SK海力士白天漲,美股晚上跟:全球 AI 行情的新「亞洲盤風向標」?

- 核心观点:SK海力士作为亚盘交易时段的AI存储龙头,其股价波动已成为美股科技板块(尤其是费城半导体指数)的领先指标,这源于其在HBM、DRAM、NAND及企业级SSD领域的全产业链核心地位,而其赴美上市将有望推动其估值从“韩国周期股”向“全球AI基础设施资产”转变。

- 关键要素:

- 数据验证:海力士单日上涨超1%时,费城半导体指数当晚上涨的命中率达77.1%,且相关性主要集中在美股开盘跳空阶段,显示其信号对美股开盘价有直接且显著的影响。

- 产业地位:海力士在全球HBM市场份额约58%,是英伟达核心供应商,同时通过收购英特尔NAND业务,构建了贯穿HBM、DRAM、NAND和企业级SSD的完整AI存储链条。

- 赴美上市:海力士计划于2025年7月在纳斯达克上市,拟募资约294亿美元,这将成为全球史上最大股票发行之一,旨在解决“韩国折价”问题,降低国际投资者配置门槛。

- 估值重塑:在美股市场,海力士将被直接与美光等公司比较,并可能被重新定位为“全球AI基础设施资产”,而非传统的存储周期股,有望获得更高估值倍数。

- 长期挑战:海力士需在下一代HBM(HBM4)中保持技术领先,证明HBM高利润率的可持续性,并成功将Solidigm打造为第二增长曲线,以支撑其新叙事。

In the past month, observing the South Korean stock market alongside the U.S. stock market reveals a rather interesting phenomenon.

SK Hynix during Asian trading hours increasingly resembles an early preview for the AI sector in the U.S. markets that evening: If it surges during the day, Nvidia, Micron, and the Philadelphia Semiconductor Index often gap up that night; if it pulls back first, U.S. tech stocks are likely to cool down as well.

This correlation has become particularly evident, especially against the backdrop of recent sharp volatility in global tech stocks.

The latest example occurred this morning after the U.S. market close. Micron (MU) released stellar earnings and guidance that significantly exceeded expectations. When the Korean market opened, SK Hynix quickly absorbed this memory sentiment, rising over 10% during the trading session.

Of course, simply summarizing this phenomenon as "if Hynix rises, U.S. stocks rise" is not precise. After all, a single trillion-dollar company is unlikely to determine the direction of a multi-trillion-dollar U.S. capital market.

However, as global capital trades around the same set of AI expectations, an increasingly clear cross-market pricing chain has formed. SK Hynix has become the most sensitive "thermometer" within this chain.

This raises a more pertinent question: Why SK Hynix? How did it become the "Asian session bellwether" for global AI trading? And as SK Hynix formally advances its U.S. listing, how will Wall Street reprice it?

1. Hynix by Day, U.S. Stocks by Night: Superstition or Signal?

From a trading time perspective, the South Korean market, being in the Asian session, naturally sits between the previous U.S. market close and the next U.S. market open.

This means that when the Korean market opens, investors have already absorbed the performance of the U.S. market from the previous night and will simultaneously trade on new earnings reports and macroeconomic changes that emerged after the U.S. close.

By the time the Korean market closes, U.S. investors will use the performance of Asian semiconductor companies, along with U.S. pre-market trading and stock index futures, as a reference for the day's risk appetite.

Therefore, in theory, a relay pricing chain spanning two trading time zones exists between SK Hynix and U.S. stocks: The U.S. market first provides the underlying sentiment overnight. Hynix confirms or revises it during the Asian session. The U.S. market then absorbs the incremental information released by the Asian market when it opens next.

To verify this intuition, MSX conducted backtesting using common trading days for the Korean and U.S. markets, examining the co-direction rate, correlation, and conditional hit rate between SK Hynix and major U.S. indices.

First, looking at the direction of gains and losses over the past month, the co-direction rate between SK Hynix and the Philadelphia Semiconductor Index (SOX) reached 70%. That is, on 14 out of 20 common trading days, they moved in the same direction.

In comparison, Hynix's co-direction rate with the Nasdaq Composite Index was 65%, with the QQQ Trust (QQQ) at 60%, and with the S&P 500 ETF (SPY) at 55%.

This result first indicates that SK Hynix is not a broad-based signal equally effective for all U.S. stock assets. It shows a clear industrial gradient: the strongest linkage is with the Philadelphia Semiconductor Index, followed by the more tech-heavy Nasdaq and QQQ, and finally, it spreads to the S&P 500, representing the broader U.S. market.

