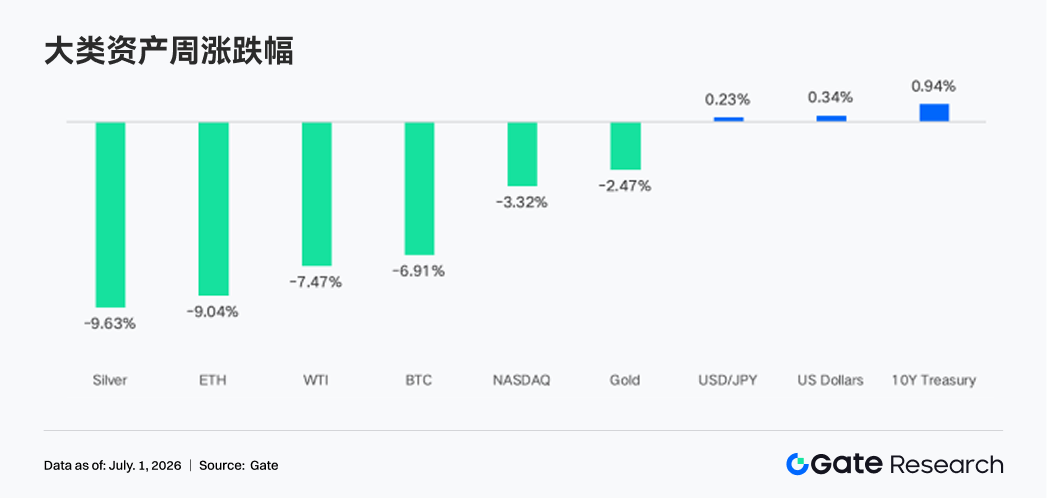

- 핵심 의견: 지난주(2026년 6월 22~28일) 시장 거래 논리가 지정학적 '전쟁 프리미엄'에서 연준의 고금리 장기화로 전환되었고, 인플레이션 경직성이 더해져 미국 증시와 암호화폐 자산이 압박을 받았습니다. BTC는 약 6.9%, ETH는 약 9% 하락했으며, ETF 자금은 대규모 순유출을 기록, 온체인 자금은 방어적 성향과 고회전 시나리오에 치중되었습니다.

- 핵심 요소:

- 거시 배경 전환: 중동 정세 완화로 유가 하락을 주도했지만, 5월 근원 PCE가 3.4%로 목표치를 상회하면서 시장은 '고금리 장기화' 판단을 유지, 나스닥은 3.3% 하락했으며 BTC와 ETH도 약세를跟随했습니다.

- ETF 자금 대규모 유출: BTC 현물 ETF에서 약 17.87억 달러 순유출, ETH 현물 ETF에서 약 2.74억 달러 순유출. BlackRock의 IBIT와 ETHA가 최대 유출원으로, 기관들의 포지션 축소 및 방어적 움직임을 시사합니다.

- 온체인 자금 구조 분화: PumpSwap이 DEX 최대 증가분을 기록, Solana 생태계 자금이 기존 DEX에서 발행 및 고빈도 거래로 전환되고 있음을 반영합니다. 반면 DeFi 유동성(스테이블코인, LST, 대출 시장)은 전반적으로 방어적 포지션을 유지합니다.

- 파생상품 시장 변화: BTC 가격이 6만 달러 근처로 하락했지만, OI는 확장되지 않았고 자금 조달 비율은 여전히 플러스로, 저레버리지 조정에 해당합니다. 옵션 시장의 25D Skew는 약화되고 DVOL은 47~48로 상승, 시장이 하방 위험을 재평가하고 있음을 반영합니다.

- TradFi 비즈니스 지속 성장: Gate 기관 선물 거래량 주간 대비 15% 증가, CrossEx 월간 거래량 전월 대비 10% 증가하며 사상 최고치 경신, AI 고객센터 문제 해결 정확도 85% 초과로 기관 서비스 수요의 안정성을 보여줍니다.

Summary

• The easing of tensions in the Middle East has driven a decline in crude oil prices, shifting the market's trading logic from a 'war premium' to 'the Fed maintaining high interest rates for longer.' The NASDAQ fell approximately 3.3%, while BTC and ETH dropped by about 6.9% and 9%, respectively.

• BTC and ETH spot ETFs experienced significant net outflows, with BlackRock's IBIT and ETHA being the largest sources of outflows. As geopolitical risks cool and AI tech stock volatility intensifies, the proportion of equity trading on TradFi Perp rose to 55%–60%, with capital refocusing on U.S. stock risk trading.

