三折买Aave?被误读的传言,藏着Kraken的上市野心

- 核心观点:Kraken拟入股Aave的传闻揭示了交易所向全栈金融基础设施转型的战略意图,同时凸显了AAVE代币与股权之间价值归属的结构性疑问,但Aave创始人否认了交易折扣的报道。

- 关键要素:

- Kraken计划以约7100万美元(含3.5万ETH)换取25万枚AAVE及Aave Group 15%股权,估值仅3.85亿美元,较AAVE代币市值折让约七成。

- Aave创始人Stani澄清,交易涉及Labs持有的代币份额,非协议层面,且协议收入全部流向代币,否认以三折出售AAVE。

- 交易价值归属成谜:若协议价值全归代币,Kraken买入股权而非代币的具体权益未被明确解释,绕过了散户的核心疑问。

- Kraken战略转型明确:自建Layer2(Ink)、密集收购(Bitnomial、Reap、Backed Finance)并获美联储主账户,打造全栈金融基础设施。

- IPO进程暂缓:3月因比特币跌至6.5万美元及BitGo上市后股价下跌44%暂停,但计划2026年底前完成,此次入股意在充实招股书叙事。

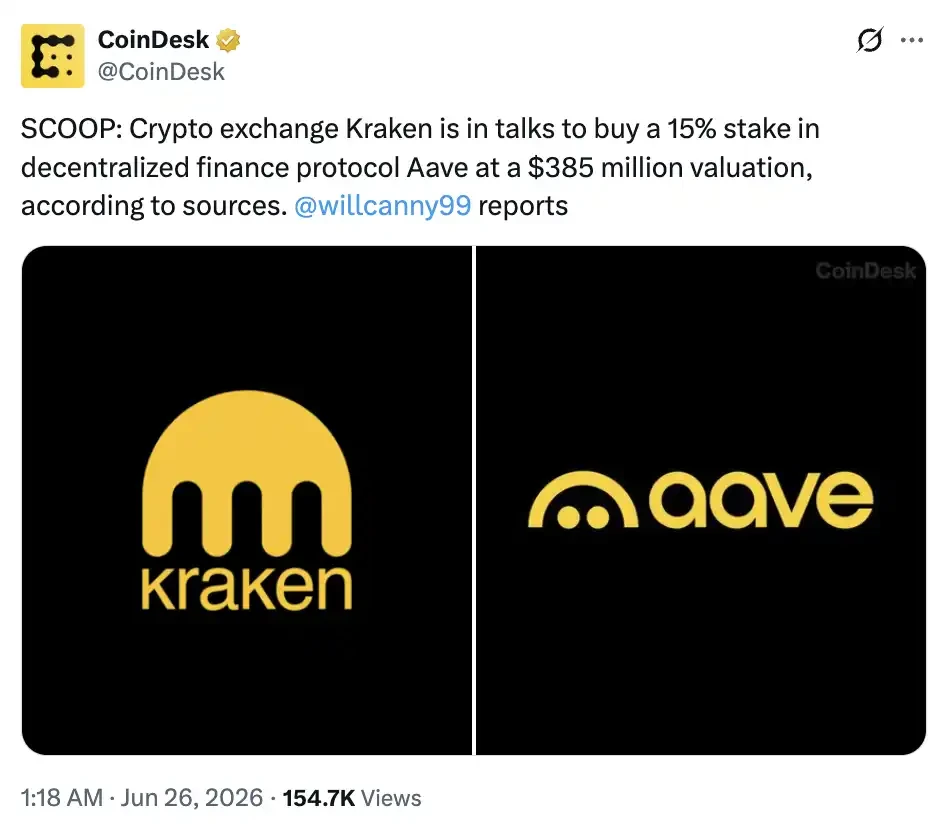

In the early hours of today, a report ignited the DeFi community.

CoinDesk, citing three sources familiar with the matter, reported that crypto exchange Kraken is in talks to take a stake in Aave. The proposed deal structure involves Kraken putting up 35,000 ETH in exchange for 250,000 AAVE tokens, plus a 15% common equity stake in Aave Group, with the entire transaction valued at approximately $71 million, implying a $385 million valuation. The report also mentioned that this is the first in a series of transactions under Payward Asset Management, and that Kraken intends to syndicate the deal externally while taking a more active role in DeFi and other investment opportunities moving forward.