This aligns closely with SK Hynix's industrial attributes.

Capital first trades memory and semiconductor cyclicality through Hynix. This risk appetite then transmits to the entire AI tech sector. Only when the momentum is strong enough and the impact broad enough does it further diffuse into the broader U.S. market.

In other words, SK Hynix acts more like a semiconductor sentiment outpost than a macro-level predictor for the U.S. stock market.

Examining daily return correlations over the past three months reveals this industrial gradient. The correlation coefficient between SK Hynix and the SOX was 0.363, with QQQ at 0.344, and with the Nasdaq Composite Index at 0.313.

It's important to note that these numbers do not mean a 1% rise in Hynix mechanically leads to a 0.363% rise in the SOX. Instead, they measure the degree to which the two return series move in the same direction over the sample period – a value closer to 1 indicates a stronger tendency to rise or fall together; a value closer to 0 indicates a weaker linear relationship.

Realistically, 0.3 to 0.4 represents only a moderate positive correlation. However, considering daily financial markets contain significant noise, this is already a high and highly valuable signal.

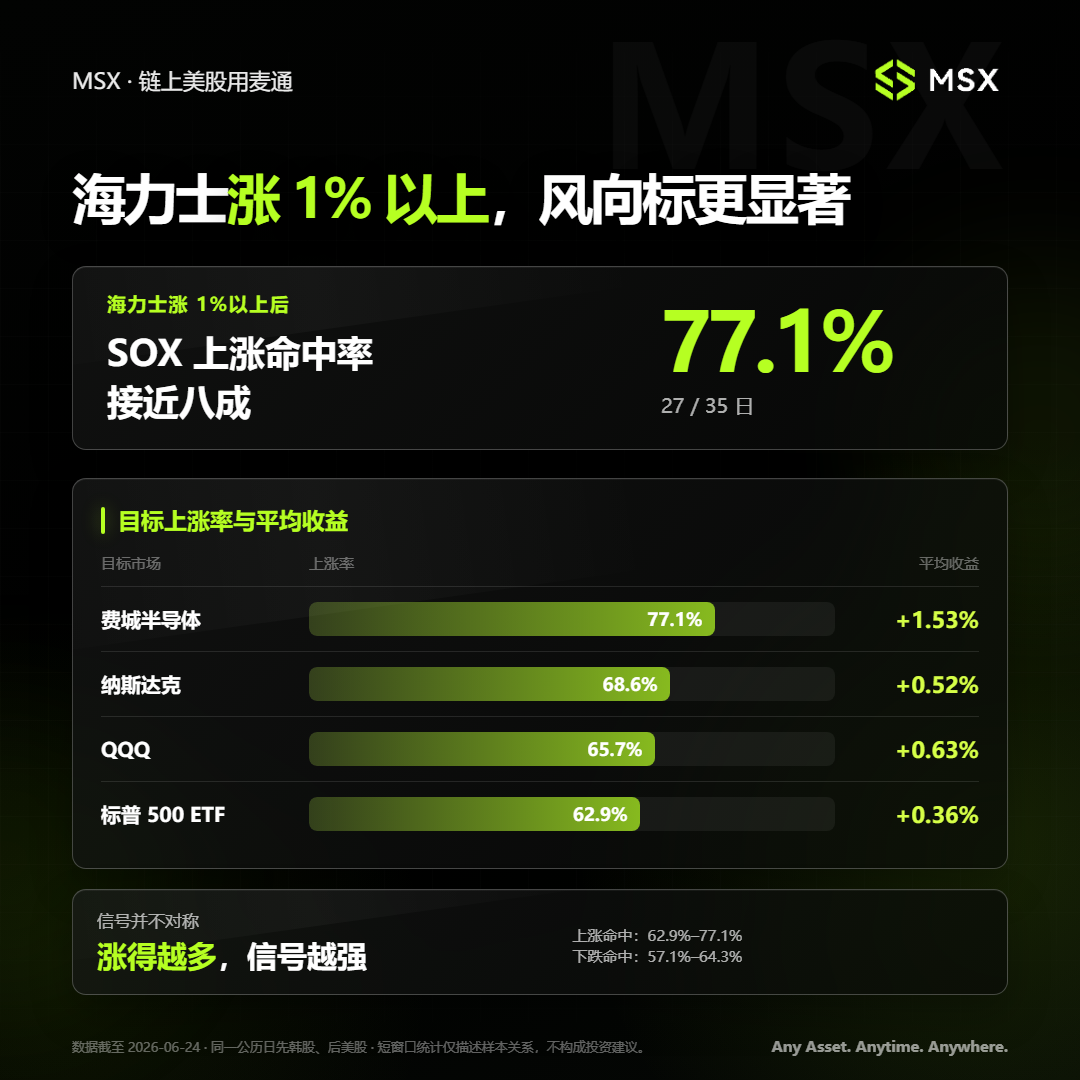

Consequently, after further data cleaning and filtering, MSX identified a pronounced "strong volatility trigger" feature: When SK Hynix rose more than 1% in a single day, the Philadelphia Semiconductor Index's hit rate for rising that evening reached 77.1%. In 27 out of 35 qualifying samples, the index recorded a gain, with an average return of 1.53%.

Under the same conditions:

- The Nasdaq Composite Index's hit rate for rising was 68.6%, with an average return of 0.52%;

- QQQ's hit rate was 65.7%, average return 0.63%;

- The S&P 500 ETF's hit rate was 62.9%, average return 0.36%;

These results are undoubtedly more explanatory than simple co-direction rates of gains and losses.

When Hynix experiences only minor fluctuations, its movement may be mixed with significant noise like domestic Korean capital flows, currency effects, and index weight adjustments. However, a single-day rise exceeding 1% often implies the market is pricing in a more specific and clear industry signal.

Interestingly, this signal is not entirely symmetrical. In the current sample, after a significant rise in Hynix, the hit rate for U.S. major indices rising falls between 62.9% and 77.1%. Conversely, when Hynix falls significantly, the corresponding hit rate for U.S. stocks falling is only about 57.1% to 64.3%.

This suggests that, within the current sample period, Hynix's upward signals are temporarily more stable than its downward signals.