• On-chain capital continues to concentrate in high-turnover trading scenarios. PumpSwap was the biggest gainer this week, reflecting a migration of Solana ecosystem funds from traditional DEXs to issuance and high-frequency trading environments.

• DeFi liquidity maintains a defensive posture, with stablecoins, LSTs, and lending markets generally cautious. Aave's lending scale contracted slightly, interest rates remained low, capital continued to concentrate on the Ethereum main market, and overall risk appetite has not yet shown clear signs of recovery.

• BTC's price fell back to around $60,000, but this was not accompanied by a significant expansion in OI. The funding rate continued to hold positive, indicating that this adjustment was driven more by spot and position adjustments rather than new short positions, and overall BTC derivatives maintain a low-leverage environment.

• Monthly option trading volume surged significantly before expiration, the 25D Skew continued to weaken, and DVOL rose to approximately 47–48, reflecting a market repricing of downside risk.

• Gate Institutional's contract trading volume increased 15% week-over-week. CrossEx's weekly trading volume grew 6% week-over-week, and its monthly trading volume in June increased 10% month-over-month, continuing to hit new all-time highs. The AI customer service bot was continuously upgraded, achieving an accuracy rate of over 85% for basic issues.

1. Market Focus

Last week (June 22-28, 2026), the global macro landscape was dominated by three themes: cooling geopolitical risks in the Middle East, sticky U.S. inflation, and a hawkish Federal Reserve policy outlook. Firstly, as tensions between the U.S. and Iran eased temporarily, the market quickly reduced its concerns about supply disruptions in the Strait of Hormuz, leading to a substantial unwinding of the war premium in oil prices. Brent crude briefly fell to around $73.83 per barrel, and WTI dipped below $70 per barrel. The decline in oil prices reduced the risk of another surge in energy inflation and improved short-term consumer sentiment. The University of Michigan Consumer Sentiment Index for June rebounded nearly 5 points from its previous reading. Consequently, the market shifted its focus from trading on 'geopolitical shocks/oil price surges/re-accelerating inflation' to assessing whether inflation will continue to cool down following the moderation in energy prices.

However, U.S. inflation data does not support a swift pivot by the Fed to an accommodative stance. The May PCE rose 4.1% year-over-year, and the core PCE stood at 3.4% year-over-year, both still significantly above the Fed's 2% target. On the positive side, the month-over-month PCE was 0.4%, which was lower than the market expectation of 0.5%, preventing a further sell-off in the bond market. This combination implies persistent inflationary pressure, particularly the stickiness of core services and wage-related prices, but without a more severe upside surge in the short term. The market therefore maintained its 'higher-for-longer' interest rate view while reducing fears of more aggressive rate hikes. U.S. Treasury yields retreated over the week, with the 10-year yield falling to around 4.37% and the 2-year yield to about 4.09%, reflecting lower oil prices dampening inflation expectations, although the policy rate path remains constrained by inflation.

From a macro transmission perspective, the easing of geopolitical tensions is positive for risk appetite and bonds, but sticky inflation limits the room for asset valuation recovery. The U.S. dollar and real interest rates continue to exert downward pressure on gold, tech stocks, and crypto assets. The NASDAQ fell about 3.3%, while BTC and ETH dropped approximately 6.9% and 9%, respectively. The decline in oil prices, however, alleviated corporate cost pressures and consumer inflation expectations. Overall, last week wasn't simply a risk-off move, but a repricing process where the market moved from a 'war premium' to evaluating whether the Fed can maintain its tightening stance amidst high inflation.

2. Liquidity Analysis

2.1 ETF Institutional Risk Appetite Cools Down in Tandem, IBIT Sees $1.304 Billion Outflow

Both BTC and ETH ETFs experienced significant fund outflows last week, indicating a synchronized cooling of institutional risk appetite. BTC spot ETFs saw a total net outflow of approximately $1.787 billion, worsening from the previous week's net outflow of about $228 million. ETH spot ETFs recorded a net outflow of around $274 million during the same period, a significant expansion from the prior week's net outflow of about $10 million. At the product level, the BTC ETF with the highest inflow was the Grayscale Bitcoin Mini Trust BTC, with about $71.7 million; the one with the highest outflow was BlackRock IBIT, with approximately $1.304 billion. For ETH ETFs, the one with the highest inflow was Bitwise ETHW, but only about $0.6 million; the one with the highest outflow was BlackRock ETHA, with approximately $236 million.

