Bạn mua cổ phiếu Mỹ trên CEX không phải là thật: Phân tích độc quyền thanh lý 94% và sự bốc hơi quyền lợi qua 5 lớp trung gian

- Quan điểm cốt lõi: Các sản phẩm cổ phiếu Mỹ trên các sàn giao dịch tiền mã hóa hiện tại không đơn giản là một cuộc cách mạng tài sản RWA, mà đã phân hóa thành ba con đường: API truyền thống, Token hóa (Tokenized) và hợp đồng vĩnh viễn tổng hợp. Trong đó, mô hình Token hóa phụ thuộc rất nhiều vào sự độc quyền thanh lý của Alpaca, tồn tại rủi ro chênh lệch thời gian giữa giao dịch thời gian thực trên chuỗi và thanh toán T+1 ngoài chuỗi, và người dùng không có quyền lợi thực sự của cổ đông, mà chỉ nắm giữ chứng từ nợ do các thực thể ngoài khơi phát hành.

- Các yếu tố chính:

- Ba con đường phân hóa: Mô hình API truyền thống (ví dụ như quan hệ hợp tác giữa Binance và Alpaca) cung cấp quyền lợi thực sự của cổ đông và bảo vệ SIPC; Mô hình Token hóa (ví dụ Backed, Ondo) hy sinh quyền sở hữu để đổi lấy tính thanh khoản trên chuỗi; Hợp đồng vĩnh viễn tổng hợp (ví dụ Hyperliquid) chỉ cung cấp trò chơi phái sinh giá cả, không có giao dịch tài sản thực tế.

- Sự độc quyền và rủi ro của Alpaca: Alpaca độc quyền 94% thị trường thanh lý lưu ký cổ phiếu Mỹ đã được Token hóa. Mặc dù hệ thống ITN của họ đạt được khả năng đúc token trên chuỗi trong vài giây, nhưng chứng khoán cơ sở vẫn bị giới hạn bởi chu kỳ thanh toán T+1 truyền thống, tạo ra rủi ro "chênh lệch thời gian" và sự gián đoạn thanh khoản mà cuối cùng do người dùng cuối gánh chịu.

- Quyền lợi và rủi ro pháp lý: Trong cấu trúc 5 lớp trung gian, quyền biểu quyết của người dùng không có hiệu lực ở cấp tổ chức phát hành; cổ tức trở thành quyền đòi nợ theo hợp đồng chứ không phải quyền của cổ đông; Bảo vệ SIPC không thể xuyên thấu đến người nắm giữ trên chuỗi. Một khi tổ chức phát hành phá sản, token của người dùng sẽ không thể truy hồi tài sản cơ sở.

- Tăng trưởng và quy mô thị trường: Tổng quy mô token cổ phiếu Mỹ trên chuỗi đã mở rộng từ dưới 100 triệu đô la lên 1,56 tỷ đô la trong 10 tháng (tính đến tháng 6 năm 2026), nhưng vẫn thấp hơn nhiều so với thị trường truyền thống. Đồng thời, con đường API truyền thống đang nhanh chóng thu hút một phần dòng vốn tìm kiếm sự tuân thủ và đảm bảo.

- Tiềm năng DeFi bắt đầu lộ diện: bStocks do Binance phát hành đã được đưa vào quỹ cho vay của Venus Protocol làm tài sản thế chấp, đánh dấu sự khởi đầu khám phá khả năng kết hợp DeFi của cổ phiếu Mỹ Token hóa, nhưng ứng dụng này vẫn đang trong giai đoạn thử nghiệm ban đầu.

- Hướng phát triển công nghệ: DTCC có kế hoạch khởi động thí điểm chứng khoán Token hóa vào nửa cuối năm 2026. Nếu thành công, nó sẽ đưa vào tài sản Token hóa các đảm bảo pháp lý và thanh toán ở cấp độ truyền thống, có khả năng định hình lại cục diện cạnh tranh hiện tại.