This might be related to the sample period coinciding with an upswing phase in the AI memory cycle. In a market where capital tends to seek bullish AI opportunities, a strong rally in Hynix is more easily interpreted as a confirmation of industrial demand, similar to the direct catalyst provided by Micron's earnings today.

A decline in Hynix, however, could stem from short-term profit-taking, technical adjustments in the Korean market, or stock-specific capital flows, and may not necessarily mean a simultaneous deterioration in the global AI fundamentals.

A third set of data further reveals the specific timing when the SK Hynix signal exerts its influence.

If we decompose the daily return of U.S. stocks into two parts:

- Opening Gap: The change from the previous day's closing price to the current day's opening price;

- Intraday Return after Open: The change from the opening price to the closing price;

We find that the correlation between Hynix and U.S. stocks is almost entirely concentrated in the opening gap phase.

Specifically, the correlation coefficient between Hynix's daily return and the Philadelphia Semiconductor Index's opening gap was 0.497, with QQQ at 0.483, the Nasdaq Composite at 0.435, and the S&P 500 ETF at 0.405.

Again, as previously discussed, a correlation coefficient close to 0.5, amidst noisy daily cross-market returns, implies that the stronger Hynix performs during the day, the more likely the SOX and QQQ are to open higher that night; the weaker Hynix performs, the more likely U.S. semiconductor and tech stocks are to open lower.

However, once the U.S. market truly opens, this correlation almost immediately disappears. The correlation between Hynix's daily return and the SOX's intraday return was only 0.051, with QQQ at 0.055, the Nasdaq Composite at 0.054, and the S&P 500 ETF at 0.081 – essentially close to zero.

The stark contrast between these two phases indicates that the information conveyed by SK Hynix during the Asian session is primarily absorbed by the U.S. market into the opening price in one go. Once U.S. trading begins, local U.S. data, news, and intraday liquidity take over pricing, and Hynix's explanatory power rapidly diminishes.

Synthesizing the three sets of data, a relatively complete transmission chain emerges:

SK Hynix first confirms memory and semiconductor sentiment. The SOX most directly absorbs this signal at the U.S. market open. The influence then spreads to QQQ and the Nasdaq, and only finally potentially transmits to the S&P 500. Here, the SOX helps verify the signal's industry-specific nature; QQQ and the Nasdaq allow observation of whether it has diffused to the broader U.S. AI theme; and the S&P 500 serves as a broad market reference.

From this perspective, the linkage between SK Hynix and the U.S. AI sector doesn't imply that the former unilaterally "drives" the latter. Rather, it suggests two markets continuously pricing the same set of industrial variables at different times.

