Gate 機構週報:BTC 價格低位修復,Gate 美股交易量再創階段新高

- 核心觀點:上週加密市場風險偏好修復,BTC 與 ETH 均上漲,ETF 資金淨流出放緩,ETH ETF 率先出現小幅回流;市場結構分化,Solana 生態(PumpSwap)貢獻主要增量,穩定幣供給偏弱但機構化通道利好 USDC。

- 關鍵要素:

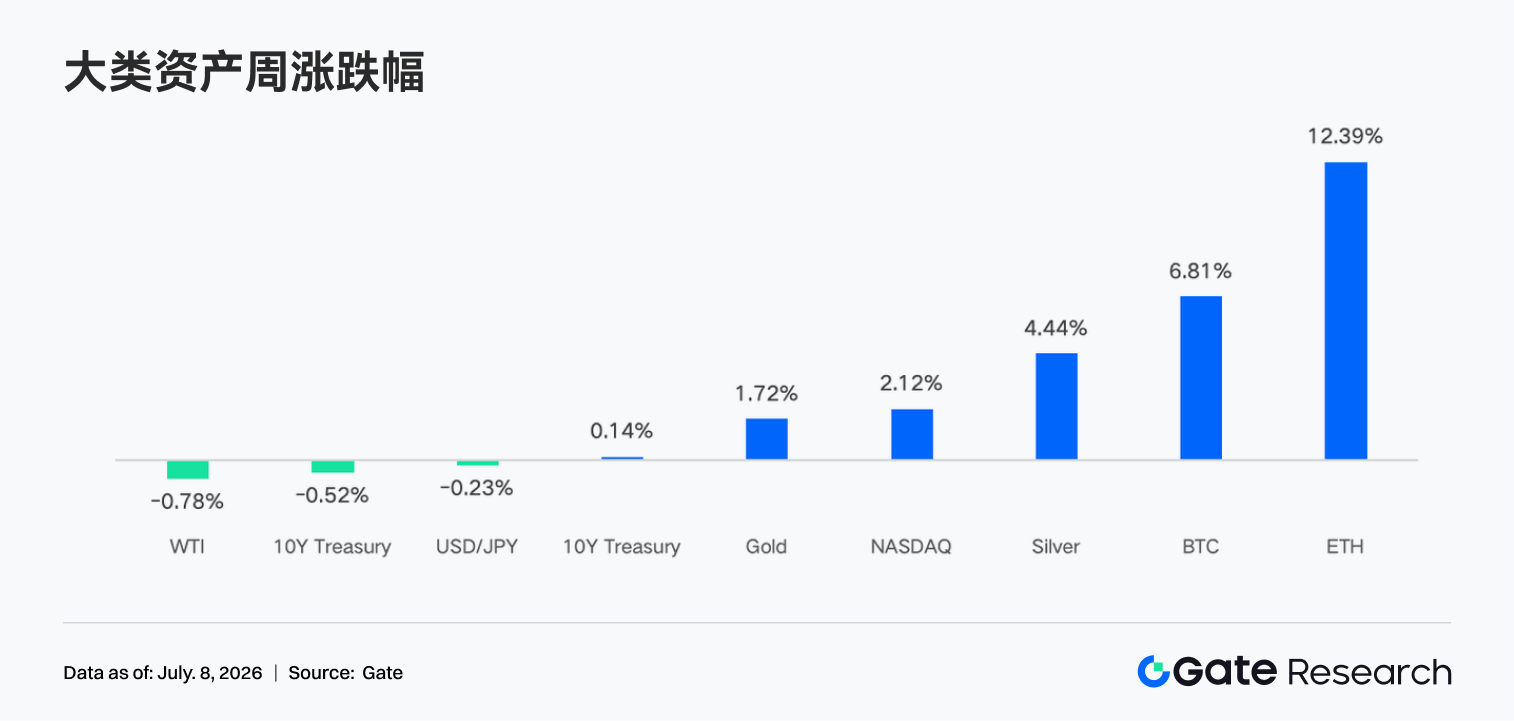

- 美國6月非農就業數據低於預期,市場對聯準會加息擔憂降溫,推動風險資產整體走強,BTC 週漲約 6.8%,ETH 週漲約 12.2%。

- BTC 現貨 ETF 週淨流出約 17.87 億美元,但 7 月 2 日單日出現淨流入;ETH 現貨 ETF 週淨流出約 0.1365 億美元,資金已開始試探性回補。

