摩根士坦利 분석: SIMO 목표 주가 400달러로 상향 조정, AI 서버가 NAND 사이클을 재편하다

- 핵심 의견: 모건스탠리는 AI 서버 수요가 NAND 시장을 소비자 가전 사이클에서 엔터프라이즈 신규 사이클로 전환시키고 있다고 판단하며, 2026/2027년 글로벌 공급 부족이 각각 15%/9%에 달할 것으로 예상하고, 이에 따라 Silicon Motion(SIMO)의 목표 주가를 400달러로 대폭 상향 조정했습니다.

- 핵심 요소:

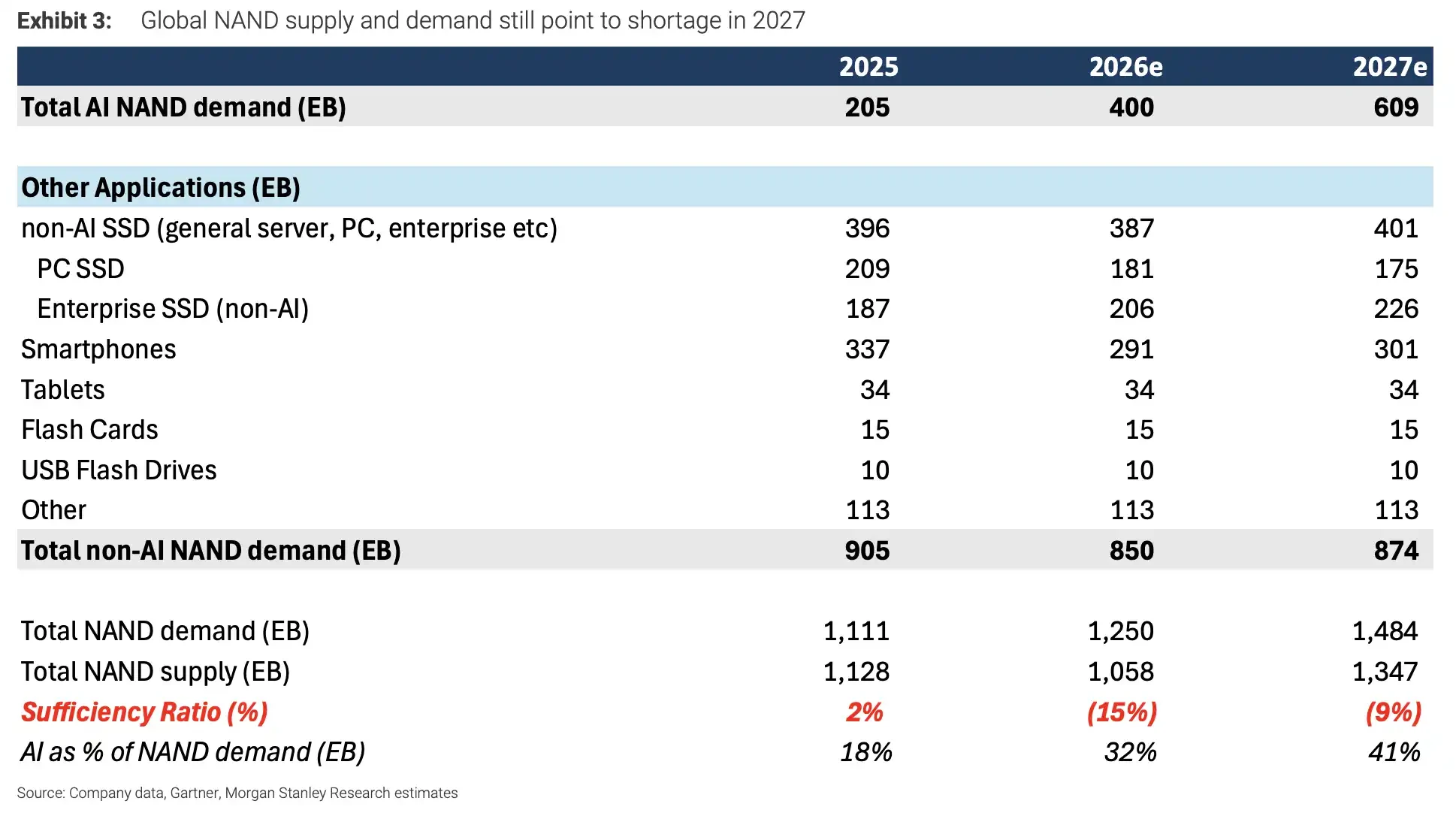

- 수급 격차 전망: 2025-2027년 글로벌 NAND 수급 비율은 각각 2%(잉여), -15%(부족), -9%(부족)로 예상되며, AI 수요가 핵심 동력입니다.

