Monera Digital 六月加密月報:當最大邊際買家轉身離場

- 核心觀點:2025 年 6 月,加密市場完成了從投降式下跌到長期持有者靜默吸籌的底部構築預演。價格腰斬、ETF 創紀錄失血與 MSTR 信仰破裂標誌著內部出清進入深水區,但賣方枯竭初步確認,籌碼正從弱手向強手遷移。

- 關鍵要素:

- 價格與槓桿出清:BTC 月跌 19.2%至 59,624 美元,月內最低 58,201 美元,較週期高點回撤達-54%,正式「腰斬」;全月衍生品 OI 累計壓縮逾 23 億美元,市場去槓桿顯著。

- 機構買盤範式破裂:Strategy 打破「永不賣出」承諾首次減持 BTC,並授權最高 12.5 億美元的 BTC 貨幣化,過去最大的價格不敏感買家可能成為結構性賣方。

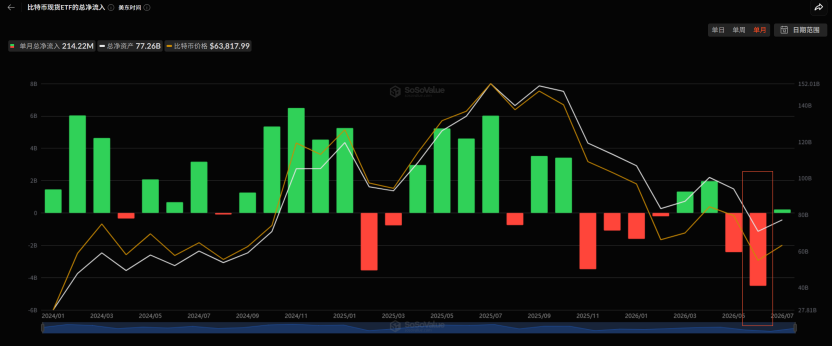

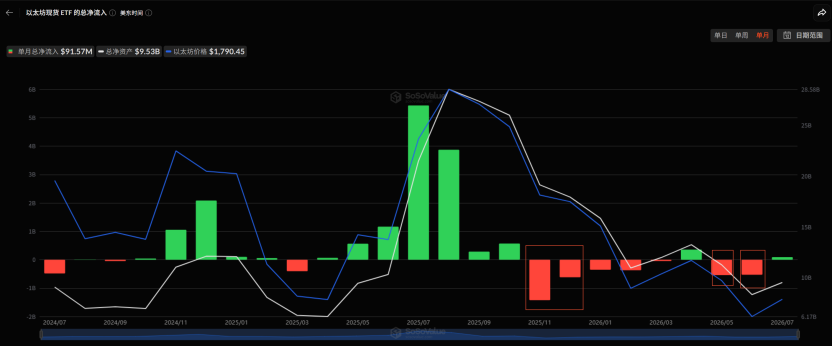

- ETF 史上最慘烈失血:BTC 現貨 ETF 全月淨流出約 45.1 億美元,創產品誕生以來最大單月流出,ETH 現貨 ETF 同步流出約 5.29 億美元,美國渠道拋壓主導。

- 宏觀利空三連擊:美國數據全面證偽降息(5 月非農火爆、CPI 及 PCE 超預期),FOMC 鷹派點陣圖確認停滯性通膨方向,DXY 重奪主導並壓制 BTC。

- 鏈上吸籌浮現與估值極值:長期持有者時隔數月重返淨買入,LTH 供應佔比升至 88.1%多年新高;Ahr999 跌至 0.283 的「鬼區」,全網虧損籌碼首次多於盈利籌碼,籌碼正大規模遷移。

- 月末結構質變:空頭陷阱驅動的新低(57.8K)與現貨賣壓枯竭形成區分,選擇權市場 Gamma 結構轉為抑制波動,做市商為 60-64K 區間定價,但反轉三軸(ETF、美元、價格)均未成立。

Core Conclusions

June was a public dismantling of faith-based narratives and a textbook rehearsal for a bottoming process. Last month we recorded a "failure of liquidity transmission"; in June, the market answered the next question: What follows failed transmission? The answer is internal liquidation descending from "distribution" into "capitulation," the cycle's most enduring narrative ("never-sell corporate treasury") completing its self-negation, and the macro environment deteriorating from "good news fails to rally" to "substantive tightening arrives." Simultaneously, however, it was a month where long-term holders returned to net accumulation after months, and strong hands quietly accumulated amidst deep fear.

