Nomura Analysis: Why Are They Bullish on Japan’s MLCC Release Film?

- Core Thesis: Nomura Securities’ report estimates that, driven by demand for high-end multi-layer MLCCs from AI servers, the upstream MLCC release film market is expected to see a compound annual growth rate (CAGR) of approximately 10% from 2025 to 2028. Japanese manufacturers dominate the market, but pricing pressure and capacity expansion timelines are key variables.

- Key Factors:

- Industry Growth Rate: Nomura projects a ~10% CAGR for MLCC release film demand from 2025 to 2028, with growth primarily fueled by AI server demand for high-capacity, high-reliability multi-layer MLCCs.

- Market Structure: Japanese manufacturers hold over 80% of the global market share, with Lintec commanding approximately 37% and Toyobo around 32%. Lintec is notably more focused on the high-end coating segment.

- Profit Contribution: The MLCC release film business accounts for roughly 17%, 13%, and 3% of the operating profits for Lintec, Toyobo, and Toray, respectively. While profit margins are high, it doesn't represent their entire business.

- Price Risk: Nomura anticipates a risk of price decline for release films in 2026 due to new capacity coming online from Toyobo and Toray. However, expansion is considered moderate, making a significant price crash unlikely.

- Capacity Constraints: If Lintec does not expand production capacity in a timely manner, it could approach full utilization by 2027, potentially causing some high-end market share to shift to competitors like Toyobo.

TL;DR

- Nomura expects MLCC release film demand CAGR of approximately 10% from 2025-2028, assigning a Buy rating to Lintec.

- AI servers require more high-end multi-layer MLCCs, with release films being critical in slurry coating, printing, and lamination processes.

- Japanese manufacturers hold over 80% market share, but price pressure and expansion pace in 2026 still limit earnings elasticity.

In a July 2nd report, Nomura Securities traced AI server demand further upstream to a Japanese materials sector: MLCC release films. The institution forecasts a compound annual growth rate (CAGR) of approximately 10% for this material from 2025 to 2028, and has initiated coverage on Lintec with a Buy rating and a price target of 7850 yen.

MLCCs are multi-layer ceramic capacitors used extensively in electronic systems like servers, power supplies, and motherboards. As AI server computing power and power consumption increase, demand grows for higher-capacity, more reliable multi-layer MLCCs. The higher the layer count, the greater the requirements for smoothness, cleanliness, and stability in the release films used during production.

The key players in this chain are primarily Japanese materials companies. According to Nomura's estimates, Japanese manufacturers hold over 80% of the global MLCC release film market share, with Lintec at approximately 37% and Toyobo at about 32%. Lintec focuses more on high-end coating needs, Toyobo is expanding production capacity, and Toray is positioned further upstream in the base film segment.

