Leverage flushed out, buying power absent: Bitcoin remains trapped in wait for a "final drop"

- Core viewpoint: The current Bitcoin market is in a deep correction phase of the late bear market. Key indicators show widespread losses among short-term holders and a retreat of institutional buying. However, the ultimate panic sell-off that historically triggers sustained rebounds has not yet occurred, and the market bottoming process remains incomplete.

- Key factors:

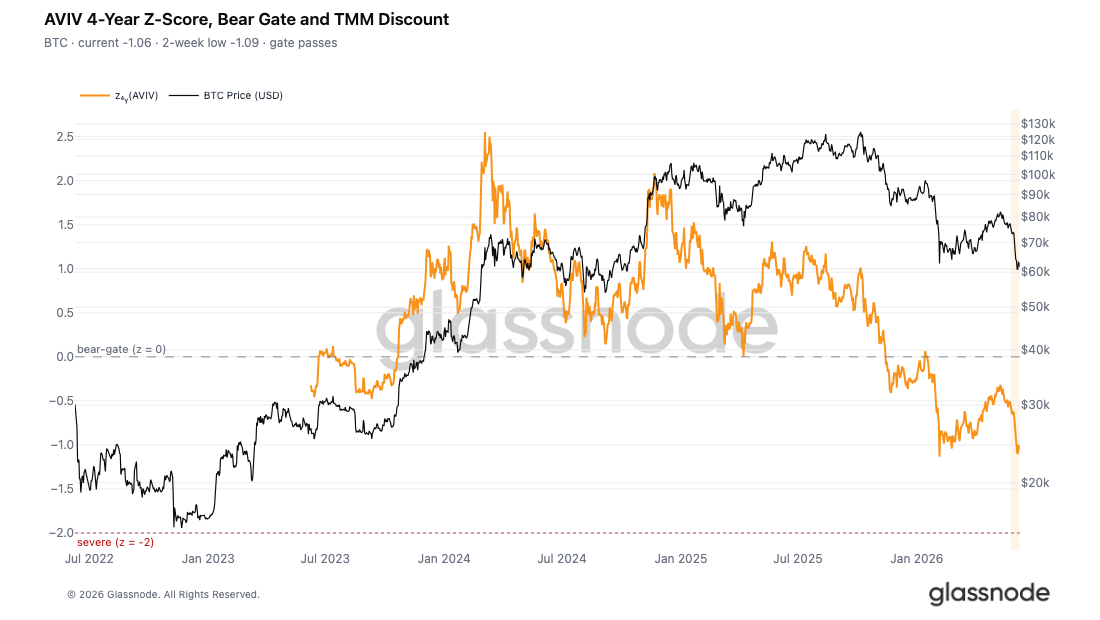

- The AVIV index Z-score has fallen to -1.06, entering deep discount territory, indicating that prices are severely oversold relative to the cycle average. However, no effective rebound has occurred at these low levels.

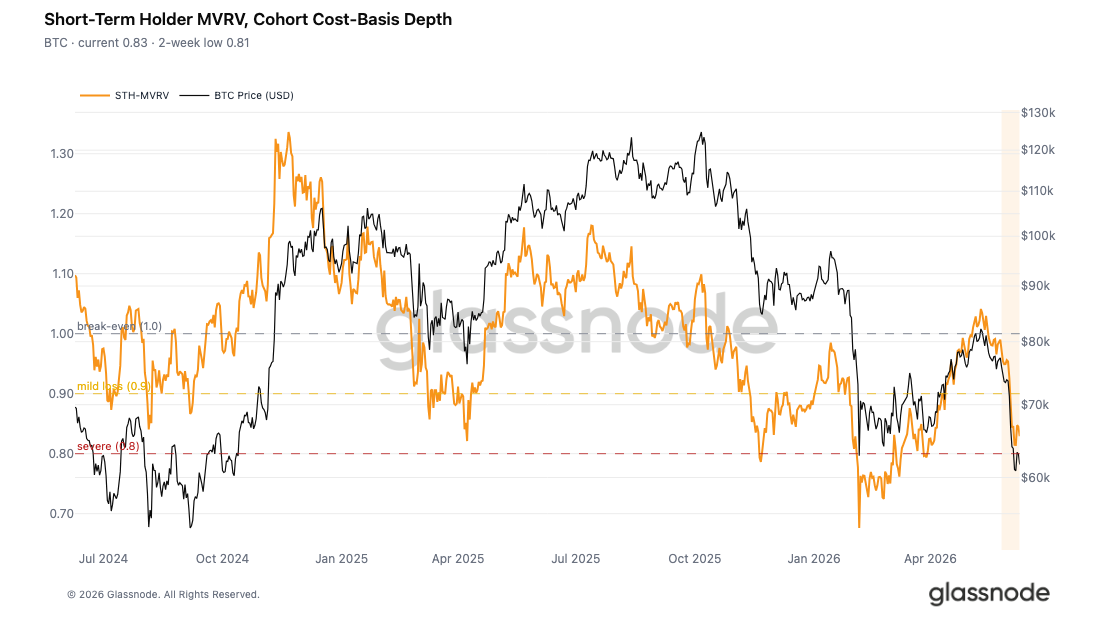

- Over 95% of short-term holders are in a loss-making position. The STH-MVRV metric shows new investors are facing an average unrealized loss of 17% to 19%, indicating a fragile market structure.

