Gate Research: Tổng vốn hóa thị trường của ba "ông lớn" lưu trữ cùng vượt 1 nghìn tỷ USD

- Quan điểm chính: Việc vốn hóa thị trường của Micron Technology vượt mốc 1 nghìn tỷ USD đánh dấu sự chuyển đổi của ngành lưu trữ từ một ngành công nghiệp chu kỳ truyền thống thành nguồn tài nguyên chiến lược quan trọng cho sức mạnh tính toán AI. Sự tăng trưởng này được thúc đẩy bởi sự định giá lại mang tính cấu trúc từ các sản phẩm cao cấp như HBM và các thỏa thuận cung cấp dài hạn (LTA), thay vì chỉ đơn thuần là sự phục hồi theo chu kỳ.

- Các yếu tố then chốt:

- Vốn hóa thị trường của Micron là khoảng 1,17 nghìn tỷ USD, với giá cổ phiếu tăng hơn 800% trong năm qua, chủ yếu nhờ nhu cầu liên tục từ máy chủ AI và trung tâm dữ liệu đối với các bộ nhớ cao cấp như HBM và DDR5.

- Doanh thu quý 2 năm tài chính 2026 đạt mức kỷ lục: 23,86 tỷ USD, biên lợi nhuận gộp Non-GAAP tăng vọt lên 74,9%, động lực cốt lõi đến từ mảng kinh doanh trung tâm dữ liệu AI, với tổng doanh thu vượt 13,4 tỷ USD.

- Nâng cấp cấu trúc sản phẩm là chìa khóa: Các sản phẩm cao cấp như HBM có khả năng định giá mạnh hơn, với giá bán trung bình (ASP) dự kiến sẽ tăng khoảng 50% so với cùng kỳ, thúc đẩy biên lợi nhuận và sự ổn định lợi nhuận vượt xa chu kỳ DRAM truyền thống.

- Các thỏa thuận cung cấp dài hạn (LTA) đang thay đổi mô hình kinh doanh: Các LTA mới không chỉ cam kết khối lượng mua hàng mà còn cố định một phần giá cả (với thời hạn 3-5 năm), cải thiện khả năng hiển thị doanh thu và khả năng sinh lời xuyên suốt chu kỳ.

- Nguồn cung ngành tiếp tục thắt chặt: DRAM và NAND được dự báo sẽ ở tình trạng thiếu hụt cung ứng cho đến quý 2 năm 2028 và quý 4 năm 2027. Công suất HBM bị hạn chế bởi quy trình sản xuất và tỷ lệ đạt yêu cầu, việc giải phóng nguồn cung diễn ra chậm, hỗ trợ cho sự co giãn giá cả.

- Nền tảng Gate đã ra mắt các dịch vụ giao dịch liên quan: Người dùng có thể giao dịch cổ phiếu Mỹ giao ngay như Micron, hợp đồng vĩnh viễn và ETF đòn bẩy bằng USDT, cho phép quản lý tập trung tài sản kỹ thuật số và cổ phiếu.

Abstract

- The total market capitalization of the global storage sector has experienced explosive growth, with the three giants Samsung Electronics, SK Hynix, and Micron Technology all surpassing the trillion-dollar mark.

- The continuous growth in demand for AI large model training and inference is significantly increasing data centers' demand intensity and value for storage products such as High Bandwidth Memory (HBM), DDR5, and enterprise SSDs.

- Micron Technology has recently officially entered the trillion-dollar market cap club, becoming one of the most closely watched revaluation targets in the AI storage industry chain. According to StockAnalysis data, as of June 3, 2026, Micron's market cap stood at approximately $1.17 trillion.

- The core driver of the current storage sector rally is not the typical cyclical rebound in traditional DRAM but rather the market beginning to reprice the structural value within AI servers, High Bandwidth Memory (HBM), Long-Term Agreements (LTAs), and the tight supply-demand dynamics in the storage industry.