What stands out most in this deal is the valuation at which it was struck. At $385 million, it represents a discount of nearly 70% compared to AAVE's token market cap of roughly $1.24 billion. Aave has consistently emphasized that all protocol value accrues to its token. So, what exactly is Kraken getting by spending real money on a 15% equity stake? If all value is supposed to flow to the AAVE token, why does Kraken need an equity seat at the table?

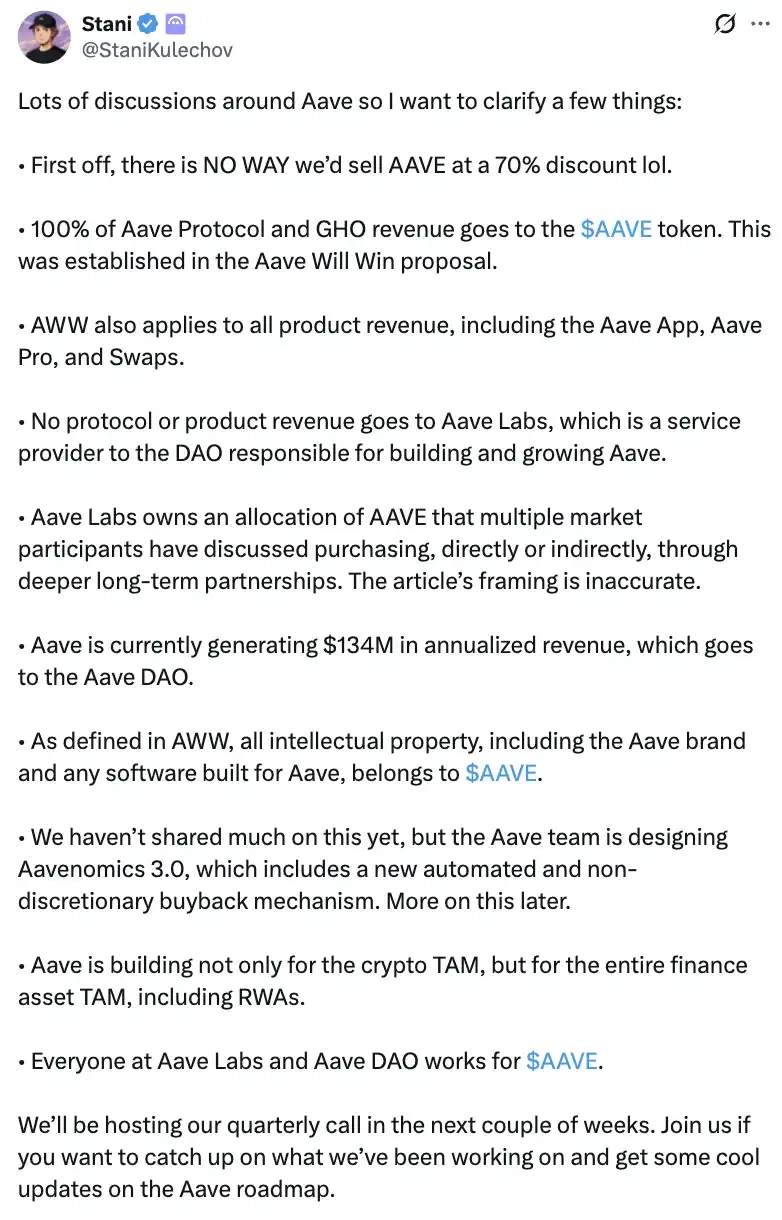

A few hours later, Aave founder Stani Kulechov stepped in to clarify.

He refuted the report's framing point by point. Aave Labs would never sell AAVE at a 70% discount; what was discussed was the portion of AAVE held by Labs itself, negotiated by "multiple market participants through deeper long-term collaborations," and unrelated to the protocol level. He emphasized that all revenue from the Aave protocol and the GHO stablecoin flows to the AAVE token, a rule established under the "Aave Will Win" proposal, which also includes revenue from products like Aave App, Aave Pro, and Swaps. Aave Labs is merely a service provider for the DAO and receives no share of protocol revenue.