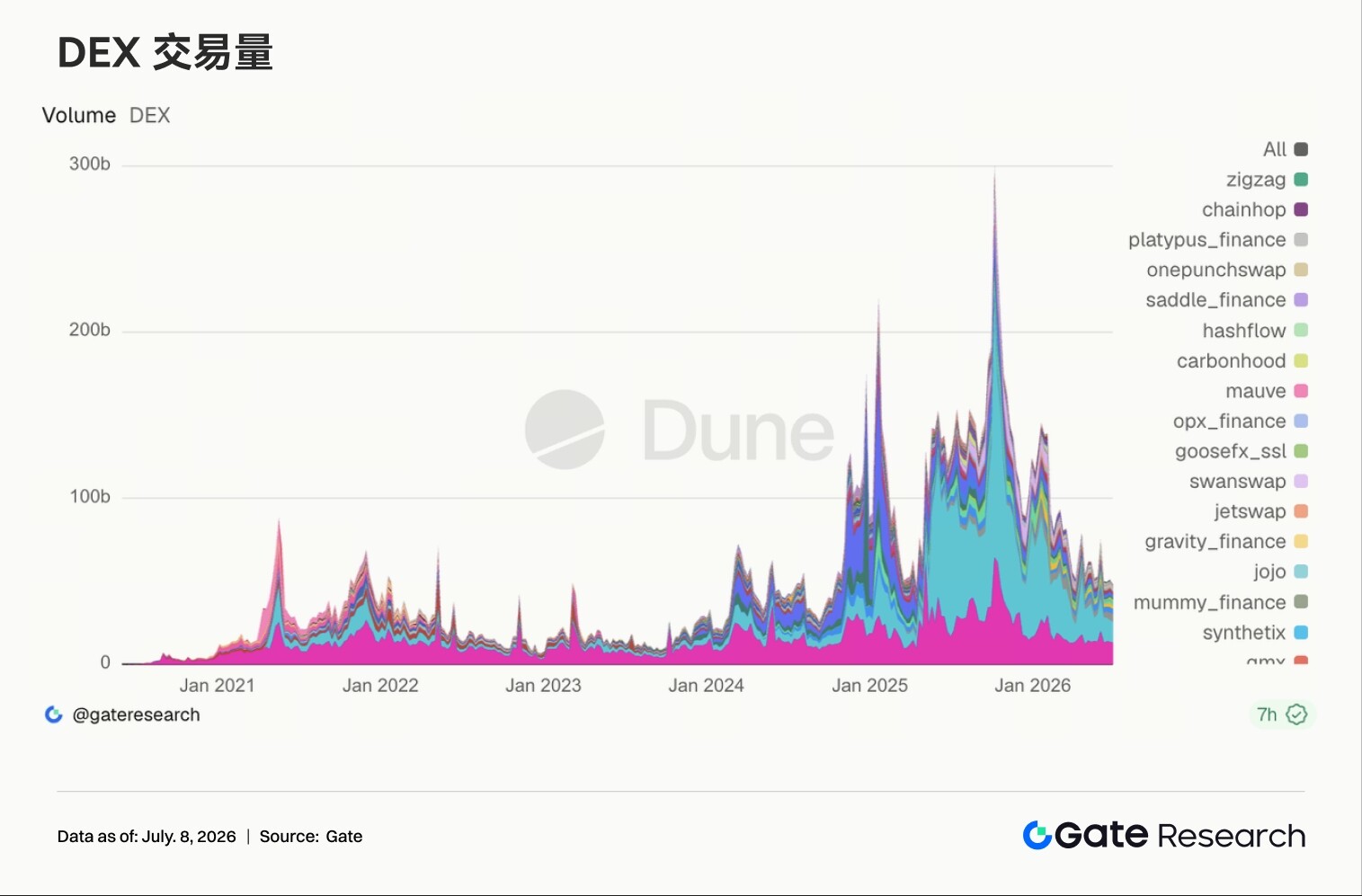

- DEX 交易結構分化,Uniswap 成交回落,Solana 生態的 PumpSwap 高增長,帶動 Solana 成為資金與協議收入的主要增量來源。

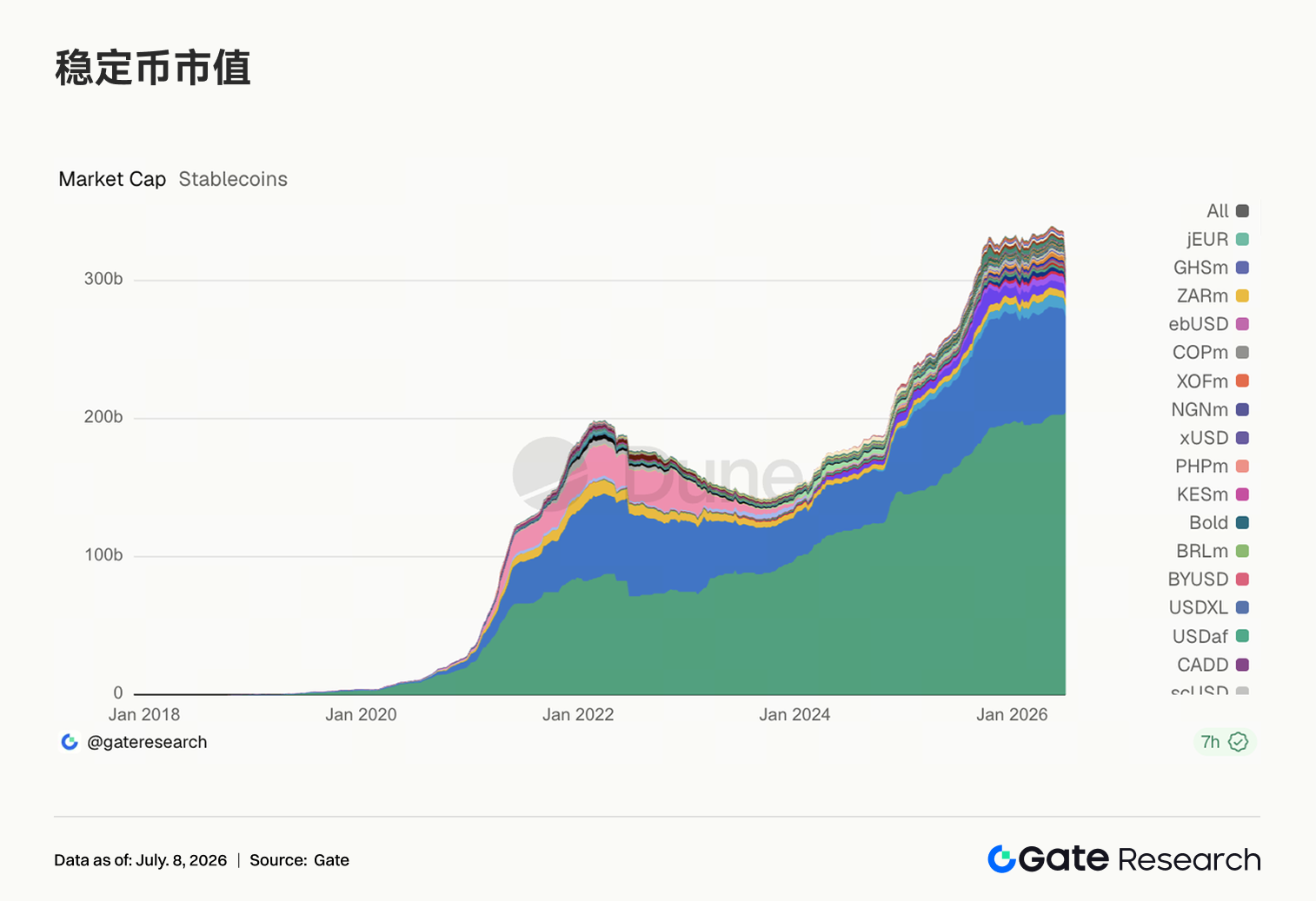

- 穩定幣供給整體偏弱,但 USDC 受 BNY Mellon 支持托管等利好,機構化通道持續強化;Aave 上 USDC 借款利率上升,反映高品質美元流動性需求回暖。

- BTC OI 由約 205 億美元回升至 220 億美元,資金費率維持正值,槓桿資金重新進場;期權 25D Skew 自深度負值修復,DVOL 回落至 39-40,波動預期降溫。

- Gate 平台6月現貨交易量月環比增長 49.39%,CrossEx Q2 交易量創新高,7月首週週環比增長 26%,機構與平台交易活躍度持續提升。

Summary

• Risk appetite in the crypto market is recovering, with BTC up approximately 6.8% and ETH up approximately 12.2% for the week. ETF funds are still seeing net outflows overall, but the ETH ETF has shown a slight return of capital, with institutional sentiment shifting from panic-driven redemptions to tentative rebalancing.