- Gate has officially launched stock trading, allowing users to trade stocks and ETFs from mainstream securities markets directly on the platform using USDT. The stock derivatives zone now offers perpetual contracts, supporting USDT settlement and 1-20x leverage for two-way trading. Gate has also introduced leveraged ETF tokens, providing investors with long exposure to stocks.

- Micron's trillion-dollar market cap is not merely the result of a single earnings cycle but reflects the combined effects of the AI storage value revaluation, HBM product upgrades, long-term agreement mechanisms, and improved industry supply-demand dynamics.

The AI-Driven Storage Sector

In the past, the storage industry was often viewed as a typical strongly cyclical sector, with corporate profits highly dependent on supply-demand fluctuations and price elasticity. However, in the AI era, storage is evolving from a supporting component in general-purpose hardware into a critical resource within computing infrastructure.

Large model training and inference not only require more powerful GPUs and interconnect capabilities but also demand storage systems with higher bandwidth, larger capacity, and lower latency. Whether it's HBM on the GPU side or DDR5 and enterprise SSDs on the server side, their importance is markedly increasing. For cloud vendors and data center clients, storage is no longer just a cost item; it is a key variable affecting model training efficiency, inference throughput, and overall deployment costs.

The changes brought about by the expansion of AI applications are not merely an increase in storage chip shipments; more importantly, there is a rising proportion of high-end products. Compared to standard DRAM, HBM offers higher bandwidth, greater integration, and higher added value; enterprise SSDs also benefit from increased data center workloads.

Unlike the historical logic of "raising prices and expanding production", the supply release speed for high-end storage products like HBM is relatively limited due to manufacturing processes, yield rates, advanced packaging, and customer qualification cycles. Concurrently, core clients increasingly prefer to lock in capacity and partial pricing through long-term supply agreements. This gives leading manufacturers greater revenue visibility and stronger bargaining power than in the past, imbuing the current boom cycle with distinct structural characteristics.

Micron Technology, Inc. (NASDAQ: MU), founded in 1978 and headquartered in Boise, Idaho, USA, is a globally leading provider of semiconductor memory and storage solutions. The company designs, manufactures, and sells DRAM, NAND Flash, NOR Flash, HBM, SSDs, and storage products for data centers, mobile devices, automobiles, industrial, and consumer electronics. Using Micron as a case study is not to focus the article on a single stock, but because Micron relatively typically reflects the evolutionary direction of the AI storage track in terms of its product portfolio, customer structure, earnings elasticity, and market pricing.

Micron Technology

In the global memory chip industry, Micron, along with Samsung Electronics and SK Hynix, is a major DRAM supplier and a significant player in the global NAND market. With the continuous growth in demand for large model training and inference, the demand from AI servers for high-bandwidth memory (HBM), high-capacity DDR5, and enterprise SSDs is rapidly increasing. Memory chips are no longer just supporting components in general-purpose computing devices but are gradually becoming one of the key bottlenecks in AI computing infrastructure. Especially in GPU clusters, the bandwidth, capacity, and power consumption of HBM directly impact the performance of AI chips. Consequently, Micron has been re-evaluated and included as a core supplier in the AI semiconductor supply chain. This report views Micron Technology as a key representative enterprise in the AI storage industry chain, analyzing its trillion-dollar market cap breakthrough, long-term agreements, HBM growth, valuation restructuring, and related stock trading support on Gate.

Fundamental Analysis and Investment Thesis

According to Gate market data, as of June 3, 2026, Micron Technology's stock price was $1,056. Based on approximately 1.1 billion fully diluted shares, the company's total market capitalization is about $1.17 trillion. Over the past year, Micron Technology (MU) has exhibited an overall trend of oscillatory rise, culminating in an accelerated breakout. The stock price started from around $110, initially strengthening alongside expectations for AI storage demand, steadily rising to above $400. After a phase of consolidation, it entered a major uptrend driven by the explosion in HBM and AI data center demand. From May to June, it experienced continuous sharp gains, hitting a high of $1,076, representing a cumulative increase of over 8x from its low point a year prior. Over the past year, Micron's stock price rose from approximately $110 to around $1,056, a cumulative increase of over 800%, while the company's market cap simultaneously broke through the $1 trillion mark, reflecting the market's continuous revaluation of AI storage demand and HBM business prospects.

