Preferred Stock "Domino Effect": Strive’s $7.08 Million Loss, Strategy’s Risk Chain Reaction

- Core Thesis: Preferred stock issued by Bitcoin reserve companies has shifted from income-generating assets to credit risk indicators. Their cross-shareholding model directly transmits the discount risk of a single company to the balance sheets of other firms, revealing the core transmission mechanism of systemic risk in the industry.

- Key Elements:

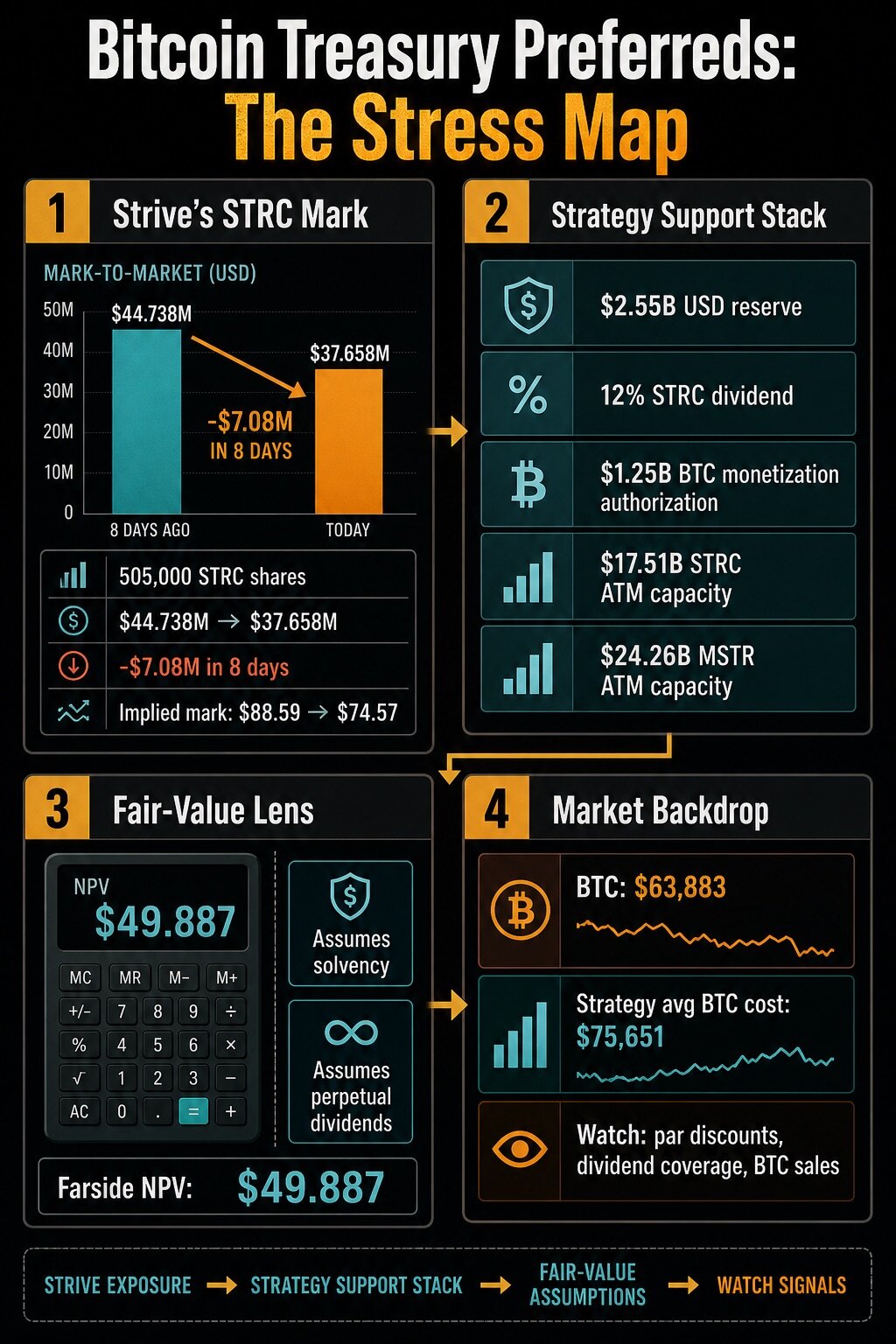

- Strive holds 505,000 shares of STRC preferred stock, incurring an unrealized loss of $7.08 million due to fair value fluctuations in 8 days, directly exposing cross-holding risks.

- Strategy has launched a Digital Credit Capital framework, setting a $2.55 billion USD reserve and mandating coverage for dividends over the next 12 months, while increasing the annualized dividend yield on STRC to 12%.

- Strategy has authorized up to $1 billion for buybacks of its own digital credit securities and $1 billion for repurchases of its common stock. It has also received approval to raise up to $1.25 billion by selling Bitcoin to replenish reserves.

- Third-party firm Farside calculates the net present value per share of STRC to be only $49.887, with its valuation highly dependent on dividend sustainability and the issuer's creditworthiness.