Original authors: Ethan, Xinyang, IOSG

In 2026, CEXs intensively launched US stock trading products, creating a booming narrative at the forefront of the industry about "seamlessly buying and selling NVIDIA with USDT." However, peeling back the smooth trading interface to examine the underlying legal relationships and clearing processes reveals that this is far from a simple "RWA asset revolution." Instead, it is a complex game of interests involving spot pricing, equity attribution, and underlying custody monopolies.

TL;DR

- Three Paths Diverging: CEX US stock products have diverged into three parallel paths: traditional API, Tokenized, and Perpetual Contracts.

- Tokenized Model Highly Dependent on Alpaca: Alpaca monopolizes 94% of tokenized US stock clearing, posing risks from the time discrepancy between on-chain real-time and off-chain T+1 settlement, with ultimate hidden costs and black swan liquidity gaps borne by users.

- Tokenized U.S. Stocks Market Still in Blue Ocean Phase: Asset scale expanded roughly 15 times in 10 months, DeFi collateral potential is emerging, while the traditional API route is rapidly diverting funds.

The Divergence of Three Paths for US Stocks

In terms of capital flow, asset form, and most fundamentally, legal relationships, the US stock trading products offered by CEXs on the market are not the same category. Beneath the highly homogenized trading interfaces, they have diverged into three completely different evolutionary paths based on differences in underlying assets and legal structures:

The coexistence of these three models is not the result of a simple product design decision but rather the product of continuous compromise and iteration over the past few years between on-chain liquidity efficiency and traditional compliance clearing friction.

Early Exploration and Liquidity Limitations of Offshore Tokenization

The starting point of this track dates back to 2021-2024, with early attempts at on-chain asset tokenization (Tokenized Securities) represented by Backed Finance (xStocks) and Ondo Finance. The core business at this stage involved establishing a Special Purpose Vehicle (SPV) in an offshore jurisdiction, fully collateralizing real stocks off-chain, and minting corresponding tokenized certificates (e.g., AAPLx) on-chain. These assets possess the native characteristics of crypto assets, can be withdrawn to Web3 wallets and transferred permissionlessly on-chain, establishing a paradigm for moving assets on-chain from 0 to 1.

However, during the window period before traditional financial clearing giants substantively entered the crypto ecosystem, this model showed severe supply scarcity and scale limitations. Lacking liquidity support from mainstream CEXs, these tokenized assets could only circulate on a few decentralized protocols or second-tier platforms, causing the Total Value Locked (TVL) of the entire track to languish at low levels. As of August 2025, the total on-chain US stock market size was under $100 million. This characteristic of "having asset mapping but lacking transaction friction efficiency" inevitably relegated early tokenized US stocks to low-liquidity on-chain holdings, failing to truly reach mainstream retail traders.

Synthetic Perpetual Contracts: Pure Price Derivative Speculation

To compensate for the liquidity shortcomings of tokenized spot stocks, US stock/ETF perpetual contracts quickly became market protagonists. In September 2025, Bitget pioneered US stock perpetual futures, quickly expanding the underlying assets to over 40, with cumulative trading volume exceeding $15 billion. However, the real catalyst was Hyperliquid's HIP-3 (Permissionless Perpetual Contract Deployment Mechanism) launched on October 13, 2025, which fully activated the around-the-clock equity derivatives market. As of June 2026, the Open Interest (OI) for US stock-related perpetual contracts has exceeded $2.25 billion. Hyperliquid, leveraging HIP-3, holds a dominant share, with its Nasdaq-100 (XYZ100) and S&P 500 index perpetuals having OI exceeding $310 million and $340 million respectively.

Binance also followed aggressively in early 2026, capturing over 56% of the RWA perpetual CEX market share. Notably, its Pre-IPO derivatives like SpaceX (SPCX) saw peak daily trading volumes reaching billions of dollars. Additionally, Binance's Korean stock perpetual futures (Samsung, SK Hynix, Hyundai) launched in early June 2026 achieved a cumulative trading volume of approximately $470 million in their first week, with SK Hynix contributing over 90% and often exceeding $100 million in daily volume. This reflects strong retail leveraged trader interest in global hotspots like AI semiconductors. This demonstrates a key advantage of crypto perpetual platforms: the ability to quickly integrate international hotspot assets that traditional brokers find difficult or insufficient to cover, providing global retail investors with timely leveraged trading channels.