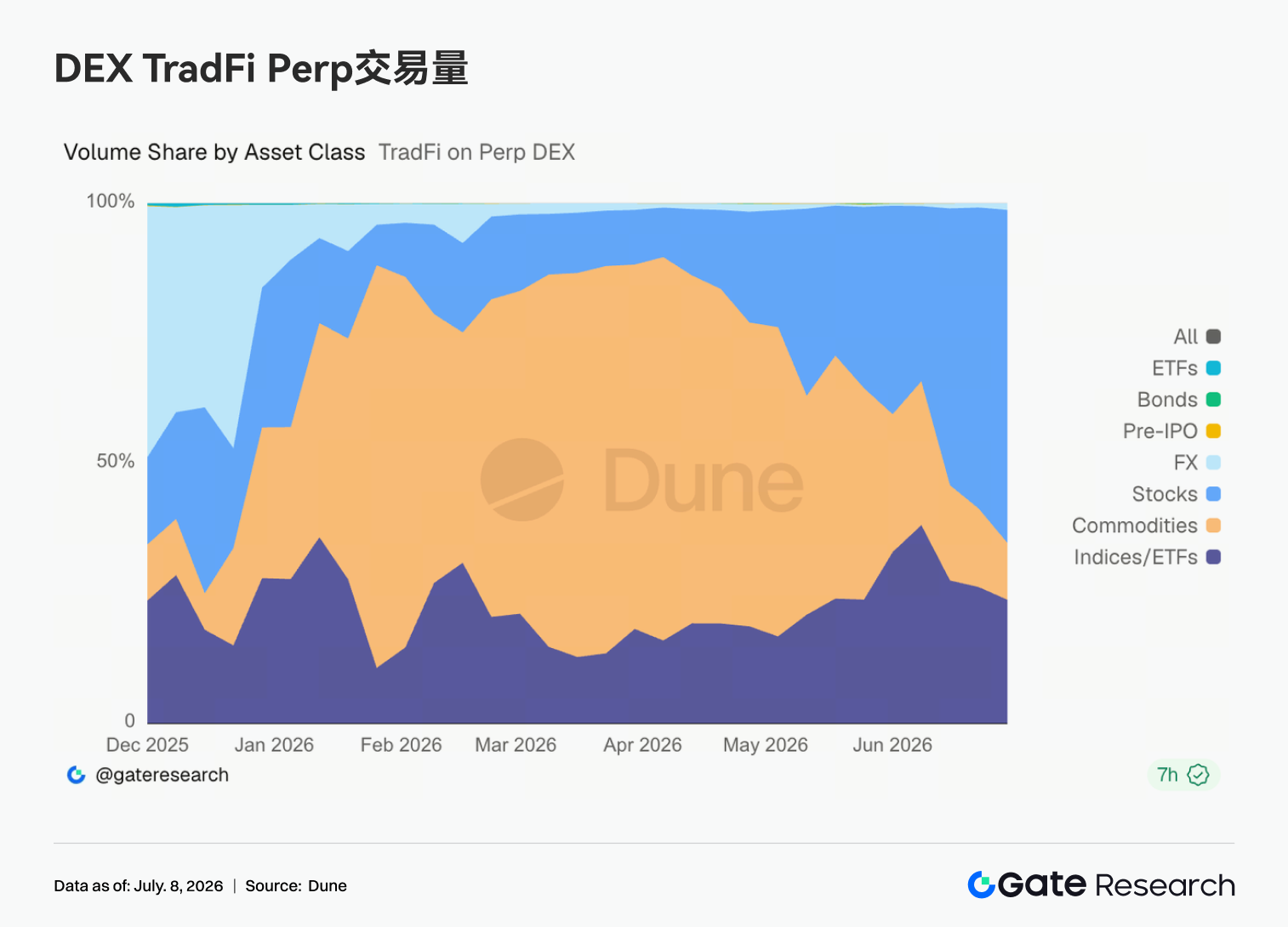

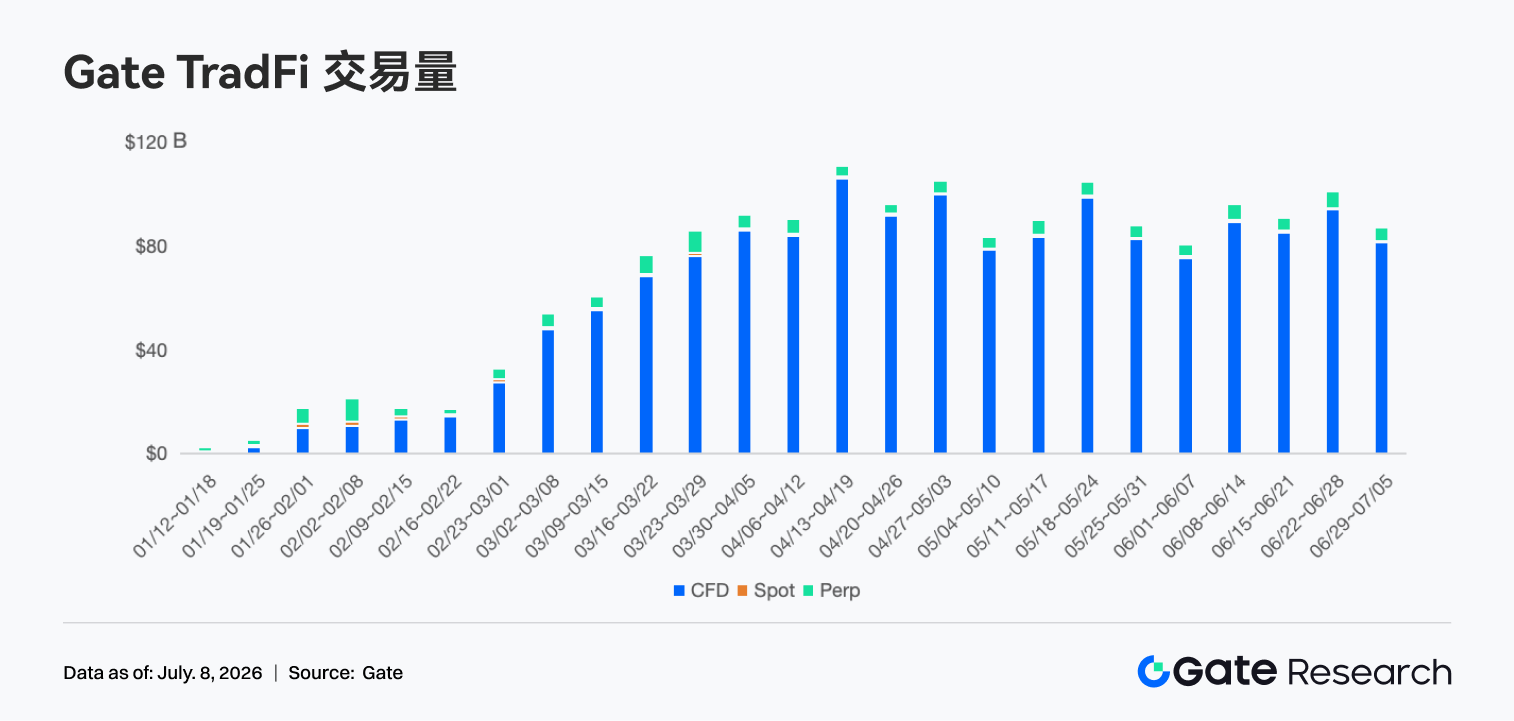

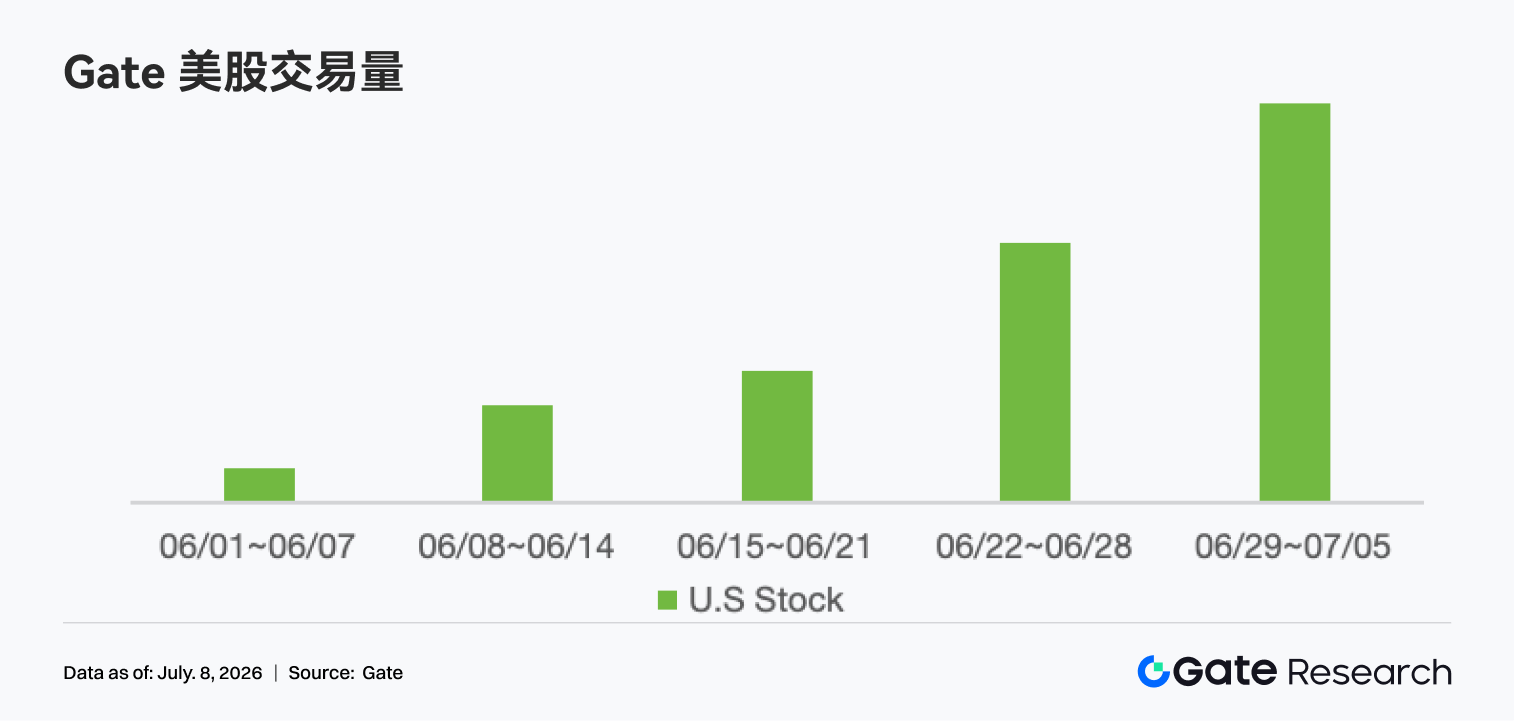

• TradFi stock Perp trading volume share has risen to approximately 60%–65%. Gate TradFi weekly trading volume remains high at around $85 billion, with CFDs still contributing approximately 95% of the volume. US stock trading volume has grown for five consecutive weeks and reached a new phase high.

• DEX trading structure continues to diverge. Volumes on Uniswap and PancakeSwap have declined, while PumpSwap maintains high growth, driving Solana's issuance, trading, and wallet ecosystem to become the main incremental source of capital and protocol revenue.