AUM is likely to have declined directionally month-over-month. BTC's price fell approximately 6.91% last week, and combined with the significant net redemptions from ETFs, the asset size was negatively impacted by both price pullback and share contraction. ETH's price dropped about 9.04% last week, and its ETF side attracted even weaker fund flows, making the AUM pressure more pronounced. Overall, institutional sentiment shifted from allocation or waiting to defense and deleveraging. Notably, BlackRock's products, previously the strongest at attracting capital, became the primary source of outflows, indicating that core institutional funds are also reducing their beta exposure to crypto assets. Compared to BTC, the buying pressure for ETH ETFs was weaker, suggesting a more significant contraction in institutional risk appetite for higher beta assets.

2.2 TradFi Liquidity

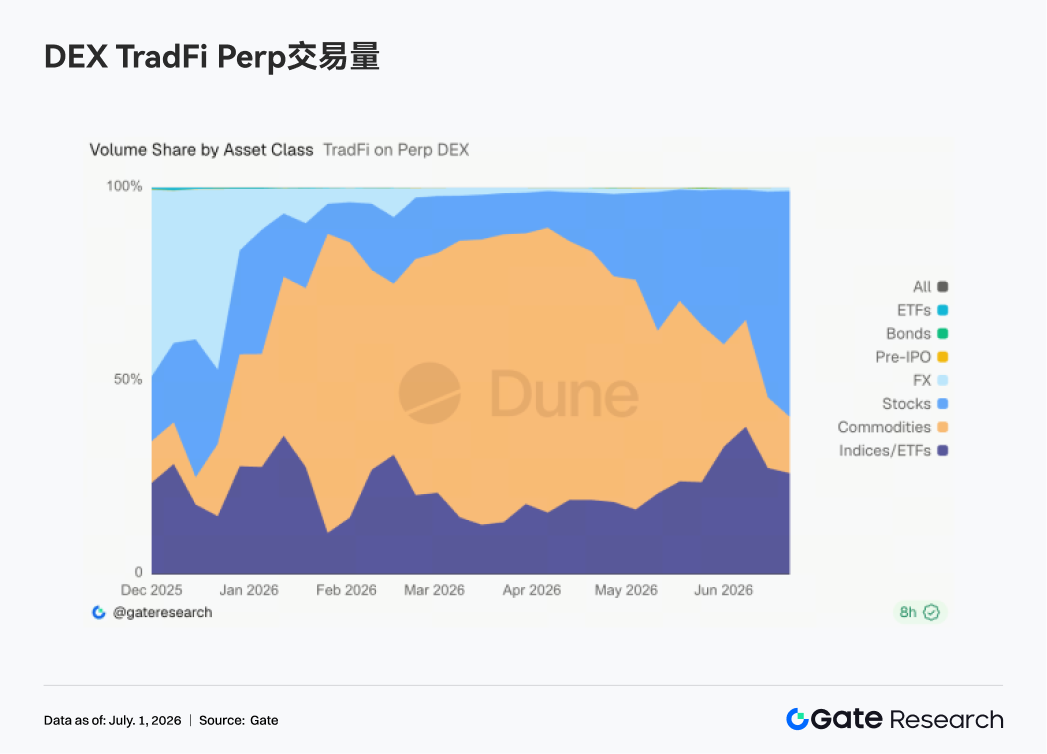

• TradFi Perp DEX: Over the past week, the trading volume structure on TradFi Perp DEXs saw a clear shift, with equity assets regaining market dominance while the trading heat for commodity assets continued to cool. Since late June, the share of equity trading volumes quickly rose to around 55%–60%, making it the largest trading category. Concurrently, the share of commodities dropped rapidly from approximately 40%–50% to below 20%, indicating a significant decline in trading activity for safe-haven assets like gold and crude oil. Meanwhile, the share of index/ETF trading remained stable at around 25%–35%, a significant allocation direction, reflecting that users continue to gain exposure to U.S. stock market volatility through index products. This shift is closely linked to the recent macro environment, where significant volatility in the U.S. AI sector, adjustments in tech stocks, and market repricing of the rate cut path have increased the trading activity of equity and index perpetual swaps. Furthermore, Pre-IPO assets like SpaceX continue to attract attention, further driving capital concentration towards the equity ecosystem. Overall, the focus of capital on TradFi Perp DEXs is shifting back from commodities to equities and index assets. The market logic has transitioned from geopolitically driven risk-off trades to risk trades centered around U.S. stock volatility, the tech sector, and macro events. Equity class assets are expected to remain the main growth driver for the TradFi Perp market.