From a business structure perspective, Micron currently focuses on four main application areas: first, data centers and cloud computing, including AI servers, enterprise servers, and networking equipment; second, mobile devices, including smartphones and tablets; third, storage, including enterprise and client SSDs; and fourth, embedded applications, including automotive, industrial, and consumer electronics. As AI data center capital expenditure continues to expand, data center-related storage demand is becoming Micron's fastest-growing and highest profit-margin business direction.

Micron's recent breakthrough to a trillion-dollar market cap is not simply a rebound from the traditional storage cycle but stems from the market's re-pricing of its strategic value within the AI infrastructure supply chain. Earnings for FY2026 Q2 showed record revenue, gross margin, EPS, and free cash flow, validating the profit inflection point driven by AI demand, tight industry supply, and high-end storage product upgrades.

The AI Era: Storage Evolves from Supporting Component to Strategic Asset

In traditional computing architectures, memory chips are often seen as supporting components next to CPUs and GPUs, with industry pricing primarily influenced by cyclical supply and demand. However, in the AI era, especially with the continuous expansion of large model training and inference scales, memory bandwidth, capacity, and energy efficiency have become key bottlenecks in unlocking AI system performance.

In its FY2026 Q2 earnings announcement, Micron explicitly stated that the record Q2 performance reflects "the strategic value of storage in the AI era." CEO Sanjay Mehrotra stated that in the AI era, storage has become a strategic asset for customers. This indicates that Micron's management has repositioned the company from a traditional storage vendor to a core participant in the AI computing infrastructure.

The rapid growth in demand for HBM, high-capacity DRAM, DDR5, and enterprise SSDs from AI servers has significantly increased the value of storage products in server BOMs. As GPU clusters scale up, customers are not only concerned with chip computing power but also increasingly with stable storage supply, matching performance, and controllable deployment costs. This change provides Micron with stronger bargaining power and higher earnings elasticity.

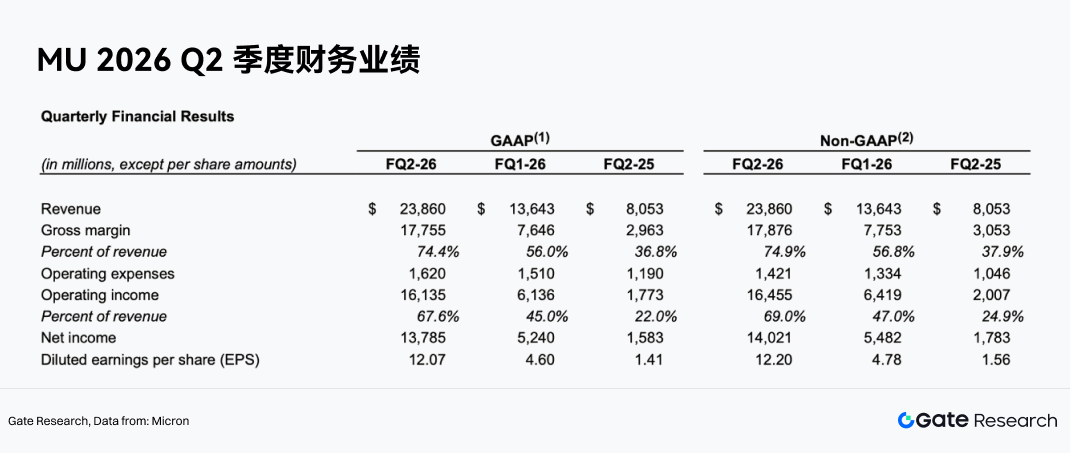

FY2026 Q2 Results Validate Demand Strength

Micron's FY2026 Q2 revenue reached $23.86 billion, a significant increase from $13.64 billion in the previous quarter and sharply higher than $8.05 billion in the same period last year. The company's Non-GAAP net profit was $14.02 billion, Non-GAAP EPS was $12.20, operating cash flow was $11.90 billion, and adjusted free cash flow was $6.90 billion.

