存储周期见顶?请收下这份美国银行的「基本面心理按摩」

- 核心觀點:美國銀行認為,近期全球存儲股的回調源於市場對 Meta 訂單、長鑫存儲進入蘋果供應鏈及韓國擴產等風險的過度解讀,並非基本面逆轉。行業仍處強週期,但行情將從普漲轉向盈利驗證和個股分化。

- 關鍵要素:

- 市場擔憂 Meta 出租算力削減存儲訂單,但美銀指出其 HBM、LPDDR5 及企業級 SSD 需求仍在增強,此舉更可能是資產變現。

- 美銀預計蘋果短期內大規模採用長鑫存儲 DRAM 機率較低,後者更可能作為蘋果與三星、海力士等廠商的議價籌碼。

- 韓國 800 兆韓元擴產計畫週期長達十餘年,短期難以形成有效供給,尚不能作為週期見頂的依據。

- 日本產業鏈調研顯示,第三、四季 DRAM 與 NAND 價格預計仍將季增,2027 年行業可能繼續短缺,廠商資本開支保持克制。

- 超大規模雲端廠商資本開支持續增長,DRAM 及 NAND 價格仍處高檔,AI 伺服器及資料中心高端存儲需求依然強勁。

Original Report: BofA Global Research《Global Memory Tech》, July 2, 2026

Compiled & Organized: DaiDai, MSX Maitong

Edited by: Frank, MSX Maitong

Key Takeaways:

- Bank of America believes the recent concentrated pullback in memory stocks is primarily driven by risk narratives such as Meta's orders, Changxin Memory Technologies entering Apple's supply chain, and South Korea's capacity expansion, rather than indicating a fundamental reversal in the industry.

- Meta's provision of data center or cloud services to external parties is more likely a strategy for computing power monetization and business diversification, rather than a significant reduction in memory demand. Its demand for HBM, LPDDR5, and enterprise SSDs continues to grow.

- In the short term, Changxin Memory Technologies is unlikely to become a major DRAM supplier for Apple. Apple is more likely to use it as leverage in price negotiations with Samsung, SK Hynix, and Micron.

- Supply chain research in Japan indicates that DRAM and NAND prices are expected to rise quarter-over-quarter in Q3 and Q4, with the industry potentially continuing to face shortages in 2027. Manufacturer capital expenditures and wafer output remain relatively restrained.

- The memory industry remains in a strong cycle, but with significant price increases in products and related stocks, future performance will depend more on earnings delivery, potentially leading to increased sector volatility and stock divergence.

Over the past week, global memory stocks have experienced a notable correction.

The market quickly found three seemingly plausible explanations for this decline: Meta's plan to sell some computing power externally might indicate an oversupply from previous data center builds; Apple is evaluating Changxin Memory Technologies' DRAM, potentially disrupting the supply landscape dominated by Samsung Electronics, SK Hynix, and Micron; and South Korea announced another massive semiconductor cluster plan, further fueling concerns about future supply gluts.

All three narratives point to the same conclusion: Demand may be peaking, supply is poised to expand, and the memory super cycle might be nearing its end.

However, Bank of America's latest "Global Memory Tech" report suggests the opposite.

In its view, the aforementioned risks are not entirely nonexistent, but the market has significantly overestimated their impact on the short-term supply-demand dynamics. Whether looking at cloud provider capital expenditures, South Korean semiconductor exports, or spot and contract prices for DRAM and NAND, none have yet indicated a directional reversal of the memory cycle.

What has truly changed is not that fundamentals have turned from strong to weak, but that after substantial price increases and stock revaluation, the industry has entered a new phase where fundamentals remain strong, yet the difficulty of trading has significantly increased.

I. Assessing Market Concerns One by One

1. Meta Selling Computing Power ≠ Cutting Memory Orders

The market's concern about Meta stems from a seemingly logical inference: If Meta starts opening its data centers or selling cloud services to external customers, does it mean the company previously purchased too many servers, and its internal business can no longer absorb the existing computing power?

If the answer is yes, demand for AI hardware like GPUs, HBM, server DRAM, and enterprise SSDs could subsequently decline.