These synthetic perpetual contracts do not involve any actual off-chain stock delivery. They rely entirely on oracle price feeds, completing long-short speculation within the crypto exchange itself. This design brings high capital efficiency and continuity, especially providing efficient price discovery and liquidity even during US market hours. In contrast, real tokenized spots, needing to interface with traditional T+1 clearing, custody, and underwriting processes, often exhibit significant liquidity gaps, large slippage, and price distortions on-chain. This paradox where "derivative pricing efficiency surpasses spot" has become a structural pain point for the current tokenized stock model.

Traditional API Model: Exchanges Reverting to Internet Brokerages

Entering 2026, despite the SEC's ongoing efforts to provide a regulatory sandbox for digital assets (like the "Project Crypto Innovation Exemption Framework"), the uncertain legal definition and full compliance challenges for native on-chain securities led mainstream exchanges to explore a more pragmatic path. In June 2026, Binance officially announced a deep partnership with the US-licensed self-clearing broker Alpaca to launch US stock and ETF trading services.

This "traditional API routing model" is essentially an extension of traditional retail brokerage architecture onto the crypto exchange front-end. Through its associated broker Nest Trading routing, blockchain technology plays no role in the product's lifecycle settlement. A user's holdings are merely a data mapping within the exchange app; orders are ultimately executed on the NYSE or NASDAQ, with the underlying securities custodied in an Alpaca account.

The cost of this model is sacrificing all native crypto characteristics: stocks cannot be withdrawn to Web3 wallets, transferred on-chain, or transferred across platforms. The user's "holdings" are just a digital mapping line in the exchange app. However, its underlying logic is the most robust. Legally, the user is the "Beneficial Owner" of the securities, entitled to full dividends and nominal voting rights, and protected by the Securities Investor Protection Corporation (SIPC). This may seem like a compromise and regression for crypto exchanges, but it is currently the only path where users can truly "own" the stock.

Exchanges' Multi-Track Parallel Approach

Looking at the current mainstream US stock product lines, a deeper industry consensus emerges: most leading exchanges are not betting entirely on one path but are adopting a multi-model product layout. For instance, platforms like Binance, Bitget, and Bybit often simultaneously operate traditional API routing, tokenized assets, and synthetic perpetual contracts. This multi-track parallelism is not product redundancy. The core reason is to cater to the actual needs of different user groups within the crypto ecosystem – high-frequency speculators value the high capital efficiency and leverage of synthetic contracts, while long-term, large-capital allocators ("whales") prioritize the compliance guarantees and SIPC legal protection offered by the traditional API model.

This mixed layout is also a hedging strategy for exchanges against regulatory uncertainty. The traditional API model leverages and compromises with the existing Web2 securities compliance framework. The Tokenized model pushes the boundaries of RWA innovation within offshore jurisdictions. Synthetic derivatives purely digest risk within the crypto ecosystem. By preparing multiple channels, exchanges can flexibly adjust product focus based on different regional regulatory policies, diversifying policy risk.