Stani also took the opportunity to reveal that the team is designing Aavenomics 3.0, which will introduce an automated buyback mechanism without human discretion.

According to his account, what was being sold wasn't discounted AAVE; CoinDesk's comparison of the total equity deal value to the market cap of a single token was inherently misleading.

If Stani's version is accurate, CoinDesk's report does contain misleading elements.

However, Stani did not address the retail investor's original question. If the protocol's value is indeed fully captured by the token, then what is Kraken actually buying with a 15% stake in Aave Group? He sidestepped this issue. The value attribution between equity and tokens remains a murky point.

The details of the transaction remain up in the air, and Kraken has not offered a direct comment on the report.

But their motivation seems clear. CoinDesk noted in its article that Kraken's parent company, Payward, characterized the deal as "the opening move in a series of asset management actions." A company preparing for an IPO is positioning its stake in a DeFi leader as a flagship maneuver.

Over the past year and a half, Kraken has made new moves almost every quarter, advancing along three parallel tracks.

The first is building proprietary infrastructure.

Kraken incubated its own L2, "Ink," attempting to replicate the path trodden by Binance and Coinbase by funneling CEX users onto the chain for lending and trading. The most active protocol on Ink is the perp DEX "Nado," offering unified margin accounts for spot, margin, and perpetuals, attracting a number of real users through its points program and airdrop expectations.

The second track is strategic acquisitions.

Over the past year and a half, Kraken's acquisitions have been frequent: acquiring derivatives exchange Bitnomial for $550 million, bringing in a full set of CFTC licenses for brokerage, clearing, and exchange operations; buying stablecoin payments company Reap for $600 million to add card issuance and cross-border settlement capabilities; purchasing Backed Finance, the entity behind the tokenized stock protocol xStock, late last year; and acquiring token management platform Magna this February.

The third track is regulatory identity.

In March of this year, Kraken became the first digital asset bank in the US to obtain a Federal Reserve master account, allowing it to settle USD directly on Fedwire without needing an intermediary bank. The same month, Nasdaq announced a partnership with Kraken to build a framework for tokenized stocks, preserving issuer control and shareholder voting and dividend rights. A crypto exchange is adopting an identity rooted in traditional finance.

Kraken is evolving from a crypto exchange into a full-stack financial infrastructure company.

An IPO is the primary driver behind all these strategic initiatives. In November last year, Payward raised $800 million at a $20 billion valuation, with its valuation increasing by 30% within two months. The investor list included Citadel Securities, Jane Street, and Apollo Global Management.

Viewed through this lens, Kraken's desire to take a stake in Aave makes perfect sense—it's extending the narrative of being able to "handle any financial business" into DeFi itself. Acquiring a partial stake in a leading protocol is much faster than building a lending protocol from scratch and provides a more compelling story for the prospectus regarding growth sources.

However, Kraken's IPO path has not been smooth.