On the price front, BTC started the month at $73,764 and closed around $59,624, a monthly decline of approximately 19.2%. The two key lows during the month – $59,130 on June 5th and $58,201 at the end of the month – represented a drawdown expansion to -54% from the cycle high of $126,000 in October 2025, officially a "crypto winter" territory. ETH fell from $2,007 to $1,572, a monthly decline of about 22%, with a low of $1,505.

Three main themes defined June:

First, the public breakdown of the institutional buying paradigm. Strategy broke its "never sell" promise early in the month, selling 32 BTC for the first time. Mid-month, its mNAV fell to 1.02, halting both equity and credit financing channels. By month-end, it officially announced the "Digital Credit Capital Framework," with the board authorizing the monetization of up to $1.25 billion in BTC – "selling coins to pay interest" transitioned from a tail risk to an institutionalized reality. The largest price-insensitive buyer of the past two years may not only fail to return but could also become a reverse supply source of approximately 20,000 BTC.

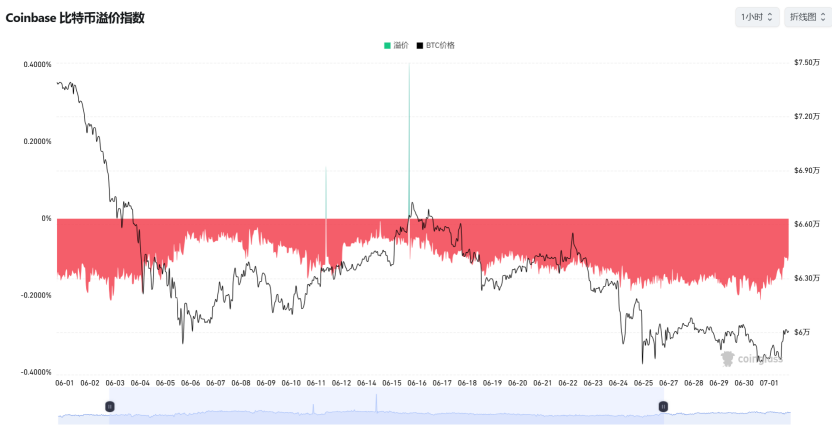

Second, the worst single-month outflow in ETF history. BTC spot ETFs saw a net outflow of approximately $4.51 billion for the month, the largest monthly outflow since the product's inception. This included a record 10 consecutive days of outflows and a panic-level redemption of -$696 million in a single day. ETH spot ETFs simultaneously saw outflows of approximately $529 million. Redemptions exhibited full-spectrum risk aversion characteristics. Coupled with persistently negative Coinbase premiums, marginal selling pressure from US channels dominated throughout the month.

Third, the complete microstructural evolution from capitulation to accumulation. The breakdown on June 24th was a "clean" capitulation driven by spot markets – selling pressure came from coin holders, with leverage merely amplifying it passively. The monthly low of $57.8K on June 30th, however, was a bear trap – spot selling pressure was exhausted, and the final leg of the decline was purely driven by derivatives shorts. This distinction is crucial: capitulatory declines require time for sentiment repair, while trap-type declines only require shorts to admit their mistake.

Our assessment for the month: The deep bear market moved from the "mid-stage of liquidation" into the "deep water of liquidation," achieving preliminary confirmation of "seller exhaustion" by month-end. Three pieces of evidence support this: panic has been fully released (Ahr999 index fell to 0.283, historically a "ghost zone"; loss-making coins on the network exceeded profitable coins for the first time); strong hands have returned to accumulation (LTHs returned to net buying, their supply share rose to a multi-year high of 88.1%, with accumulation showing broad-spectrum characteristics across groups); and a structural change occurred at month-end (MSTR's negative news failed to push BTC to new lows; market makers shifted to long Gamma in the 60-64K range).

But the other side demands caution – the three pillars for a reversal were absent at month-end: ETF outflows hadn't stopped, the USD hadn't weakened, and the price hadn't reclaimed key resistance levels. The STH-SOPR was still 0.14 standard deviations away from the severe capitulation threshold. Historically, cycle bottoms are often accompanied by one final capitulatory volatility spike, which has also not yet materialized.

