Gate Institutional Weekly: WTI Crude Falls Below $70, LST Sector Retraces Again

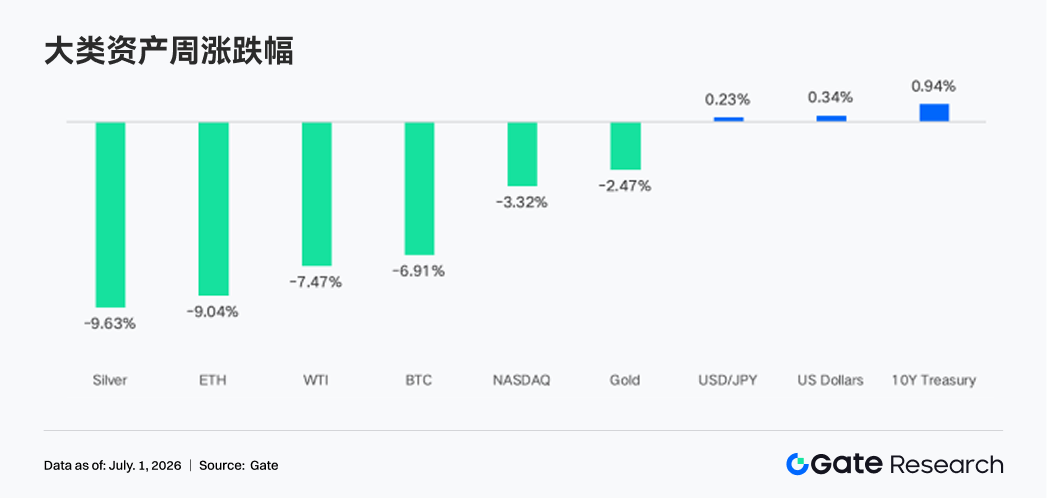

- Core Viewpoint: Last week (June 22-28, 2026), the market's trading logic shifted from a geopolitical "war premium" to the Federal Reserve maintaining higher interest rates for a longer period, compounded by persistent inflation. This put pressure on both US stocks and crypto assets, with BTC falling approximately 6.9%, ETH dropping about 9%, significant net outflows of ETF capital, and on-chain capital tending towards defensive and high-turnover scenarios.

- Key Elements:

- Macro Background Shift: The easing of the Middle East situation pushed oil prices down, but the May core PCE reached 3.4%, above target, leading the market to maintain the "higher rates for longer" judgment. The NASDAQ fell 3.3%, with BTC and ETH following suit and weakening.

- Significant ETF Capital Outflows: BTC spot ETFs saw net outflows of approximately $1.787 billion, and ETH spot ETFs saw net outflows of about $274 million. BlackRock's IBIT and ETHA were the largest sources of outflows, indicating institutional position reduction for defense.

- Divergence in On-chain Capital Flows: PumpSwap became the biggest incremental gainer among DEXs, reflecting Solana ecosystem capital shifting from traditional DEXs towards issuance and high-frequency trading. Meanwhile, DeFi liquidity (stablecoins, LSTs, lending markets) maintained an overall defensive posture.

- Derivatives Market Changes: BTC prices fell near the $60,000 mark, but OI did not expand and funding rates remained positive, indicating a low-leverage adjustment. In the options market, the 25D Skew weakened, and DVOL rose to 47-48, reflecting the market repricing downside risks.

- Sustained Growth in TradFi Business: Gate Institutional's contract trading volume grew 15% WoW, CrossEx's monthly trading volume increased 10% MoM to an all-time high, and AI customer service resolution accuracy surpassed 85%, indicating robust institutional service demand.

Summary

• The easing of tensions in the Middle East has driven down crude oil prices, shifting the market's trading logic from "war premium" to "the Fed maintaining high interest rates for longer." The NASDAQ fell approximately 3.3%, while BTC and ETH dropped around 6.9% and 9%, respectively.

• Spot ETFs for BTC and ETH saw significant net outflows, with BlackRock's IBIT and ETHA being the largest sources of outflows. As geopolitical risks cool and AI tech stock volatility increases, TradFi Perp's stock trading share rose to 55%–60%, as capital refocused on US equity risk trading.

• On-chain capital continues to concentrate in high-turnover trading scenarios, with PumpSwap being the largest incremental gainer this week, reflecting a migration of Solana ecosystem capital from traditional DEXs towards issuance and high-frequency trading environments.