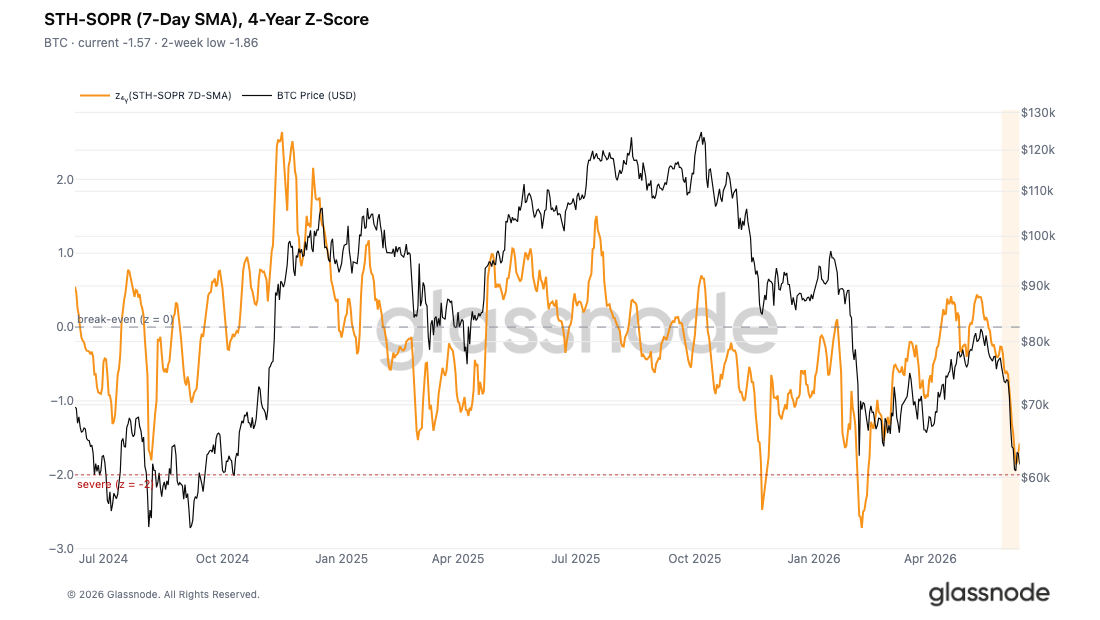

- The STH-SOPR Z-score touched a low of -1.86, approaching the -2 threshold for deep panic selling. Short-term holders' stop-loss behavior is intensifying, but it has not yet reached historical bottoming levels.