- As of June 28, Strategy held 847,363 Bitcoins with an average cost basis of $75,651. The current market price being below this cost base intensifies market focus on its reserve policy and liquidation plans.

- Subsequent market judgment will focus on the STRC discount margin, dividend cash coverage capability, the extent of further share issuance, and whether the authorized Bitcoin sales translate into actual actions.

Original author: Liam 'Akiba' Wright

Original translation: Saoirse, Foresight News

The preferred shares issued by Bitcoin reserve companies are no longer merely yield-generating assets; they have become a credit barometer for assessing the health of Bitcoin corporate balance sheets. Although market focus remains on Strategy, data disclosed by Strive, the world's seventh-largest publicly listed Bitcoin holder, vividly demonstrates the real impact of risk spillover: value fluctuations in another Bitcoin reserve company's holdings of Strategy's preferred shares have become a clear signal of market stress.

In an updated filing released on June 29, Strive disclosed that between June 18 and June 26, its holdings of 505,000 STRC shares remained unchanged, but the fair value of this position fell from $44.738 million to $37.658 million.

In just eight days, with no adjustments to the number of shares, the position's value evaporated by $7.08 million. Based on a simple calculation from the reported fair value, the market's valuation of Strive's STRC holdings dropped from approximately $88.59 per share to $74.57 per share.

This filing does not prove that the company is insolvent, forced to sell assets, or that its capital structure has completely failed. However, it reveals a more critical fact: even before a major crisis erupts, the risk of Bitcoin reserve preferred shares can be transmitted through cross-shareholding to the balance sheets of other companies.

As of June 26, Strive still held 19,864 Bitcoins, $141.7 million in cash and cash equivalents, and had 7,829,502 of its own SATA preferred shares outstanding. But the core signal of this financial report is not the scale of its own assets; rather, it is its exposure to Strategy's preferred shares that has fundamentally changed investors' logic for evaluating the entire sector.

There has long been a debate in the market regarding STRC issued by Strategy: will investors view this product as a stable income-generating instrument or as a high-risk credit asset tied to Bitcoin price movements, market liquidity, and Strategy's ability to pay dividends? Strive's disclosure has made this question more acute.

The cross-holding of preferred shares by different Bitcoin reserve companies has established a clearly visible channel for cross-company risk transmission. Once STRC trades at a discount, Strive will reflect the asset loss in its own financial statements' fair value. If the SATA preferred shares issued by Strive subsequently face market skepticism, the market can intuitively judge whether the current pressure is limited to a single company or has spread across the entire industry through the preferred share financing model.

These reserve preferred shares were initially marketed based on stable yields, fixed par value, and regular dividends, making them highly attractive to investors seeking steady returns. However, when market attention shifts to discount rates relative to par value, cash reserve coverage ratios, dividend adjustment mechanisms, share buybacks, and potential asset sales, the trading nature of these securities completely shifts towards credit-type risk assets.

The core question on investors' minds now becomes: does the issuer have sufficient cash, smooth access to financing channels, and enough Bitcoin liquidity to credibly ensure dividend payment?

The $7.08 million unrealized loss on Strive's STRC preferred shares over eight days exposes the risk of cross-shareholding in the industry. The chart also lists Strategy's full toolkit for stabilization, including cash reserves, high dividends, coin sales, and additional issuance. Combined with a third-party estimate placing STRC's fair value at only $49.887 and the current Bitcoin market price being significantly lower than the company's acquisition cost, it suggests that investors should focus on tracking preferred share discounts, dividend coverage capacity, and Bitcoin sale actions to assess the direction of industry risk.

Strategy's New Operational Framework: Essentially Credit Risk Management

A regulatory filing submitted by Strategy on June 29 further confirms the aforementioned shift in logic. The company introduced a Digital Credit Capital Framework, supported by policies including dollar reserve management rules, a revised STRC dividend plan, a preferred share buyback program, a common stock buyback program, and a Bitcoin monetization plan. This set of tools is specifically designed to address a stressed capital structure.

Strategy disclosed that its dollar reserves stood at $2.55 billion as of June 28. The board has a firm requirement that management must retain cash reserves sufficient to cover at least 12 months of future preferred stock dividends and interest payments, unless the board specifically approves a lower threshold. The filing also states that reserve funds can be supplemented through the sale of tokens via the Bitcoin monetization plan or other capital market operations.

This reserve is crucial because Strategy has raised the regular annual dividend rate on STRC to 12%, payable twice monthly, applicable to all record dates on or after July 1. The company has announced cash dividends of $0.50 per share for the settlement periods ending July 31 and August 15, subject to the terms of the STRC issuance agreement.

While raising the dividend can temporarily support this yield-oriented product, it also raises new questions: can this high dividend be sustained if the security continues to trade at a discount?

Strategy has clearly outlined the logic linking its policies: the STRC dividend plan will comprehensively reference the secondary market price of STRC, overall market yields, credit spreads, Bitcoin price and volatility, reserve coverage ratio, capital market conditions, and the company's overall capital structure. The filing also emphasizes that STRC dividends are not guaranteed and will not be unilaterally increased solely because the market price of STRC falls below its par value.

