SpaceX IPO First-Day Guide: Don't Treat It Like a Regular Hot Stock

- Core Thesis: The SpaceX IPO first day is not ordinary stock trading. Its low float (approximately 3%) and high retail allocation (approximately 30%) will lead to violent two-way volatility. Investors should abandon traditional technical analysis, switch to order flow trading, wait for the market to establish a price structure before acting, and base long-term judgments on subsequent supply tests.

- Key Elements:

- SpaceX IPO priced at $135, raising $75 billion, with a valuation of $1.7 trillion, but the initial float is only about 3%. This amplifies price swings, meaning any moderate buying pressure can cause a significant impact.

- The retail allocation ratio is approximately 30%, 3-4 times the normal level. This increases first-day uncertainty: retail investors could either chase the rally or take profits, creating the first wave of supply.

- The stock may be added to the Nasdaq 100 index on the 15th trading day post-listing. This will bring price-insensitive passive buying, potentially altering the nature of capital flows and prompting active funds to front-run the move.

- Historical hot IPOs (like Coinbase, Airbnb) show that high attention does not guarantee a one-way rally. They often experience violent two-way volatility early on, making them more suitable for order flow traders than trend followers.

- Lock-up expirations will follow the first earnings report, with phased unlocks on days 70, 90, 120, 180, and one year after listing. Long-term investors must monitor whether the market can absorb the new supply.

Original Title: SpaceX IPO Day: What Retail Traders Don't See (The Orderflow Read)

Original Author: The Flow Horse

Original Translation: Peggy, BlockBeats

Editor's Note: Against the backdrop of mega-IPOs, AI narratives, and the repricing of risk assets, the market's discussion of a SpaceX listing is shifting from "how much is this company worth" to "how will it be traded once it goes public." But as SpaceX becomes one of the most anticipated tech assets, a more critical question emerges: On the first day of trading a new stock with no price history, no mature options structure, and no clear distribution of shares, should investors use a valuation framework to understand it, or a market microstructure framework?

This article is a translation of The Flow Horse's video content regarding trading strategies for SpaceX's IPO day. The focus is not on discussing SpaceX's long-term fundamentals, but rather on deconstructing the capital flows, free float, index inclusion, and lockup expiration rhythm it might face in its early days as a public company. The video's author is a market trader with a long-term focus on IPOs and order flow, offering a perspective closer to the order book and trade execution rather than traditional company valuation analysis.

In this content, the SpaceX IPO is broken down into a set of more fundamental structural issues: It's not a simple "should I buy or not" question. It's a process where traders, retail investors, passive capital, and internal shareholders all repricing around limited liquidity across different time windows.

First, retail investors most easily misjudge the first-day trading environment. In the past, when retail investors traded hot stocks, they typically relied on trendlines, support and resistance, prior highs and lows, and opening momentum. But on SpaceX's IPO day, there is no historical chart, no volume profile, no mature options structure. Before the first candlestick forms, the market has no reusable price memory. What truly determines short-term direction now is the order book, volume, VWAP, the opening range, and where buyers and sellers form real turnover. This means that if retail investors chase the initial wave at the open, or prematurely use technical analysis to find a so-called trend, they are likely assuming the highest risk before the structure is established.

Second, past hot IPOs do not support the assumption of "inevitable one-way upward movement" in early trading. Coinbase, Airbnb, and ARM all garnered immense attention, but they didn't immediately provide a stable trend early in their trading. Instead, they first experienced severe two-way volatility. In the past, the market easily interpreted hot IPOs as a confirmation of emotional consensus. A more accurate understanding now is that they often first become a venue for repeated turnover between short-term capital, profit-takers, and new buyers. This means that even with strong narratives and high oversubscription, SpaceX's first week might not be suitable for trend followers. Those truly suited for day-one participation are often traders who can quickly read order flow, control position size, and accept two-way volatility.

Third, the day-one strategy should shift from "predicting direction" to "waiting for structure." In the past, many traders were accustomed to pre-establishing a bullish or bearish view before the open, then using the initial price wave to verify their judgment. But for an IPO with a low float like SpaceX, it's more important to let the market draw its own structure first: Is there support around the $135 price? Is the 5-minute opening range effectively broken? Does VWAP hold on a retest? Are there hidden buying or selling forces constantly refreshing in Level 2 data? The core of trading now is not to jump to a conclusion before everyone else, but to determine who holds the initiative after the market generates its first batch of price coordinates. This means the most important thing is not to enter the trade first, but to avoid being forced to execute a trade in the most chaotic, widest-spread, and most emotionally charged position.