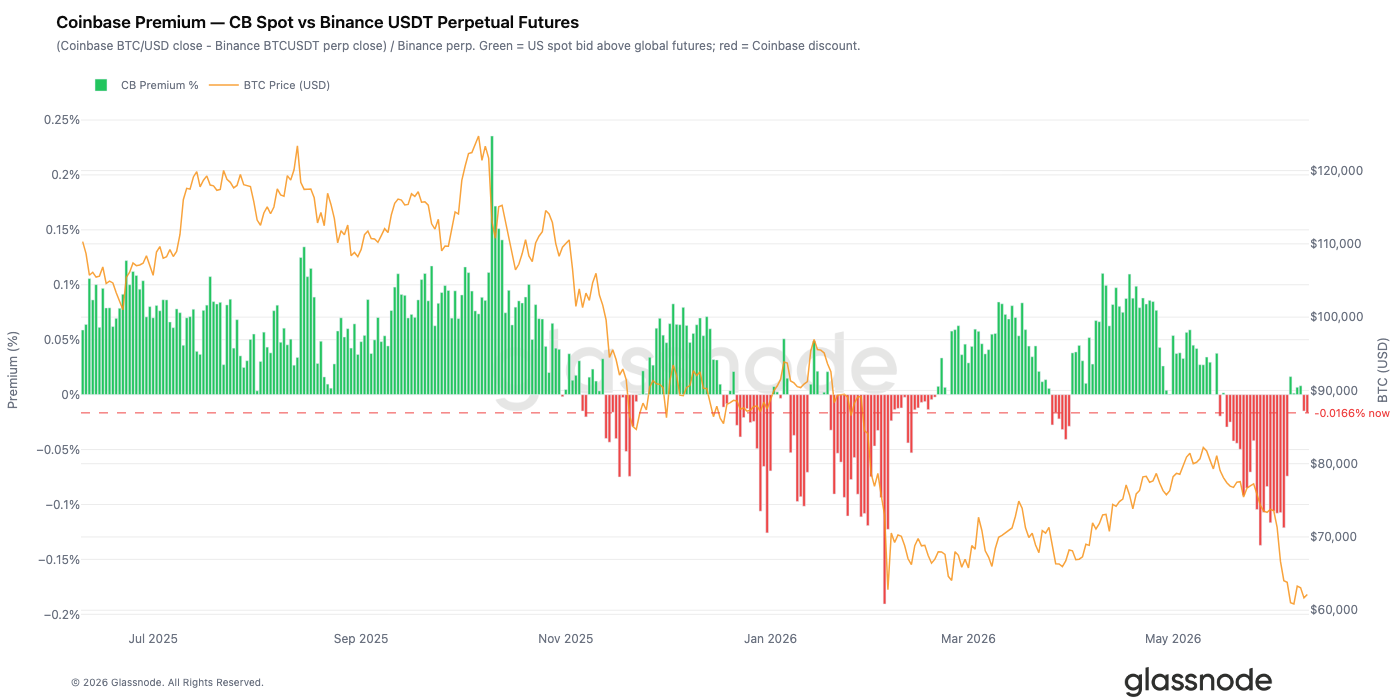

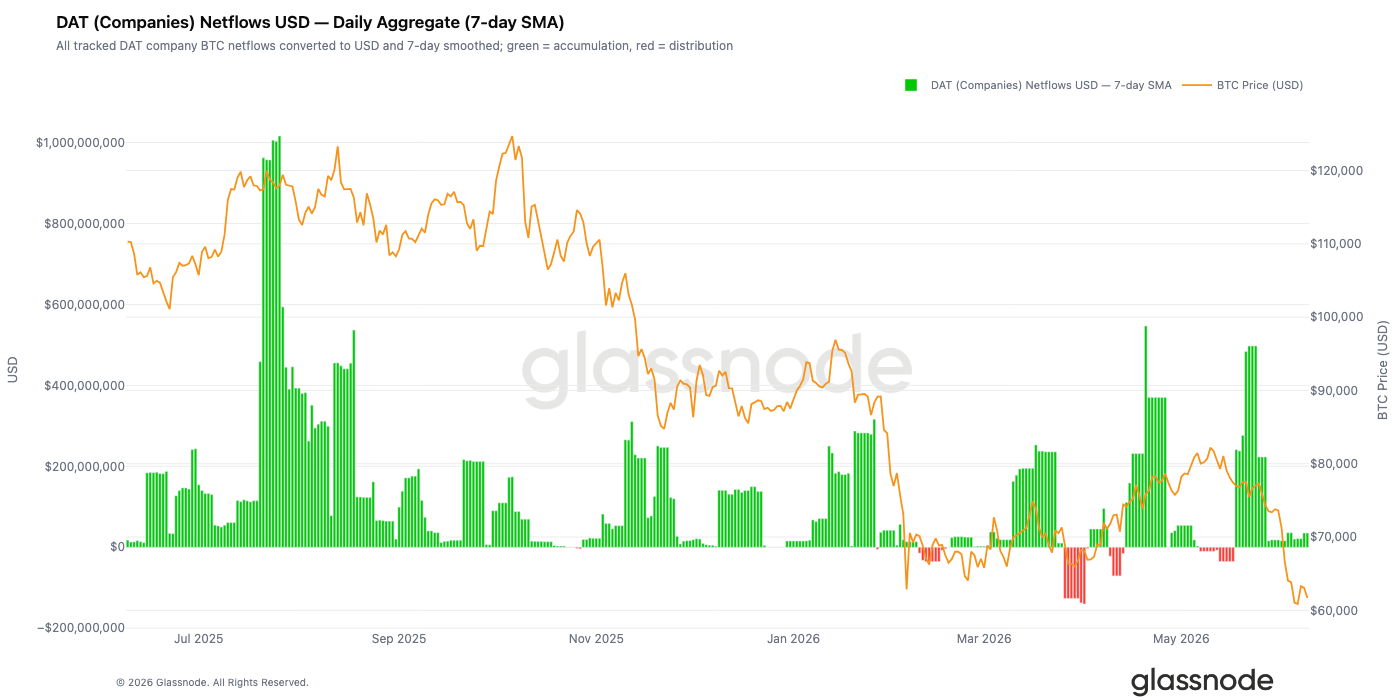

- US institutional demand has cooled significantly, with the Coinbase premium remaining in a continuous discount. The daily increase in corporate treasury Bitcoin holdings has fallen from over $500 million to near zero, indicating a weakening of core buying power.

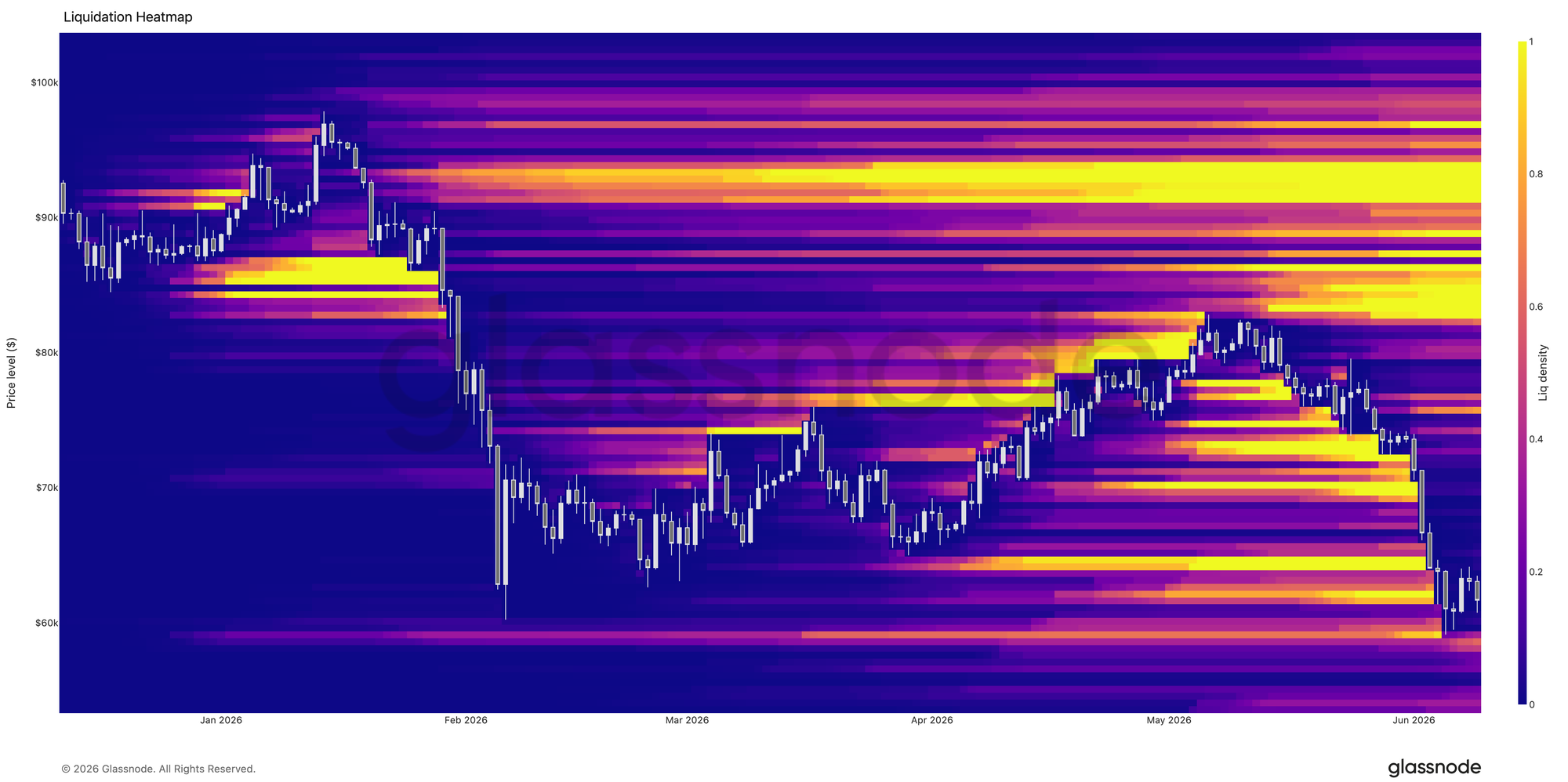

- After Bitcoin fell below $70,000, it triggered a large-scale deleveraging event. The liquidation heatmap shows that long positions in the $64,000 to $70,000 range were concentratedly liquidated.