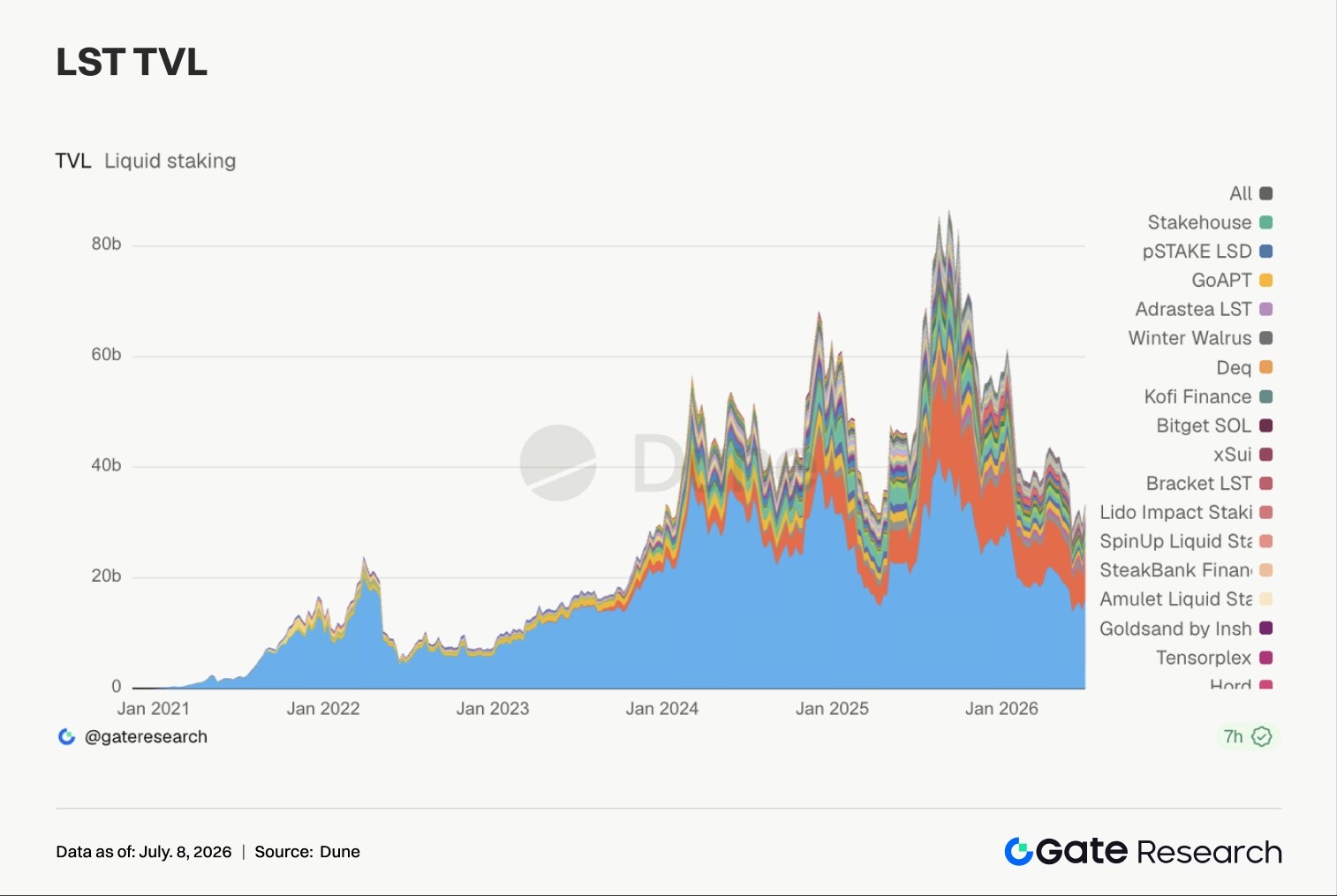

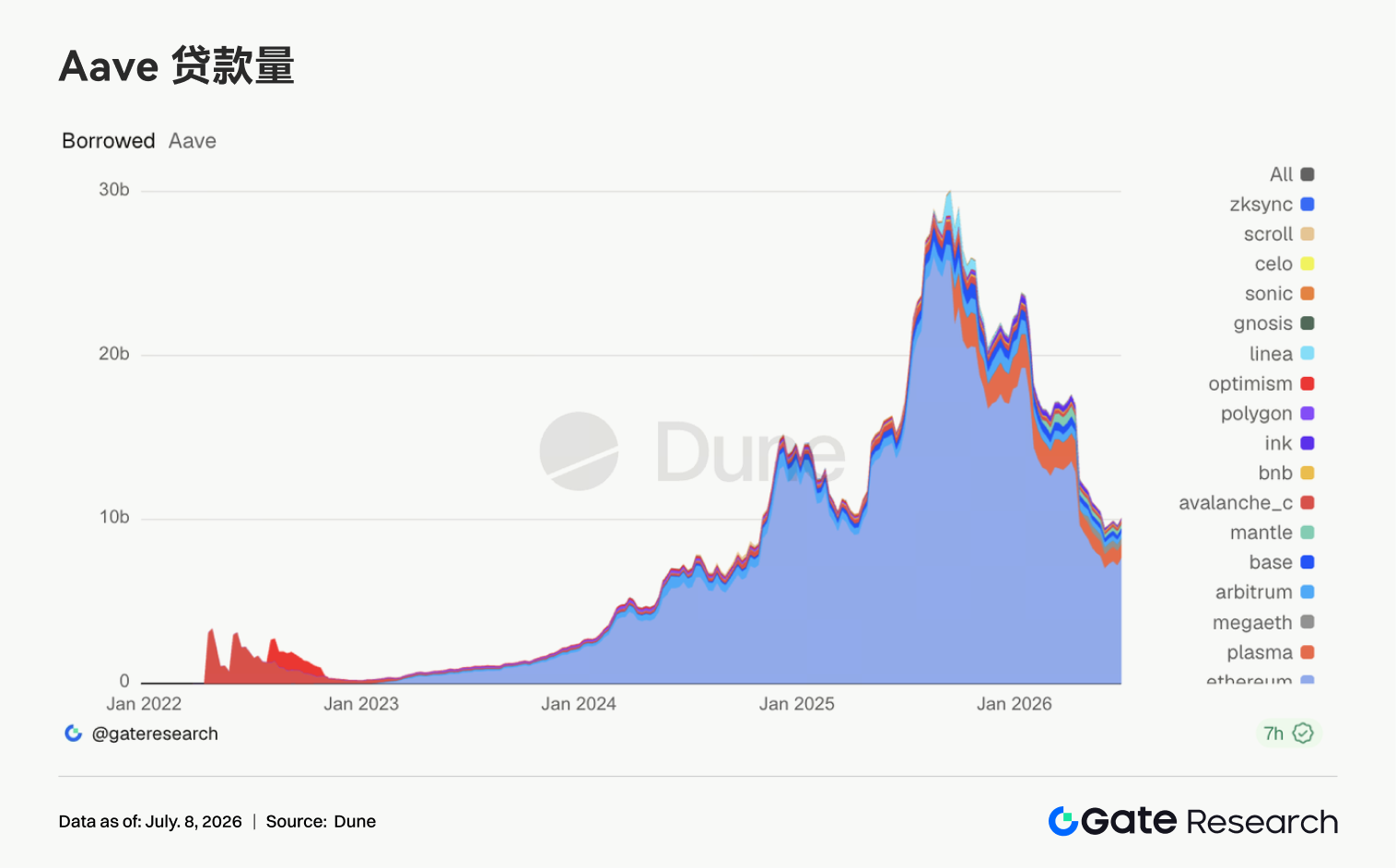

• The LST sector is also recovering concurrently. Staked assets in ETH and SOL have rebounded alongside the improvement in risk appetite, while Aave's lending demand is re-concentrating on the Ethereum main market.

• Stablecoin supply remains generally weak, but USDC's institutional channels continue to strengthen with support from institutions like BNY Mellon. The rise in Aave USDC borrowing rates reflects a recovery in demand for high-quality USD liquidity, and protocol revenue is shifting from on-chain derivatives towards the Solana traffic gateway.

• BTC OI has recovered from approximately $20.5 billion to $22 billion, with funding rates remaining positive, indicating leveraged capital is re-entering the market. Options volume has also picked up concurrently. The 25D Skew has recovered from deeply negative levels, and DVOL has fallen from 46–48 to 39–40.

