SpaceX上市交易核心窗口:7月7日納指納入日與7月財報會後解禁點

- 核心觀點:SpaceX即將進行IPO,發行價135美元,初始市值1.75萬億美元。由於初始自由流通量極低(4.3%),疊加指數基金快速納入帶來的被動買盤,上市初期可能形成「籌碼真空期」並推動股價翻倍。同時,市場推測馬斯克可能藉機推動SpaceX與特斯拉的對等合併,以解決其個人的稅務問題並構建資本帝國。

- 關鍵要素:

- 極低的自由流通量(4.3%)與納斯達克、富時羅素等指數快速納入的規則相疊加,預計在7月7日產生80-180億美元的被動買盤,形成強烈的價格上漲動力。

- 早期股份的解禁時間被精密設計與Q2財報電話會議掛鉤,但扣除創始人馬斯克的嚴格禁售期後,實際拋壓僅為10%-15%,低於市場預期的30%。

- 市場存在「對等合併」猜想:在7月7日股價衝頂與7月底財報解禁之間,可能宣布SpaceX與特斯拉進行「股票換股票」的合併,以解決馬斯克8月前需行使期權帶來的70億美元稅務壓力。

- SpaceX此次IPO引入了施瓦布、摩根士丹利等此前與馬斯克不和的投行,被視為通過巨大的經濟利益換取它們在特斯拉未來合併投票中的支持。

- SpaceX的治理架構(超級投票權、強制仲裁)為創始人提供了絕對控制權,是將其作為收購特斯拉主體的優越性所在,旨在從根本上解決創始人控制權問題。

Original Author: Xu Chao

Original Source: Wall Street CN

SpaceX is about to usher in a historic IPO this Friday, with the offering price set at $135 and an initial paper market value of $1.75 trillion. As a super unicorn of rare scale in Wall Street history, its post-listing stock price trajectory and chip game have sparked狂热 attention from global investors.

Prominent Tesla community opinion leader and former Wall Street analyst Alexandra Mertz (known online as Tesla Boomer Mama) recently engaged in an in-depth conversation with host Herbert. Mertz believes that due to the extremely low initial public float (only 4.3%), SpaceX could experience an epic chip vacuum period in the early stages of listing.

According to a Bloomberg report on Wednesday, index rebalancing forecasting firm Intropic estimates that because Nasdaq, FTSE Russell, and MSCI all plan to rapidly include SpaceX in their indices, passive investors are expected to hold approximately 30% of SpaceX's outstanding shares just 15 trading days after listing. In contrast, under the previous slower inclusion rules, this ratio would only be about 4%.

Academics and market observers warn that this scale of mechanical demand, coupled with market frenzy over Musk, SpaceX, and artificial intelligence, could form a self-reinforcing feedback loop, driving the stock price continuously higher.

Mertz believes investors need to closely watch two key time points of great trading value: the passive buying peak triggered by "the official inclusion of Nasdaq 100 on July 7," and the "coincidence of early shareholder lockup expiration and potential merger announcement in the two days following the Q2 earnings call in the second half of July." Hidden behind this highly meticulously designed IPO is also a massive capital chess game where Musk addresses his own $7 billion tax event and uses Wall Street investment banks for interest exchanges.