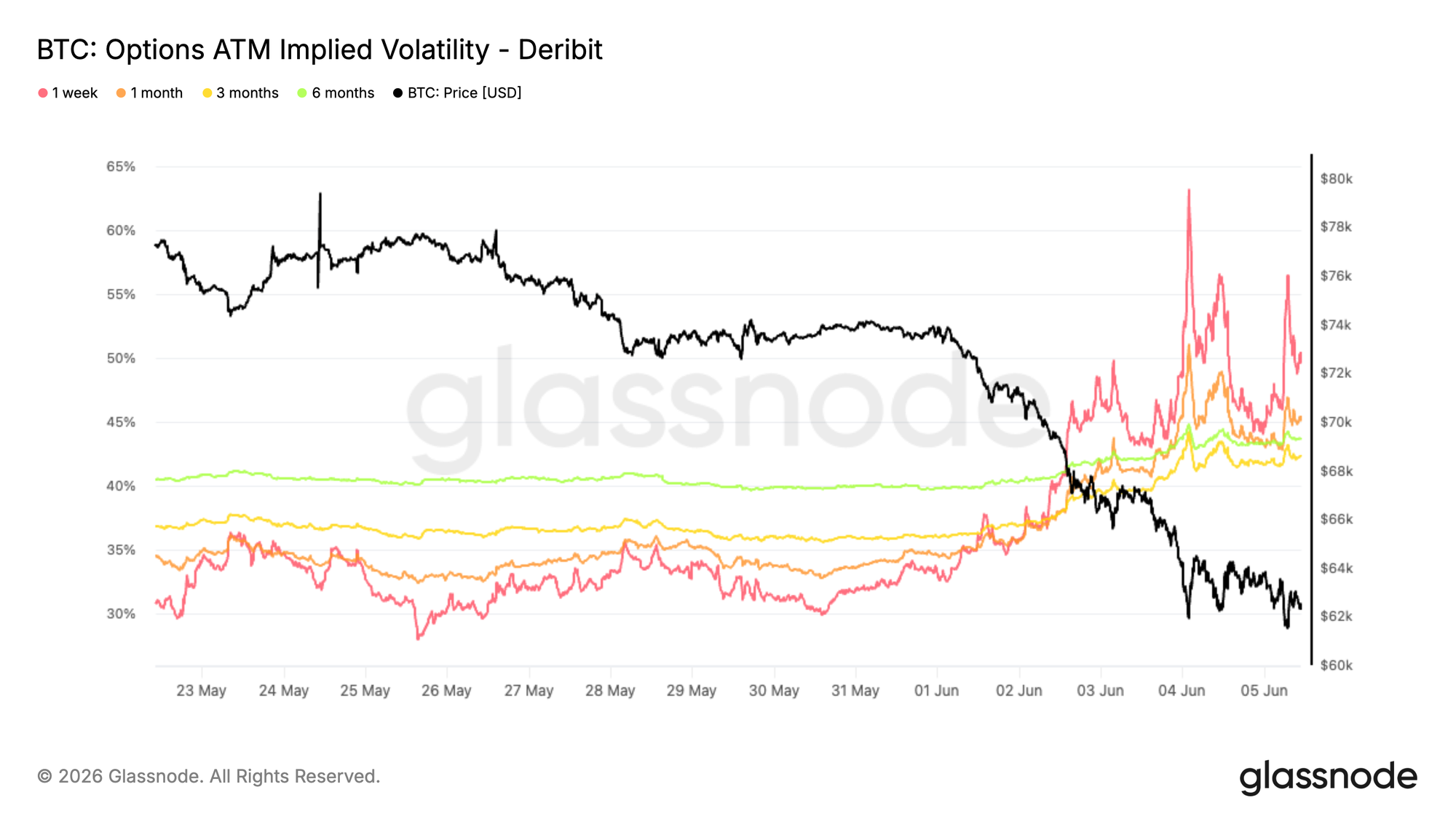

- Implied volatility has risen sharply, and the volatility risk premium remains elevated. The options market is pricing in significant future uncertainty that far exceeds recent actual volatility risks.