• DeFi liquidity maintains a defensive posture, with stablecoins, LSTs, and the lending market generally cautious. Aave's lending scale contracted slightly, interest rates remained low, capital continued to concentrate in the Ethereum main market, and overall risk appetite has yet to recover significantly.

• BTC's price fell back to around $60,000, but without a significant expansion in OI. Funding rates remained positive, suggesting this adjustment was primarily driven by spot and existing position adjustments, maintaining a low-leverage environment for BTC derivatives overall.

• Monthly options trading volume surged significantly before expiry. The 25D Skew continued to weaken, and DVOL rose to approximately 47–48, reflecting the market's repricing of downside risk.

• Gate's institutional business saw a 15% week-over-week increase in contract trading volume. CrossEx's weekly trading volume grew 6% WoW, and its June monthly volume increased 10% MoM, continuously hitting new all-time highs. The AI customer service chatbot has been upgraded further, with an accuracy rate exceeding 85% for basic issue resolution.

1. Market Focus Analysis

Last week (June 22-28, 2026), the global macro narrative focused on three points: the cooling of geopolitical risks in the Middle East, persistent US inflation, and a maintained hawkish Fed policy stance. Firstly, after the temporary easing of tensions between the US and Iran, the market quickly lowered its concerns about a supply disruption through the Strait of Hormuz, leading to a significant unwinding of the war premium in oil prices. Brent crude briefly fell to around $73.83/barrel, and WTI dropped below $70/barrel. Falling oil prices reduced the risk of another uptick in energy inflation and also improved short-term consumer sentiment, with the University of Michigan's Consumer Sentiment Index for June rising by nearly 5 points from the previous month. Consequently, the market shifted from trading based on "geopolitical shocks / rising oil prices / accelerating inflation" to assessing whether inflation will continue to cool down following the moderation in energy prices.

However, US inflation data does not support a rapid pivot to accommodative policy by the Fed. The May PCE rose 4.1% year-over-year, and core PCE was 3.4% YoY, still significantly above the Fed's 2% target. However, the month-over-month PCE figure was 0.4%, below the market expectation of 0.5%, preventing a further sell-off in the bond market. This combination implies that inflationary pressures persist, particularly with strong stickiness in core service and wage-related prices, but there hasn't been a more severe upward spiral in the short term. The market consequently maintained its "higher rates for longer" assessment while reducing concerns about more aggressive rate hikes. US Treasury yields fell over the week, with the 10-year yield dropping to around 4.37% and the 2-year yield to about 4.09%, reflecting lower oil prices dampening inflation expectations, though the policy rate path remains constrained by inflation.

Looking at macroeconomic transmission, geopolitical easing is positive for risk appetite and bonds, but sticky inflation limits the scope for asset valuation repairs. The US dollar and real interest rates continue to exert pressure on gold, tech stocks, and crypto assets. The NASDAQ fell by approximately 3.3%, while BTC and ETH declined by about 6.9% and 9%, respectively. Falling oil prices alleviate corporate cost pressures and household inflation expectations. Overall, last week wasn't purely a risk-off session, but rather a repricing process as the market transitioned from "war premium" to assessing "whether the Fed can maintain tightening amid high inflation."

2. Liquidity Analysis

2.1 Institutional Risk Appetite Cools in Sync, IBIT Sees $1.304 Billion Net Outflow

Both BTC and ETH ETFs experienced significant capital outflows last week, indicating a synchronized cooling of institutional risk appetite. BTC spot ETFs saw a total net outflow of approximately $1.787 billion, worsening from the previous week's net outflow of about $228 million. ETH spot ETFs recorded a net outflow of roughly $274 million during the same period, a significant expansion from the prior week's net outflow of about $10 million. At the product level, the BTC ETF with the largest inflow was the Grayscale Bitcoin Mini Trust BTC, at approximately $71.7 million. The largest outflow came from BlackRock's IBIT, at about $1.304 billion. For ETH ETFs, Bitwise's ETHW had the largest inflow, but only about $0.6 million. The largest outflow was from BlackRock's ETHA, amounting to roughly $236 million.