• Gate TradFi Perp Trading Volume: Despite the cautious macro environment, user demand for trading TradFi perpetual products remains robust. Over the past week, Gate's TradFi Perp trading volume saw a notable increase week-over-week, with daily turnover mainly in the $4 million to $6 million range. While overall volatility narrowed compared to previous weeks, trading activity did not show a significant decline. By asset class, metals remain the absolute core source of trading volume, with perpetual contracts for precious metals like gold contributing the majority of the turnover. This reflects that amidst the Fed's hawkish stance, recurring geopolitical risks, and high gold prices fluctuating, safe-haven assets remain a key focus for market funds. Meanwhile, the share of index trading has increased significantly compared to before, with a notable surge in volume at the start of the week. This suggests that user participation in U.S. stock-related perpetual contracts continues to rise, driven by adjustments in the AI sector, increased volatility in the U.S. stock market, and stronger individual stock event-driven activity.

• Gate TradFi U.S. Stock Asset Count: Gate officially launched its U.S. stock trading service on June 2nd. Leveraging advantages such as support from real underlying assets, direct trading with USDT, no overnight holding fees, and high liquidity, the service has continuously garnered market attention since its launch, with trading volume growing steadily. Currently, Gate supports 7 major asset classes: ADRs, stocks, ETFs, ETNs, ETSs, ETVs, and PFDs, and is continually expanding its product coverage. In terms of asset count, the total number of tradable instruments has doubled since the launch. Stocks have seen the most significant growth, with their proportion of all assets increasing from about 70% at launch to 85%, further enriching users' investment choices. Going forward, Gate will continue to advance market access, global liquidity integration, and cross-market trading capabilities, constantly expanding its diversified asset coverage and further strengthening its strategic positioning as a global asset trading and market access platform.