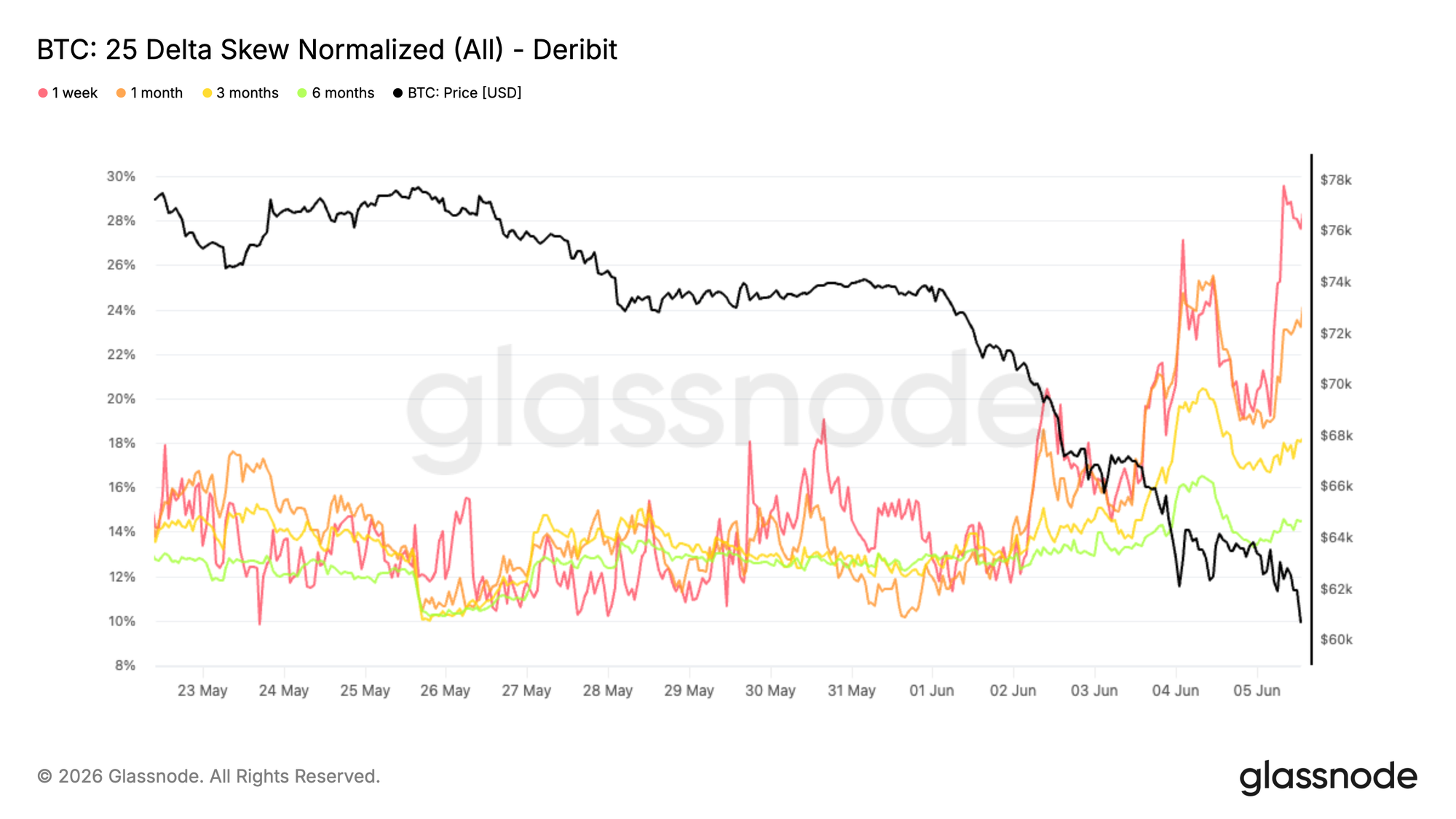

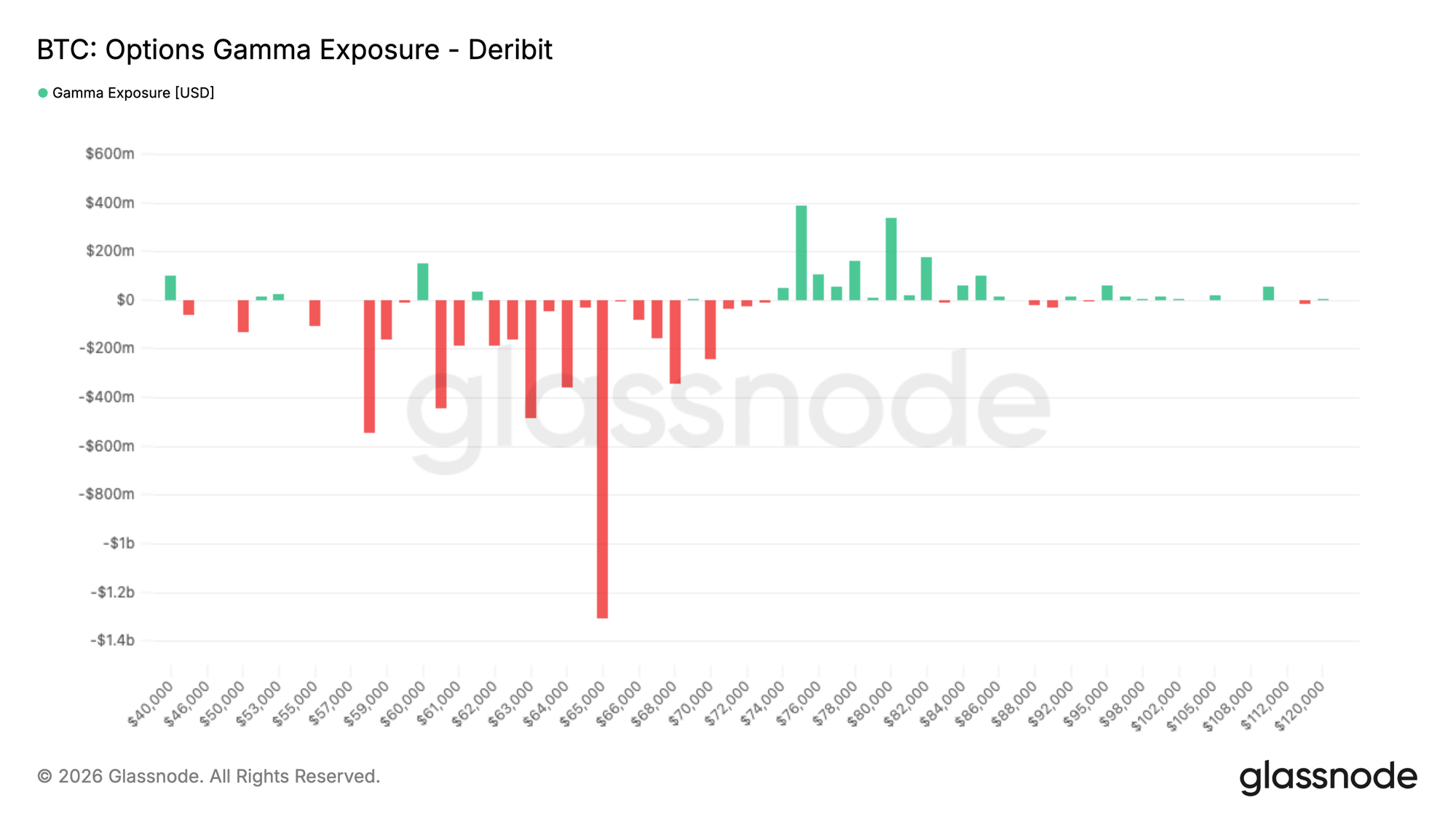

- The 25-delta volatility skew for all tenors has surged, with the market concentrating on downside protection. Market makers' largest negative gamma exposure is located near the $65,000 level.

Original Authors: Chris Beamish, CryptoVizArt, Antoine Colpaert, Glassnode

Original Compilation: Chopper, Foresight News

TL;DR:

- The AVIV index Z-score dropped to -1.09 before recovering slightly to -1.06, indicating that the current price has entered a deep oversold territory relative to the cyclical average. The price failed to see an effective rebound at the low, and market panic sentiment continues to spread.