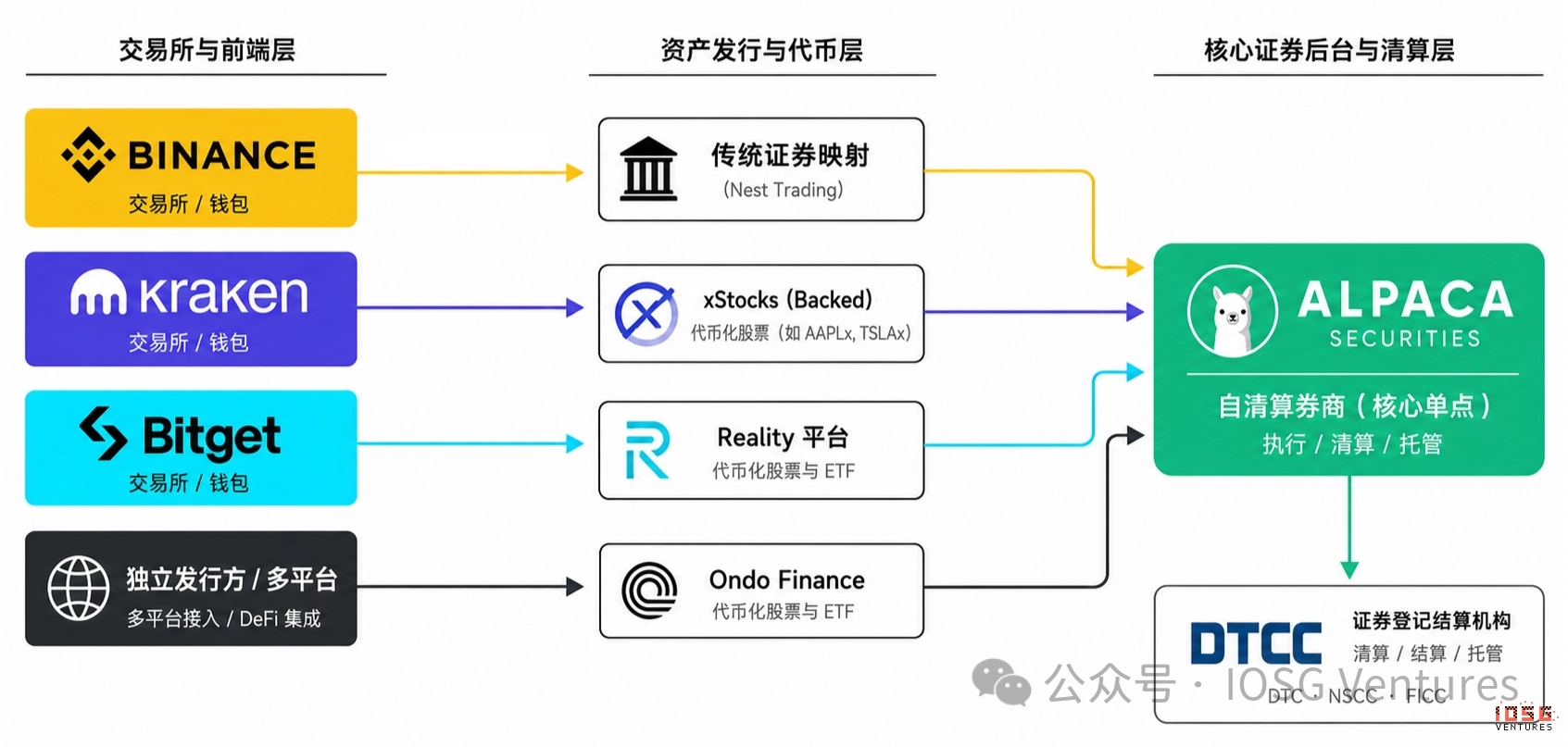

Architecture Layers: Rights Stripping Across a Five-Layer Pipeline

To understand the essence of equity dilution in on-chain US stocks, one must look away from the smooth front-end experience and audit the data pipeline downward. The difference stems not from the token's name or on-chain narrative, but from how many intermediary layers exist between the end-user and the ultimate underlying asset.

The traditional API model fully preserves shareholder rights because it follows a clean Web2 three-layer architecture:

User → Broker → Depository Trust & Clearing Corporation (DTCC)

In this pathway, the broker is merely a conduit holding assets on the user's behalf. The law provides direct ownership protection that extends to the end-user, ensuring their legal status as "Beneficial Owner."