AUM direction on a WoW basis is likely negative. BTC's price fell by about 6.91% last week, and combined with large net ETF redemptions, its asset size suffered from both price retracement and share contraction. ETH's price dropped by about 9.04% last week, and with even weaker capital inflows into its ETFs, the pressure on its AUM was more pronounced. Overall, institutional sentiment has shifted from previous allocation or wait-and-see to a defensive posture and position reduction. Notably, BlackRock's products, which were the strongest capital magnets previously, became the main source of outflows, indicating that core institutional capital is reducing its beta exposure to crypto assets. Compared to BTC, ETH ETFs showed weaker new buying interest, suggesting a more significant contraction in institutional risk appetite for high-beta assets.

2.2 TradFi Liquidity

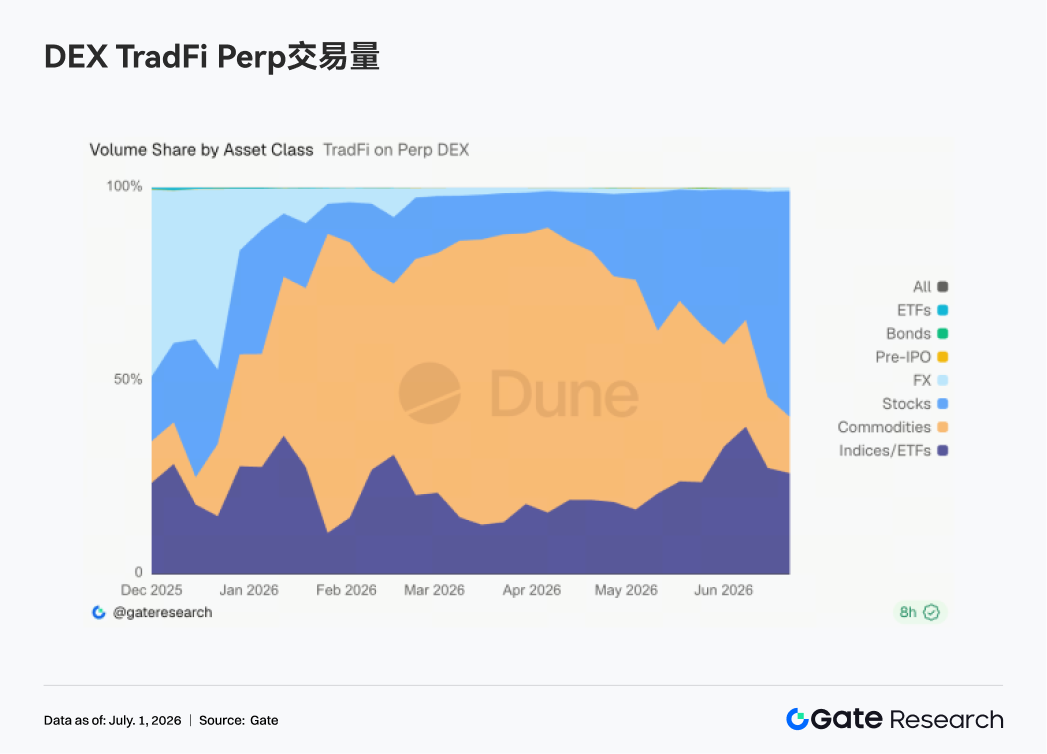

• TradFi Perp DEX: Over the past week, the trading volume structure on TradFi Perp DEX saw a clear shift, with equity assets regaining market dominance while the trading heat for commodity assets continued to cool. Since late June, the share of equity trading rapidly rose to around 55%–60%, becoming the largest trading category. Concurrently, the commodity share quickly dropped from a previous range of about 40%–50% to under 20%, indicating that the trading frenzy previously driven by safe-haven assets like gold and crude oil has significantly weakened. Meanwhile, the share of index/ETF trading remained stable around 25%–35%, continuing as an important allocation avenue, reflecting user participation in US stock market volatility through index products. This shift is closely related to the recent macro environment. The significant volatility in the US AI sector, the adjustment in tech stocks, and the market's repricing of the rate cut path have increased trading activity in equity and index perpetual contracts. Furthermore, continued interest in pre-IPO assets like SpaceX has further driven capital concentration towards the equity ecosystem. Overall, the capital focus on TradFi Perp DEX is shifting back from commodity trading to equity and index assets. The market's trading logic has transitioned from risk-averse trading driven by geopolitical risks to risk trading centered around US stock volatility, the tech sector, and macro events. Equity assets are expected to continue being the primary growth driver for the TradFi Perp market.