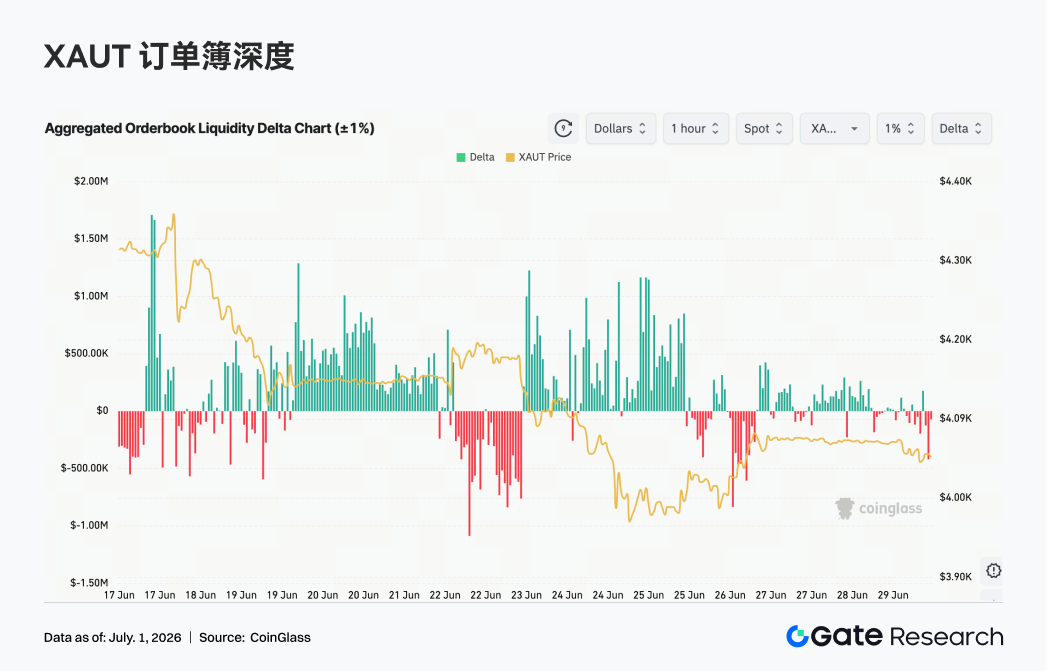

• TradFi Order Book Depth: We selected XAUT, the highest-volume TradFi asset, for an analysis of its order book depth (Delta). Over the past week, XAUT's order book liquidity shifted from being dominated by buyers to being dominated by sellers, with the price trending downwards in a volatile manner. At the start of the week, Delta remained positive multiple times, and buy-side liquidity continued to flow in, supporting the XAUT price in the $4,180–$4,330 range, indicating relatively strong market absorption capacity. Entering June 22nd, as macro risk sentiment changed and gold prices fell, the order book Delta quickly turned negative, with consecutive negative values of $500,000 to $1 million. This indicated a significant increase in active selling pressure, and the XAUT price simultaneously broke below $4,100, briefly approaching the $4,000 level, reflecting a concentrated release of short-term selling pressure. Over the weekend, although there were periodic buy-side orders in the order book, the persistence of positive Delta weakened significantly, lacking sustained upward capital momentum. If the U.S. dollar and Treasury yields remain elevated, gold tokens may continue to face pressure in the short term. If expectations for rate cuts revive or geopolitical risks escalate again, order book buy-side flows could strengthen, driving a price recovery.

3. On-Chain Data Insights

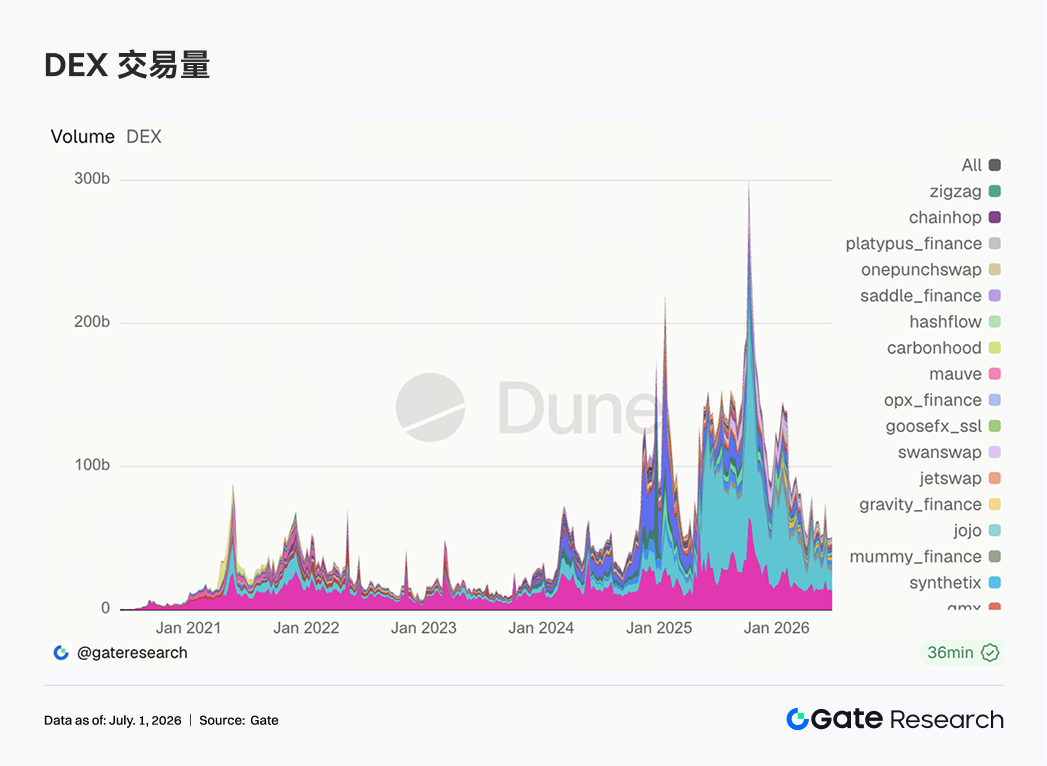

3.1 DEX Volumes Haven't Broadly Expanded, PumpSwap Emerges as the Week's Most Prominent Structural Change

DEX volumes overall did not continue the previous strong uptrend. Uniswap and PancakeSwap remain firmly in the top two spots, but their volumes decreased slightly compared to the previous week, with top-tier spot pools entering a phase of consolidation at high levels. The change comes from PumpSwap, which saw its volume and number of traders jump significantly, breaking directly into the top three. Speculative flow on the Solana side hasn't disappeared; it has shifted from traditional entry points like Raydium and Meteora towards scenarios more focused on issuance and high-frequency trading. Protocols like Aerodrome, Bisonfi, and Tessera also saw some recovery, with Base and emerging matching environments continuing to absorb active capital.