More critically, earnings quality also improved. FY2026 Q2 Non-GAAP gross margin reached 74.9%, significantly up from 56.8% in the previous quarter and 37.9% in the same period last year; Non-GAAP operating margin reached 69.0%, a substantial expansion from 47.0% in the previous quarter and 24.9% a year ago.

This indicates that Micron is not solely reliant on revenue growth to drive profits but has achieved a leap in profit margins through joint improvements in product pricing, product mix, and cost efficiency. For a memory company, a gross margin increase from the 30-40% range to over 70% signifies a profound shift in the industry's supply-demand dynamics and the company's product portfolio.

Data Center and Cloud Business Become Growth Core

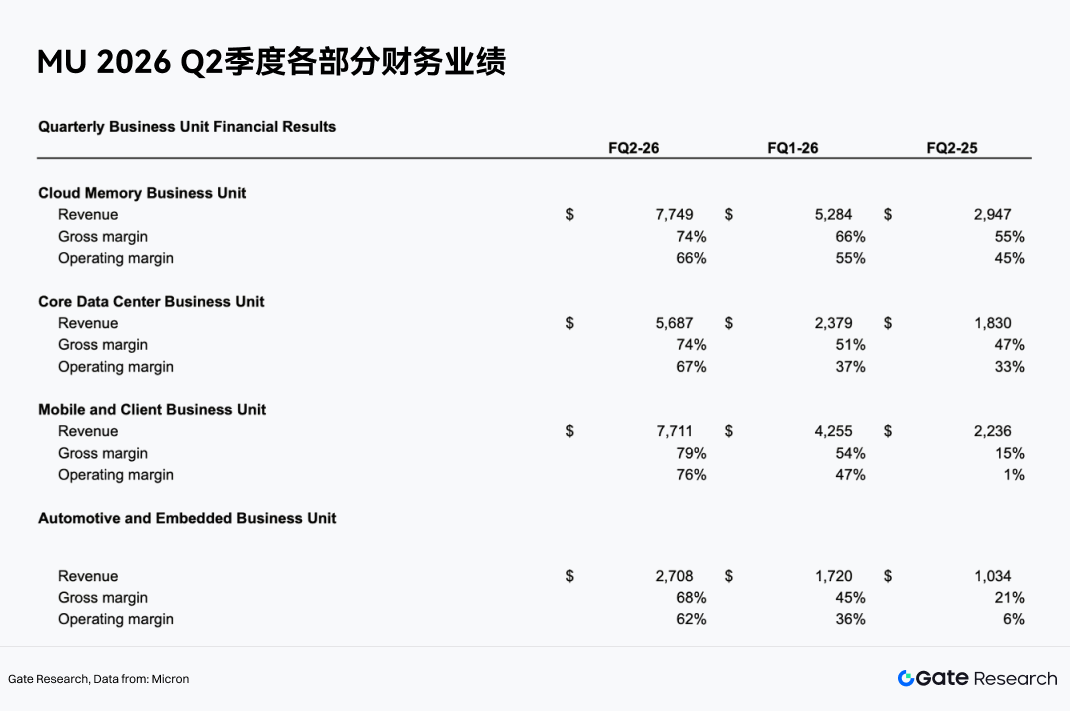

In terms of business segments, Micron's FY2026 Q2 growth was highly concentrated in AI and data center-related areas.

The Cloud Memory Business Unit generated revenue of $7.749 billion, with a gross margin of 74% and an operating margin of 66%. The Core Data Center Business Unit generated revenue of $5.687 billion, with a gross margin of 74% and an operating margin of 67%. Combined, these two businesses generated over $13.4 billion in revenue, establishing them as the company's most important growth engines.