Extreme undervaluation and accumulation signals define a bottoming zone, not a bottoming point in time. June provided a preliminary confirmation of seller exhaustion, not a final one. A bear trap can explain a tactical rebound, but it cannot define a cyclical bottom.

I. Macro: From "When Will Rates Be Cut" to "Rate Hikes Are Priced In"

In May, the market was still debating whether easing expectations could recover. In June, the macro environment delivered a definitive three-pronged denial.

The first blow: data comprehensively disproved rate cuts. On June 2nd, JOLTS job openings hit 7.62 million, a near two-year high and 750,000 above expectations, pushing the 10-year US Treasury yield back above 4.45%. On June 6th, the May non-farm payrolls report was "hot," dousing hopes for rate cuts. The market immediately priced in a 25bp rate hike before December and a roughly 60% probability of an October hike, triggering a US stock market crash that day (Nasdaq -4.18%, Philadelphia Semiconductor Index -10% intraday). On June 11th, the May CPI was 4.2% YoY, the highest since April 2023. On June 25th, core PCE was 3.4% YoY, the highest since October 2023, and headline PCE at 4.1% breached 4% for the first time in three years – inflation stickiness was repeatedly confirmed by four major data releases.

The second blow: the FOMC's hawkish dot plot. On June 18th, the Fed held rates steady for the fourth consecutive time (3.5%–3.75%), but the SEP underwent a systematic revision towards stagflation: the 2026 median rate was raised from 3.4% to 3.8%, the PCE forecast was raised to 3.6%, and GDP was lowered to 2.2%. New Chair Powell's first press conference set the tone: "Persistently high prices are a burden on the people." Market institutions have already shifted from pricing in rate cuts to pricing in rate hikes.

The third blow: the USD regained dominance. The DXY reclaimed its 200-day moving average (101.80 vs 98.72) in late June, the first time since the April "Liberation Day" shock. The negative correlation between a "strong USD suppressing crypto" seen in 2022-23 has re-established itself after a period of decoupling: the S&P 500 recovered its year-to-date losses and reclaimed its 200-day moving average, while BTC closed the month 18% below its own 200-day MA ($76,466). Macro recovery was a pure equity story; BTC didn't get a ticket to the show. The Bank of Japan's 25bp rate hike to 1.00% on June 16th (highest since 1995) paradoxically led to a weaker Yen, which broke through 162 by month-end to hit a nearly 40-year low, laying the fuse for intervention in global risk assets.

Equity markets experienced extreme roller-coaster moves: The Nasdaq broke 27,000, the Nikkei reached 70,000, and the KOSPI hit repeated highs with multiple two-way circuit breakers in a single month. The June 6th non-farm payrolls triggered a global chain crash (KOSPI circuit breakered at -8.4% in a day). By month-end, the AI capex bubble was systematically priced for the first time: the Philadelphia Semiconductor Index fell 7.87% on June 23rd, Apple dropped 6.1% in a day due to price increases for "passing AI infrastructure costs to end-users," while Micron's blowout earnings and Korea's hundreds of trillions of won national semiconductor investment repeatedly rescued the narrative. For crypto, the brutal truth throughout the month was: there were no spillovers during the AI boom, but full resonance during the AI crash.

II. Geopolitics: Four Rollercoaster Rounds; Crypto Absorbs Bad News, Ignores Good News

June in the Middle East completed a full cycle of "breakdown – actual combat – agreement – renewed fighting – renewed ceasefire."

Early in the month, negotiations rapidly descended into live fire: June 2-3 saw mutual military strikes between the US and Iran; June 10-11 saw multiple US airstrikes on Iranian soil, Iran's announcement of closing the Strait of Hormuz, over 160 oil tankers stranded, and the IMO's first-ever advisory against commercial vessel transit – market pricing briefly switched from a "geopolitical premium" to a "wartime discount rate," with WTI surging to $96.

Mid-month, the script did a 180-degree turn: On June 14th, Trump announced a "birthday gift" agreement and the full opening of the Strait; the MoU was signed remotely on June 17th and took immediate effect. Crude oil crashed from $86 to $76, gold's safe-haven premium was drained, and BTC only managed to reclaim the $65-66K corridor – oil was repricing based on genuine demand outlook, while BTC was merely repricing the disappearance of a headwind.