However, to forcibly "move" stocks on-chain, the Tokenized model introduces multiple intermediary layers. It is forced into a complex five-layer structure:

[End User] ──> [Crypto Exchange] ──> [Token Issuer] ──> [Intermediary Broker (Alpaca)] ──> [DTCC]

This increase in layers is not a harmless engineering cost; it represents a significant loss of asset rights during transmission. Within this structure, each layer intercepts or distorts the legal rights originally belonging to the shareholder.

Idle and Evaporated Voting Rights

At the foundation of the traditional securities system, the underlying shares of all US stocks are registered under the DTCC's nominee, Cede & Co. Entities like Alpaca or Apex, as DTCC participants, are holders at the beneficial ownership level. This means corporate actions like shareholder meeting notices and voting guidelines are sent only to licensed brokers like Alpaca at the terminal end of the traditional clearing network.

When the architecture extends to five layers, the transmission chain of rights breaks down. Alpaca, as a standard broker, has legal obligations and system interfaces only for its direct clients – the token issuers like Backed Finance or Ondo. Alpaca has no legal obligation to develop a complex voting rights penetration system for these crypto entities.

The issuer layer faces a similar technological and compliance vacuum. They lack the infrastructure to map the daily voting decisions of potentially millions of underlying shares to on-chain token holders in real-time and securely. Consequently, voting rights stop transmitting at the bridge broker layer, become idle, and ultimately evaporate at the issuer layer.

Dividend Redistribution and Contractualization

Unlike the complete disappearance of voting rights, dividends – the most attractive economic right – transform into an indirect, repackaged distribution mechanism within the complex five-layer architecture.

When Apple or Nvidia pays a cash dividend, the dollars first flow into Alpaca's account. After deducting applicable taxes and fees, Alpaca remits the funds to the account's nominal owner – the token issuer. From this point, the funds leave the jurisdiction of securities law and become the issuer's corporate assets. Whether on-chain token holders receive money, and in what form, depends entirely on the contractual agreements and operational processes defined by the issuer in its offshore jurisdiction.

In practice, to avoid the complex cross-border clearing and securities regulatory risks associated with directly distributing dollars, mainstream projects like xStocks and Ondo commonly employ an "automatic reinvestment" mechanism. Upon receiving cash dividends off-chain, they automatically reinvest in more underlying shares in the secondary market. Then, by adjusting the multiplier in the on-chain smart contract or the Net Asset Value (NAV) price of the token, they reflect this benefit non-intuitively in the user's token balance or token price.

Currently, only a very few platforms like Bitget Reality attempt to distribute dividends directly on-chain in the form of USDT. However, both models are fundamentally not the shareholder dividend granted by securities law. Instead, they represent a contractual right between the user and the offshore token issuer, dependent on the proper functioning of the issuer's technical nodes.

SIPC Protection Void

The most critical hidden danger in the five-layer architecture is the legal vacuum during extreme risk events. In the traditional US securities market, the SIPC provides brokerage clients with up to $500,000 in bankruptcy protection, forming the trust bedrock for retail investors to entrust assets to new brokers.

However, under the Tokenized model, the direct client on Alpaca's books is the SPV registered in the Cayman Islands or Seychelles by Backed, Ondo, or Bitget, not each specific user on-chain. This means SIPC's protection network only extends to the "token issuer" layer.

If Alpaca itself faces a clearing crisis, the issuer might file a claim with SIPC as a client. However, if the token issuer itself goes bankrupt, absconds, or is hacked, the traditional securities law umbrella becomes completely ineffective. No clear legal precedent exists in current bankruptcy or securities law to "pierce" SIPC protection to benefit an on-chain holder who holds a Solana SPL token on one hand but has no record in the securities system on the other.

This harsh legal reality is frankly disclosed in the official compliance documents of major issuers. Ondo Finance's legal terms explicitly state: The token provides economic exposure to the performance of the underlying asset; holders do not have the right to hold or receive the underlying asset.

This clearly defines the ultimate physical reality of on-chain US stocks: You are not the owner of the stock. You are the holder of a digital IOU, issued by some offshore entity, that tracks the price of the US stock.