However, the Bank of America report states that based on supply chain feedback, memory chip manufacturers believe Meta will continue to more aggressively adopt high-performance memory products like HBM, LPDDR5, and enterprise SSDs in its AI data centers. Therefore, market speculation about "Meta renting out previously over-invested AI servers or cloud infrastructure" lacks sufficient basis.

Furthermore, some NAND controller chip and packaging substrate material manufacturers have indicated that Meta's chip and component orders are actually strengthening. Thus, Meta opening its data centers to external customers is more likely an attempt at asset monetization and business diversification, rather than being forced to handle a severe surplus of computing power.

2. Changxin Memory Technologies Entering Apple's Supply Chain: More Likely a Bargaining Chip

The Bank of America report anticipates a low probability of Apple adopting Changxin Memory Technologies' DRAM on a large scale in the short term.

There are three main constraints:

- Policy and Supply Chain Restrictions: Apple must consider U.S. restrictions on China's semiconductor industry and the associated compliance and supply chain risks.

- Technical Specifications: Apple has high requirements for mobile DRAM regarding transmission speed, power consumption, and reliability, including speeds above 10Gbps, low power consumption around 1.1V, and ECC error correction capabilities. Whether Changxin Memory Technologies can consistently and massively meet these demands requires further validation.

- Intellectual Property Risks: Core DRAM patents have long been concentrated in the hands of top manufacturers like Samsung, SK Hynix, and Micron. If Apple adopts products with insufficient patent coverage on a large scale, it could face potential lawsuits and supply disruption risks.

Theoretically, Changxin Memory Technologies could vie for orders for the low-end iPhone 18e, but given the scale of related models in the Chinese market, the actual procurement volume is expected to be limited.

Rather than truly restructuring its supply chain, Apple is more likely using this opportunity to enhance its bargaining power in contract price negotiations for the second half of 2026 or 2027. Therefore, this event is more likely to impact the pricing expectations of Samsung, SK Hynix, and Micron in the short term, rather than immediately altering the global DRAM supply-demand landscape.

3. South Korea's Massive Capacity Expansion ≠ Short-Term Supply Out of Control

Another recent concern stems from South Korea's new semiconductor industry cluster plan.

Some investors believe the South Korean government's plan to invest approximately 800 trillion won in a new memory fab cluster in the southwestern region might signal the memory cycle is nearing its peak. However, the Bank of America report dismisses this view, expecting the project to be unlikely to generate significant effective supply before the early 2030s. Moreover, the priority for now remains the expansion of the Yongin and Pyeongtaek clusters from 2026 to 2035.

Therefore, an industrial plan spanning over a decade cannot be directly equated to supply running out of control in the next two to three years. Long-term expansion warrants continuous monitoring, but it is not yet sufficient evidence to conclude the current memory cycle has peaked.

4. Supply Chain Research in Japan Remains Relatively Optimistic

Bank of America's recent supply chain research in Japan further reinforces a positive outlook for the memory industry.

Japanese investors generally acknowledge the current industry prosperity, but with rapid stock price increases alongside product prices, the market is starting to pay more attention to potential downside cycles. Compared to cautious investors, management along the supply chain offers a still-positive outlook:

- Q2 memory ASP performance was strong, especially for NAND.

- ASP in Q3 and Q4 is expected to be higher than in Q2.

- DRAM and NAND may continue to be in short supply in 2027.

- The number of long-term supply agreements is increasing, but most remain primarily based on volume commitments.

- Capital expenditure and wafer output remain restrained, especially for Japanese NAND manufacturers.

This suggests that although the market has begun discussing the next supply cycle prematurely, the industry has not yet entered a phase of obvious supply loss of control, based on actual manufacturer expansions and customer procurement behavior.

5. Samsung's Memory Business Could Still Surprise on the Upside

In a report published on July 2, Bank of America estimated that due to special bonus expenses and margin pressure in its smartphone business, Samsung Electronics' overall Q2 operating profit might slightly miss overly optimistic market expectations. However, thanks to strong ASPs for DRAM and NAND, the operating profit specifically for the memory business was still expected to exceed market consensus.

Five days after the report, Samsung released its Q2 preliminary earnings on July 7: consolidated sales of approximately 171 trillion won and operating profit of about 89.4 trillion won, representing year-over-year growth of 129.3% and 1810.3% respectively. The operating profit was higher than the market's earlier expectation of around 86 trillion won, meaning BoA's judgment that consolidated profit might slightly miss optimistic expectations ultimately did not materialize.