Fourth, investors must understand that different stages are dominated by different types of capital. For the first 15 trading days, SpaceX is more like a short-term trade dominated by low float, emotional capital, and order flow. Around the 15th trading day, the expectation of Nasdaq index inclusion might bring a second phase of price-insensitive buying. After the first earnings report, unlock supply begins to test market absorption. Further out, lockup expirations for major shareholders at days 70, 90, 120, 180, and one year will gradually provide more reliable long-term signals. In the past, IPOs were often seen as a success or failure based on the first day's price move. Now, SpaceX appears more like a series of consecutive liquidity tests. This means long-term judgments should not be based on day-one sentiment, but on whether the price can form a stable bottom after new supply enters the market.

Fifth, SpaceX trading may not solely occur in SpaceX itself. Related aerospace and space economy assets like Rocket Lab and LUNR might become proxy stocks for capital expressing the same theme during the listing period. In the past, IPO trading typically revolved around the primary asset. Now, when the primary asset has too low a float, too high volatility, and too wide spreads, related assets might actually provide a clearer trading structure. This means the market isn't just trading SpaceX's stock; it's also trading the industry narrative and liquidity spillover that SpaceX activates.

If this article were compressed into one judgment, it would be this: The first day of the SpaceX IPO belongs to traders; long-term judgment must wait for a supply test. For a trader, day one could be the "Super Bowl" of order flow trading. For an investor, the first day's rise or fall should not be over-interpreted. In this sense, the core question of the SpaceX IPO has shifted beyond whether to buy on day one. It's now about whether participants can first determine which game they are entering: day one is about order flow, the long-term is about supply absorption capacity. Mixing these two up is precisely the primary reason most retail investors lose money.

The following is the video content (edited for readability):

Why Most Retail Investors Might Lose Money on the SpaceX IPO

The most dangerous aspect of SpaceX's IPO day is that many people will treat it like an ordinary hot stock to trade.

Normal stocks have historical price ranges, prior highs and lows, volume profiles, and enough market memory. Traders can refer to past support and resistance, moving averages, options open interest, and cost basis. But an IPO day is a blank chart. Before the first candlestick appears, the market has zero real trading history.

This means drawing trendlines prematurely is meaningless, and chasing the first surge after the open can easily get you stopped out by a counter-move. Especially in a low float environment, prices can spike quickly on transient buy orders, but also collapse suddenly due to profit-taking or institutional supply. If retail investors only look at the percentage gain and sentiment, they are very likely to enter at the most noisy position.

The real trading logic for SpaceX's IPO day is the real-time formation of the auction mechanism (where buyers and sellers seek a balance of transactions at various prices). A trader needs to observe: Who is willing to bid up the price? At what price levels is the seller constantly replenishing? At which prices is a lot of volume trading, but the price can't push through? This order book information is far more important than any pre-drawn technical pattern.

Trading Details: $75 Billion Fundraising, ~3% Float, and High Retail Allocation

SpaceX's IPO plans to issue approximately 555 million shares, raising around $75 billion at a price of $135 per share, giving it a total valuation of roughly $1.7 trillion. This scale alone makes it a market-level event.

But what truly determines day-one volatility is not just the fundraising size, but the float. The freely tradable shares at the start of the IPO are estimated to be only about 3% of the total. This means that even moderate buying pressure can have a significant impact on the price. Buying by retail chasers, active fund initiators, or small institutional purchases can all push the price away from fundamentals temporarily.

Another unique variable is the retail allocation. This IPO's retail allocation is estimated to be as high as 30%, roughly 3 to 4 times that of a typical IPO. This makes post-open trading even harder to judge. On one hand, more retail investors getting shares beforehand might reduce the "can't-buy" FOMO surge on the first day. On the other hand, these investors who received shares early might also take profits after the open, creating the first wave of supply.

Therefore, the core of the SpaceX IPO is not simply judging that "oversubscription is bullish," but understanding the share structure: an extremely low float amplifies both upside and downside moves, while a high retail allocation could make both buying and selling more aggressive on the first day.