SK Hynix gains a temporal advantage by opening first. Furthermore, being at the core of the AI memory supply chain gives it a higher information density compared to typical Asian tech stocks.

This leads to a more crucial question: Why is SK Hynix uniquely positioned to play this role?

2. Why SK Hynix Specifically?

The fundamental reason SK Hynix has achieved this market status isn't just that the Korean market opens earlier; it's that it has effectively become a "critical few" that the AI infrastructure cannot easily bypass.

As is well known, market discussions about AI over the past few years primarily focused on GPUs.

Nvidia provides the computing power. Cloud providers build data centers. Electricity, networking, optical communications, and liquid cooling ensure the computing clusters operate stably. In this narrative, memory, while equally important, has long been viewed as a relatively traditional cyclical component.

But as model sizes, training data, and inference demands continue to grow, the challenge for AI systems is no longer just "having enough GPUs." This has redefined the role of memory in AI:

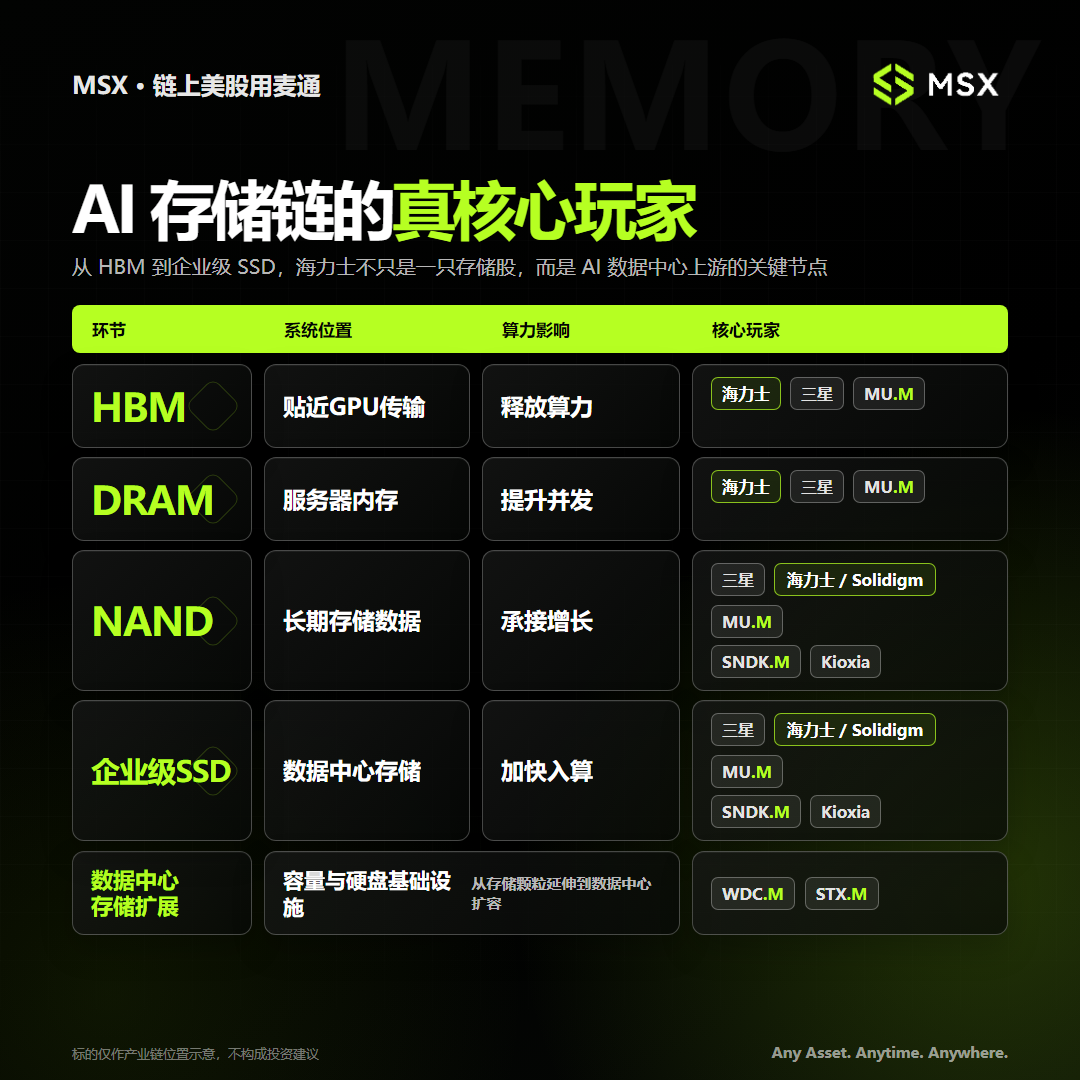

- HBM sits right next to the GPU, responsible for high-speed data transfer, determining whether expensive AI chips can fully unleash their compute power.

