韩国券商一句业绩“不及预期”,SK海力士大跌12%,存储板块全线承压

- 核心观点:韩国券商KIS下调SK海力士第二季业绩预期,引发股价暴跌,主因并非基本面恶化,而是其HBM(高频宽记忆体)营收占比过高,长期合约价格锁定导致平均售价涨幅低于市场预期,但长期获利可持续性逻辑未变。

- 关键要素:

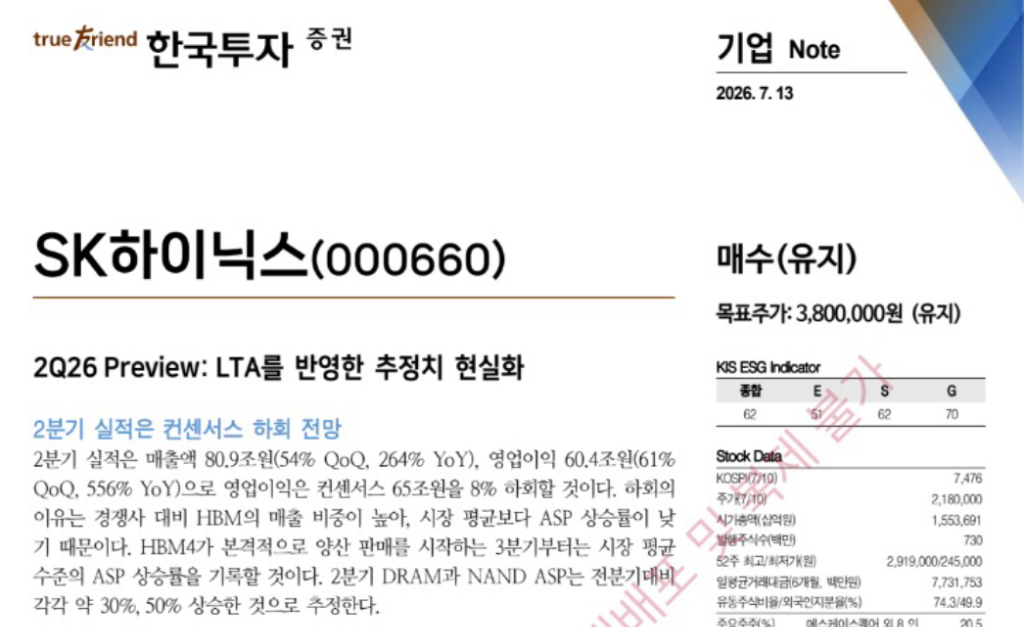

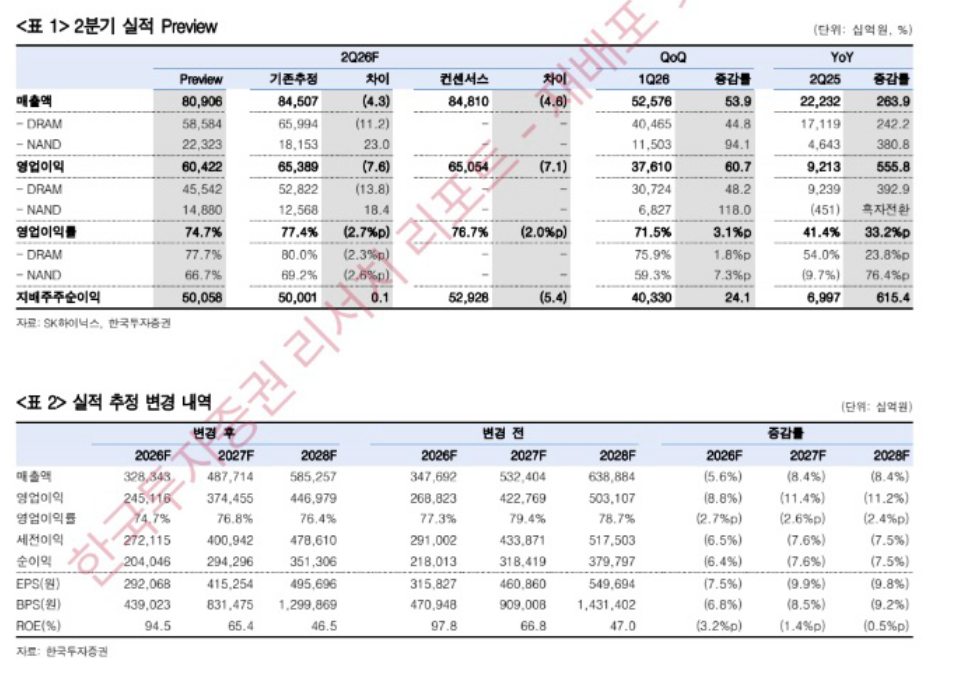

- KIS预测SK海力士Q2营业利润约60.4万亿韩元,低于市场共识的65万亿韩元约8%,直接引发股价单日跌逾10%,较历史高点回档33%。

- 获利不及预期核心原因:HBM因长期合约(LTA)价格固定,未能充分捕捉同期DRAM(均价上涨30%)和NAND(均价上涨50%)的现货涨价红利。

- KIS指出预期下修仅为修正LTA价格假设,非业绩疑虑,并维持目标价380万韩元及增持评级,预计2026年Q2营业利润率将达到74.6%创历史新高。

- 市场情绪脆弱,叠加SK海力士美股ADR上市后资金套现,导致卖压加剧,并传导至港股杠杆ETF(单日跌逾22%)及A股存储概念股。

- 行业趋势:随着LTA合约结构扩展至3-5年,估值核心驱动力从单季ASP涨幅转向获利可持续性,合约营收占比提升将降低业绩波动性。

Original Author: Long Yue

Original Source: Wall Street Sights

On July 13, South Korean local brokerage KIS released its Q2 earnings forecast for SK Hynix. It projects SK Hynix's Q2 revenue at 80.9 trillion Korean won, up 54% quarter-on-quarter and a massive 264% year-on-year; operating profit is estimated at 60.4 trillion Korean won, up 61% QoQ and 556% YoY.