Day 15: Nasdaq Index Inclusion Could Change the Nature of Capital

Another key timeline is the 15th trading day after listing. Based on current schedules, SpaceX could be eligible for inclusion in the Nasdaq 100 Index (NDX). This arrangement is still subject to final rules and actual results, but the corresponding trading logic is very important.

In the early days of trading, the main price drivers are fast money, retail investors, active funds, and emotional capital. This capital is price-sensitive and flows in and out quickly based on volatility. But after index inclusion, another type of capital enters the market: passive capital.

The characteristic of passive capital is that it is price-insensitive flow (flow that must buy due to index rules or portfolio requirements, not because the price is cheap). Index funds, ETFs, and related tracking products need to allocate component stocks according to the rules. This buying pressure is often more mechanical and easier for the market to front-run.

Therefore, before the 15th trading day, active capital might try to front-run (buy in anticipation of the assured buying pressure). If SpaceX has already established upward momentum early on, the mechanical buying from index inclusion could further amplify the trend. However, if the first two weeks are weak, this buying pressure alone may not be sufficient to reverse the market's trajectory.

This is another aspect that distinguishes the SpaceX IPO from a typical first-day trade: it is not a single-point event, but a series of capital flow nodes.

Day One is Order Flow Trading, Not Chart Trading

The most important judgment for SpaceX's first day is: Do not treat it as chart trading.

An ordinary trader habitually asks: Where is support? Where is resistance? Where is the prior high? Where is the volume profile? Where is the options max pain point? But for an IPO day, most of these questions have no answers. Without a historical chart, there is no reliable technical structure. Without a mature options market, there are no reference points for options open interest.

The real questions for day one are: Where do buyers and sellers find agreement? Where is there a high volume of turnover? Is there buying support if the price falls below the issue price? Is there a continuous supply of sellers when the price spikes? This is the core of order flow trading.

The first few critical price levels must be drawn by the market itself on the day. First is $135, the set issue price in the video. Traders must observe the price action relative to $135: Does it quickly recover after breaking below? Does it hold after breaking above? If buying support consistently appears every time it drops below $135, it suggests this level could be an early cost anchor. If it gets sold off every time it breaks above $135, it suggests stronger supply overhead.

Second is VWAP (Volume Weighted Average Price, representing the average cost of shares traded on the day). An hour after listing, whether the price is above or below VWAP, and whether it finds support on a pullback to VWAP, will directly reflect who is in control between buyers and sellers.

Finally, there are the day's high and low. After the close, the first day's high and low become the most important structural reference points for the following days. For a new stock with no chart history, the first day's price range is the initial coordinate system formed by the market.