Late in the month, "sign first, fight later": A cargo ship was attacked by a drone on June 25th; US airstrikes resumed on June 26th, with Iran retaliating against a US military outpost; a ceasefire was again reached on June 28th with a scheduled negotiation in Doha, which Iran then denied, and Israel publicly threatened "independent action."

Gold fell from $4,483 at the start of the month to lose the $4,000 mark by month-end, losing about 10% for the month. Every injection and withdrawal of the geopolitical risk premium was priced by precious metals, but BTC refused to absorb any de-escalation and fell fully on any escalation – the "digital gold" narrative was thoroughly disproven in June. BTC was traded entirely as a high-beta risk asset throughout the month.

III. Capital Flows: Largest Single-Month ETF Outflows in History, Weakening Buyer Absorption

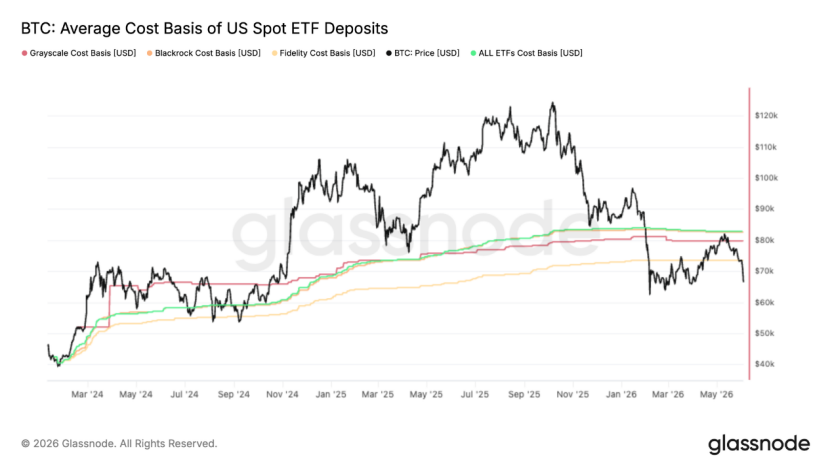

First, BTC spot ETFs suffered record outflows of approximately -$4.51 billion for the month, with a rhythm of "three waves of amplification": early-month crash period with 11 consecutive days totaling -$3.45 billion, a single-day peak of -$520 million; mid-month geopolitical easing period with only two or three minor inflow days worth tens of millions, and the consecutive outflow streak becoming the longest since inception; late-month deterioration even against a supposedly easing geopolitical backdrop, with a single-day outflow of -$696 million on June 25th, a new interim high. This round of redemptions was "orderly but persistent," more indicative of rational profit-taking by institutions who built positions at much lower prices, rather than pure panic – but this doesn't change the conclusion: "good news doesn't bring flows back, bad news accelerates flight," with the most important incremental inflow channel in a state of drainage all month. The 82.8K rally in mid-May was precisely rejected at the ETF aggregate cost basis of 83K – the average ETF investor remained underwater all month, and "bag holders reducing positions on rallies" created a structural top-side supply.

Second, ETH spot ETFs saw net outflows of approximately $550 million for the month. The only hedging force came from the DAT side: Bitmine increased its holdings by ~280,000 ETH counter-cyclically, totaling 5.7 million ETH; Sharplink restarted accumulation after an 8-month hiatus. However, overall DAT AuM in the industry has shrunk from $220 billion to $140 billion, with financing virtually halted except for the top two or three players. Corporate treasury net inflows plummeted from a peak of $500M+/day in April-May to near zero in June – yet another marginal buyer went dark.