The numbers look impressive, but the issue is: Market consensus expectations were for 65 trillion Korean won, and KIS's forecast is about 8% below that consensus.

This deviation directly ignited the market.

After the South Korean stock market opened, SK Hynix's share price quickly fell over 10%, breaking below the 2 million won mark. This represents a 33% correction from its all-time high on June 25 in just three weeks.

High HBM Proportion Actually Drags Down ASP

In its report, KIS explained the core reason for the profit shortfall against consensus: SK Hynix's proportion of revenue from HBM (High Bandwidth Memory) is higher than its peers, with a higher shipment share, causing its average selling price (ASP) growth to lag behind the market average.

This logic seems counterintuitive at first glance – HBM is a high-end product; shouldn't a higher proportion mean more profit?

The key lies in the pricing structure. HBM prices are typically locked in via long-term supply contracts (LTAs). These contract prices are relatively fixed and do not increase significantly in the short term along with market fluctuations. In contrast, regular DRAM and NAND have higher price elasticity in the spot market. When the overall market prices rise, the ASP growth for these products tends to be larger.

SK Hynix's high HBM proportion means it has "enjoyed less benefit from the price increase" in this round of market average price uptrend compared to its peers.

During the same period, the average spot prices of regular DRAM and NAND were still soaring – KIS forecasts Q2 DRAM average prices to rise about 30% QoQ and NAND about 50% – but SK Hynix's overall ASP growth was "held back" by the contract prices of HBM.

Downgrade Due to Recalculated LTAs, Not Fundamentals Deterioration

In its report, KIS explicitly stated that this downgrade is not due to concerns over performance, but is a revised result after incorporating the price assumptions of signed long-term supply contracts (LTAs) into the calculations.

The report's original text states: "This is a result of making the forecast more realistic by incorporating signed LTA price assumptions, and is not a concern about performance."

KIS also lowered its operating profit forecasts for 2026 and 2027, approximately 9% and 11% lower than previous estimates, respectively. However, the brokerage emphasized that with the official mass production shipment of HBM4 starting from the third quarter, the market average price uptrend will drive overall ASP higher. At that point, SK Hynix's ASP growth rate will return to the market average level.

KIS predicts the Q2 2026 operating profit margin will reach 74.6%, a new all-time high, and will continue to rise quarterly thereafter.

The brokerage maintains its target price of 3.8 million Korean won and an overweight rating, believing that this forecast downgrade is merely a short-term disruption and does not change the medium-to-long-term earnings uptrend.

"A 556% Surge Falls Short of Expectations": The Crack in Market Sentiment

A 556% year-on-year increase is an extremely strong number in any industry. But the logic of the capital market is: What matters is not how much it increased, but whether it met expectations.

The market had already fully priced in the consensus expectation of 65 trillion Korean won. KIS's forecast was about 4.6 trillion Korean won lower than this number, effectively signaling "expectations were too high."

This triggered two layers of concern: first, the direct impact of short-term earnings missing expectations; second, whether the high proportion of HBM poses a structural risk – meaning the more SK Hynix bets on HBM, the more constrained its ASP flexibility becomes during the contract price lock-in period.

Compounding this was the fact that SK Hynix just listed on the US stock market last Friday. Some capital that had bet on the IPO chose to cash out after the ADR listing, further exacerbating the selling pressure.

Contagion Spreads: Hong Kong ETFs and A-Share Memory Stocks Plunge Simultaneously

SK Hynix's decline quickly transmitted to neighboring markets.

In Hong Kong stocks, the 2x Long SK Hynix Leveraged ETF fell over 22% in a single day, while the 2x Long Samsung Electronics ETF dropped over 13%.

A-share memory concept stocks followed suit, with core names like Gigadevice, Ingenic Semiconductor, Longsys Electronics, and Biwin Storage all falling over 7%.

However, from a broader macro perspective, the memory semiconductor sector has been in a correction period for nearly half a month. Some individual stocks have fallen over 20%, crossing the technical bear market threshold. Behind this are factors such as global funds rebalancing allocations within the AI sector and across different markets, including a rotation logic of "selling chips, buying cloud," as well as a phased rebound in the Hong Kong stock market attracting capital back.

Brokerage: Long-Term Thesis Unchanged, Focus on Earnings Sustainability

Despite triggering market turmoil, KIS's overall stance in the report is not pessimistic.

The brokerage believes that as the memory industry shifts towards a 3-5 year LTA contract structure, the core driver of corporate valuations will transition from "single-quarter ASP growth" to "how long high profitability can be sustained."

The KIS report notes: "From now on, the focus needs to be on the sustainability of earnings. The expansion of LTAs is reducing the long-standing volatility of the memory industry's performance."

The brokerage expects that with the increase in contract-based revenue share and the squeezing effect of HBM capacity expansion on overall supply, SK Hynix's high profitability levels can be maintained long-term, and its valuation will correspondingly be repriced.

The target price of 3.8 million Korean won still represents significant upside from the current share price. KIS maintains its overweight rating.