Core Viewpoint Summary

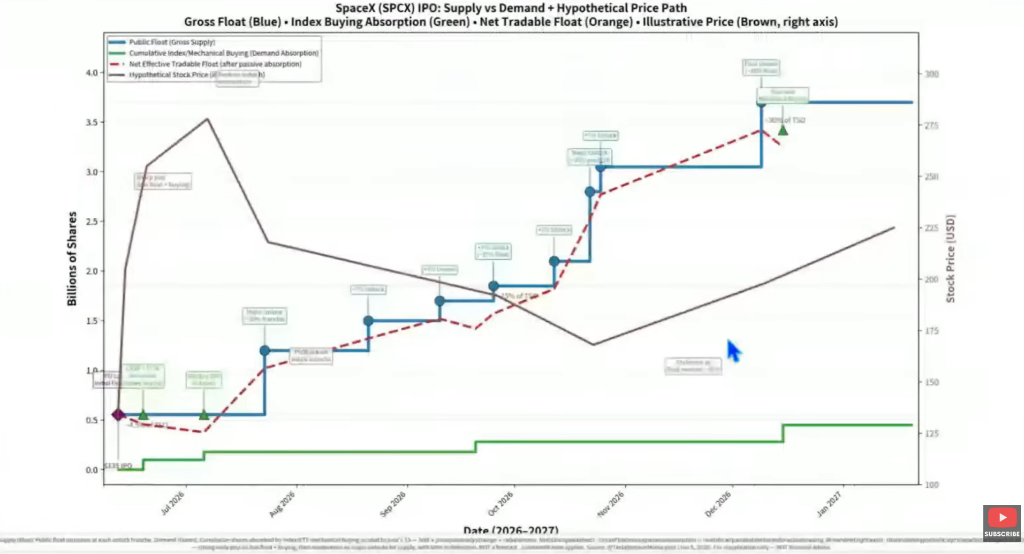

July 7 Nasdaq Inclusion Day: Nationwide passive fund building positions will collide head-on with the historically lowest public float. Market estimates peg this passive buying volume between $8 billion and $18 billion (closer to $15 billion). Since old shareholders cannot sell shares at this time, the market's public float hits its lowest point.

Two Days After Q2 Earnings Call Lockup Expiration: The initial unlock amount appears to be 30%, but after deducting Musk's own 50% share with a 1-year absolute lock-up period, the actual selling pressure is only 10%-15%.

July "Merger of Equals" Speculation: Musk faces a $7 billion tax pressure from exercising Tesla options before August 15. Announcing a "stock-for-stock" merger of equals between the two companies between the SpaceX stock price peak on July 7 and the earnings lockup expiration at the end of July is a highly clever capital script consistent with Musk's style.

Wall Street Investment Banks' Interest Exchange: Schwab, Morgan Stanley, JPMorgan, and other former Tesla institutional "adversaries" are rarely allocated generous SpaceX IPO quotas. This could be Musk's pre-arranged institutional "yes votes" for the November shareholder meeting merger vote.

1. Extremely Low Public Float (4.3%): Grok Model Predicts Stock Price Could Double by July 7

SpaceX (ticker symbol tentatively SPCX) has priced its IPO at $135, giving it an initial paper market value of $1.75 trillion. It plans to issue 555 million shares of Class A common stock (approximately $7.5 billion in fundraising). As market subscription interest is already oversubscribed by 2 times, underwriters are highly likely to fully exercise the "Greenshoe option" (over-allotment option) within 30 days, increasing total fundraising to $8.6 billion.

Despite the massive fundraising scale, the issued Class A shares only account for 4.3% of the total market value. This means SpaceX's public float in the early stages of listing is extremely tight, and SpaceX will face a very strong chip vacuum period within 15 trading days after listing.

First Key Time Point: July 7 This day is the first trading day after the Independence Day weekend and the 15th trading day after the IPO. The Nasdaq 100 Index will officially include SpaceX.

At that time, major index funds like Vanguard CRSP and FTSE Russell must unconditionally passively build positions in the open market based on the float-adjusted mechanism.

Market estimates peg this passive buying volume between $8 billion and $18 billion (closer to $15 billion). Since old shareholders cannot sell shares at this time, the market's public float hits its lowest point.

2. "Precision Lockup Expiration" Tied to Earnings Call: Selling Pressure Halved, $135 Forms a Strong Price Floor

Conventional IPO lock-up periods are usually a simple one-size-fits-all (e.g., 180 days), but SpaceX's lockup expiration (unlocking) schedule is precisely tied to the Q2 earnings conference call.

Second Key Time Point: Two business days after the Q2 earnings call (estimated around July 22 or 29)

Market rumors suggest that after the Q2 earnings conference call, early insider shareholders will face the first batch of large-scale unlocks up to 30%, triggering market panic over selling pressure.