This shows that Micron's business focus is shifting from traditional consumer electronics cycles like PCs and phones towards cloud computing, AI servers, and data centers. Compared to consumer electronics, AI data center clients typically have large capex budgets, demanding product performance requirements, and a strong need for supply continuity. This environment is more conducive to creating premiums for high-end products and fostering long-term supply relationships.

HBM and High-End DRAM Drive Product Mix Upgrade

The product area where Micron benefits most significantly is HBM and high-end DRAM. HBM is a key memory product for AI GPUs and accelerators, characterized by high bandwidth, high capacity, and high energy efficiency, fetching higher prices per GB and gross margins than standard DRAM.

UBS estimates that Micron's HBM ASP will grow approximately 50% year-over-year in 2027, driving continuous expansion in HBM revenue. As AI chip platforms evolve, demands for HBM capacity and bandwidth increase, allowing Micron to capture a higher revenue share through HBM3E, subsequent HBM products, and advanced packaging capabilities.

The significance of the product mix upgrade is that Micron is no longer just following the average DRAM price fluctuations in the industry but is gaining stronger pricing power through high-end products. As the proportion of HBM increases, the company's overall gross margins and earnings stability are expected to improve.

Industry Supply Constraints Enhance Price Elasticity

Micron's strong performance in FY2026 Q2 also stems from tight industry supply. The results were driven by a robust demand environment, constrained industry supply, and the company's execution. Some institutions expect the DRAM supply shortage to persist until at least Q2 2028, while the NAND supply shortage is expected to continue until Q4 2027. In this supply-constrained environment, DRAM and NAND prices have sustained support, allowing Micron's revenue and profit margins to remain at high levels.

More importantly, this cycle differs from the past. Previously, memory manufacturers would often rapidly expand production after price increases, eventually leading to oversupply and price declines. However, the demand for high-end memory from AI servers is growing relatively quickly, and HBM capacity expansion is constrained by technology, yields, advanced packaging, and customer qualification cycles. Therefore, supply release cannot easily catch up with demand.

Long-Term Agreements (LTAs) Enhance Earnings Visibility

LTA stands for Long-Term Agreement. In the semiconductor memory industry, an LTA typically refers to a supplier and a core customer agreeing in advance on supply arrangements for a future period, including purchase quantities, delivery schedules, product specifications, and, in some cases, a pricing framework. In the past, procurement agreements in the memory industry were more often "volume-locked but not price-locked." Customers would commit to a certain purchase volume upfront, giving suppliers some demand visibility, but prices would still fluctuate rapidly with DRAM and NAND market supply and demand. Therefore, during industry downturns, significant price drops would directly hit the revenue and profits of memory manufacturers like Micron, Samsung, and SK Hynix.

LTAs represent another key logic behind Micron's valuation revaluation. The new type of LTA not only locks in purchase volumes but also partially locks in prices for terms lasting 3-5 years. This differs from the past volume-only procurement agreements. For Micron, the value of LTAs lies in improving revenue visibility, reducing price volatility, and enhancing cross-cycle profitability. For cloud vendors and AI customers, LTAs can secure future memory supply and partially lock in costs, avoiding being forced to accept higher prices during supply crunches. If LTAs are widely adopted, Micron's business model could gradually shift from a traditional cyclical commodity company to a semiconductor supplier characterized by long-term orders, stable cash flows, and higher customer stickiness.

Earnings and Cash Flow Support Valuation Restructuring

Micron's adjusted free cash flow for FY2026 Q2 reached $6.9 billion, and the board of directors approved a 30% increase in the quarterly dividend. This indicates that not only have profits significantly improved, but cash flow quality has also markedly strengthened. In capital markets, stable and high free cash flow typically supports higher valuations. Micron's valuation was low in the past mainly due to market concerns about the sustainability of its earnings. Now, if AI demand, LTAs, and HBM product mix upgrades collectively reduce cyclical volatility, Micron has the potential to transition from a traditional cyclical memory stock valuation towards a core AI semiconductor asset valuation.