However, Samsung's disclosure remains at the group-level preliminary stage, without detailed profit figures for its memory, foundry, and mobile businesses. Whether the memory division individually exceeded expectations requires confirmation from the full financial report. Considering the rise in DRAM and NAND prices in Q2 and the significant increase in South Korean semiconductor exports, the memory business was highly likely the core driver of Samsung's profit surge this cycle.

II. What Signals are Exports, ASPs, and Product Prices Sending?

1. Significant Growth in South Korean Semiconductor Exports

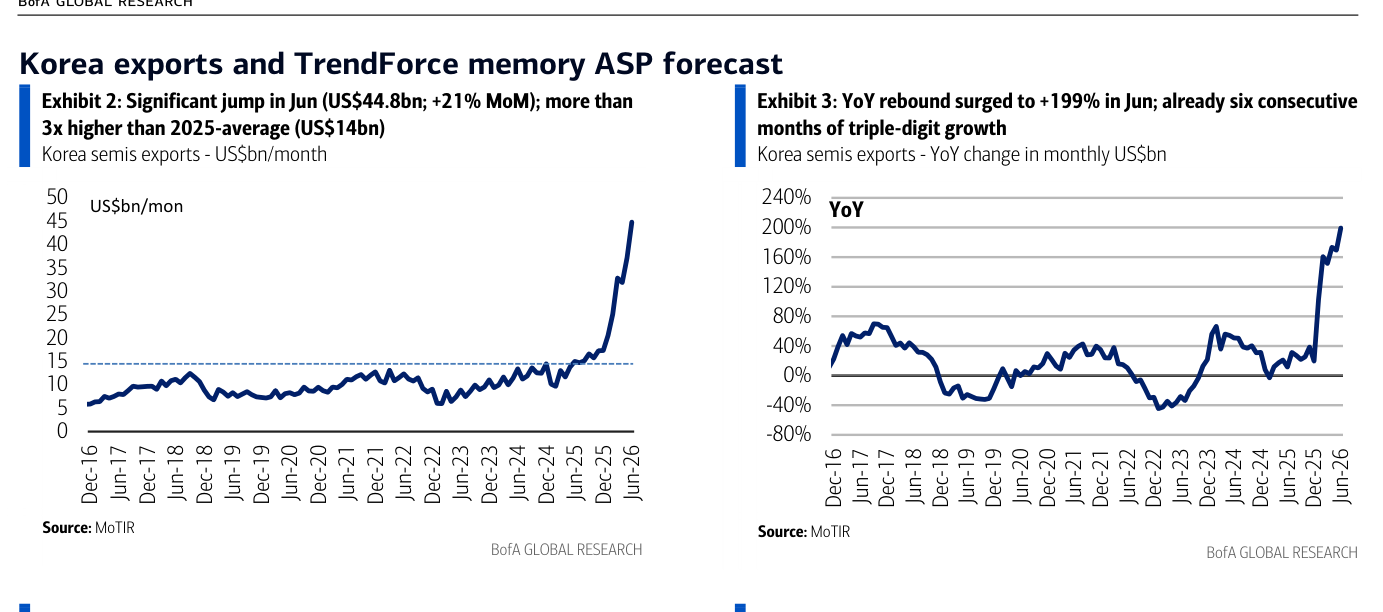

In June 2026, South Korea's semiconductor exports reached $44.8 billion, a 21% month-over-month increase and a 199% year-over-year increase, marking six consecutive months of triple-digit year-over-year growth.

This figure is roughly three times the average monthly export value of about $14 billion in 2025, indicating that current memory price increases are clearly flowing through to export revenue and corporate earnings.

Of course, rising export values don't entirely represent equivalent growth in shipment volumes; a significant portion of the increase comes from rapidly rising average selling prices. However, this precisely illustrates that the core contradiction in the current supply chain remains price increases and tight supply, not inventory buildup or significantly shrinking demand.