The entire policy framework is clearly an active credit management approach. The company has also authorized up to $1 billion for repurchasing its own digital credit securities. If management believes buybacks can enhance corporate value and optimize the capital structure, STRC will be a priority target. An additional $1 billion has been authorized for repurchasing Class A common stock. These authorizations do not obligate the company to execute them, but they clearly demonstrate the full range of tools available to management if the discount risk continues to worsen.

Within this same capital framework, selling Bitcoin has been formally included as a response measure. The board approved a Bitcoin monetization plan, allowing the company to raise up to $1.25 billion by selling Bitcoin to supplement its dollar reserves. If management determines this method is preferable to issuing additional common stock or other capital market operations, the proceeds from coin sales can be used to fund preferred stock dividends and interest payments, as well as share buybacks.

The company has stated that this plan does not mandate a forced sale of Bitcoin, but the authorization fundamentally changes the market narrative: this company, originally focused on accumulating Bitcoin as its core business, now has a formal channel to use its Bitcoin assets to stabilize its credit structure.

Fair Value Calculation: The Core Test of Dividend Sustainability

A publicly available STRC fair value calculator from the third-party firm Farside explains why the market's focus has long moved beyond nominal yields. When CryptoSlate queried this tool on July 7, the calculated net present value per STRC share was only $49.887 under default assumptions, which include an initial coupon rate of 11.50% that steps down to 3.60% starting in month 33.

This calculation relies on a key assumption: that the company will continue as a going concern and pay dividends in full and permanently. This valuation is not an official price from Strategy and should not be confused with Strategy's announced 12% annualized STRC dividend policy. However, it clearly reflects the core variables that preferred stock investors truly care about: the valuation is highly dependent on dividend sustainability, the discount rate, and the issuer's ability to continue paying interest amidst fluctuations in Bitcoin prices and capital markets.

The broader Bitcoin market environment further amplifies this credit test. CryptoSlate's Bitcoin price data shows that on July 8, Bitcoin was trading at approximately $62,000, down 1.8% in 24 hours but up 5.5% over seven days. Its total market cap was $1.24 trillion, representing a Bitcoin dominance of 58%.

However, Strategy's Bitcoin holdings as of June 28 show that the company holds 847,363 Bitcoins with an average acquisition cost of $75,651. While the current market price being significantly below the average cost does not force an immediate sale, it explains the intense market focus on reserve policies, at-the-market (ATM) issuance mechanisms, and clauses related to Bitcoin monetization.

Strategy's ATM data shows that the business model still has ample financing capacity. Between June 22 and 28, the company did not issue any preferred shares through the ATM channel. It sold only 12,669,017 shares of MSTR common stock, raising a net $1.1524 billion. Remaining issuance capacity was: $17.5108 billion for STRC preferred shares, $24.2575 billion for MSTR common stock, along with other preferred stock issuance plans.

The entire business model still has multiple buffer tools, but the key question remains: what price will be paid to use these tools when investors demand higher yields, securities trade at significant discounts, or stronger collateral assets are needed?

Two Scenarios for Judging Whether Risk Has Spread Broadly

Current market analysis of the future path falls into two core logic streams:

Scenario 1: Risk is Contained, Affecting Only Strategy

The discount on STRC narrows. Dollar reserves and the dividend policy stabilize market sentiment. The Bitcoin monetization plan remains a backup option only. The asset impairment for Strive represents a one-off short-term impact from cross-shareholding. Other reserve companies in the sector are unaffected, and pressure is concentrated solely on Strategy itself.

Scenario 2: Risk Spreads Broadly

STRC maintains a deep discount for an extended period, and the dividend increase fails to calm the market. The company relies increasingly on the common stock ATM facility. The Bitcoin monetization plan transitions from authorization to actual sales. Simultaneously, Strive's own SATA preferred shares come under pressure, no longer viewed as an independent product but grouped with STRC as a high-risk asset by the market. At this point, Bitcoin reserve preferred shares would evolve from a single-company problem into a systemic risk for the entire sector.

Existing filings do not prove that the second scenario has occurred, but they are sufficient to explain the root of market concern: Strive's STRC holding directly transforms Strategy's discount risk into a fair value loss on another company's financial statements.

The framework introduced by Strategy integrates dividends, cash reserves, share buybacks, ATM issuance, and potential Bitcoin sales into a unified risk buffer system. Meanwhile, the Farside valuation tool highlights that the company's ability to continue as a going concern and the assumption of perpetual dividends are central to determining the value of these preferred shares.

The key indicators for future market observation are clear: whether the discount of STRC and SATA relative to par value widens, the credibility of cash dividend coverage, whether the company increases the pace of common stock or preferred stock issuance, and whether Bitcoin sales remain only at the authorization stage.

Strive's subsequent financial disclosures will be a critical signal for determining whether its losses on Strategy's preferred shares are an isolated incident or the first public indication of Bitcoin reserve credit risk spreading across the industry via the preferred share model.