AI Servers Drive Demand to Release Films

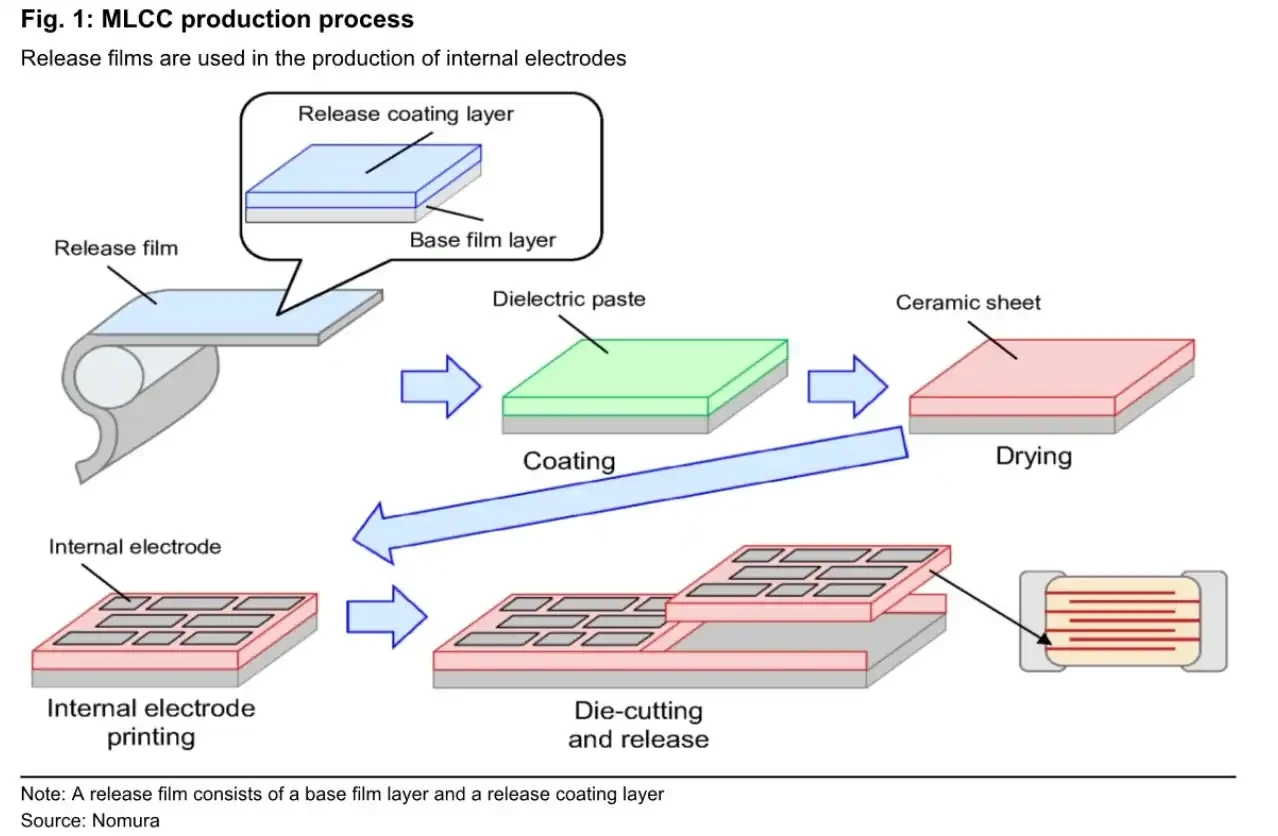

Release films are not a final component of MLCCs, but they play a crucial role in the manufacturing process.

During MLCC production, manufacturers first coat a dielectric slurry onto the release film, dry it, and then proceed to internal electrode printing and lamination. Toray's IR materials illustrate this process with steps like "Slurry Casting," "Inner electrode printing," "Release film," and "Base PET film." An uneven release film surface can negatively impact electrode printing accuracy and interlayer stability.

The change brought by AI servers is the simultaneous increase in the volume and specifications of high-end MLCCs. TrendForce also noted on June 17th that AI ASIC and accelerator platforms are driving concentrated demand for high-end MLCCs, with significantly increased usage of some specifications, and flagged a rising risk of supply tightening in the second half of 2026. This external viewpoint doesn't directly confirm the ~10% CAGR for release film demand but supports the directional trend of AI servers driving high-end MLCC demand.

Schematic diagram of the MLCC production process, illustrating the role of release film from dielectric slurry coating to internal electrode printing and lamination.

The key figure from Nomura is the ~10% CAGR for MLCC release film demand from 2025 to 2028. For a mature materials segment, this growth rate is significant, especially against a backdrop of no broad-based high growth in consumer electronics, making AI servers the primary incremental driver.

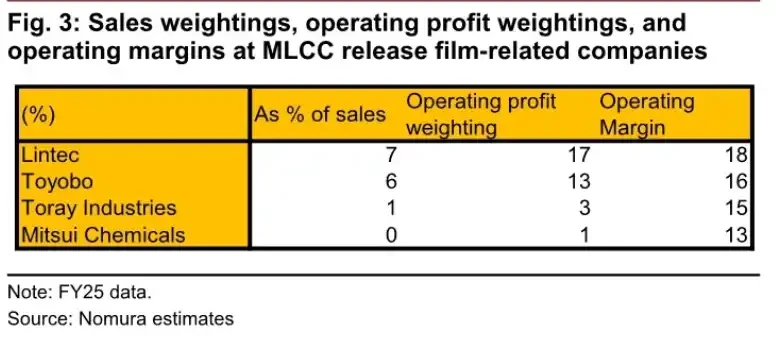

However, demand growth does not directly translate into overall company earnings elasticity. According to the report, MLCC release film-related businesses account for approximately 7% of Lintec's sales and 17% of its operating profit; for Toyobo, it's about 6% of sales and 13% of operating profit; and for Toray, roughly 1% of sales and 3% of operating profit. This indicates the business has a high profit margin but is not the sole determinant of revenue for these large materials companies.