South Korea Semiconductor Export Value and YoY Growth: Notable surge in June 2026 (Original Report Page 2)

2. DRAM Remains the Strongest Memory Category

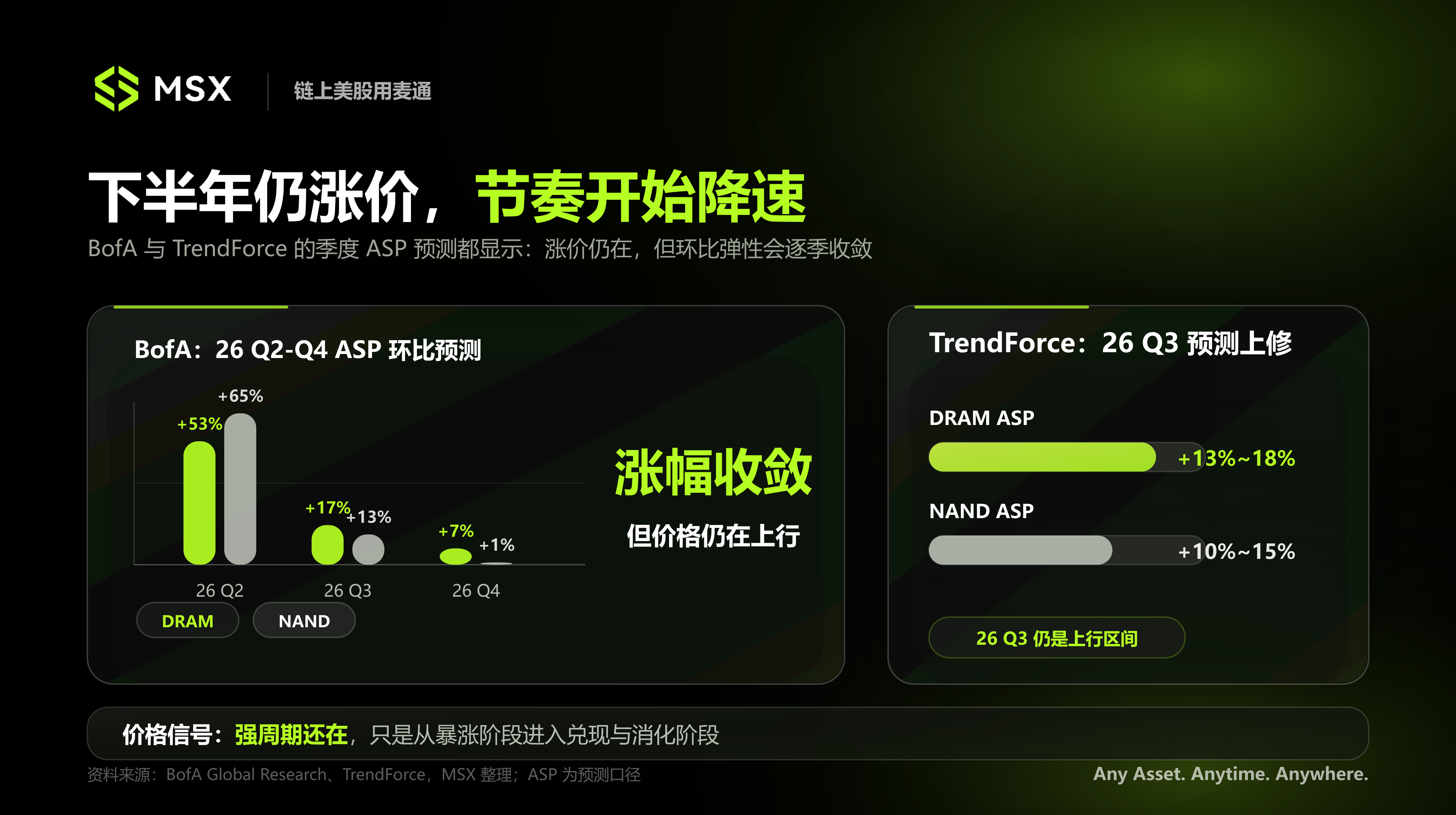

TrendForce has revised its Q3 2026 DRAM ASP forecast from a 3%-8% quarter-over-quarter increase to a 13%-18% increase. Bank of America estimates DRAM ASPs will rise 53%, 17%, and 7% quarter-over-quarter in Q2, Q3, and Q4 2026, respectively.