- AI 수요 비중: 2027년 AI 관련 NAND 수요는 609EB에 달해 전체 수요의 41%를 차지할 것으로 예상되며, 데이터센터 및 클라우드 업체의 구매가 핵심 변수가 될 전망입니다.

- 가격 차별화 뚜렷: 2026년 3분기 엔터프라이즈 SSD 가격은 전분기 대비 약 30% 상승하지만, 소비자용 NAND의 상승 폭은 제한적입니다. 이는 모바일/PC 고객의 수익성 압박 때문입니다.

- SIMO 상향 조정 논리: 엔터프라이즈 SSD 컨트롤러(MonTitan) 및 AI 부트 드라이브 사업이 2026년 매출의 20% 이상을 기여할 것으로 예상되며, 이는 밸류에이션 상향 조정의 핵심 요인입니다.

- 2028년 리스크: YMTC가 생산 능력을 470kwpm으로 확장하거나 AI 자본 지출이 둔화될 경우, 시장은 공급 부족에서 잉여로 전환되어 낙관적 전망이 깨질 수 있습니다.

TL;DR

- Morgan Stanley raised SIMO's target price from $155 to $400, citing AI-driven acceleration in demand for enterprise SSDs and boot drives.

- They predict a 15% global NAND shortage in 2026 and a continued 9% shortage in 2027, with AI-related demand reaching 609EB by 2027.

- Suppliers and controller manufacturers benefit more directly, but price increases for consumer products are limited. YMTC's capacity expansion and a slowdown in AI capital expenditure could change the supply-demand dynamics in 2028.

In its latest report, Morgan Stanley significantly raised its target prices for Silicon Motion (SIMO.O) and Longsys, pointing to the NAND demand gap driven by AI servers. For investors, this is not just a typical expectation of higher SSD prices; it signals that AI data centers are shifting NAND demand away from the consumer electronics cycle of phones and PCs towards a new cycle driven by enterprise SSDs, AI boot drives, and long-term procurement by cloud providers.

The most aggressive adjustment was for SIMO. Morgan Stanley raised its target price from $155 to $400, based on 23 times the expected 2027 EPS, and projects the company's 2026 revenue will hit a record high. Longsys's target price was also raised from 300 yuan to 673 yuan, and Phison's from NT$2,248 to NT$2,588. However, Morgan Stanley maintained an Equal Weight rating for both Longsys and Phison, suggesting that not all module manufacturers will benefit equally from this trend.

The core judgment of this report is that AI's pull on NAND demand will persist until 2027. In 2025, lingering inventory surplus is still expected to create a roughly 2% excess in global NAND supply-demand balance. By 2026, the market is expected to shift to a 15% shortage. Even as supply increases in 2027, a 9% gap is still anticipated. The key drivers behind this are not phones and PCs, but AI servers, cloud provider SSDs, enterprise storage, and boot drive demand.

Global NAND supply-demand still points to a shortage in 2027. 2025-2027e total demand: 1111/1250/1484 EB; supply: 1128/1058/1347 EB. The supply-demand balance shifts from +2% to -15% and -9%.

AI Shifts NAND Demand Focus from Consumer Electronics to Data Centers

Historically, NAND demand has been more easily influenced by inventory cycles in phones, PCs, and consumer-grade SSDs. The change now is that AI servers require not only GPUs and HBM but also substantial local storage, enterprise SSDs, and boot drives. Once cloud providers adopt long-term procurement agreements, the way NAND prices and supply-demand fluctuations behave will also change.

Morgan Stanley forecasts that AI-related NAND demand will grow 60% year-over-year in 2027, reaching 609EB and accounting for 41% of total NAND demand. That same year, global total NAND demand is projected at 1484EB, while supply is expected to be 1347EB, resulting in an approximately 9% shortage. In contrast, assumptions for smartphones and PCs are not aggressive: NAND content per device is broadly flat, and terminal shipments are assumed to decline according to hardware team models.

This means the report's shortage thesis is not built on a broad consumer electronics recovery, but on the continued expansion of AI server and cloud capital expenditure. The greater the contribution from AI demand, the higher the sensitivity of the NAND cycle to CSP procurement, server configurations, and enterprise SSD supply.

Channel prices are already starting to diverge. 3Q26 channel checks show that pricing for TLC enterprise SSDs rose approximately 30% quarter-over-quarter, server-grade DRAM rose 20%, and legacy DRAM like DDR3/DDR4 rose 30%-40%. However, consumer-grade NAND price increases were significantly smaller, as phone and PC customers face greater profit pressure and cannot absorb similar price hikes.