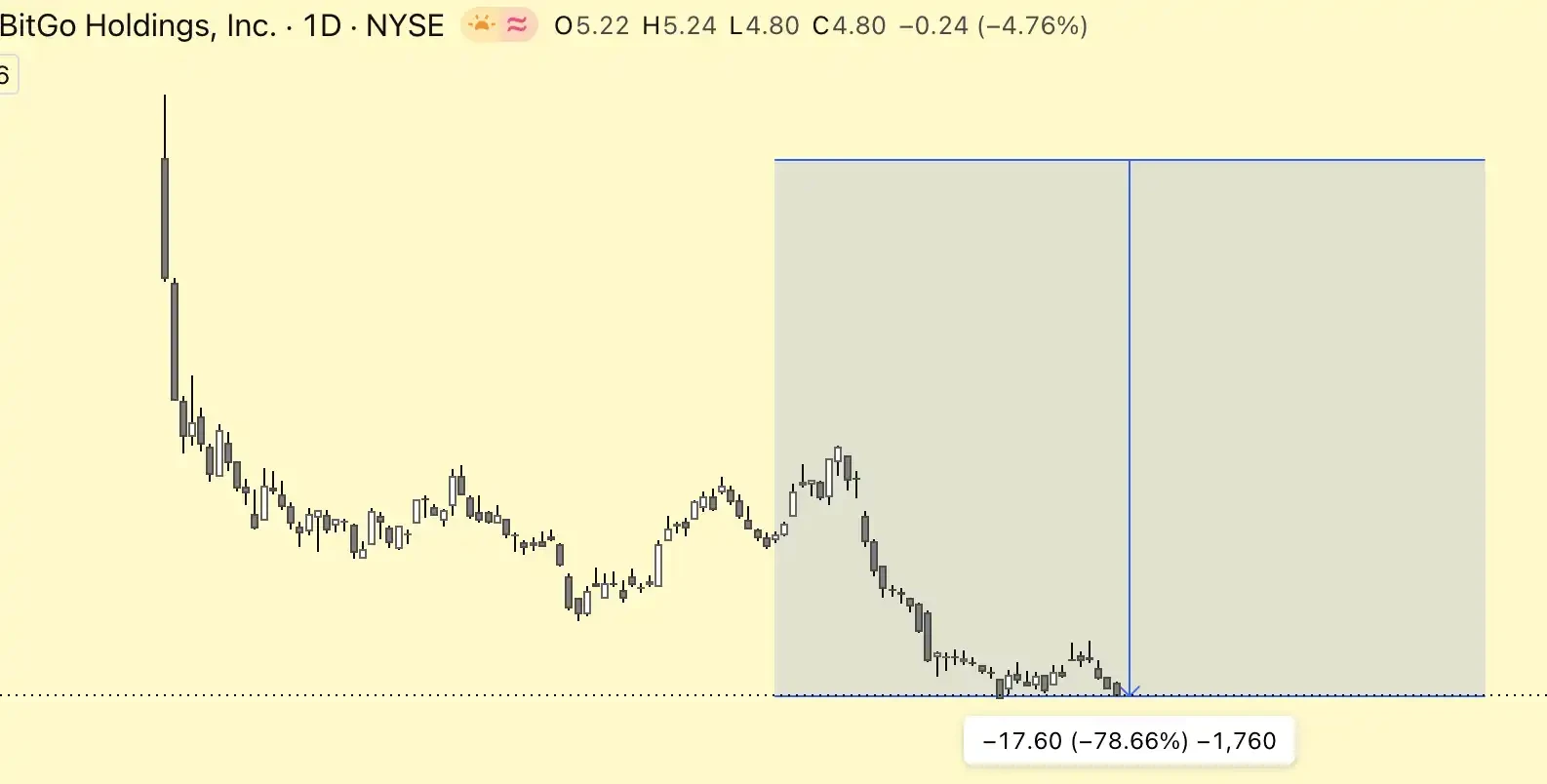

On March 18 of this year, Kraken's IPO was put on hold. The core reason was the bleak market environment, with Bitcoin falling from $126,000 in October last year to around $65,000, wiping over a trillion dollars in market value. BitGo, which went public before Kraken, was the only digital asset company to list in 2026, and its stock price has dropped 44% since its IPO—a stark warning visible to everyone.

Market tastes are also changing. While at least 11 crypto IPOs raised a combined $14.6 billion in 2025, 2026 has started much colder. Advisors say investors are now scrutinizing financial infrastructure targets more carefully, re-evaluating regulatory maturity, recurring revenue, and resilience point by point. Just one month before the IPO was paused, Kraken replaced its CFO of only 16 months, handing the duties to a newly promoted deputy CFO. Changing the financial chief at the eleventh hour is a red flag for any company undergoing due diligence.

But a pause doesn't mean an exit.

In May of this year, reports emerged that Payward was raising a new round of funding at a $20 billion valuation. Co-CEO Arjun Sethi has also publicly stated multiple times in recent months that the company's goal is to complete its IPO by the end of 2026. It's foreseeable that over the next six to nine months, Kraken may increase the frequency of its moves to add weight to the valuation narrative in its prospectus.

The rumor of taking a stake in Aave is just the latest step in this process. As for whether the deal will close, and what exactly that 15% equity stake buys, the written answer will likely only surface when the S-1 filing is made public.