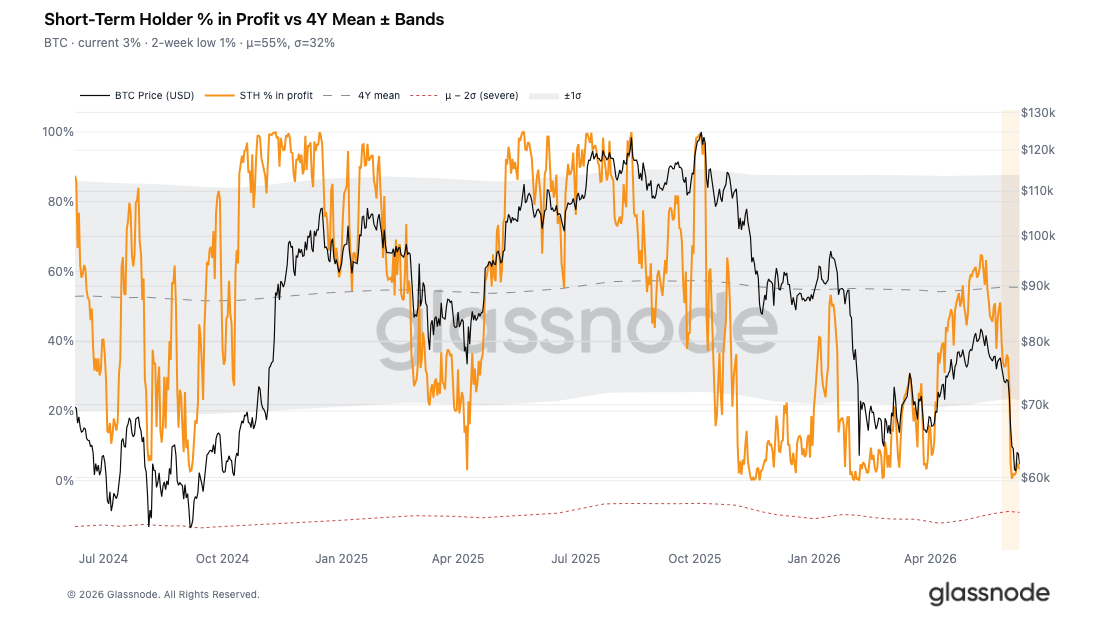

- Over 95% of short-term holders are in a loss position. The proportion of profitable supply held by short-term holders has only slightly recovered to 3.3%, far below the four-year average of 55%. The market fundamentals are fragile and highly susceptible to external shocks.

- The Z-score of the Short-Term Holder Spent Output Profit Ratio (STH-SOPR) bottomed at -1.86, just a step away from the critical threshold of -2 for deep panic selling. This indicates that market stop-loss actions are intensifying but have not yet reached the selling pressure intensity historically required to generate a sustainable rebound.

- Institutional demand in the US has cooled significantly. As Bitcoin pulled back to $60,000, the Coinbase premium consistently remained in a discount zone, reflecting a lack of active institutional buying on the spot market of that platform.

- The pace of Bitcoin accumulation by corporate treasuries has slowed dramatically. Since June, the daily net purchase volume by institutions has fallen from a peak of over $500 million to near zero, removing another major source of market support.

- After Bitcoin broke below key support levels, the market experienced a significant deleveraging event, leading to the concentrated liquidation of a large number of leveraged long positions and clearing out excessive speculative positions.

- After Bitcoin broke out of its range, implied volatility surged significantly. The volatility risk premium continued to rise, with the uncertainty priced by the options market far exceeding the risk level corresponding to recent actual price movements.

- Options volatility skew indicators across all tenures surged, indicating a significant increase in demand for downside protection instruments, with traders paying higher premiums for put options.

- Market trading is predominantly defensive. The largest negative gamma exposure is concentrated near the $65,000 strike price, which is not far from the current spot price.

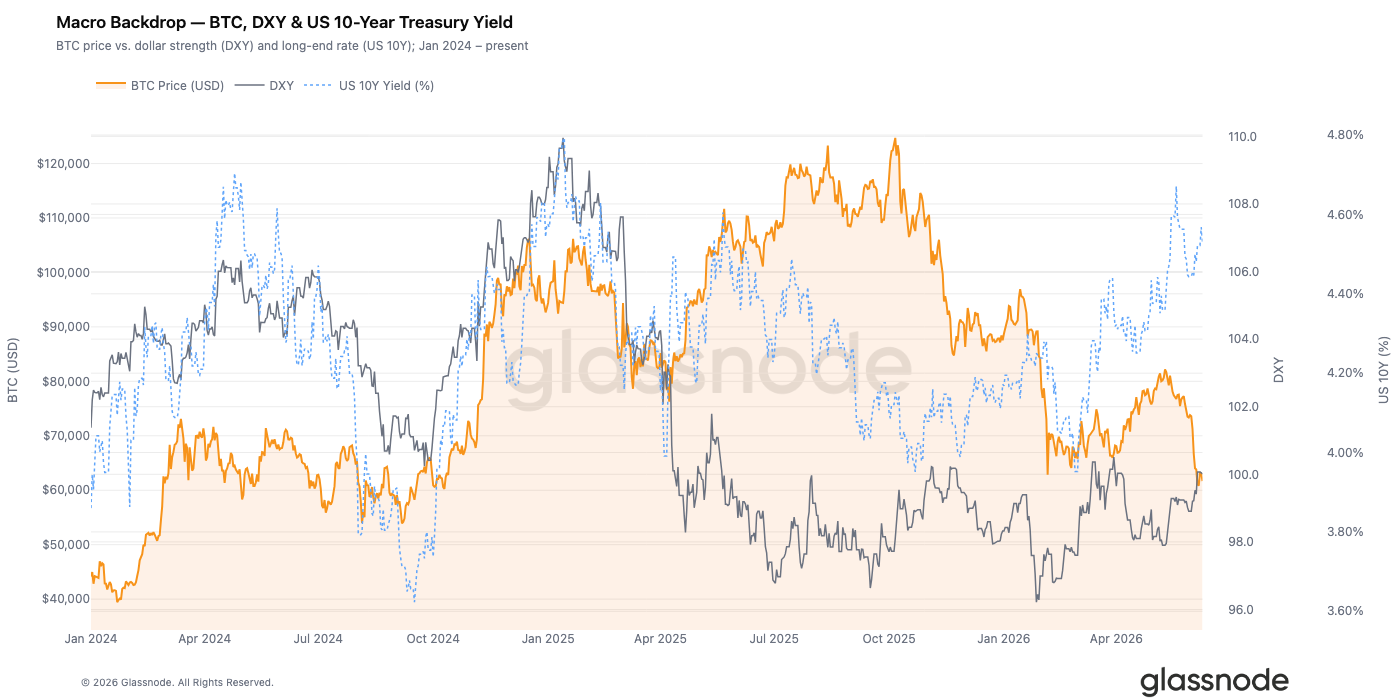

Macro Market Insights

The US Dollar Index closed at 100.01, up 0.8% for the week and 2.1% over the past thirty days. The continued strengthening of the US dollar has led to a general tightening of global liquidity over the past month. The US 10-year Treasury yield remained at 4.53%, while the 2-year yield was 4.14%, resulting in a spread of 0.39%. The shape of the yield curve suggests the US economy is in the late cycle phase, and the Federal Reserve has not yet made substantial adjustments to its monetary policy.

Affected by adverse macro factors, Bitcoin fell 7.5% this week to a current price of $61,700. After a period of divergence, the negative correlation between a 'strong dollar and pressured crypto assets' that formed during 2022-2023 has re-emerged. With the Dollar Index holding above 100 and the 10-year yield breaking above 4.5%, history suggests such a combination of interest rates and the dollar typically compresses speculative premiums for risk assets.