- Server DRAM acts as the system's operating memory, impacting the server's concurrency capabilities and task throughput.

- NAND handles long-term storage of models, training data, and inference data, absorbing the overall growth in data volume driven by AI.

- Enterprise SSDs reside in the data center storage layer, accelerating data flow into computing systems through higher capacity and faster read speeds.

To put it more bluntly: GPUs determine "if you can compute." HBM determines "if the compute power can be fully utilized." DRAM determines "how many tasks can be processed simultaneously." NAND and enterprise SSDs determine "where massive amounts of data are stored and how quickly they can be accessed."

And SK Hynix spans almost every layer of this AI memory chain, achieving a "grand slam."

In the HBM space, SK Hynix remains one of the world's most critical suppliers. As of the first quarter of 2026, Hynix held approximately a 58% share of the global HBM market, with Samsung and Micron each holding around 21%. It is also one of the most important HBM suppliers for Nvidia's AI accelerators.

The key difference between HBM and traditional standardized memory is that it is difficult for customers to easily substitute.

At the same time, SK Hynix is not solely an HBM company. As early as 2020, it announced the acquisition of Intel's NAND and SSD business for approximately $9 billion. The first phase was completed in 2021, establishing Solidigm focused on enterprise SSDs and data center storage in the U.S. In March 2025, the second phase was completed with the official transfer of Intel's remaining NAND technology, intellectual property, and related personnel, finalizing the multi-year acquisition.

This deal not only filled a critical gap in Hynix's enterprise storage capabilities but also gave it two interconnected yet distinct growth curves:

- One revolves around HBM and server DRAM, participating in the expansion of AI accelerators and servers.

- The other revolves around NAND and enterprise SSDs, catering to demands for training data, model weights, inference caching, and data center storage.

In essence, the current SK Hynix is like a high-purity AI memory asset. Its profits, capital expenditures, and market expectations are tightly bound to the memory cycle.

This business concentration undoubtedly maximizes its stock price elasticity. Consequently, the three conditions for Hynix becoming the Asian session bellwether form a closed loop here:

- First, it opens first temporally, allowing it to digest Asian session information before U.S. markets.

- Second, it is sufficiently core industrially, spanning almost the entire four-layer memory chain of HBM, DRAM, NAND, and enterprise SSDs.

- Third, its business purity and stock price elasticity are high enough to quickly amplify global capital's assessment of the AI memory cycle.

Therefore, when SK Hynix experiences significant volatility, the market is not just trading the rise or fall of one Korean company. It is trading the likelihood of continued volume growth in AI servers, whether memory supply remains tight, and whether global capital is willing to continue paying higher valuations for AI hardware.

However, the problem is that SK Hynix's historical capital market identity, primarily confined to the Korean market, has not fully kept pace with its evolving global industrial status.

The recently pursued U.S. listing aims to change this.