Weight of MLCC release film business in sales, operating profit, and profit margins for each company: Lintec 7%/17%/18%, Toyobo 6%/13%/16%, Toray 1%/3%/15%.

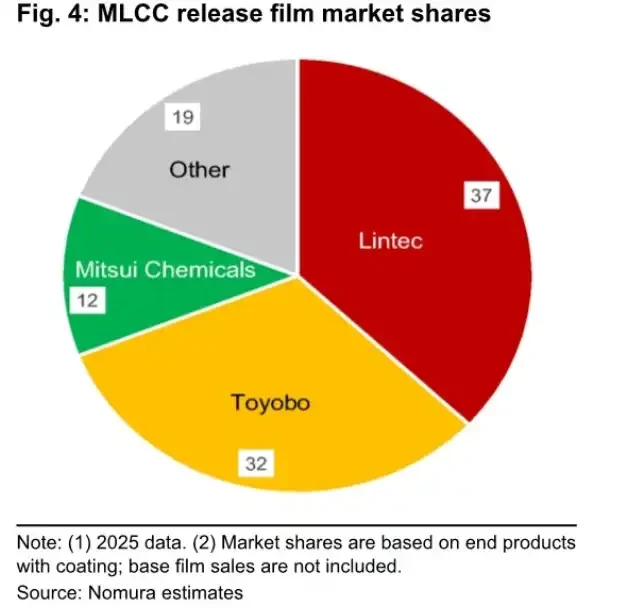

Lintec and Toyobo Combine for Nearly 70% Market Share

The MLCC release film market is highly concentrated.

Measured by finished coated products, Lintec holds approximately 37% market share, Toyobo ~32%, Mitsui Chemicals ~12%, and others ~19%. Together, Lintec and Toyobo command nearly 70% of the market.

Lintec's advantage lies primarily in its high-end coating capabilities. It purchases base films externally, performs release coating processing, and delivers them to MLCC customers. In high-end applications like AI servers, Lintec is better positioned to directly benefit from the volume growth of multi-layer MLCCs.

Toyobo's differentiation lies in possessing both base film and coating capabilities. According to public company materials, its new release film facility in Utsunomiya has been completed and started operations. Investor materials mention commercial production beginning in Spring 2025, with full capacity expected by the end of FY3/26. Nomura's report pegs the full-scale production milestone for Q3 2026. If capacity ramps as planned, Toyobo could capture more high-end demand after 2027.

Toray is positioned further upstream. It holds over 50% of the external sales market share for MLCC release film base films. Public IR materials show Toray's new Gifu production line starting operation in February 2026. According to Nomura's report, after increasing related capacity by 1.6 times, there is still room for sales volume growth.

MLCC release film market share: Lintec 37%, Toyobo 32%, Mitsui Chemicals 12%, Others 19%.

This also means the incremental materials demand from AI servers will not be evenly distributed. Lintec appears as the direct beneficiary of high-end demand, Toyobo as a share challenger after capacity is released, and Toray benefits from growth in external base film sales.