• Gate's platform spot and futures trading volumes in June grew by 49.39% and 11.19% month-over-month, respectively. Gate Institutional's spot and futures trading volumes grew by 17.71% and 10.70% month-over-month, respectively. In the first week of July, CrossEx trading volume grew by 26% week-over-week.

1. Market Focus

Last week (June 29 to July 5, 2026), the global market narrative was driven by a combination of cooling US employment, falling interest rate expectations, and the recovery of risk appetite. The US added 57,000 non-farm payrolls in June, below the market expectation of approximately 115,000. Data for April and May was revised down by a total of 74,000. The unemployment rate edged down to 4.2% from 4.3%, but this was mainly due to a decline in labor force participation.

Following the data release, market concerns about a Fed rate hike in July diminished. The 10-year US Treasury yield settled around 4.4477% after weekly fluctuations, while the 2-year yield fell to approximately 4.13%, marginally easing interest rate pressures. US stocks broadly rose during the shortened holiday trading week. The Dow Jones gained about 2.0% for the week, the S&P 500 rose about 1.8%, and the Nasdaq climbed about 2.1%. However, rotational pressure emerged in the AI and semiconductor sectors, indicating that capital was not solely chasing high-valuation growth stocks but was repricing risk assets under a "slowing economy but no more hawkish policy" framework. In commodities, oil prices oscillated between the risk premium from the Middle East and expectations of increased OPEC+ production, with WTI crude trading around $70. Gold remained at elevated levels, reflecting lingering inflation and geopolitical risks. The crypto market benefited from falling US Treasury yields, easing pressure on USD liquidity, and improved risk appetite in US stocks. Both BTC and ETH strengthened during the week, with ETH showing higher elasticity, suggesting capital was shifting from defensive BTC allocations towards higher-beta assets.

2. Liquidity Analysis

2.1 ETF Still in Significant Net Outflow, BTC ETF Weekly Net Outflow of ~$1.787 Billion

Regarding ETFs, the BTC spot ETF continued to see significant net outflows last week. US BTC spot ETFs saw a weekly net outflow of approximately $1.787 billion, extending the pressure from large redemptions seen in June. However, July 2 saw a single-day net inflow of $221.72 million, ending a streak of approximately 10 trading days with cumulative outflows of around $2.73 billion. On a sequential AUM basis, the total net assets of BTC spot ETFs were approximately $72.818 billion on June 26, rising to $74.369 billion on July 2, an increase of about $1.551 billion, mainly driven by the BTC price rebound offsetting net redemptions. By individual product, Fidelity's FBTC saw the largest inflow on July 2, at approximately $166 million, followed by ARKB at roughly $91.84 million. The most notable outflow was from BlackRock's IBIT, with a single-day outflow of about $40.43 million, and it remains in a continuous outflow narrative.

The pressure on ETH spot ETFs was significantly less than on BTC. Combined public daily frequency data indicates a net outflow of approximately $13.65 million between June 29 and July 2. This includes outflows of roughly $30.04 million on June 29 and $27.6 million on June 30, turning into inflows of approximately $14.89 million on July 1 and $29.08 million on July 2. AUM rose from approximately $8.594 billion on June 29 to about $9.020 billion on July 2, an increase of some $426 million, more attributable to the ETH price rebound and minor capital rebalancing. At the product level, ETHA was among the top inflows on July 1 and July 2, with about $29.74 million flowing in on July 2. Products like ETHE/ETHB bore the brunt of redemption pressure during the week.

Overall, institutional sentiment is not a full turn to bullish but rather a shift from panic redemptions to tentative rebalancing: BTC still needs inflows from IBIT to confirm the trend, while ETH shows small-scale capital starting to return at lower levels.

2.2 TradFi Liquidity

• TradFi Perp DEX: Over the past week, the trading volume structure of the TradFi Perp DEX continued to concentrate towards stock assets. The share of trading volume for stock perpetual contracts rapidly increased to approximately 60%–65%, once again becoming the absolute market dominant. The share of commodity trading volume, which had been dominant previously, continued to fall to about 10%–15%, indicating a cooling off in safe-haven trades like gold and crude oil. Meanwhile, the share of Index/ETF contracts remained stable at around 20%. Other asset classes like FX, bonds, Pre-IPO, and ETFs still accounted for a low share of total volume, contributing little. Market capital continues to concentrate on high-liquidity stock products.

• Gate TradFi Trading Volume: In the past week, Gate TradFi's total trading volume was approximately $85 billion, a week-over-week decrease of about 13%–15%. Last week, total trading volume was close to $98 billion, hitting a recent high. This week it fell back to about $85 billion, but it is still higher than levels seen in late May and early June, indicating that overall trading activity remains stable. CFDs remain the absolute core business. CFD trading volume was approximately $81 billion, accounting for about 95% of the total. Although down from last week, they still contribute the vast majority of volume, continuing to be the primary growth driver for the Gate TradFi product suite. Perps remain resilient. Perp trading volume maintained a range of $400–$500 million, representing about 5%, with little overall change. This suggests that demand for derivatives trading remains stable against a backdrop of moderating market volatility.

• Gate US Stock Asset Trading Volume: Gate officially launched its US stock trading service on June 2. Leveraging advantages such as support by real underlying assets, the ability to trade directly with USDT, no overnight holding fees, and high liquidity, Gate's US stock trading volume continued its rapid growth over the past week, hitting a new phase high and further improving from the previous week. This extends the trend of growth seen for five consecutive weeks since the beginning of June. User participation continues to increase with the successive launches of features like US stock trading, pre-market and after-hours trading, web-based trading, and 24/7 trading. At the same time, weakening US employment data spurred a recovery in market risk appetite, leading to active US stock trading volume, which further promoted the growth of the platform's US stock trading volume. This reflects that Gate's global stock business is entering an accelerated expansion phase.

• TradFi Order Book Depth: We selected XAUT, the asset with the highest TradFi trading volume, to analyze its order book depth (Delta). Over the past week, green Delta bars significantly outnumbered red bars, especially on July 1, 3, and 6, where there were multiple instances of net buy-side liquidity increases ranging from $500,000 to $800,000. This indicates that market makers are continuously replenishing bid orders, demonstrating strong market support capacity. The price of XAUT rose from around $4,000 to the $4,160–$4,180 range. During this period, the buy-side depth of the order book increased concurrently, suggesting that the upward movement was more supported by genuine liquidity rather than short-term price spikes on thin depth. Although there were some negative Delta values of $200,000 to $500,000 between July 2 and July 5, these periods were short-lived and did not form a continuous liquidity drain, having a limited impact on the price. Overall, the latest large buy-side liquidity injection means that a strong liquidity support level has formed around $4,150. In the short term, if macro safe-haven sentiment persists, the depth structure of XAUT will be conducive to maintaining price strength.