Four Types of Capital Flows Driving the Price

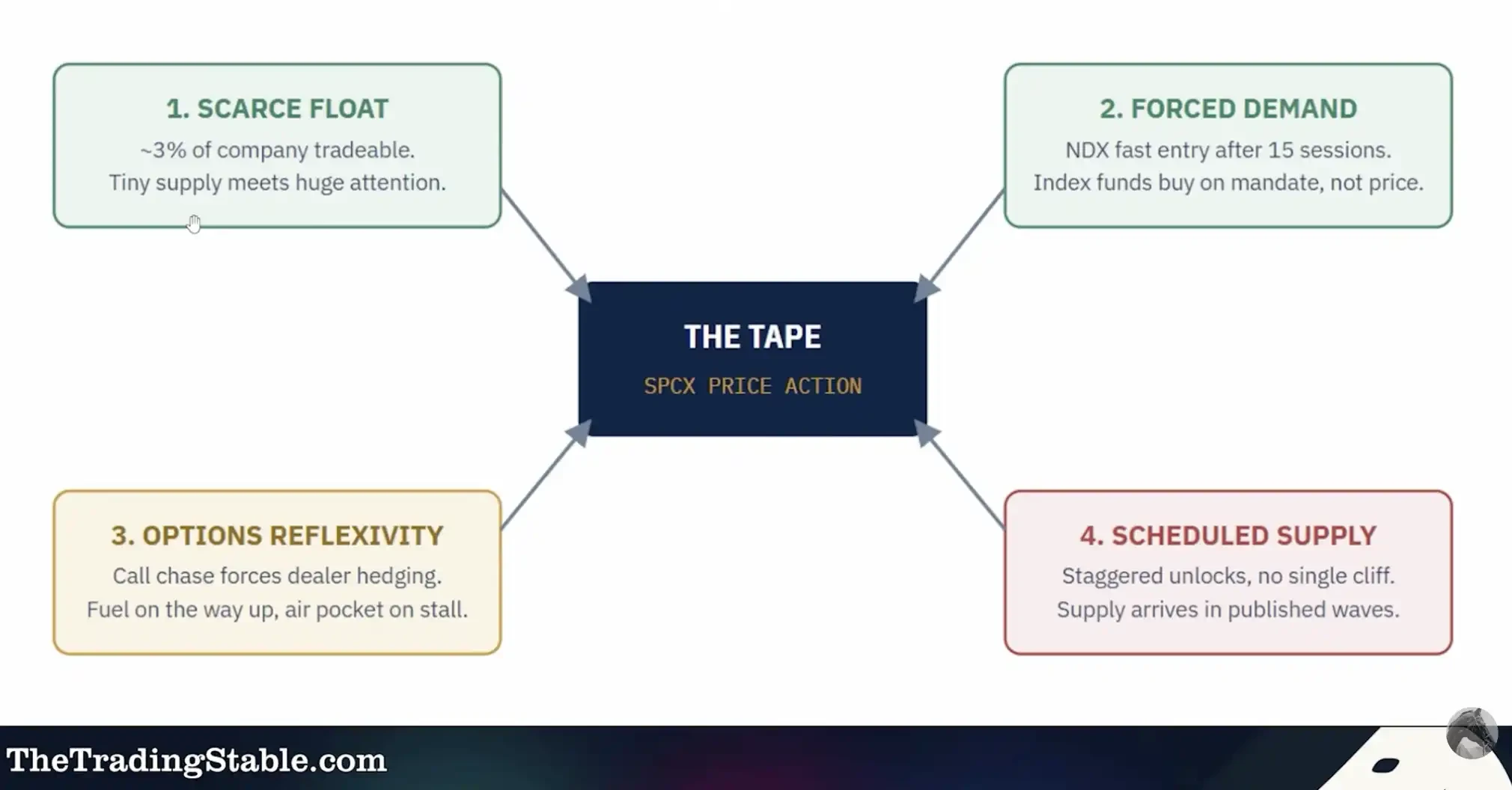

The initial price volatility of the SpaceX IPO can be broken down into four types of capital flows.

The first is scarcity buying power due to the extremely low float. A 3% float means there are very few shares available for trading. If demand concentrates even slightly, it can push the stock price up rapidly. This is also why blindly shorting on day one is very dangerous. A low-float stock won't necessarily go up forever, but it is most capable of "squeezing" short sellers in a short amount of time.

The second is passive buying from Nasdaq index inclusion. If included in the NDX on the 15th trading day, index funds and related products must buy according to the rules. This capital places orders based on index weight, not valuation. For a long-side holder, this is an ideal source of mechanical demand. For a short-term trader, this is a time window that can be traded in advance.

The third is options reflexivity (where the options market inversely affects the stock price). Once options begin trading, if retail investors heavily buy call options, it might force market makers to buy the underlying stock to hedge, thus creating a Gamma cycle (options buying forces market makers to hedge by buying stock, further amplifying the upward move). However, this mechanism typically doesn't appear immediately on the first day and may not mature in the first week.

The fourth is share unlocks (shares previously restricted from sale gradually entering the market). This introduces new supply and is a risk point all long-term investors must monitor. SpaceX's special aspect is that it might not simply have a single cliff unlock after 180 days, but could release shares in phases.

Unlock Schedule: Not a Single 180-Day Cliff

A common risk point for traditional IPOs is the 180-day lockup expiration, where early investors and employee shares unlock en masse, suddenly flooding the market with supply. But the SpaceX unlock structure presented in the video is more complex: it may not be a single cliff, but a series of phased liquidity events.