However, Alexandra clearly clarified in the conversation that market analysts overlook the core equity structure: Among early insider shareholders, the majority (about 50%) is Musk himself. As the founder, Musk's shares have a strict 366-day lock-up period.

Therefore, two days after the Q2 earnings call, the truly potential new unlocked shares flowing into the public market are not 30%, but actually only 10% to 15%.

Furthermore, the will of major early shareholders is highly aligned:

Ron Baron has explicitly stated, "Not selling a single share, and will add another $1 billion in the public market";

BlackRock has publicly expressed a strong intention to buy $5 billion to $10 billion at the IPO, exceeding the market's ready supply;

Ark Invest (ARC), although limited by the 10% single stock cap and may selectively sell old shares, plans to add SpaceX positions in its other newly opened funds.

3. July's "Goldilocks" Script: $7 Billion Tax Event and "Merger of Equals" Speculation

Sharp money on Wall Street is connecting all the breadcrumbs. Alexandra points out that Musk faces a huge personal timeline: He must exercise his stock options from the 2018 Tesla compensation plan before August 15 this year, triggering a massive $7 billion personal tax event (payable in January 2028).

In the days surrounding the option exercise on August 15, the higher Tesla's stock price, the more favorable it is for Musk's personal net share settlement or pledge loan. This is not small change, but a massive game involving tens of billions of dollars.

Therefore, the most reasonable "Goldilocks scenario" speculation on Wall Street is emerging:

- Timing: During the power vacuum between the completion of the Nasdaq inclusion on July 7 (SpaceX stock price more than doubles, market cap peaks) and the earnings unlock at the end of July (fresh shares flood in).

- Strategic Action: SpaceX and Tesla announce a merger of equals via a stock-for-stock exchange.

This type of merger would automatically put the two companies' stock prices into a perfectly synchronized "lock step" mode, driven by market arbitrage funds. By leveraging positive news from both companies to boost market cap through public market "non-sellers," Musk's tax funding pressure would be perfectly resolved.

4. Wall Street Investment Banks' "Political Arbitrage": Swapping IPO Feast for November Election Yes Votes

The biggest uncertainty in the merger script lies in the November shareholder meeting vote.

According to Alexandra's precise calculations: After exercising options, Musk holds approximately 17.5% voting power in Tesla. Passing the merger requires an absolute majority of "50% plus one vote" from all outstanding shares, meaning Musk needs to secure 32.5% more yes votes externally.

Currently, Tesla's retail shareholder proportion has dropped from over half in the past to 31%, while institutional big whales have been secretly increasing their holdings aggressively in Q1 this year. To succeed, support from big whales like Vanguard and BlackRock (together holding over 15%) is necessary. BlackRock CEO Larry Fink has already mended relations with Musk at venues like the Davos Forum, and the institutional vote base (about 35%) seems initially secure. The remaining 15% gap requires mobilizing half of the 31% retail shareholders.

Interestingly, SpaceX's IPO has rarely included Charles Schwab, Morgan Stanley, and JPMorgan as core underwriters and distributors. These three institutions were the leading "adversaries" who voted against in the past Tesla compensation case and the relocation to Texas case:

Wall Street Political Bet: As the most profitable and prestigious IPO quota in Wall Street history, no investment bank can resist the billions in commissions and client prestige.

By giving this "fat piece of meat" to these three institutions, Musk's implicit wager is: Take SpaceX's money, then manipulate the shares they custody to vote "yes" for the merger at the November Tesla shareholder meeting.

Wall Street is profit-driven; faced with enormous economic benefits, they will not hesitate to compromise.

5. "The Perfect Defensive Fortress": Why Must SpaceX Acquire Tesla?