3. On-Chain Data Insights

3.1 Top DEX Spot Volumes Continue to Cool, PumpSwap Brings Solana Speculative Flow Back to the Forefront

The structure of the DEX trading narrative continued to shift this week. Uniswap and PancakeSwap firmly held the top two spots, but their volumes edged lower compared to the previous week, with no significant expansion in turnover for mainstream spot pools. PumpSwap, however, continued its upward trend, maintaining high levels of both volume and active traders. Speculative flows on Solana are pivoting towards platforms integrating issuance and secondary trading. Meteora also saw some recovery, but more mature liquidity venues like Raydium, Curve, and Aerodrome showed flatter performance, indicating that capital is not flowing into a broad cross-chain rally.

3.2 Stablecoin Supply Generally Weak, but USDC's Institutional Channels Continue to Open

Stablecoin supply remained somewhat contracted this week. Most major assets like USDT, USDC, USDS, USD1, and USDe saw slight declines, with no large-scale new USD inflows appearing on-chain. A relative bright spot was the expansion of PYUSD, and DAI remained relatively stable, reflecting capital doing small-scale reallocations between regulatory and yield narratives. BNY Mellon announced this week that it would support the custody, transfer, minting, and burning of USDC on its digital asset platform. This is a material positive for USDC's institutional channels. Meanwhile, news that BlackRock, Google, Coinbase, and others are participating in supporting Open USD also indicates that the stablecoin competition is shifting towards embedding them into payment, custody, clearing, and institutional wallets. However, opposition from community banks to stablecoin legislation is still brewing, and regulatory hurdles have not disappeared.

3.3 LST Sector Clearly Recovers from Last Week's Setback, ETH and SOL Staked Assets Rebound Simultaneously

The LST sector saw a clear recovery this week. ETH-side protocols like Lido, Rocket Pool, and StakeWise all rebounded from their lows last week. The SOL side was similarly resilient, with Jito, Sanctum, and Jupiter Staked SOL all experiencing varying degrees of rebound. Since TVL is denominated in USD, this recovery is linked to the price recovery of ETH and SOL, but it also indicates that the de-risking of the previous week did not evolve into sustained redemption pressure. Following the KelpDAO/rsETH incident, institutional judgment on LSTs remains more focused on safety and route clarity, with the risk premium between standard LSTs and cross-chain wrapped assets already having diverged. Overall, this week's LST recovery was driven by both valuation repair and the rebound in risk appetite.

3.4 Aave Lending Activity Rebounds, Led by Ethereum Main Market; Multi-Chain Structure Still Divergent

Aave's lending balances saw a recovery this week. The primary growth came from the Ethereum main market, showing that when risk appetite returns, capital still prioritizes the core market with the deepest liquidation depth and strongest collateral quality. Markets like Arbitrum, Base, Mantle, and Ink also saw slight improvements. However, Plasma and MegaETH continued to decline, slowing the pace of expansion in newer markets from previous periods. This structure aligns with the risk-recovery logic seen in past weeks: Aave hasn't lost lending demand, but capital is more selective about chains, collateral types, and risk parameters.

