伯恩斯坦上调高通目标价至235美元,为何评级仍按兵不动?

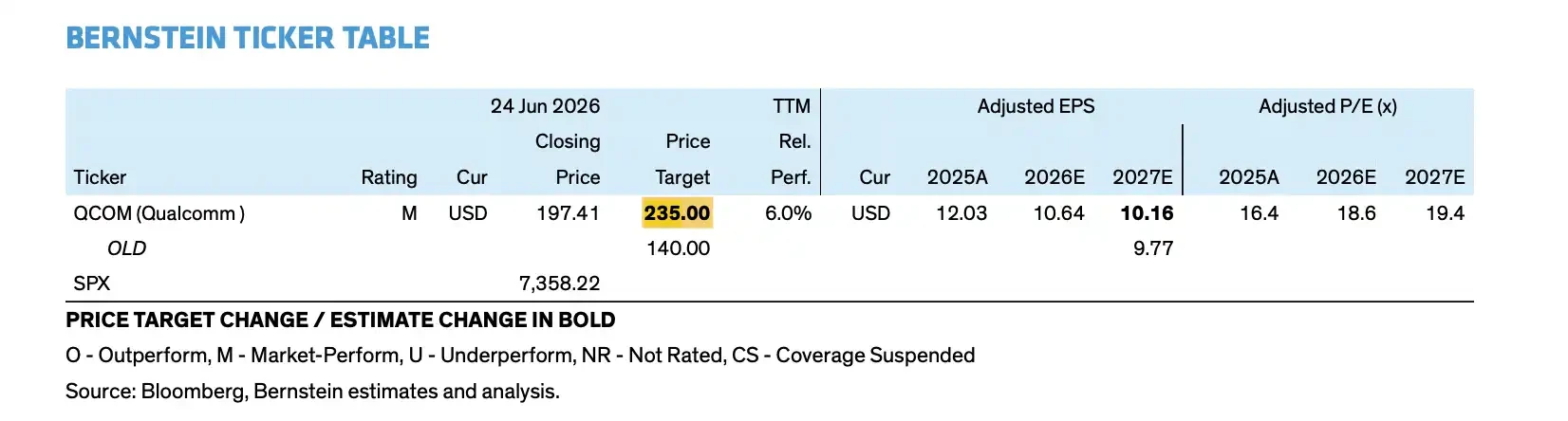

- 核心观点:伯恩斯坦将高通目标价从140美元上调至235美元,但维持“市场表现”评级,核心在于认可其AI数据中心等远期增长目标(FY2029非手机收入约400亿美元),但短期手机业务下滑、运营支出上升及数据中心毛利率不确定性构成约束,风险回报未明显偏向买入。

- 关键要素:

- 目标价上调源于估值模型纳入更大数据中心收入(FY2029超150亿美元)和多元化结构,市盈率从14倍升至20倍,而非短期盈利大幅上修。

- 数据中心路线包括定制ASIC和Dragonfly C1000 CPU,有两个未具名云客户预计FY2027各自贡献超10亿美元定制硅收入,Meta合作确认非独家的多代CPU合作。

- 汽车和IoT构成第二增长曲线,汽车设计管道从450亿美元增至650亿美元,FY2029目标分别达100亿和140亿美元以上。

- 手机业务面临压力:FY2027安卓收入预计持平或略降,苹果收入退出使手持设备收入可能减少50-60亿美元,安卓手持收入FY2026-2029复合增速仅约5%。

- 费用端提前承压:FY2027运营支出将双位数增长,数据中心收入确认滞后于投入,可能导致FY2027前后每股收益面临下修风险。

- 数据中心毛利率约40%低于公司平均水平,整体毛利率可能从FY2026的55.2%降至FY2029的51.6%,影响盈利质量。

- 下行情景中即使数据中心收入显著低于150亿美元目标,FY2029每股收益仍约15美元,显示基本盘稳健,但18美元以上目标的实现需依赖客户放量、毛利率稳定及手机业务平稳过渡。

TL;DR

- Bernstein raised Qualcomm's price target from $140 to $235, but maintained a Market Perform rating.

- Qualcomm's FY2029 vision targets data centers, automotive, and IoT, with a goal of approximately $400 billion in non-handset revenue.

- A declining handset business, rising OPEX, and uncertainty over data center gross margins remain core constraints preventing an upgrade.