• Gate TradFi Perp Trading Volume: Despite the cautious macro environment, user demand for trading TradFi perpetual products remains strong. Over the past week, Gate's TradFi Perp trading volume saw a noticeable WoW increase, with daily turnover mainly concentrated in the $4 million to $6 million range. While overall volatility has moderated compared to previous weeks, trading activity has not significantly declined. By asset class, metals remain the absolute core source of trading volume, with precious metal perpetual contracts like gold contributing the majority of trades. This reflects that against the backdrop of the Fed's hawkish stance, recurring geopolitical risks, and high gold price volatility, safe-haven assets remain a key focus for market capital. Meanwhile, the share of index trading has increased significantly compared to earlier periods, with a notable volume surge early in the week. This indicates that as the AI sector adjusts, US stock volatility rises, and individual stock event-driven dynamics strengthen, user participation in US stock-related perpetual contracts continues to increase.

• Gate TradFi US Stock Asset Count: Gate officially launched its US stock trading service on June 2. Leveraging advantages such as real underlying asset backing, direct trading with USDT, no overnight holding fees, and high liquidity, this service has continuously attracted market attention since its launch, with trading volume growing steadily. Currently, Gate supports 7 major asset classes: ADRC, Stocks, ETFs, ETNs, ETSs, ETVs, and PFDs, and continues to expand product coverage. In terms of asset count, the total number of tradable instruments has doubled since launch. The stock category has seen the most significant growth, increasing its share of total assets from approximately 70% at launch to 85%, further enriching users' investment choices. Going forward, Gate will continue to pursue broader market access, global liquidity integration, and cross-market trading capabilities, continuously expanding its diversified asset coverage and further strengthening its strategic positioning as a global asset trading and market access platform.