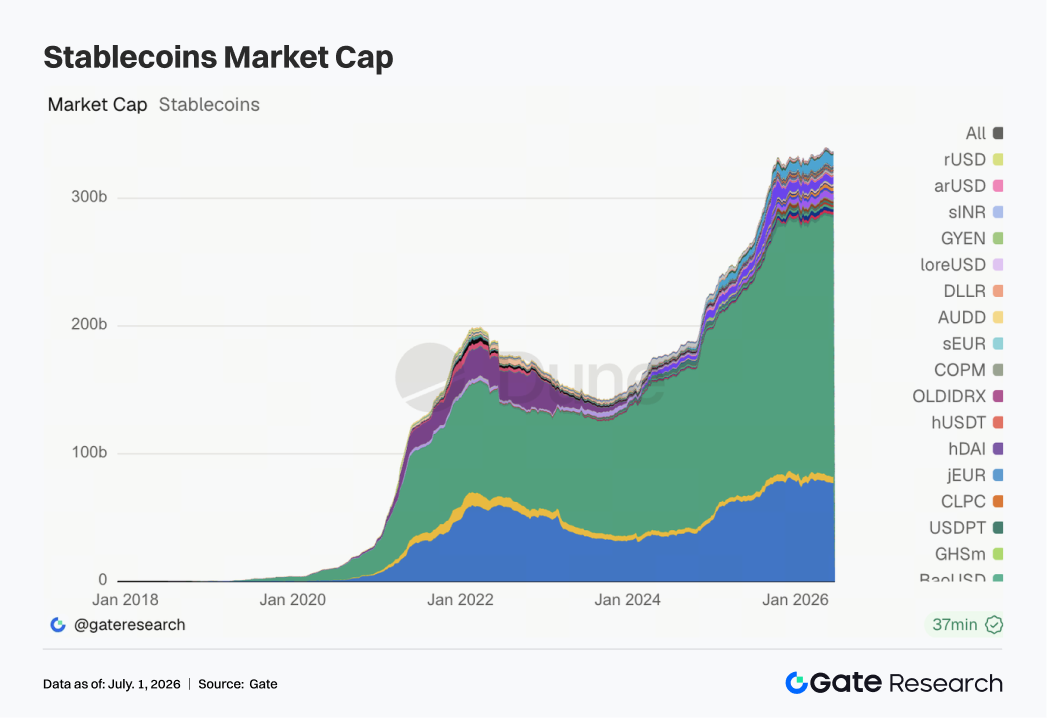

3.2 Stablecoin Supply is Defensive; Regulatory Debate Impacts Market Pricing More Than Short-Term Issuance

The stablecoin sector remained somewhat contracted overall this week. USDT and USDC both saw slight declines, while USDS, USDe, USD1, and PYUSD did not show significant expansion. DAI performed relatively stronger. There was no large-scale net inflow of new dollars on-chain; more activity involved the migration of existing capital between different stablecoins. On the news front, an organization representing U.S. community banks publicly opposed stablecoin-related legislation on June 28th. The core concern was that reward-bearing stablecoins could drain deposits from the local banking system, elevating the stablecoin regulatory debate from a crypto industry issue to a matter of redistributing interests within traditional finance. The Bank of England also adjusted its stablecoin regulatory framework in the same week, shifting from holder position limits to issuance size caps, indicating that major jurisdictions are trying to balance innovation, payment efficiency, and banking system stability.