The specific methodologies of the two forecasts differ, but both point to the same trend: DRAM prices will continue to rise in the second half of the year, although the quarter-over-quarter growth rate may slow sequentially as the price base increases.

As of early July 2026, the spot price for 16Gb DDR5 is approximately $47, and for 16Gb DDR4, it's about $75, both significantly higher than the peaks of the previous memory cycle. The core reason is not just end-customer inventory replenishment, but memory manufacturers continuously shifting wafer capacity towards higher-margin HBM and server DRAM.

After advanced capacity is absorbed by AI-related products, the supply available for traditional DDR4 and conventional DDR5 decreases simultaneously.

DDR4, in particular, is experiencing a structural shortage as top manufacturers gradually phase out mature products. Contract prices for both 16Gb DDR4 and DDR5 have risen to the $35-$40 range, effectively eliminating the long-standing technical premium of DDR5 over DDR4.

This doesn't mean the market prefers the older generation DDR4, but rather that the speed of manufacturer phase-outs is exceeding the speed of customer product transitions, making mature products scarcer.

3. NAND Price Increases Slow, but Absolute Prices Remain High

Compared to DRAM, the marginal change in NAND prices is more pronounced.

After hitting a cyclical high in March 2026, the spot price of 512Gb NAND wafers stabilized or edged lower from April to June, but is still up over 50% year-to-date and roughly eight times the low point in February 2025.

The NAND contract price is around $25, about ten times the low of $2.5 in February 2025. After experiencing substantial increases in Q4 2025 and Q1 2026, the monthly growth rate of NAND contract prices from April to June has moderated to around 1%-5%.

This does not signal a reversal in NAND prices, but rather indicates that customer tolerance for high prices is gradually approaching its limit, and the pace of price increases is normalizing.

Changes in client SSD prices are particularly intuitive. As of June 2026, the price of a 512GB client SSD has risen from $73.1 at the end of 2025 to $137.5, nearly doubling, reflecting the ongoing pass-through of upstream NAND price increases to end products.

Therefore, a more accurate description of NAND's current state is that absolute prices remain very high, but the quarter-over-quarter growth rate is decelerating.

4. Server Memory Continues to Hit New Highs

Server memory also continues its strong performance.

The price of 64GB server DRAM modules has hit an all-time high, with DDR5 around $1,400 and DDR4 around $1,100. In June 2026, DDR5 server DRAM contract prices rose again, while DDR4 prices remained largely flat.

This suggests that even as price increases for some consumer-grade memory products begin to slow, demand for high-end memory related to AI servers and data centers remains robust.