3. A U.S. Listing Changes More Than Just the Trading Venue

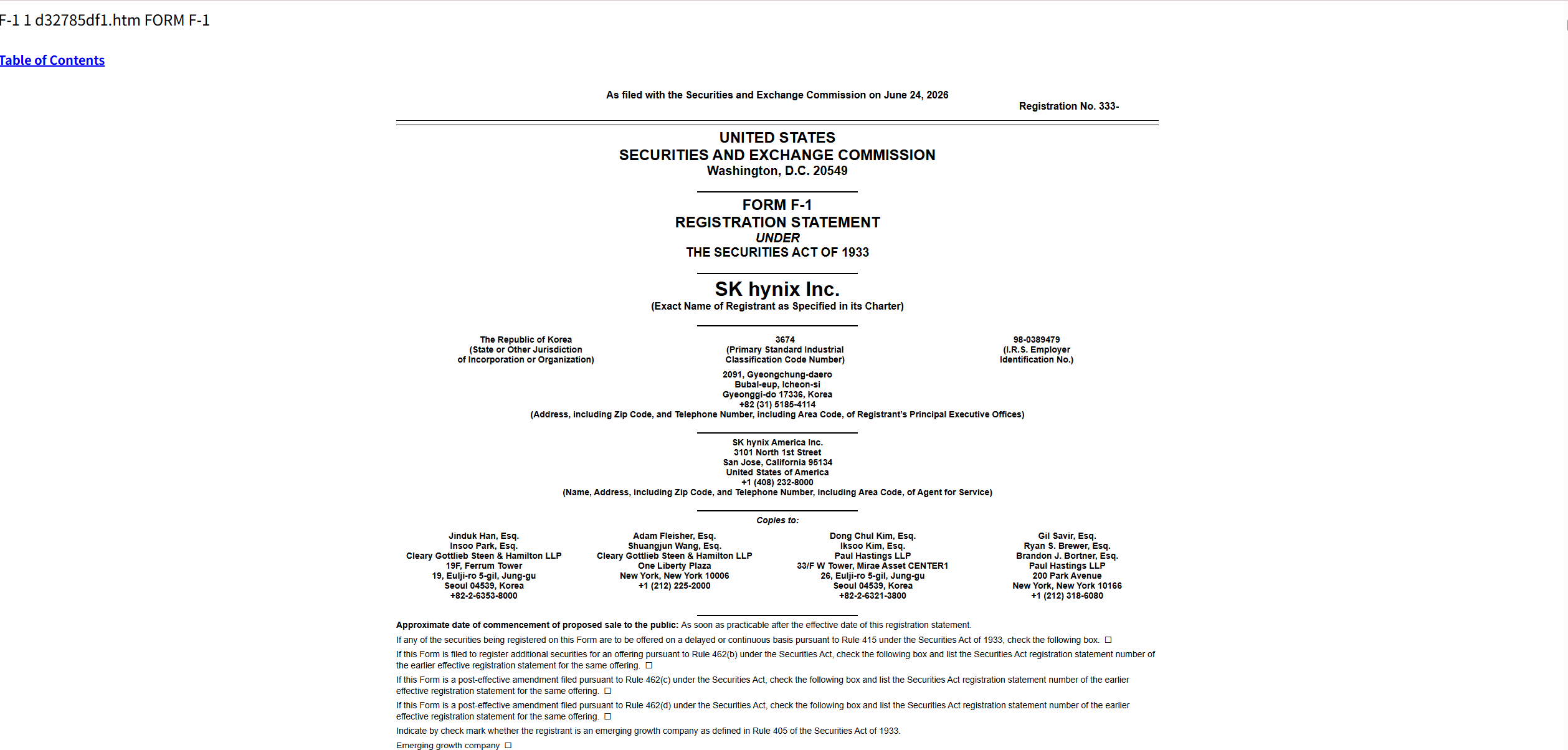

Coincidentally, on June 24th, SK Hynix publicly filed its F-1 registration statement with the U.S. Securities and Exchange Commission (SEC), formally advancing its Nasdaq ADR listing under the proposed ticker symbol "SKHY."

According to the disclosed plan, Hynix intends to issue up to 17.79 million new ordinary shares, with a potential maximum fundraising scale of approximately $29.4 billion, and plans to debut on the Nasdaq as early as July 10th.

If completed at the current indicative price range, this would become one of the largest stock offerings in global capital market history – surpassing the approximately $25.6 billion offerings of Alibaba in 2014 and Saudi Aramco in 2019, second only to SpaceX's record $85.7 billion raise in mid-June.

In other words, if not for SpaceX breaking the record earlier in June, SK Hynix itself would have been positioned for the largest global stock offering.

It's important to clarify that this is not a traditional IPO for a previously unlisted company. SK Hynix is already listed in South Korea. This is a secondary listing via ADR in the U.S., coupled with issuing new shares.

Theoretically, changing the trading venue doesn't create new revenue or profit out of thin air. Beyond raising capital, the business itself doesn't seem to change immediately.

But what capital markets truly price is never just current period profits. What the U.S. listing might actually change is its investor base, liquidity, capital expenditure capacity, and the narrative framework the market assigns to it.

The most direct change is that SK Hynix may undergo a transformation from a 'Korean memory cyclical stock' to a 'global AI infrastructure asset'.

For a long time, many large South Korean companies, including SK Hynix, have suffered from the so-called "Korean discount." Complex group governance structures, foreign exchange risk, market liquidity, and high entry barriers for international capital have often prevented even globally competitive Korean firms from achieving valuations comparable to their U.S. counterparts.

Objectively speaking, this isn't unique to Korea; it applies to all markets compared to the