Gate Stock Investment Products

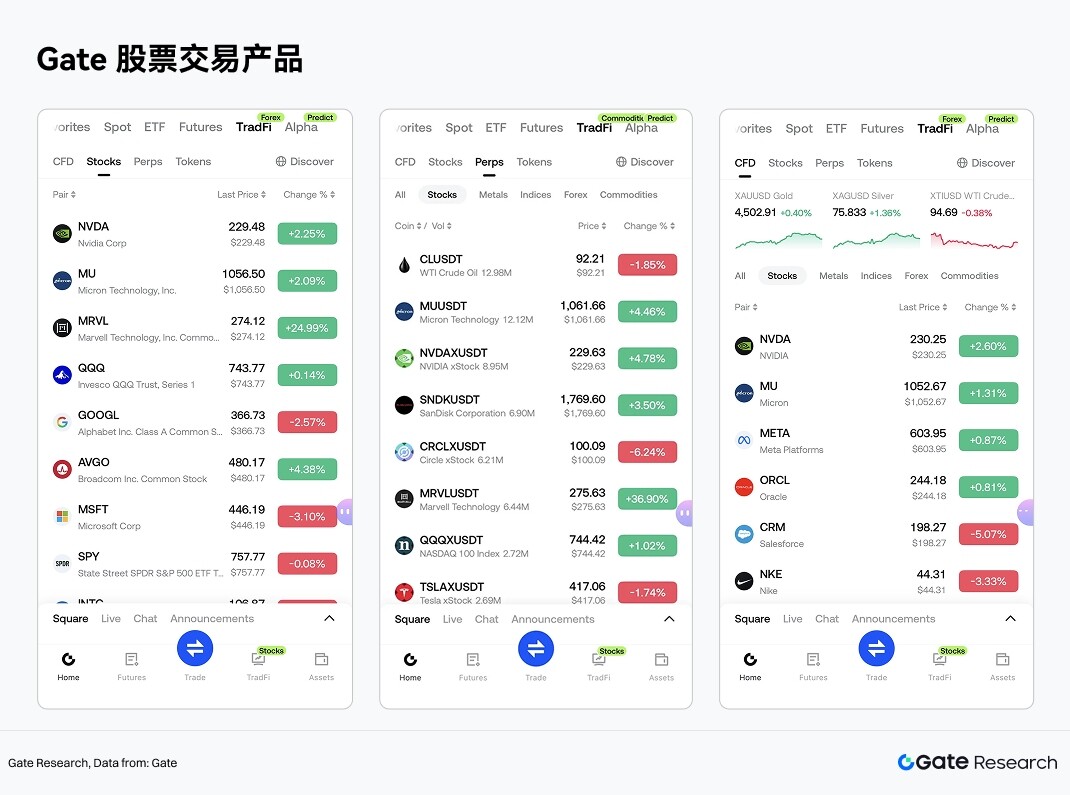

The storage sector features one of the most closely watched US stock targets. Gate has also supported related US stock trading services within its TradFi segment. Users can trade stocks and ETFs from mainstream securities markets using USDT through a unified account system.