III. Cloud CapEx Remains the Demand Anchor, but the Investment Narrative is Changing

1. Hyperscale Cloud Providers Continue to Expand

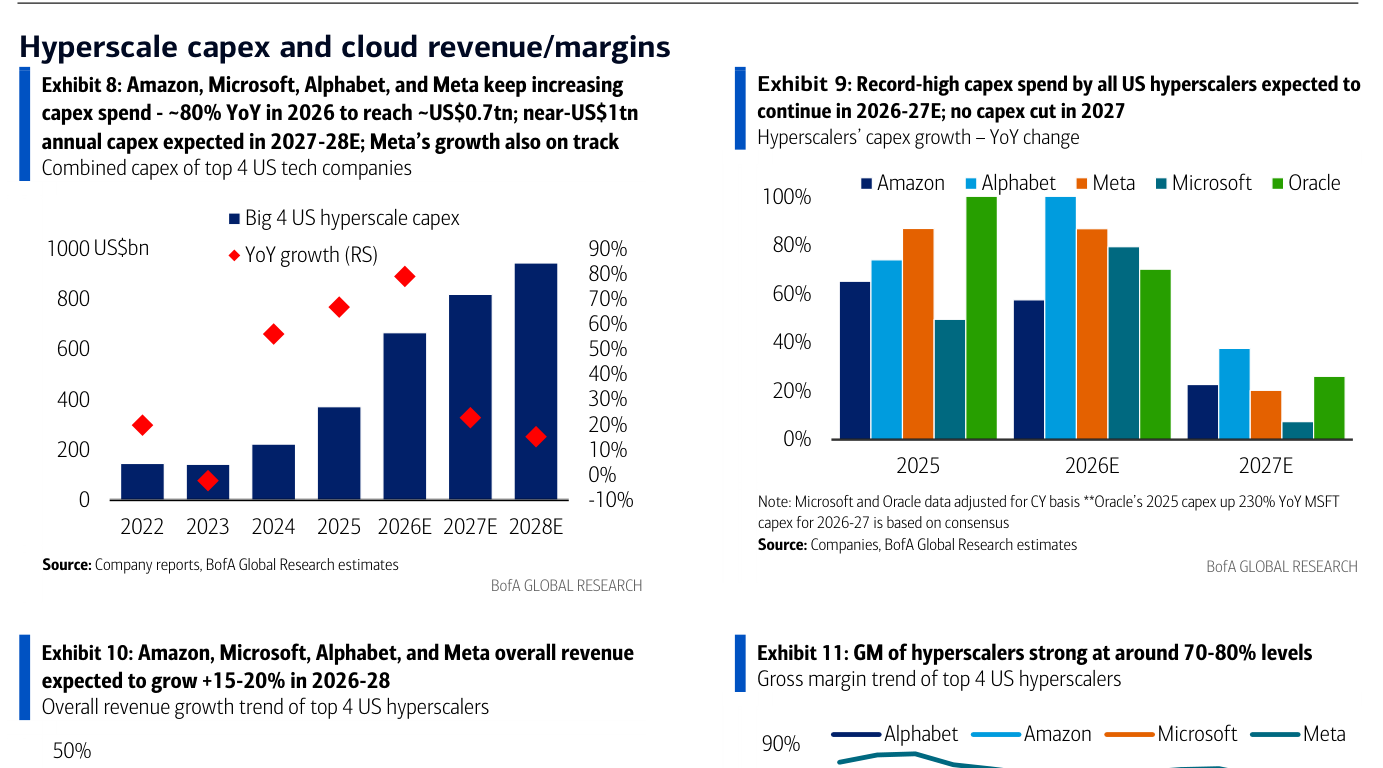

Hyperscale cloud providers like Amazon, Microsoft, Alphabet, and Meta are becoming the most important sources of new memory demand. The report estimates that the combined CapEx of these four companies will be approximately $700 billion in 2026, a year-over-year increase of about 80%. By 2027-2028, annual CapEx could approach $1 trillion.

Furthermore, Bank of America sees no signs of major cloud providers significantly cutting CapEx in 2027, implying that these investments will ultimately translate into more AI accelerators and HBM, more server DRAM, more enterprise SSDs, and more data center and AI inference infrastructure.

CapEx, Revenue, and Gross Margin Trends for Major US Hyperscale Cloud Providers (Original Report Page 3)