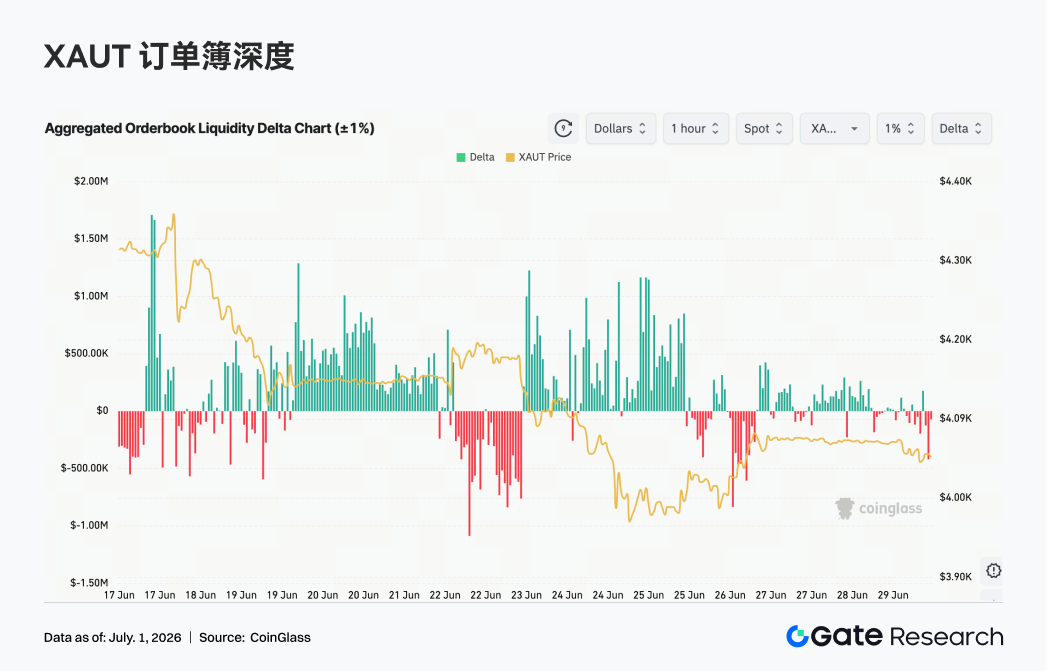

• TradFi Order Book Depth: We selected XAUT, the highest volume TradFi asset, to analyze its order book depth (Delta). Over the past week, XAUT's order book liquidity shifted from being dominated by longs in the early part of the period to being controlled by shorts, with the price exhibiting an overall volatile downward trend. Early in the week, Delta remained positive multiple times, with continuous buy-side liquidity inflow, pushing the XAUT price to oscillate in the $4,180–$4,330 range, indicating relatively strong market absorption capacity. After June 22, following changes in macro risk sentiment and a pullback in gold prices, the order book Delta quickly turned negative, consistently showing negative values ranging from $500,000 to $1 million. This pointed to a significant increase in active sell orders. The XAUT price concurrently broke below $4,100, briefly approaching the $4,000 level, reflecting a concentrated release of short-term selling pressure. Although there were periods of buy-side inflows over the weekend, the persistence of positive Delta weakened noticeably, and the market lacked sustained upward capital momentum. If the US dollar and Treasury yields continue to stay elevated, gold tokens might face continued pressure in the short term. However, if expectations for rate cuts revive or geopolitical risks flare up again, order book buy-side could strengthen, driving price recovery.

3. On-Chain Data Insights

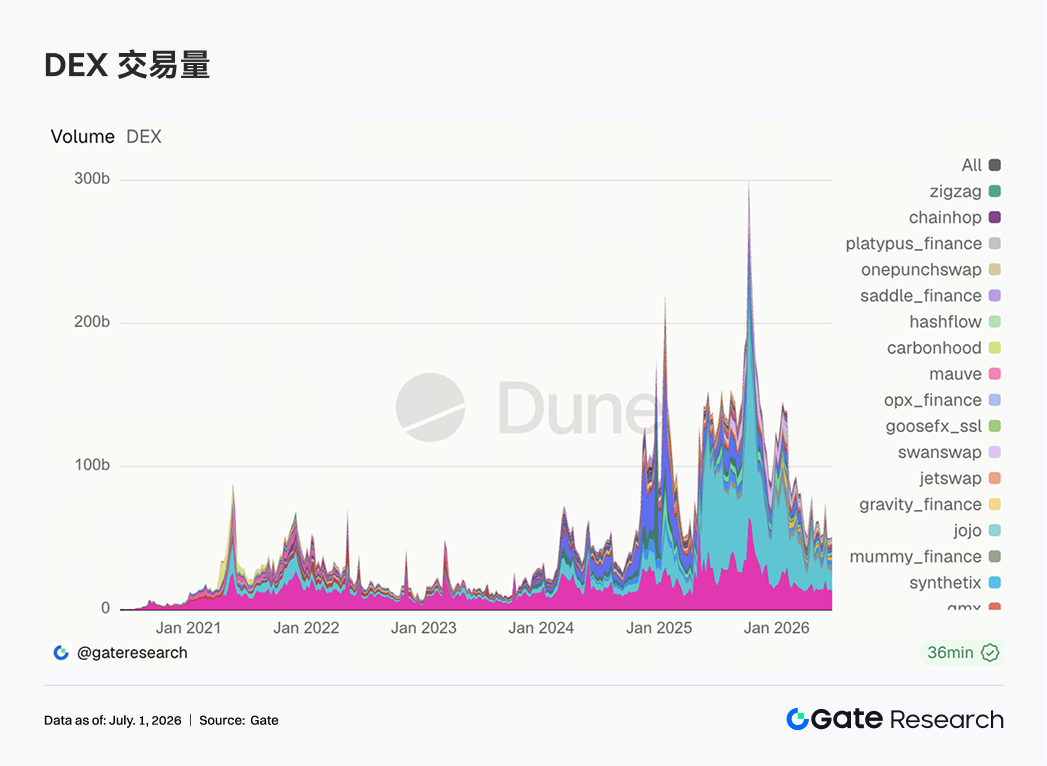

3.1 No Broad Expansion in DEX Volume; PumpSwap is the Most Prominent Structural Change This Week

DEX volume overall did not sustain the prior period's strong growth. Uniswap and PancakeSwap remain solidly in the top two positions, but their volumes slightly declined week-over-week, with top spot pools entering a consolidation phase at high levels. The change came from PumpSwap, whose volume and number of traders both stepped up significantly, propelling it directly into the top three. Speculative flow on Solana hasn't disappeared; it has shifted from traditional entry points like Raydium and Meteora towards issuance and high-frequency trading scenarios. Protocols like Aerodrome, Bisonfi, and Tessera also saw some recovery, with Base and emerging matching environments continuing to absorb active capital.