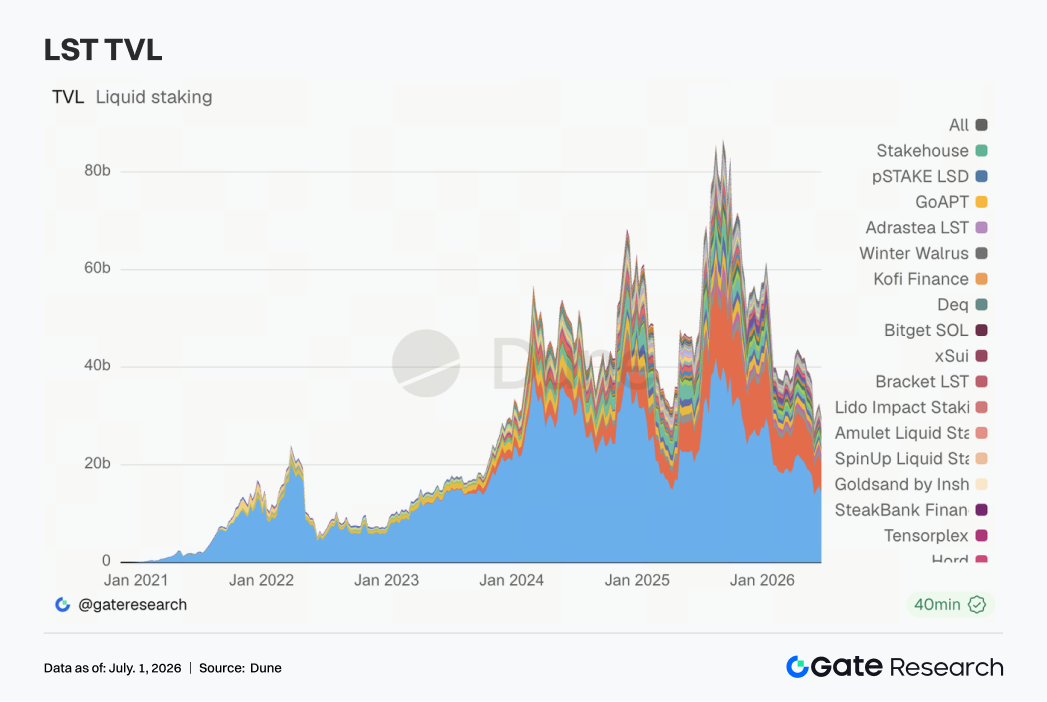

3.3 LST Sector Retreats Again, Market's Risk Discount on Staked Assets Widens Anew

The LST sector reversed its recovery from the previous week and saw a broad decline. Lido, Rocket Pool, and StakeWise on the Ethereum side faced pressure, and Jito and Sanctum on the Solana side also weakened simultaneously. Since TVL is denominated in USD, the pullback was largely influenced by price fluctuations in ETH and SOL, but capital preferences were indeed more cautious. Following the KelpDAO/rsETH incident, institutional risk assessment of staked assets has already stratified. Standard LSTs, restaking assets, and cross-chain wrapped assets are no longer viewed within the same risk basket. Recent discussions surrounding wstETH cross-chain security and Chainlink CCIP at Lido have reinforced the importance of bridge security and issuance control in LST pricing.