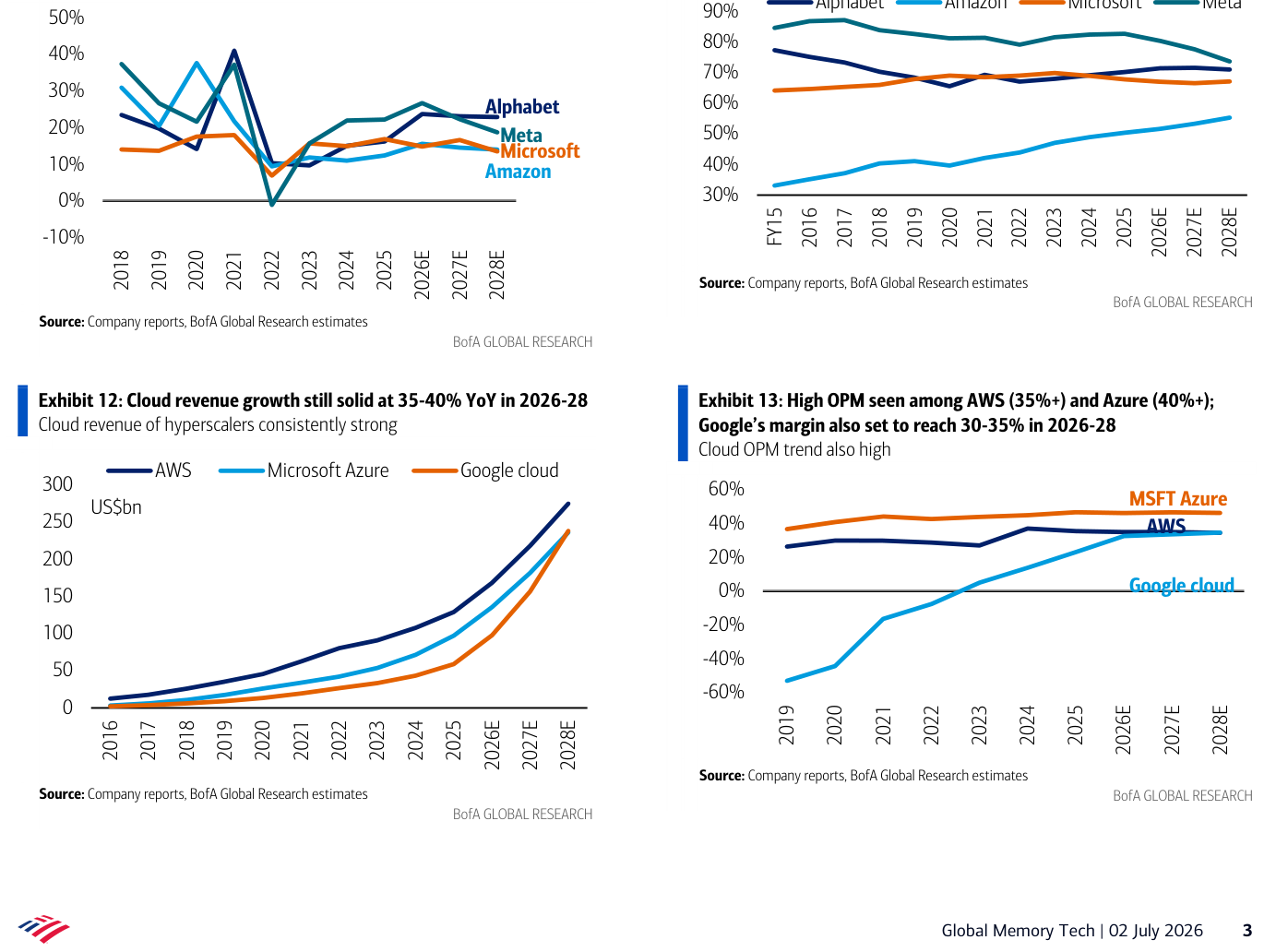

The report projects that from 2026 to 2028, the overall revenue of these four tech giants could grow by 15%-20%, with cloud revenue year-over-year growth potentially reaching 35%-40%.

Among them, AWS operating margin is expected to remain above 35%, Azure may exceed 40%, and Google Cloud could reach 30%-35%.

As long as cloud businesses maintain high revenue growth and margins, tech giants will continue to have the commercial incentive to expand AI infrastructure investment.

Cloud Revenue and Cloud Business Operating Margin Trends (Original Report Page 3)

2. This Cycle is No Longer Just About Consumer Electronics Inventory Replenishment

The biggest difference between this memory cycle and past ones is that demand is no longer primarily dependent on smartphone and PC inventory replenishment.

Past memory cycles were often mainly driven by inventory changes in PCs and smartphones, creating classic cyclical characteristics: rising end demand, customer inventory replenishment, rising memory prices; then manufacturer capacity expansion, gradual inventory buildup, and prices entering a downward cycle.

However, the structure of this memory cycle is more complex. Current demand has already expanded beyond simple consumer electronics inventory restocking to encompass:

- HBM

- Server DRAM

- Enterprise SSDs

- AI Inference Infrastructure

- Hyperscale Cloud Capital Expenditures

- Structural Shortage from DDR4 Capacity Phase-outs

This means that observing only PC and smartphone sales is no longer sufficient to judge the entire memory cycle. Even if some consumer electronics demand weakens due to high prices, AI servers and data centers can continue to absorb high-end capacity, keeping overall supply relatively tight.

But it also means that divergence within the sector will become increasingly apparent. In short, companies focused on HBM, server DRAM, enterprise SSDs, and advanced packaging may continue to benefit from stronger orders and margins. Conversely, manufacturers heavily reliant on client, mobile, and consumer-grade