3.2 Stablecoin Supply Remains Defensive; Regulatory Disputes Impact Market Pricing More Than Short-Term Issuance

Stablecoins were generally contracting this week. Both USDT and USDC saw slight declines. USDS, USDe, USD1, and PYUSD did not show significant expansion. Only DAI performed relatively stronger. There was no massive influx of new on-chain dollar inflows; instead, existing capital migrated between different stablecoins. On the news front, on June 28, a US community banking organization publicly opposed stablecoin-related bills, with the core concern being that yield-bearing stablecoins would drain deposits from local banking systems. This elevated the stablecoin regulatory debate from a crypto industry issue to a traditional financial interest reallocation problem. The Bank of England also adjusted its stablecoin regulatory framework the same week, shifting from position limits to issuance scale restrictions, indicating that major jurisdictions are trying to balance innovation, payment efficiency, and banking system stability.

3.3 LST Sector Retreats Again; Market's Risk Discount on Staked Assets Widens

The LST sector reversed from last week's recovery into a broad decline. Protocols on the ETH side like Lido, Rocket Pool, and StakeWise faced pressure, and SOL-side protocols like Jito and Sanctum weakened in tandem. As TVL is denominated in USD, this pullback was significantly influenced by price volatility in ETH and SOL, but capital preferences were indeed more cautious. Following the KelpDAO/rsETH incident, institutions' risk assessment of staked assets has become stratified. Standard LSTs, re-staked assets, and cross-chain wrapped assets are no longer placed in the same risk basket. Recent discussions within the Lido community regarding wstETH cross-chain security and Chainlink CCIP have reinforced the importance of bridge security and issuance control in the pricing of LSTs.