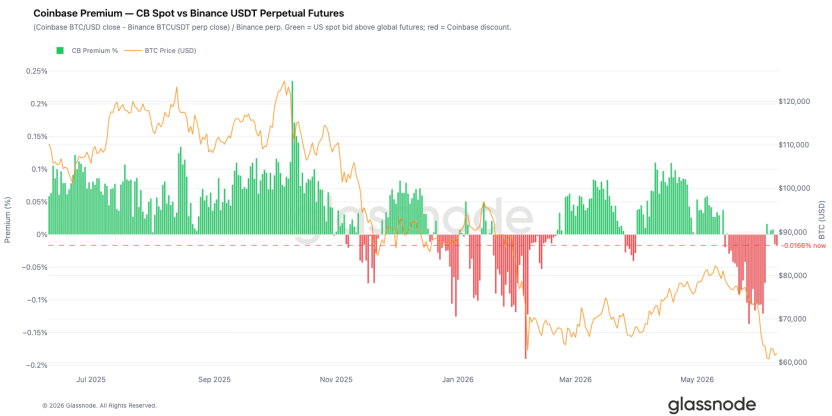

Third, the Coinbase premium was deeply negative throughout the month, but late in the month, the most important marginal change occurred: after BTC broke below $62K, the Coinbase Spot CVD Bias turned positive first, while Binance remained negative – US institutions began absorbing in the spot market, while offshore speculative capital remained on defense. Combined with the Binance order book depth imbalance turning to the strongest buy-side dominance in months, this "sell ETF + buy spot" hedging structure reveals that genuine US buying interest had already re-emerged at these lower levels.

Third, the Coinbase premium was deeply negative throughout the month, but late in the month, the most important marginal change occurred: after BTC broke below $62K, the Coinbase Spot CVD Bias turned positive first, while Binance remained negative – US institutions began absorbing in the spot market, while offshore speculative capital remained on defense. Combined with the Binance order book depth imbalance turning to the strongest buy-side dominance in months, this "sell ETF + buy spot" hedging structure reveals that genuine US buying interest had already re-emerged at these lower levels.

Third, the Coinbase premium was deeply negative throughout the month, but late in the month, the most important marginal change occurred: after BTC broke below $62K, the Coinbase Spot CVD Bias turned positive first, while Binance remained negative – US institutions began absorbing in the spot market, while offshore speculative capital remained on defense. Combined with the Binance order book depth imbalance turning to the strongest buy-side dominance in months, this "sell ETF + buy spot" hedging structure reveals that genuine US buying interest had already re-emerged at these lower levels.

IV. On-Chain: Structural Shift from Rally Disproof to Accumulation Emergence

June presented the most contradictory yet information-rich on-chain picture of the month, with the overall evolution tracing a clear "disproof – capitulation – repair – accumulation" chain.

The initial core signal was the disproof of the rally. The 7-day moving average of the Realized Profit/Loss Ratio crashed from 3.16 to 0.29, with the 90-day moving average failing to touch the 2.0 threshold throughout the period, confirming the 82K rally as a bear market dead-cat bounce rather than a structural shift. The short-term holder cost basis dipped below the real market mean for the first time since January 2022, formally establishing a "late bear market" structure. Single-day realized losses amplified to $1.35 billion, with $770 million coming from panic selling by cycle-top buyers, indicating substantial liquidation of high-position bags.

Subsequently, capitulation deepened but didn't reach historical extremes. The AVIV z-score bottomed at -1.09, deep into historically extreme discount territory. The short-term holder profitable supply ratio briefly stood at only 0.6% (4-year average is 55%), meaning over 95% of new buyers were simultaneously underwater. The STH-SOPR z-score hit a low of -1.86, just 0.14 standard deviations away from the -2 "severe capitulation" threshold. The market is in a typical uncomfortable intermediate state – loss realization is sufficient to confirm a deep bear market, but hasn't yet reached the final intensity to catalyze a durable rebound.

Entering the second half of the month, signs of repair began to emerge. The short-term holder cost basis shifted down to $71.4K, with new buyers systematically building positions below the cycle mean for the first time – a key early step in bottom structure formation. The Net Realized P/L 90-day moving average remained at -$205 million/day, continuing to tilt market gravity towards the Realized Price ($53.4K). The short-term supply cluster in the $66.8K–$70.7K range was clearly marked as the most immediate overhead resistance zone.

The most important change at month-end was the emergence of accumulation, showing broad-spectrum characteristics across groups for the first time. The Long-Term Holder Net Position Change returned to positive territory, ending the prolonged distribution phase. The Accumulation Trend Score rose significantly, with cohorts holding <1 BTC and 100–1,000 BTC showing near-perfect accumulation scores, while large holders (1k–10k BTC) similarly turned to net buying. LTH supply share rose to 88.1%, a multi-year high. Concurrently, a cycle-level milestone occurred: loss-making coins on the