3.4 Aave Lending Contracts Slightly, Capital Still Favors the Deepest Ethereum Main Market

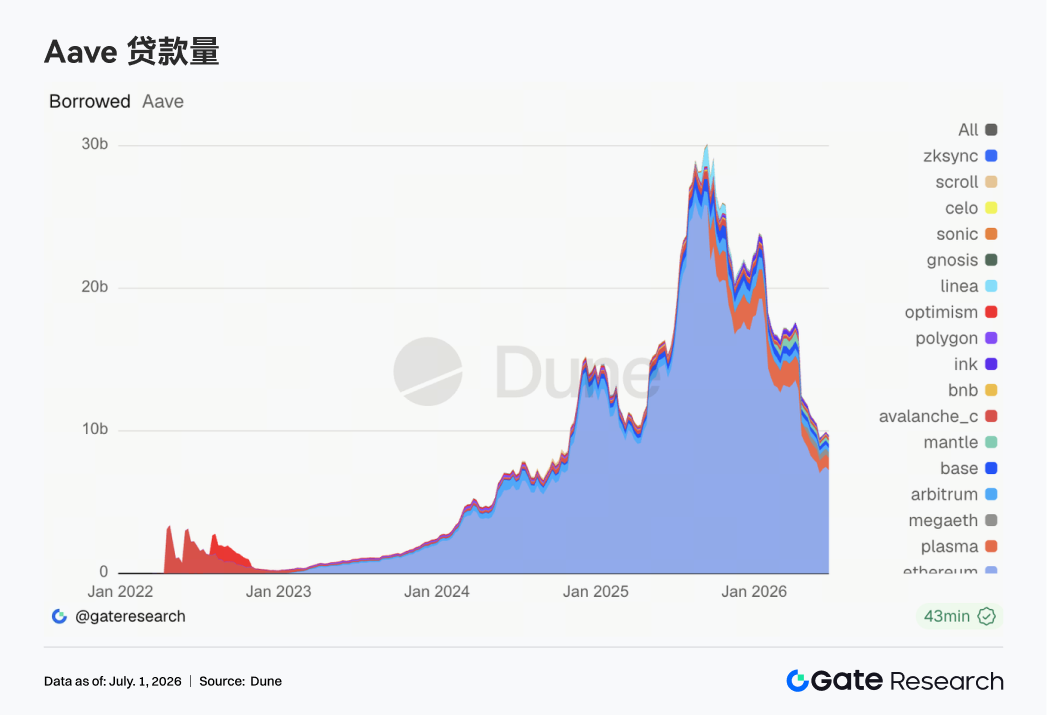

Aave's lending balance this week saw a slight decline compared to the previous week. The Ethereum main market remains the absolute core but also bore the brunt of the contraction pressure. Plasma was largely stable, Mantle saw some recovery, while MegaETH, Arbitrum, and Base were weaker. This suggests that capital hasn't left Aave, but the pace of multi-chain expansion has clearly slowed. The aftereffects of the rsETH/KelpDAO incident persist, making borrowers more sensitive to collateral safety, liquidation depth, and risk parameters. Recent governance discussions at Aave, centered around unfreezing WETH, USDC liquidity buffers, and the V4 Hub-and-Spoke architecture, are transforming this risk event into institutional-level remediation. For institutions, Aave remains the core infrastructure for DeFi lending, but the short-term growth logic has shifted towards stabilizing leverage in the main market and repricing risk frameworks.

3.5 Aave Core Asset Rates Remain at Low Levels with Divergence; USDC Remains the Most Sensitive Pool

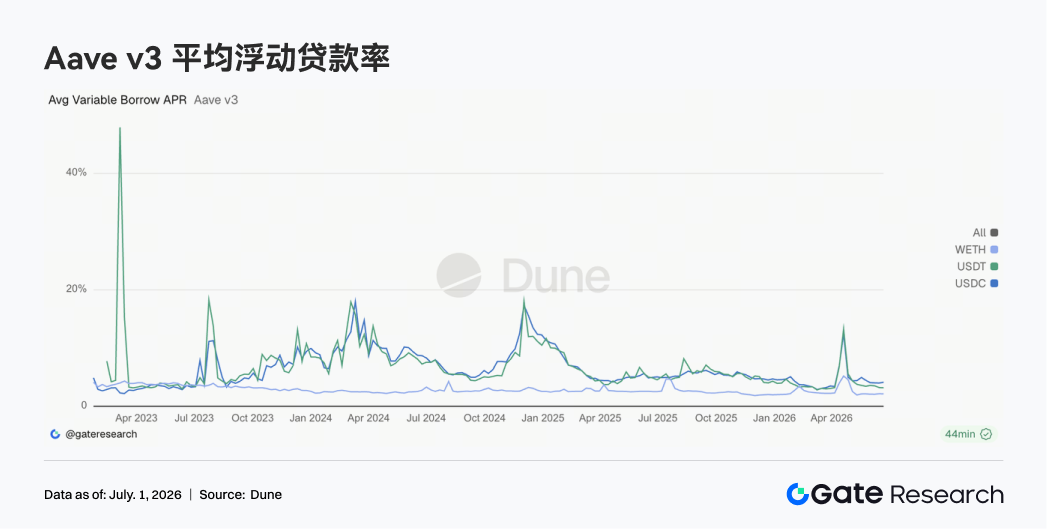

This week, the loan rates for Aave's three core assets showed little overall change. The average borrowing cost for USDC rose slightly, USDT fell, and WETH remained low. USDC's highest intraday rate still saw brief upward spikes, indicating that the core USD pool remains sensitive to changes in utilization. USDT rates were more stable. WETH borrowing did not see a significant surge, implying that directional ETH leverage has not returned on a large scale. This combination points to a cautious capital environment. Stablecoin financing is still used for working capital, arbitrage, and liquidity management, but the market is not rebuilding aggressive one-sided risk exposure. Considering the Aave community's discussions on USDC liquidity buffers, the protocol is actively working to reduce the risk of interest rate jumps during extreme utilization scenarios. The signals from interest rates are more tempered than the lending balance figures. The panic is over, but the memory of the risk hasn't faded.

3.6 Protocol Revenue Structure Improves; Stablecoins Provide a Base, Trading & Infrastructure Regain Elasticity

Protocol revenue showed more depth this week compared to last. Tether and Circle remain the most stable sources of cash flow, with little overall change. Hyperliquid Perps' revenue grew again, demonstrating that despite weakness in the spot market, demand for on-chain perpetual contracts and high-frequency matching remains resilient. Solana traffic funnels like Pump.fun, Pump