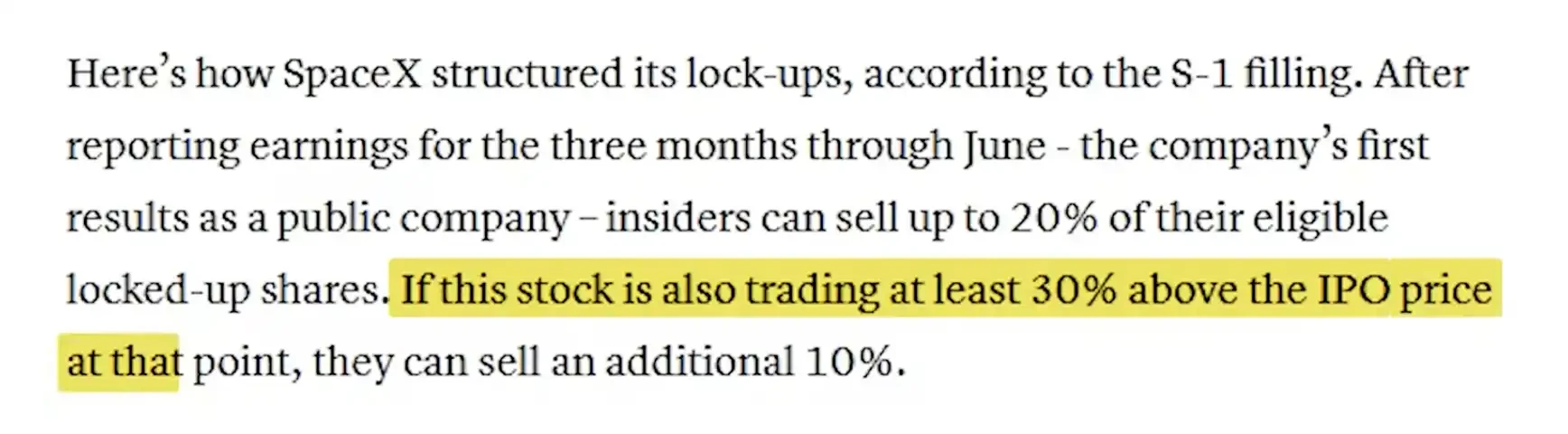

First, up to 20% of eligible shares could unlock 2 days after the first earnings report. This means the earnings report itself is not just a performance event, but also a supply event. If the stock price is driven high by sentiment before the earnings, the new supply post-earnings could dampen the momentum.

Second, unlocks might also be tied to price performance. If the stock price stays 30% above the $135 issue price for 5 out of the 10 trading days before the earnings report, an additional 10% of shares could unlock. This type of arrangement causes upward price movement to trigger more supply, creating a dynamic equilibrium: the stronger the rally, the more shares become available for sale later.

Subsequent milestones are equally important. The video mentions that approximately 7% of shares could unlock on days 70, 90, and 120, with full unlock after 180 days. Regarding employee shares, about 5% of employee holdings might be eligible for sale immediately after the first earnings report, without needing additional performance or price conditions. Elon Musk and the largest holders may need to wait over a year, approximately 366 days.

These dates are especially important for long-term investors. Judging whether SpaceX has formed a true bottom cannot rely solely on the first day's price move. It requires observing whether buying demand can absorb each new wave of supply as it enters the market.

Lessons from Past IPOs: Coinbase, Airbnb, and ARM Didn't Start with a One-Way Trend

Hot IPOs can easily create the illusion that high market attention automatically translates into a continuous upward trend after listing. But the early trading of Coinbase, Airbnb, and ARM all shows that hype does not equal a one-way trend.

The video mentions that these hot IPOs all experienced massive volatility in their early days. Coinbase's early price swing was about 119 points, Airbnb's was about 53 points, and ARM's was about 22 points. The key isn't the specific numbers, but what they illustrate: the first few days and weeks of a hot IPO are often periods of violent two-way trading, not a stable trend.

This kind of environment is more suitable for scalpers (traders who profit from frequent entry and exit on small, short-term price fluctuations) and order flow traders, rather than ordinary trend followers. Trend traders need structure, but the IPO's initial phase is precisely when structure is most lacking.

SpaceX could be more extreme. It is already heavily oversubscribed and might allocate more shares to retail investors. This means that after the open, there will be both chasing buying and profit-taking selling; some will try to position for the day-15 index inclusion, while others see the high hype itself as a selling opportunity. When bullish and bearish forces are simultaneously crowded, the result is often not a clean trend, but high turnover, high volatility, and high noise.

Day One Trading Strategy: Let the Market Draw Its Structure, Then Act

The first rule for trading SpaceX on day one is: Do not chase the initial open wave.

The opening moments are typically when noise is loudest, spreads are widest, and sentiment is most extreme. Especially in a low float environment, the first surge might just be a brief sweep of orders, and the first dip might just be a sharp drop due to a lack of liquidity. A truly