Potential Risks Under SEC Compliance Regulation

Under the multi-layered five-tier architecture, risk events do not follow the traditional securities law compensation path. Instead, they are directly subject to the compliance game between the offshore SPV and the upstream clearing broker. When regulators like the SEC conduct penetrating enforcement against cross-border securities tokenization, the potential default and risk transmission path typically presents three distinct stages:

First, the upstream licensed self-clearing broker, to mitigate compliance reputation risk, typically chooses to cut the API routing to the offshore SPV. With the offshore issuer losing its actual clearing and settlement channels off-chain, its on-chain smart contracts are forced to halt all minting and redemption functions.

Second, because anonymous on-chain addresses lack compliant ownership records within the traditional settlement system (DTCC), SIPC's bankruptcy protection umbrella stops completely at the issuer entity level, unable to "pierce" down to the terminal holder. If the issuer goes bankrupt, users holding the tokens face the risk of default, unable to recover the underlying assets.

Facing this legal gap, the current path for on-chain US stock tokenized spots is gradually evolving towards a contractual trust model. Platforms like Ondo Finance are moving away from the simple SPV mapping model towards embracing a more structurally sound off-chain compliant trust fund architecture. They legalize dividend and liquidation rights through contractual arrangements. This design, while unable to bypass regulatory friction, maximizes the retention of legal claims for holders within traditional financial courts, representing the current best solution for this model against the legal vacuum.

The On-Chain Financial Clearing Giant: Alpaca's Single-Point Monopoly and Liquidity Gap

Scrutinizing the pipelines of all current Tokenized US stocks and traditional API trading products reveals a startling fact: almost the entire crypto industry's underground network for accessing US stocks converges at a single point at the most critical execution and custody layer – Alpaca.

Whether it's on-chain RWA focused platforms like Ondo Finance, Backed Finance (xStocks), exchange-backed offerings like Bitget Reality, or even Binance's traditional US stock trading launched in June, the underlying asset purchase, clearing, and securities custody are solely handled by Alpaca. According to an official announcement from Alpaca on December 4, 2025, Alpaca effectively monopolizes over 94% of the clearing and custody market share for tokenized US stocks and ETFs (Source: Alpaca Official).

Why Alpaca: Self-Clearing Qualification vs. Traditional Broker's "Risk Aversion"

This highly concentrated single-point monopoly is not because Alpaca provides irreplaceable cutting-edge Web3 technology, but is dictated by the extreme scarcity of the traditional financial supply side and the innate compliance gap.

Within the US securities system, brokers have strict tiers. One category is the large number of Introducing Brokers, which can only take orders and must outsource clearing, settlement, and custody to third parties. The other is the rare Self-Clearing Brokers. Alpaca belongs to the latter. It is a formal member of DTCC, OCC, and FICC, capable of independently completing the entire chain from order execution to final asset registration. For crypto asset issuers, connecting to Alpaca means they don't need to separately interface with multiple execution, clearing, and custody institutions; one broker provides the full chain service.

Alpaca's core moat lies in the unwillingness of other traditional large licensed institutions to partner with offshore crypto exchanges due to compliance and reputation risks. Giants like Interactive Brokers, with multi-billion-dollar market caps and high reputational costs, are reluctant to risk regulatory backlash for minor API access fees by partnering with exchanges registered in offshore tax havens. Vertically focused giants like DriveWealth are already profitable in the Web2 traffic pool (e.g., Revolut, Cash App) and lack the incentive to cross over into this risky territory.

For a long time, Alpaca was virtually the only licensed broker willing to serve crypto tokenization companies while possessing self-clearing capabilities and an open API architecture. For token issuers, Alpaca provides not only the transaction execution, clearing, and custody needed from a traditional broker but also reduces the conversion cost between securities assets and on-chain tokens through standardized APIs and the Instant Tokenization Network (ITN).

The Illusion of Efficiency: The "Asymmetric Risk of Time Lag" between On-Chain Real-Time Minting and Off-Chain T+1

To solidify its infrastructure position, Alpaca