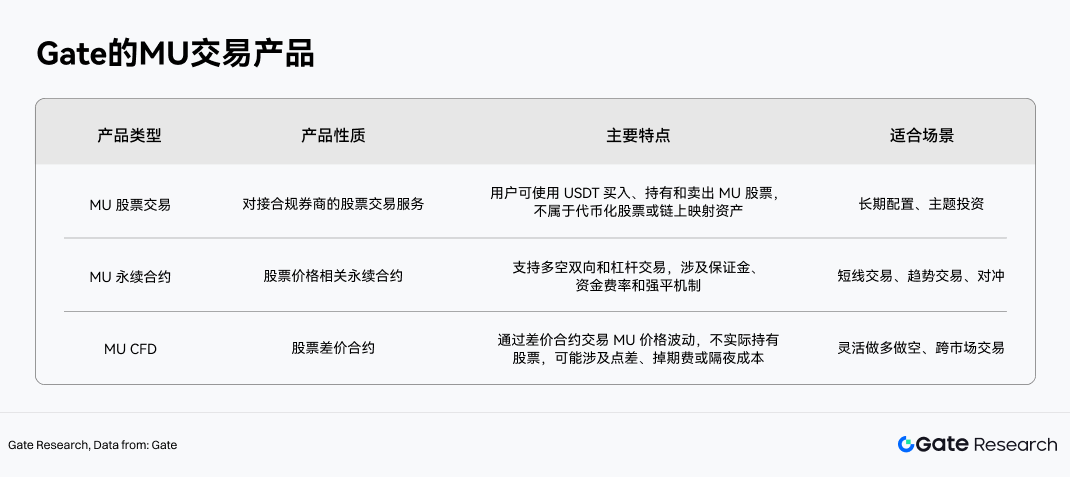

Unlike common market models involving stock tokenization or RWA mapping, Gate's stock service emphasizes market access capabilities and a compliant trading framework. Gate Stock connects with licensed brokers to provide users with stock and ETF trading services; it does not involve on-chain mapped assets or tokenized stock derivatives. Users can buy, hold, and sell stock assets through their Gate accounts, with related holdings, P&L, fund flows, and corporate action information viewable and manageable within the account.

Regarding asset coverage, Gate Stock currently supports over 10,000 stocks and ETFs, covering major securities trading markets and liquidity networks such as NYSE, Nasdaq, NYSE Arca, NYSE American, and BATS. Gate Stock currently supports intraday trading, with plans to gradually expand to 24/7 trading, offering global users more flexible access to US stock asset allocation.

In terms of product structure, the stock-related trading tools within Gate TradFi can be categorized into three types, using MU trading products as an example:

Among these, Gate's spot stock trading operates independently from the traditional CFD system. Stock trading does not involve the funding rates associated with perpetual contracts, nor does it incur holding costs like swap fees or overnight fees found in CFD products. This makes it more suitable for users aiming for long-term allocation in US stocks. In contrast, perpetual contracts and CFDs are more suited as trading tools for directional trading or risk management based on short-to-medium-term price fluctuations of stocks like Micron.

Leveraging a unified crypto asset account system, Gate further bridges digital asset trading with stock investment scenarios. After completing KYC and meeting regional access requirements, users can enter the stock section via the TradFi module on the Gate App to view quotes and participate in trading after transferring stablecoins through the trading page or asset page. This means the application scenario for USDT is extending from crypto asset trading to global stock asset allocation.

From an industry trend perspective, Gate's launch of stock trading services provides users with a unified trading entry point for digital assets and traditional financial assets. For users focused on the AI semiconductor theme, the availability of real stocks, perpetual contracts, and CFDs allows them to engage in more flexible asset allocation and trading management related to storage, AI, HBM, and semiconductor cycles within a single platform.

Risk Warning

From a sector research perspective, future judgments on the storage industry's health and company quality can focus on four key dimensions: First, whether AI server and cloud vendor capital expenditure continues to expand; second, changes in the penetration rate and ASP of high-end categories like HBM, DDR5, and enterprise SSDs; third, the supply discipline and expansion pace of leading manufacturers like Samsung, SK Hynix, and Micron; and fourth, whether LTAs, customer qualifications, and advanced packaging capabilities continue to strengthen industry barriers.

This implies that the storage sector can no longer be fully understood using the old framework of a pure "cyclical price stock." For researchers, a more appropriate analytical approach is to view it as a semiconductor sub-sector where "cyclical attributes persist, but the weight of structural upgrades is continuously increasing." Micron's case provides a highly identifiable sample