Behind the 7850 Yen Target Price, Lintec Faces Capacity Pressure

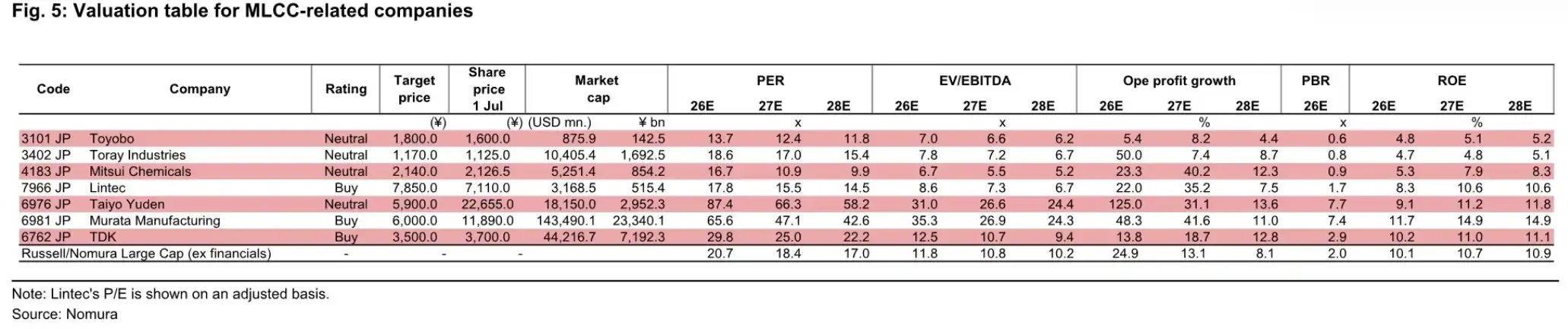

Regarding specific stocks, Nomura is most clear on its stance for Lintec, rating it a Buy with a price target of 7850 yen. The report uses a stock price of 7110 yen as of July 1st, implying a forward P/E of 17.8x for 2026.

In the same valuation table, Toyobo is rated Neutral with a target of 1800 yen; Toray is rated Neutral with a target of 1170 yen; and Murata Manufacturing, a downstream MLCC leader, is also rated Buy with a target of 6000 yen. These targets and valuations are from Nomura's report and not market consensus.

Comparison table of MLCC-related company valuations, including ratings, target prices, current stock prices, and 2026-2028 valuations for Lintec, Toyobo, Toray, and Murata Manufacturing.

Lintec's weakness also lies in capacity. Nomura points out that if the company does not proceed with new expansion in a timely manner, it could approach full capacity by 2027. If AI server-related demand continues to grow, supply constraints could cause Lintec to lose some market share to competitors like Toyobo.

Toyobo's opportunity arises precisely from this scenario. After capacity is released, if industry demand maintains annual growth of ~10%, the new capacity can translate into market share gains. However, if demand falls short of expectations, the new supply could also create pressure on pricing and capacity utilization.

Toray's base film expansion is more like an upstream bottleneck relief. Given the high surface smoothness requirements for MLCC release film base films, increased base film supply capacity helps support coated manufacturers in expanding shipments. However, Toray's related business contributes a relatively small portion to group revenue and profit, making it harder for this segment alone to significantly alter the overall valuation.

Volume is Growing, but Prices May Not Rise Unilaterally

This is not a simple narrative of "rising demand, rising prices, rising stock prices." The key constraints are pricing and the pace of capacity expansion.

Nomura anticipates a risk of MLCC release film selling prices declining in 2026. As Toyobo's new capacity comes online and Toray boosts base film capacity, industry supply will increase, and prices may not necessarily rise in tandem with demand. The report also believes overall expansion remains moderate, capacity utilization is unlikely to drop sharply, and the probability of a significant price decline is low. Materials manufacturers will primarily benefit from shipment growth.

This judgment relies on two prerequisites: continued realization of demand for multi-layer MLCCs used in AI servers, and new capacity not significantly exceeding the growth in high-end demand. If end-user capital expenditure slows down, or if MLCC manufacturers enter an inventory adjustment phase, the growth rate for release film demand could fall below the ~10% modeled by Nomura.

A more realistic divergence lies in company execution. If Lintec lags in expansion, it may miss out on some high-end orders. If Toyobo faces insufficient demand after expansion, it could encounter price and utilization pressure. While Toray has a high base film market share, its related business contribution to the group is limited.

AI servers have indeed thrust the small materials segment of MLCC release films into the market spotlight, but earnings realization still depends on whether high-end MLCC orders can sustain volume growth, and whether Japanese manufacturers' capacity expansion keeps pace appropriately, rather than prematurely creating new supply pressure.