For Bitcoin to see a sustained rebound, one of two conditions needs to be met: the Dollar Index effectively breaks below 99, or the 10-year Treasury yield falls back to around 4.2%. Currently, neither condition has been fulfilled.

On-Chain Data Analysis

Valuation Deep in Oversold Territory

Our previous analysis pointed out that the May rally was a bear market rally. The short-term holder cost basis falling below the Real Market Price for the first time since January 2022 signaled that the market had entered the late stages of a bear market. This analysis continues to interpret the subsequent pullback, including the price dip to $59,000 and the fragile consolidation that followed.

We use the Active Investor Value Deviation (AVIV) ratio to judge how much the current price is oversold relative to the cyclical average. This metric compares the spot price against the Real Market Price (the aggregate cost basis of active investors, excluding miner holdings). Its four-year Z-score measures the deviation of the price from this benchmark, with a Z-score of 0 marking the boundary between valuation premium and discount.

Currently, the AVIV ratio stands at 0.80, corresponding to a Z-score of -1.06, which touched a low of -1.09 over the past two weeks. Current valuations are in a deep discount zone within the historical range. The price's persistent failure to rebound effectively from its cyclical low over the past week is ample evidence of lingering market panic.

New Entrants are Universally Underwater

Adding to the overall discounted market state, we analyze the specific situation of recently entered capital. The Short-Term Holder Market Value to Realized Value (STH-MVRV) ratio compares the spot price to the cost basis of short-term holders. A value below 1 indicates this group is, on aggregate, holding unrealized losses.

This metric recently hit a low of 0.81 before rebounding slightly to 0.83. This implies that new investors are, on average, facing an unrealized loss of 17% to 19%. This corroborates that the dense trading zone formed between $78,000 and $82,000 during May's rally is now broadly underwater, consistent with our previous assessment of 'pressure on new entrants'.

A temporary stabilization of price at lows is a common pattern in downtrends. Once the most heavily loss-making investors complete their initial round of passive selling, the remaining market participants enter a wait-and-see mode. Whether this consolidation phase ultimately forms an effective bottom or is just a pause before further decline depends on the emergence of new buying demand at current levels.

95% of Short-Term Holders in Loss

To further assess the pressure on short-term holders, we look at the percentage of short-term holder supply in profit. This metric tracks the proportion of short-term supply held in profit to judge the *breadth* of losses, distinct from metrics measuring the *depth* of losses.

This metric recently bottomed at just 0.6% and has only slightly recovered to 3.3%, far below the four-year average of 55%. In practical terms, over 95% of short-term holders are currently in a loss position. This magnitude of loss historically signifies a pronounced capitulation zone, where new investors are under widespread stress, making the market structure fragile and highly vulnerable to any negative external catalyst.

The near-universal losses across the market, coupled with the lack of significant recovery in related metrics, strongly suggests that the current sideways movement is merely a temporary exhaustion of selling pressure, not a completed market bottoming process.

Market Approaches Panic Selling Threshold

Beyond unrealized loss data, the actual selling behavior of investors further confirms the severity of the current market situation. Using the four-year cyclical average as a baseline, we calculate the Z-score for the 7-day moving average of the Short-Term Holder Spent Output Profit Ratio (STH-SOPR) to measure the intensity of realized losses among new investors this cycle.

The current Z-score for this metric is -1.57, with a two-week low of -1.86. This is just 0.14 standard deviations away from the historical deep panic selling threshold of -2.

At this stage, short-term holder capitulation is becoming more frequent and accelerating, corroborating the single-day total realized loss of $1.35 billion reported previously and the deep unrealized losses indicated by the STH-MVRV. However, the ultimate panic selling event historically required to catalyze a medium to long-term rebound has not yet occurred.

The market is currently in an awkward middle state: the scale of realized losses is sufficient to confirm a bear market depth, but it has not yet reached the standard for a complete cleansing of selling pressure that builds a solid bottom.

Off-Chain Market Insights

Coinbase Premium Disappears Completely

The Coinbase premium metric, which measures the price difference between Coinbase spot and Binance perpetual futures, is a key window into US institutional demand. When Coinbase trades at a premium, it indicates institutions are actively buying spot Bitcoin, pushing its price above offshore contract market quotes.

In recent weeks, the market dynamic has completely reversed, with this premium persistently in a discount zone. During Bitcoin's decline towards $60,000, buying appetite in the US spot market cooled entirely. The 'buy-the-dip' behavior typically seen in previous corrections has not materialized this time. Institutions are generally on the sidelines, removing another important source of market support.

Corporate Treasury Demand Cools

From April to May, sustained accumulation by corporate treasuries was a core pillar of market support, with several instances of daily net purchases exceeding $500 million. However, since June, this demand has weakened significantly.

During Bitcoin's decline from above $75,000 to $60,000, the scale of net corporate treasury buying shrank dramatically, dropping to a fraction of previous levels. While corporates appear to still be net buyers overall, the reduced pace of accumulation indicates a more cautious risk appetite within this cohort. Marginal buying demand has further diminished in an environment of generally low market sentiment.

Broad Deleveraging Below $70,000

Liquidation heatmap data shows a significant cluster of leveraged long positions concentrated in the $64,000 to $70,000 range. As Bitcoin rapidly declined last week, long positions within this range were forcibly liquidated in a cascading fashion, briefly pushing the price below $60,000 before finding support.

Long liquidity in the immediate vicinity has now been largely exhausted, completing a significant round of market deleveraging. Compared to data from a week ago, the current leveraged position structure is healthier, with much of the excessive speculative leverage accumulated during the recent trading range having been cleared out.

Implied Volatility Surges Upwards

After Bitcoin broke out of its months-long trading range, the entire volatility surface underwent a repricing. Demand for option instruments increased across the board as the spot price approached February lows.

Short-term volatility reacted most violently. The 1-week at-the-money implied volatility briefly spiked above 60% before settling back near 50%. 1-month implied volatility rose from approximately 34% to 45%. Longer-dated tenors also moved higher, with the 6-month implied volatility increasing from around 40% to 44%.