Price Target Raised, But Rating Unchanged

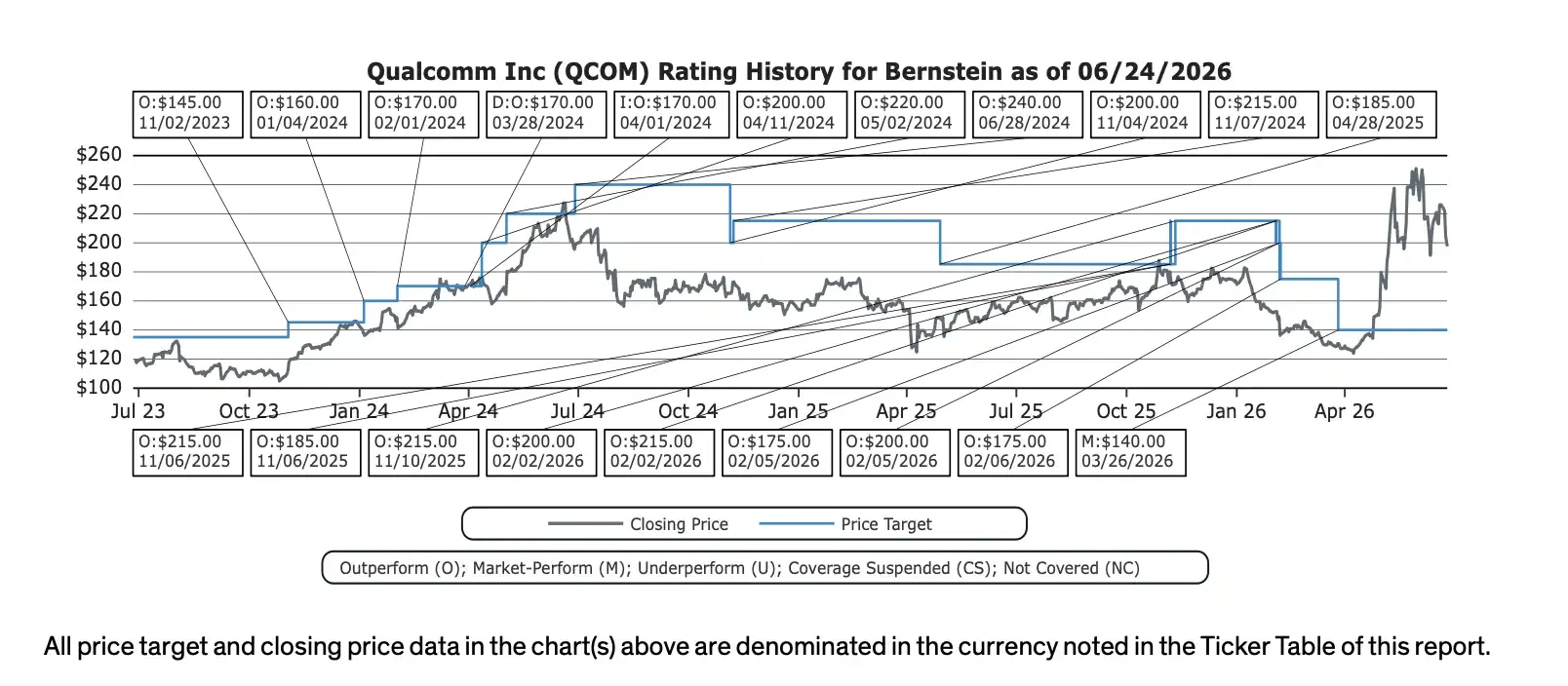

Following Qualcomm's Investor Day in New York, the company presented a significantly larger long-term growth story to the market. Subsequently, Bernstein raised Qualcomm's price target from $140 to $235 but maintained a Market Perform rating.

The price target hike indicates Bernstein acknowledges that Qualcomm's long-term narrative is expanding. The company is no longer positioning itself solely as a mobile chip supplier but is attempting to enter broader computing markets, including AI data centers, automotive, IoT, and personal AI devices. According to Qualcomm's official targets, by FY2029, the company aims for non-handset revenue to reach approximately $400 billion, data center revenue to exceed $150 billion, and Non-GAAP EPS to surpass $18.

However, the unchanged rating suggests the sell-side does not yet see this story as sufficiently proven. The core constraint lies in the timing gap: the realization of data center and automotive revenues is further out, while headwinds from a declining handset business, the loss of Apple revenue, rising OPEX, and margin pressure will hit financials sooner.

This explains why a $235 price target does not equate to a "buy" signal. Bernstein acknowledges that Qualcomm's long-term valuation ceiling has been raised, but with current stock prices already reflecting some optimistic expectations, the risk-reward ratio hasn't tilted decisively towards the buy side.

The New Narrative: Shifting from Mobile Cycles to AI Data Centers

Qualcomm's most important new narrative this time is the data center.

The company's official target indicates data center revenue will exceed $150 billion by FY2029. Compared to its current data center revenue base of approximately $30 billion, this means Qualcomm must successfully tap into cloud giants' AI infrastructure budgets over the next few years, rather than just remaining in the mobile chip and edge computing markets.

Qualcomm's disclosed data center roadmap includes custom ASICs, AI inference accelerators, the Dragonfly C1000 CPU, connectivity products, and related software layers. The company also mentioned two unnamed Hyperscaler customers, each expected to contribute over $10 billion in custom silicon revenue by FY2027.

