Is the growth story over? Oracle's plunge suggests the market is now demanding returns on investment

- Core Thesis: Oracle's strong earnings and cloud business guidance failed to boost its stock price, which fell over 10% in after-hours trading. The market is concerned that the massive capital expenditure and financing needs for AI infrastructure will erode future free cash flow. The AI trade is shifting from a "growth narrative" to an "asset return on investment" assessment.

- Key Factors:

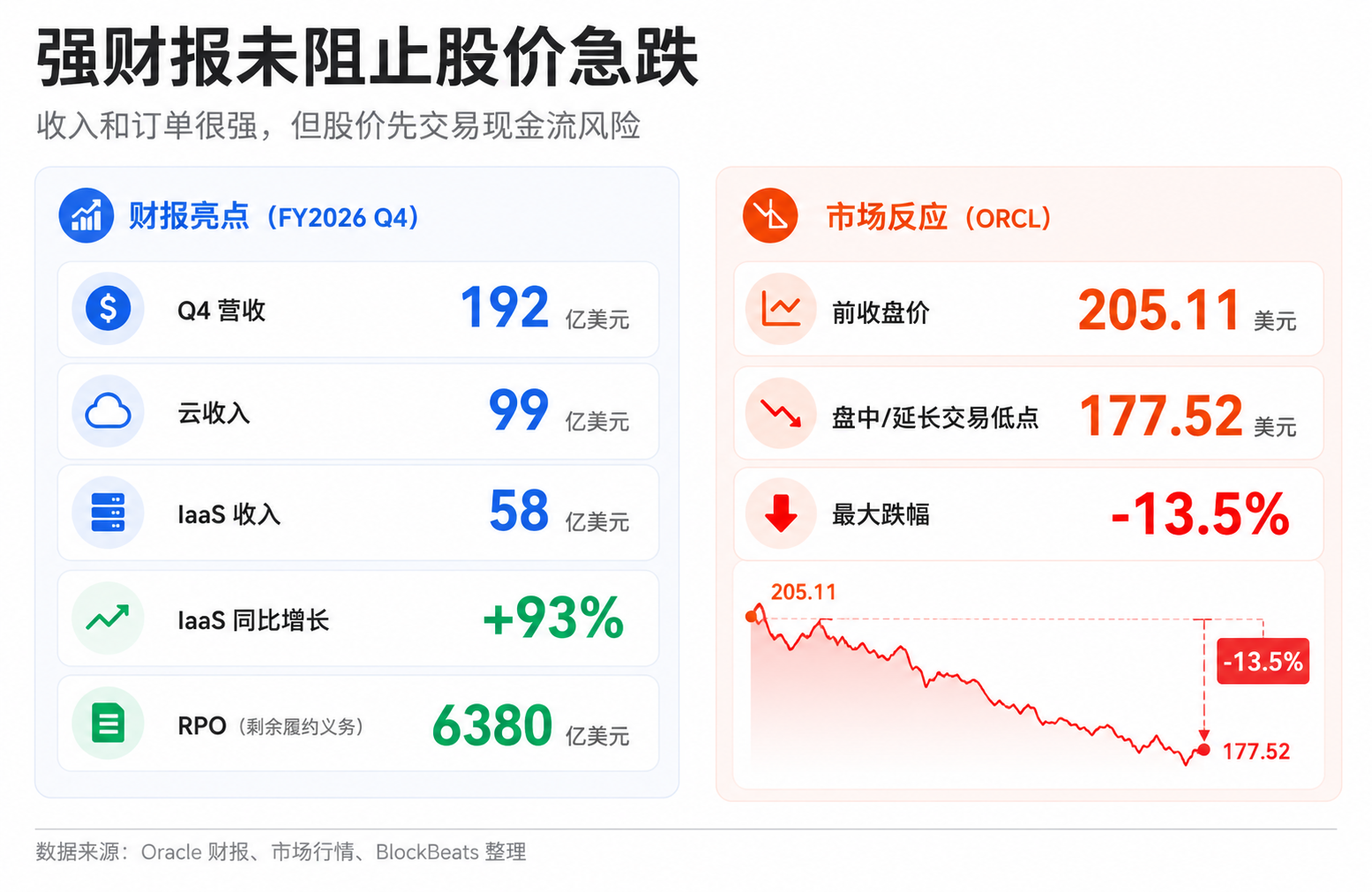

- Oracle reported Q4 FY2026 revenue of $19.2 billion, cloud revenue of $9.9 billion, IaaS revenue up 93% year-over-year, remaining performance obligations (RPO) surging to $638 billion, and FY2027 revenue guidance of $90 billion. Demand-side data is robust.

- The main reason for the market sell-off is that investors have reinterpreted growth data as capital consumption: FY2026 free cash flow was -$23.7 billion, and the company plans to raise approximately $40 billion in FY2027 through debt and equity financing, including a $20 billion ATM offering program.

- The AI infrastructure business model is akin to a power plant, requiring massive upfront investment (data centers, GPUs, electricity), with revenue lagging behind cash flow expenditures. The market is beginning to demand proof that this growth can translate into high-quality profits and cash flow.

- Customer prepayments or self-supplied GPUs totaling $75 billion can share part of the capital burden, but the market still needs to confirm whether the company's remaining financing, depreciation, and operational burdens are too heavy after accounting for these contributions.

- The market is deepening its comparison of AI assets: moving from "who has an AI story" to "who can translate AI demand into the profit and cash flow statements." The return on capital expenditure is becoming the core pricing factor.

TL;DR

- Oracle reported strong earnings and cloud business guidance, but its stock fell over 10% in after-hours trading as the market worries about the high costs of AI infrastructure.

- Demand hasn't disappeared; the question has shifted to how much free cash flow remains after orders pass through the costs of data centers, GPUs, electricity, and financing.

Related tickers: ORCL, NVDA, MSFT, AMZN, GOOG, META, QQQ, and potentially upcoming IPOs like OpenAI, Anthropic, and SpaceX.

Oracle's earnings report was almost everything an AI bull could hope for.