In other words, price increases are indeed happening, but the strongest rises are for data center-related products, not all NAND categories.

Why Was SIMO Upgraded the Most?

The reason for the significant target price increase for SIMO lies in its business perfectly aligning with two segments of AI storage growth: enterprise SSD controllers and AI boot drive modules.

The MonTitan enterprise SSD business is considered the company's most important new growth driver in the coming years. Morgan Stanley expects this business to contribute 5%, 13%, and 19% of SIMO's revenue in 2026, 2027, and 2028, respectively. Simultaneously, boot drive modules are expected to start ramping up, contributing a combined ~15% and ~21% of company revenue in 2026 and 2027.

For AI servers, the boot drive is not the most prominent component, but it is an indispensable storage configuration for system startup, management, and operation. As the shipment of AI servers increases, demand for related controllers and modules will also rise. SIMO was previously more easily viewed by the market as a consumer-grade controller company. The key driver for the upward valuation revision is the potential for a rapid increase in the revenue share from enterprise and AI-related products.

However, this remains a forecast, not realized profit. Morgan Stanley's $400 target price corresponds to 23 times the expected 2027 EPS, implicitly assuming that enterprise SSD and boot drive volumes ramp up smoothly, customer adoption progresses, and AI server demand does not decelerate significantly. Any shortfall in these areas could impact whether the valuation holds up.

Module Maker Target Prices Raised, But May Not Capture the Biggest Share

Longsys and Phison also benefit from storage price increases and AI server demand, but the report did not upgrade their ratings to a more positive level. The reason is that module makers face a practical constraint in this cycle: when NAND supply is tight, manufacturers are more likely to prioritize capacity allocation for large cloud providers and core CSP customers, meaning the incremental supply available to module makers may not be substantial enough.

This is why target prices can be raised, but the ratings remain at Equal Weight. Price increases benefit inventory and ASP improvements, and a better enterprise product mix can support profit margins. However, if volumes are constrained by upstream suppliers and key customers, the revenue elasticity for module makers will be limited.

Long-Term Agreements (LTAs) are another important clue. Suppliers can secure some downside price protection through LTAs, with Kioxia's LTA coverage expected to exceed 50% in 2027. However, these agreements are not a one-way benefit. Micron has also indicated that LTAs often include both price ceilings and floors. They can mitigate the risk of price plunges but may also limit suppliers' ability to raise prices during extreme shortages.

Module makers hope to transfer more inventory pressure to customers through models like TCM, aiming for stable long-term gross margins in the 25%-35% range. However, this also depends on customer acceptance, the severity of supply tightness, and whether the products are sufficiently high-end.

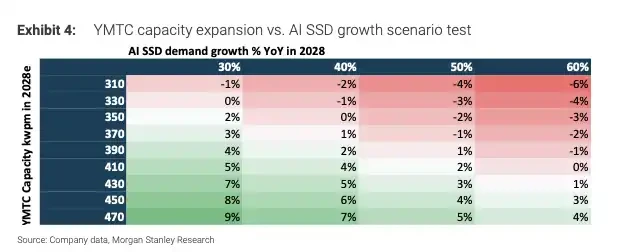

2028 Risks Lie in Supply and AI Spending

The biggest boundary for this optimistic forecast is 2028.

Under Morgan Stanley's baseline scenario, even by 2028, if AI NAND demand continues to grow 60% year-over-year and YMTC's capacity remains around 310kwpm, the market could still face approximately a 5% shortage. However, if YMTC's capacity increases to 470kwpm while AI growth slows down, the NAND market could shift from shortage to surplus.

Scenario test: YMTC 2028 capacity expansion vs AI SSD growth. The matrix shows that under combinations of YMTC capacity (310-470kwpm) and AI growth (30%-60%), supply-demand can shift from shortage towards balance or even surplus.

This is also the most challenging aspect of the memory cycle: short-term price increases and low inventory levels easily reinforce optimistic expectations. However, once semiconductor storage supply discipline loosens, surplus can return quickly. Some order cuts are already appearing on the consumer side; phone and PC customers have limited ability to absorb price hikes. The price ceiling for consumer-grade NAND may appear sooner than for enterprise products.

Therefore, the real question this report poses to the market is not "Will SSD prices rise?" but "Is AI demand strong enough to absorb the new supply coming online over the next two years?" For companies like SIMO in the controller and AI storage chain, 2026 could be the starting point for ramping up enterprise and AI business. For the entire NAND cycle, the pace of capacity expansion by YMTC and other manufacturers, the intensity of CSP capital expenditure, and supplier discipline in 2028 will be the key factors determining whether the shortage can persist.