The partnership with Meta serves as another crucial validation point. Qualcomm and Meta announced a multi-generational collaboration on data center CPUs, with the Dragonfly C1000 CPU planned to begin production in the second half of 2028. However, caution is warranted: the official statement indicates Qualcomm will be a supplier, but the specific value, production capacity, and exclusivity terms remain undisclosed.

Automotive and IoT form the second growth curve. Qualcomm's official targets show FY2029 automotive revenue reaching $100 billion and IoT revenue exceeding $140 billion. The automotive design-win pipeline has grown from $450 billion 18 months ago to $650 billion, with the company continuing to bet on digital cockpits, driver assistance systems, and in-vehicle connectivity.

The $235 Price Target Bets on 2029, Not Next Year

The core reason for Bernstein's price target increase is not a sudden improvement in Qualcomm's near-term performance, but rather the integration of larger data center revenue and a more balanced business structure into the valuation model.

According to Bernstein's model calculations, Qualcomm's FY2029 revenue is approximately $648 billion with an EPS of about $18.12, closely aligning with the company's long-term target of "Non-GAAP EPS exceeding $18." Compared to the past, when the market primarily priced Qualcomm based on mobile cycles, data centers, automotive, and IoT now offer the company the potential for higher valuation multiples.

The $235 price target corresponds to a higher valuation framework. Bernstein uses an average FY2027/FY2028 EPS of approximately $11.75 and a 20x P/E multiple for valuation; the previous $140 target corresponded to a multiple of about 14x. In other words, the key to the price target increase is not a significant upward revision in next year's earnings, but rather the market's willingness to pay a higher multiple for Qualcomm's AI data center and diversified revenue story.

However, this also harbors divergence. Bernstein's model assumes a gross margin of approximately 40% for the data center business, which is lower than Qualcomm's current company average. Even as data center revenue scales up, it may not immediately lift overall profitability. The report estimates that due to the changing business mix, Qualcomm's overall gross margin could decline from 55.2% in FY2026 to 51.6% in FY2029.

Handset Headwinds Arrive First, Data Center Realization Awaits

Qualcomm aims to prove its revenue structure is changing through data centers, automotive, and IoT, but the pressure on the handset business has not disappeared.

According to the sell-side report and management Q&A, FY2027 Android handset revenue is expected to be flat or slightly down. Coupled with the loss of Apple revenue, total handset revenue could decline by $5 billion to $6 billion year-over-year. The handset business remains Qualcomm's largest current revenue source, and this decline will directly impact the profit base for the next two years.

The company's long-term assumptions for Android handsets are also more cautious. From FY2026 to FY2029, the compound annual growth rate for Android handset revenue is expected to be around 5%, significantly lower than the high-growth phases of previous cycles. While Qualcomm may maintain advantages in high-end Android, AI phones, and RF front-end components, this will likely not fully offset the pressures from Apple's exit and the broader slowdown in the smartphone industry.

Cost pressures will also emerge earlier. Qualcomm explicitly guided for double-digit OPEX growth in FY2027. To advance data center CPUs, AI accelerators, custom silicon, and the software ecosystem, the company needs to invest upfront in R&D, sales, and customer support. Revenue recognition typically lags these investments, implying that EPS forecasts around FY2027 face potential downside risk.

This is the key reason for the raised price target yet unchanged rating: Qualcomm's long-term story is bigger, but the profit trajectory for the next two to three years is not necessarily smoother. Investors must simultaneously accept two propositions: FY2029 EPS could be lifted by AI data centers, but earnings pressure around FY2027 might also be more pronounced.

The Debate Hinges on Whether $150 Billion in Data Center Revenue Can Translate into Real Profit

Bernstein's report is not a simple bearish view on Qualcomm. Rather, while repricing the stock, it reminds the market not to treat long-term targets as already realized performance.

In a downside scenario, if data center revenue falls significantly short of the $150 billion target and growth in personal AI and computing businesses is limited, Qualcomm's FY2029 EPS could still reach approximately $15. This indicates that Qualcomm's fundamental base isn't fragile; automotive, IoT, licensing, and cost control can still sustain a certain level of profitability.

However, the gap between $15 and over $18 EPS has a significant impact on valuation. If the market has already priced Qualcomm based on more optimistic data center revenue and higher valuation multiples, the company must prove three things: that cloud customers can ramp up as planned; that data center gross margins won't persistently drag down overall profitability; and that the handset business decline won't excessively depress EPS before new businesses materialize.

Therefore, the $235 price target is not a conclusion that "Qualcomm's AI transformation is already successful," but rather a new price reflecting the long-term diversification prospects within the valuation. Qualcomm's story is indeed bigger than before, resembling more of a chip platform company spanning mobile, automotive, IoT, and AI data centers.

However, the Market Perform rating serves as a reminder: until handset headwinds ease, data center revenue materializes, and gross margins are tested, the market has reason not to rush into labeling Qualcomm a definitive AI winner. What truly needs verification next is not whether Qualcomm can articulate a $150 billion data center target, but whether this target can translate into revenue on time and ultimately into sufficiently good profits.