Addressing technical questions from some investors, the interview provided answers with significant legal and corporate governance depth:

1. How can SpaceX complete the acquisition without hundreds of billions in cash on its balance sheet?

This is absolutely not a cash deal, but 100% pure equity swap. SpaceX currently has an authorized share capital ceiling of up to 36 billion shares, with only about 13 billion shares actually issued post-IPO. It has enormous room for issuance and can directly issue new shares to exchange for all Tesla shares.

2. Why can't Tesla acquire SpaceX instead?

Because SpaceX's S-1 prospectus established a perfect "founder's defensive fortress."

Musk suffered greatly from malicious short sellers, activist investors, and Delaware judges during the Tesla era. In contrast, SpaceX's governance structure was rigorously fortified from the ground up:

Super Voting Rights: SpaceX's Class B shares carry 10x super voting rights, with 97% firmly controlled by Musk himself;

Judicial Firewall: All shareholder lawsuits are mandatorily subject to private arbitration, not public court proceedings, directly neutralizing the weapons of malicious litigation lawyers;

Successor Clause: Even if Musk unfortunately passes away, the super control rights of his Class B shares directly transfer to his family.

Tesla's current governance structure has inherent flaws, preventing Musk from achieving absolute control. Therefore, only by incorporating Tesla entirely under SpaceX's legal framework can Musk's absolute control over his entire business empire be permanently protected from activist investors and local court interference.

The following is the full interview text, translated with the assistance of AI

Herbert:

Alright, welcome everyone, and thank you for joining us today. We have Alexandra Mertz with us today, also known as Tesla Boomer Mama. I think today is going to be a very special episode where she will share with you the most authoritative guide to the SpaceX IPO. We'll also share a few very important slides with everyone, and I think I'll give you a little preview now.

First, Alexandra has done a lot of work, outlining what everyone can expect step by step if a merger is announced; then, she will walk you through in detail what happens on IPO day, when the Nasdaq inclusion occurs, and when shareholders can unlock and sell. So, thank you very much for all this work, Alexandra. I know this IPO is this Friday, so many people have been asking about it. Tell us, what are you going to share with us today?

Alexandra:

Hi, Herbert, thank you for having me. Well, it all started with—I mean, obviously for weeks and months, we've been discussing this merger idea. I am a firm believer in this merger. I want to start by saying that nothing that follows is financial advice.

But I personally bought a significant number of call options for August this year because I firmly believe in this. I didn't participate in Tesla—correct, it's Tesla, I didn't participate in the SpaceX IPO because in my predicted scenario, a merger will be announced sometime in July or early August this year.

The timing of the SpaceX IPO now actually gives me a lot of confidence, and that's why I wanted to do this episode. We've discussed before why this is very important for those investing in SpaceX, those staying in Tesla, and those investing in both. Because I think there are many key dates you must pay attention to, as SpaceX's stock price could jump around wildly, and no one knows what will happen, not even Elon. So, Herbert, let's go slide by slide. Which one do you want to start with?

Herbert:

Yes, this one looks like the most important one. First, thanks to Aurelius for putting this together, right?

Alexandra:

Exactly. Aurelius read my article on the details of the SpaceX IPO, which is pinned to my X (formerly Twitter) profile. You can go there, and you'll see his comment below, saying: "I input all your data into Grok."

Then Grok gave me this chart, which is highly interesting. You might need to zoom in a bit so everyone can see it. But, um, maybe they don't need to see us anymore, I don't know. Move a little to the left, if you can, to the left—I can't operate that. Okay, it all starts with the IPO this Friday, that's the brown point, the IPO price at 135, that's the inverted brown square, right.

Then you see this blue line, which represents that early investors currently cannot sell. As you can see, this lasts until the Q2 earnings conference call, where they will have the first batch of potentially large unlocks, up to 30%. That's the blue line, and I'll detail what happens after that shortly. The green line below is the demand from index funds buying SpaceX stock.

This is relative to the float. The first wave of dilution they put into the market is 555 billion shares (Note: this likely refers to market value share or a conversion of shares, clarified further below), accounting for 4.3% of the paper market value. This market cap will change, you'll see, but it starts