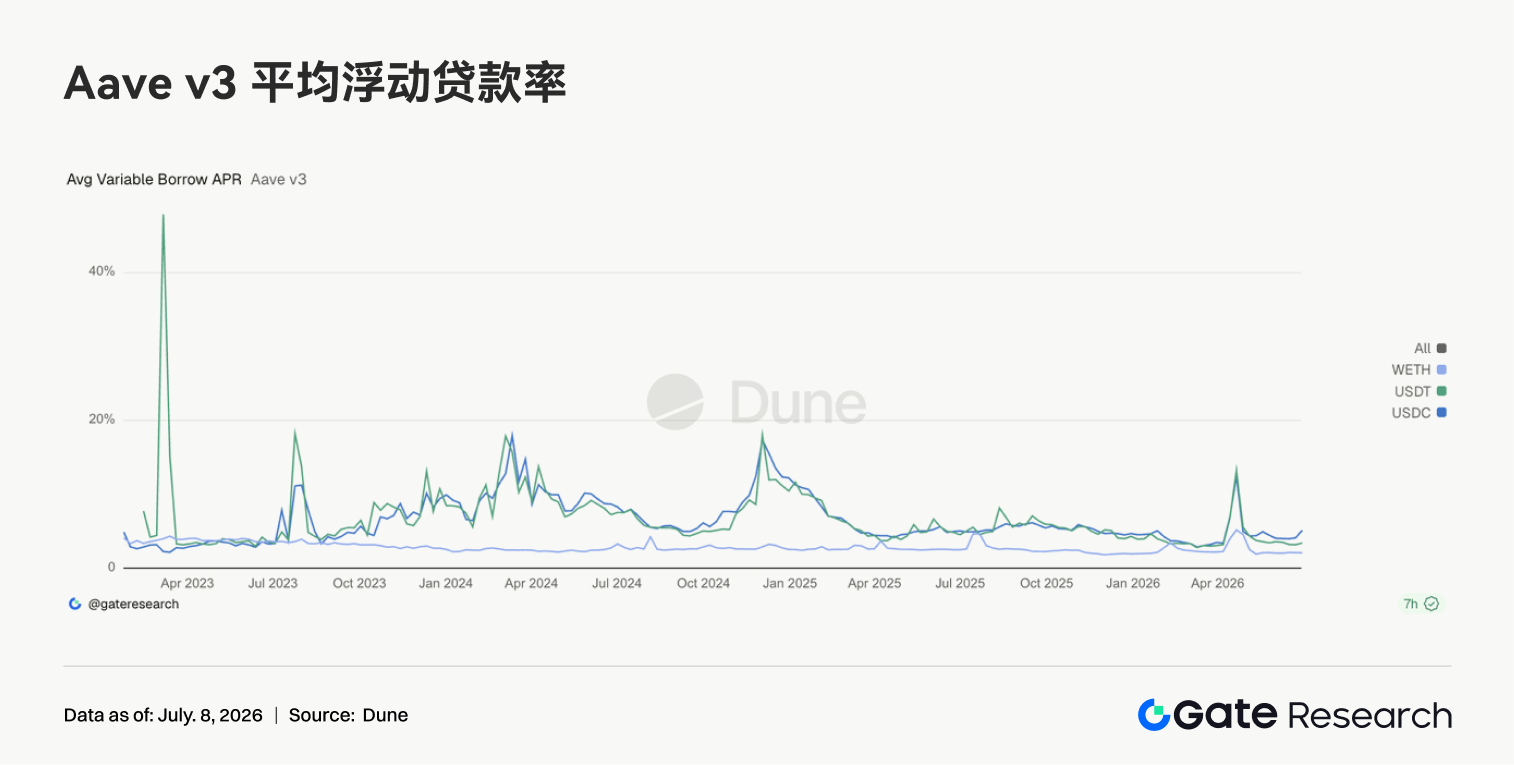

3.5 Aave Core Asset Borrow Rates Diverge Again; USDC Funding Pressure Clearly Rises

Interest rates for Aave's three core assets showed new divergence this week. The average borrowing cost for USDC rose significantly, USDT saw a slight increase, while WETH remained largely at low levels. USDC's highest rates still saw brief spikes during the week, indicating that the core USD pool remains sensitive to utilization rate changes. In contrast, WETH rates did not rise in tandem, suggesting no crowding in directional leverage on ETH. This combination typically corresponds to increased institutional demand for stablecoin turnover, arbitrage, and collateral management. Discussions within the Aave community about increasing the USDC liquidity buffer take on practical significance this week. The conclusion on the rates side is clear: market risk appetite has somewhat recovered, but the first thing to become more expensive is high-quality USD liquidity.

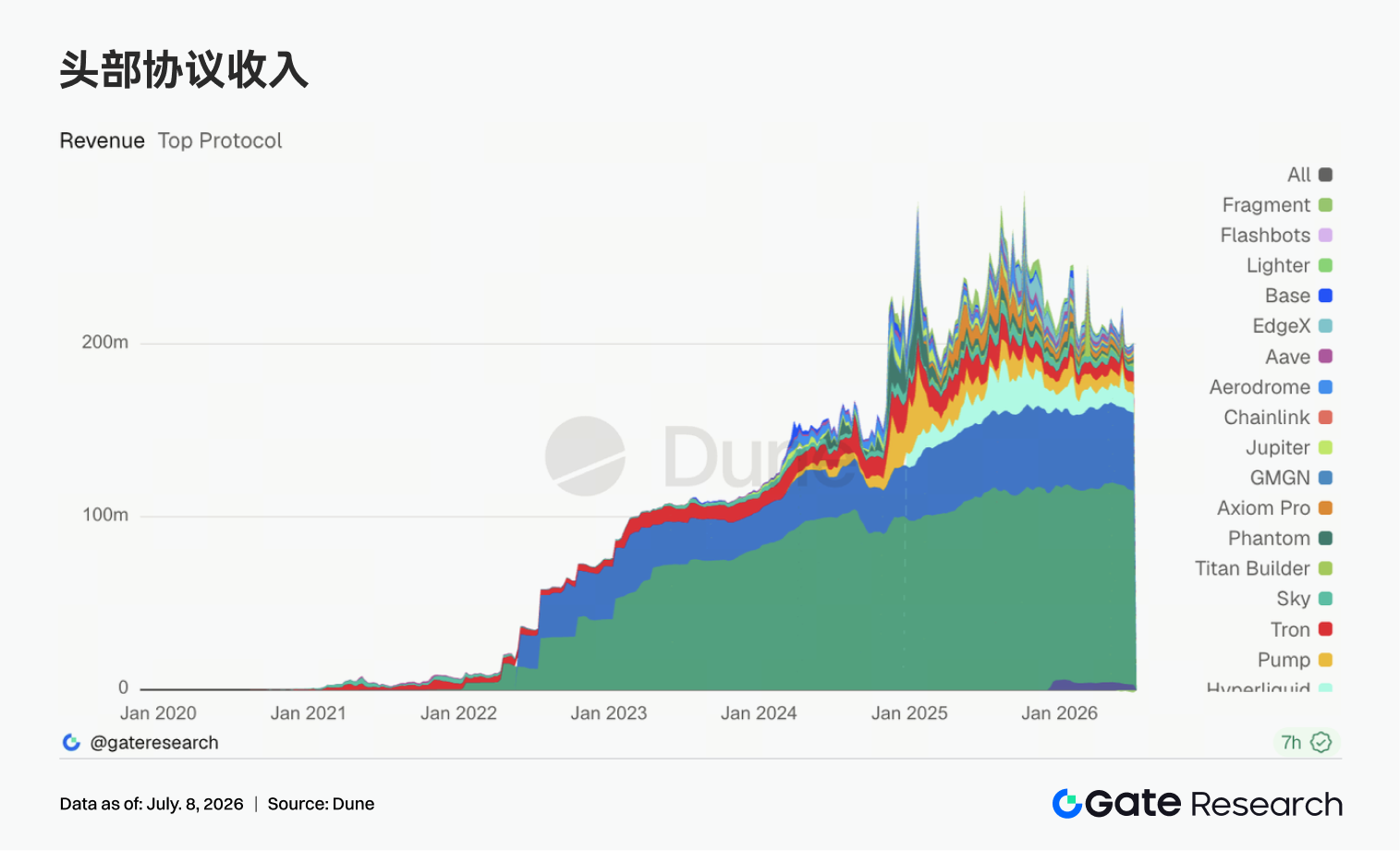

3.6 Protocol Revenue Shifts from High-Beta Derivatives to Solana Traffic Gateways; Pump Ecosystem Shows Strongest Performance

The structural change in protocol revenue was evident this week. Tether and Circle remain the most stable cash flow bases, but the growth elasticity came mainly from Solana traffic gateways like Pump.fun, PumpSwap, Axiom, and Phantom. Hyperliquid Perps revenue fell compared to the previous week, as the earlier enthusiasm for on-chain perpetuals and stock index/pre-IPO trading cooled somewhat, though it remains one of the highest-earning on-chain derivatives protocols. Titan Builder's revenue continued to improve, reflecting the strong cyclical elasticity of order flow and MEV-related infrastructure. Aave V3 revenue declined slightly, consistent with divergent lending rates and uneven recovery in overall balances. Viewed alongside DEX data, this week's revenue and trading activity point towards the same main narrative: mainstream spot platforms stabilize the base, while the real marginal elasticity comes from Solana issuance, wallets, and high-frequency trading front ends. Stablecoin issuers provide steady cash flow, while trading infrastructure and traffic gateways provide short-term elasticity.

4. Derivatives Tracking

4.1 BTC Price Recovers from Lows; OI Rebound Indicates Re-entry of Leveraged Capital

BTC price experienced a decline followed by a rise last week. The price oscillated around $60,000 at the beginning of the week, briefly dipped to near $59,000 around June 30, then gradually recovered, climbing back into the $63,000 to $64,000 range between July 3 and July 5. Overall, the price shifted from a weak downward trend in the previous week to a rebound