This volatility increase represents a comprehensive reassessment of future uncertainty by the market, not a short-term emotional disturbance. Although volatility has receded from its peak, demand for hedging instruments remains robust. Even with a temporary stabilization in spot price, traders are still willing to pay a higher cost for risk protection. This downturn has fundamentally changed the market's expectation for volatility, with hedging costs rising across all tenors, indicating persistent risk aversion.

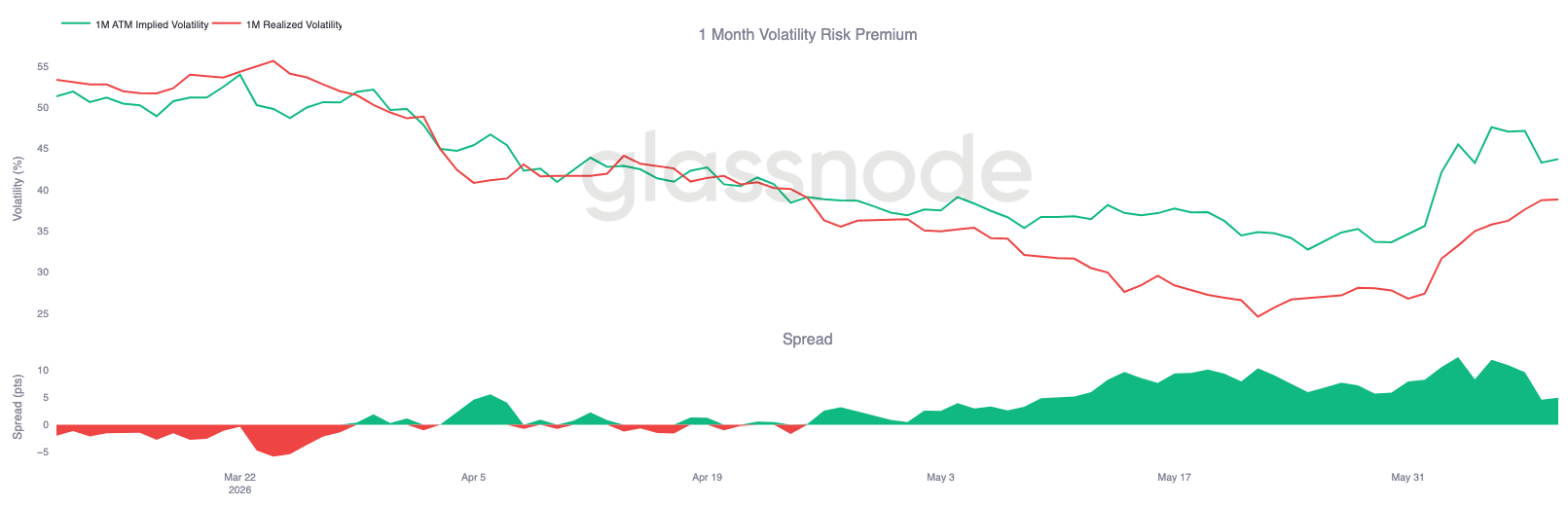

Volatility Risk Premium Remains Elevated

Comparing implied volatility (IV) to realized volatility (RV) after the surge in IV reveals that the options market is pricing in future volatility that is still higher than the spot's recent actual volatility.

1-month IV rose from ~35% to 44%. During the same downtrend, realized volatility also increased, from 27% to 39%. While both metrics moved higher together, the increase in IV was more aggressive, keeping the volatility risk premium positive.

Following the breakdown of a key support level, the market urgently repriced risk, causing the IV/RV spread to widen to as much as 10 volatility points. Although this spread has narrowed somewhat, option prices remain above the level justified by actual market volatility. This reflects a broad market expectation that significant turbulence is still to come.

The future uncertainty priced by the options market far exceeds the risk reflected by recent actual price movements, hence the persistently high volatility risk premium.

25-Delta Volatility Skew Surges Sharply

Within the context of generally higher volatility premiums, the volatility skew metric clearly reveals the direction of capital flows. As Bitcoin broke support and headed towards February lows, traders focused their buying on downside protection instruments.

Volatility skew is calculated as put option volatility minus call option volatility. A positive value indicates that puts are more expensive than comparable calls. This downturn caused skew figures across all tenures to rise collectively: 1-month skew increased from around 11% to 24%, while 3-month and 6-month skews climbed to 18% and 14%, respectively.

The short-term metric reacted most strongly, with 1-week skew briefly approaching 30%. During the sell-off, the market's demand for short-term downside hedging erupted in a concentrated manner. If the rise in implied volatility represents a market-wide risk alert, then the volatility skew clearly points in a single direction – capital is being deployed predominantly for downside hedging.

As the market environment continues to weaken, the demand for downside protection has intensified significantly, with traders paying ever-increasing premiums for put options.

Significant Gamma Exposure Clusters Near $65,000

Beyond options prices, gamma exposure helps identify the strike prices where option market makers' hedging activities have the greatest impact on price action.

The current market trading style is predominantly defensive. Over the past seven days, put option volume constituted 32.4% of total options volume; over the last 24 hours, this share has increased further to 35.9%. Even after a significant sell-off, market trading remains focused on buying downside protection.

This trading behavior is directly reflected in the gamma exposure profile: the largest negative gamma exposure is currently concentrated at $65,000, with substantial negative gamma also distributed across the $59,000 to $70,000 range. Bitcoin's current price of ~$62,000 places it just below this zone of maximum short-term negative gamma. Conversely, positive gamma exposure is mainly concentrated higher up in the $76,000 to $82,000 range.

Defensive trading dominates market makers' positioning, resulting in the market's largest negative gamma zone being located around the $65,000 level, very close to the current spot price.

Summary

The current market displays classic characteristics of a late-stage bear market correction: recently entered investors are deeply trapped, realized losses remain at elevated levels, and multiple core buying forces have weakened.

Bitcoin's pullback towards $60,000 triggered a significant deleveraging event, leading to a concentrated liquidation of speculative positions. Leverage levels have returned to more reasonable levels, but the spot market has failed to see any effective new buying demand emerge.

The options market maintains a defensive posture overall, with high implied volatility, strong demand for downside hedging, and key dealer gamma exposure tightly bound to the current spot price. This, coupled with a decline in institutional participation and reduced pace of corporate treasury accumulation, clearly indicates persistently low market risk appetite.

Synthesizing the data, the market is gradually moving towards a phase of deep panic selling. While leverage has been largely cleared and valuation metrics have fallen into historically deep discount territory, the incremental buying demand typically required in history to build a solid bottom has not yet appeared.