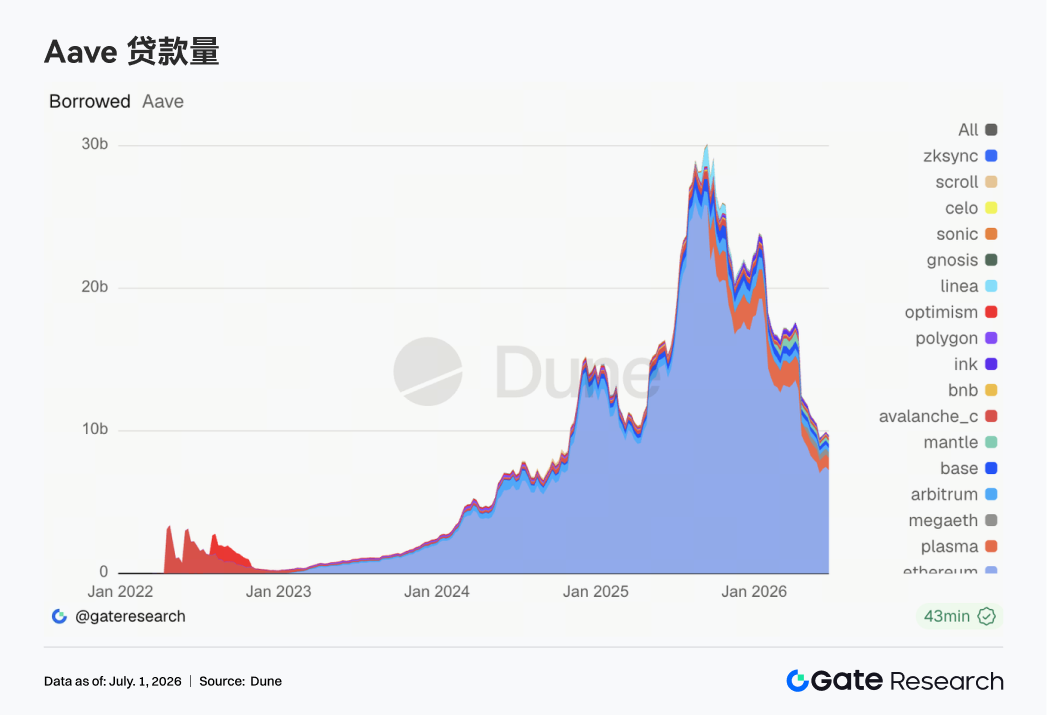

3.4 Aave Lending Contraction Continues; Capital Still Favors the Deepest Ethereum Main Market

Aave's lending balance this week saw a slight decline compared to the previous week. The Ethereum main market remains the absolute core but also bore the brunt of the contraction. Plasma was largely stable, Mantle saw some recovery, while MegaETH, Arbitrum, and Base were weaker. This suggests capital hasn't left Aave, but the pace of its multi-chain expansion has clearly slowed. The lingering effects of the rsETH/KelpDAO incident persist, with borrowers becoming more sensitive to collateral safety, liquidation depth, and risk parameters. Aave's recent governance discussions around WETH unfreezing, USDC liquidity buffers, and the V4 Hub-and-Spoke architecture are leveraging this risk event into institutional-level fixes. For institutions, Aave remains the core DeFi lending infrastructure, but its short-term growth logic has shifted towards stabilizing leverage on the main market and repricing the risk framework.

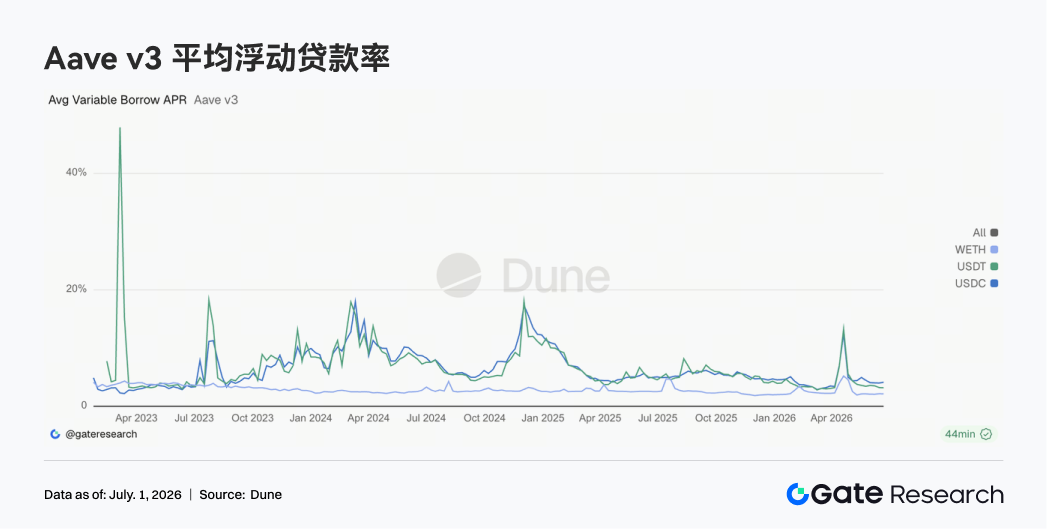

3.5 Aave Core Asset Rates Remain Low and Differentiated; USDC Remains the Most Sensitive Pool

This week, the lending rates for Aave's three core assets showed little overall change. The average borrowing cost for USDC inched up, USDT decreased, and WETH remained low. The peak rates for USDC within the week still saw brief upticks, indicating that the core USD pool remains sensitive to utilization rate changes. USDT rates were more stable, and there was no significant rush to borrow WETH, suggesting directional ETH leverage hasn't returned on a large scale. This combination corresponds to a cautious capital environment. Stablecoin financing is still used for turnover, arbitrage, and liquidity management, but the market hasn't restarted stacking one-sided risk exposure. Considering the Aave community's discussions on USDC liquidity buffers, the protocol is proactively mitigating interest rate jump risks under extreme utilization rates. The signals from interest rates are more moderate than the lending balance data. While the panic has subsided, the memory of risk remains.

3.6 Protocol Revenue Structure Improves; Stablecoins Provide a Base, Trading & Infrastructure Regain Elasticity

Protocol revenue showed more depth and texture this week compared to the previous one. Tether and Circle remain the most stable sources of cash flow, with little overall change. Hyperliquid Perps revenue grew again, indicating that despite a weaker spot market, demand for on-chain perpetual contracts and high-frequency matching remains resilient. Solana traffic entry points like Pump.fun, PumpSwap, Phantom, and Jupiter also showed recovery, correlating with PumpSwap's volume surge in DEXs. Improvements in revenue for Aerodrome, Base, Titan Builder, and Aave V3 suggest that revenue elasticity is spreading from purely Meme-driven traffic to matching platforms, L2 transactions, and lending infrastructure. On a macro level, Bitcoin's sluggishness, unstable ETF flows, and stable