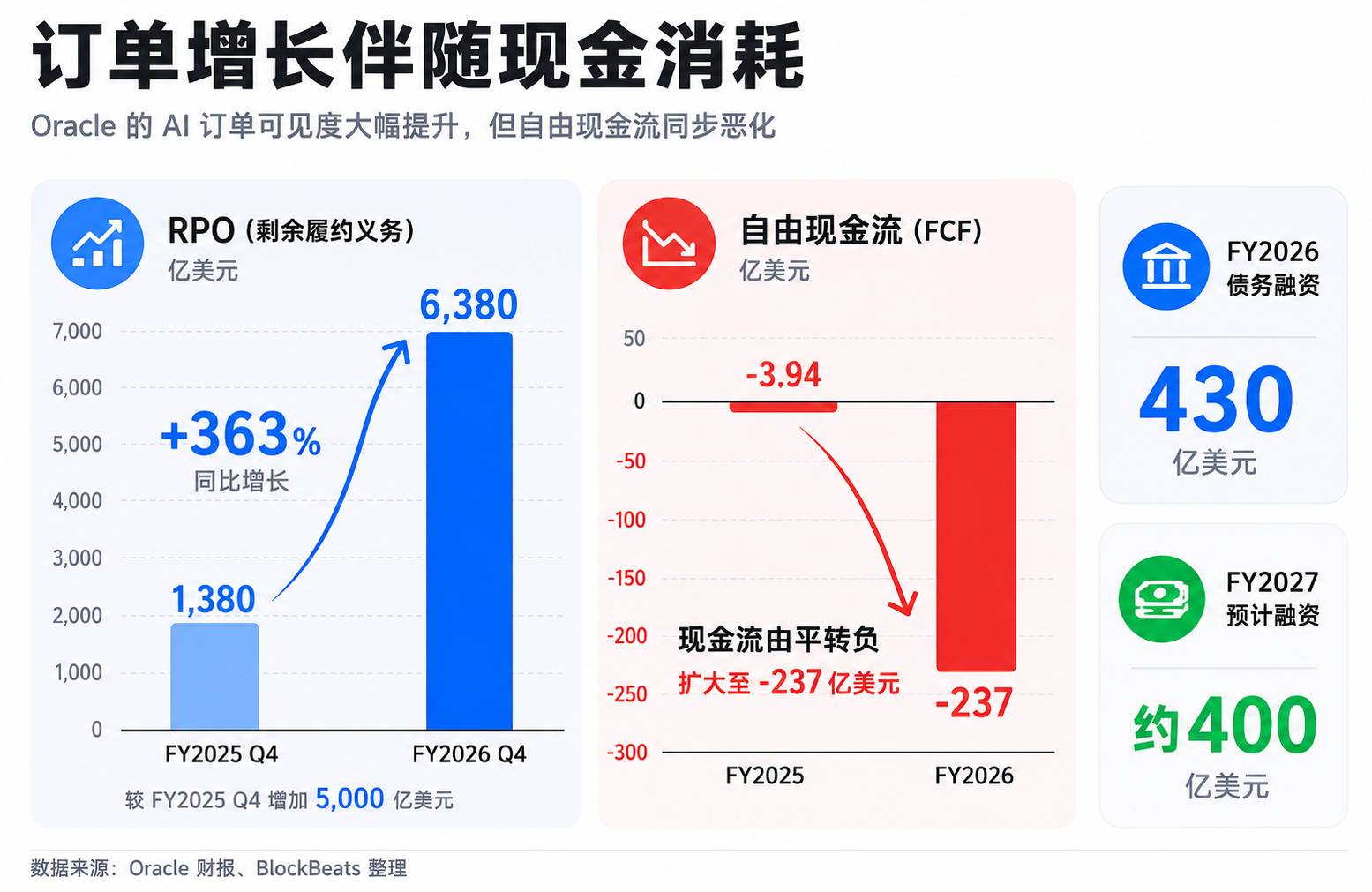

According to Oracle's official financial results, Q4 of fiscal 2026 saw revenue of $19.2 billion, cloud revenue of $9.9 billion, and IaaS (Infrastructure as a Service) revenue of $5.8 billion, up 93% year-over-year. Remaining Performance Obligations (RPO, contracted but not yet recognized revenue) grew from $553 billion to $638 billion. The company's guidance for Q1 of fiscal 2027 was also strong, projecting total revenue growth of 27% to 29% year-over-year, and cloud revenue growth of 57% to 63% at constant currency. Full-year fiscal 2027 revenue guidance stands at $90 billion.

But the market's first reaction wasn't a reward; it was a sell-off. Data shows that Oracle's stock, from its previous close of approximately $205.11 in regular trading, fell to as low as $177.52 in extended trading, a maximum drop of about 13.5%.

This is where the most noteworthy shift in AI trading lies: companies talk about growth, but the stock price asks about the return on investment.

Over the past two years, the market was willing to pay a premium for the narrative of "how big is AI demand." Cloud revenue growth, computing orders, GPU purchases, and partnerships with model companies were all reasons for valuation upgrades. Oracle's reaction this time shows that the same set of good news is being recalculated by the market using a different formula: How much money does the company have to spend upfront to secure these orders? How much does it need to borrow? Will it issue shares? How long will it take for data centers to reach full capacity after delivery? When will gross margins and free cash flow catch up?

AI demand is still there, but AI trading is shifting from "who gets the orders" to "who can make the math work."

Strong Earnings Trigger Financing Concerns

Looking only at the revenue side, Oracle doesn't appear to be a company with problems.

Q4 revenue exceeded market expectations, cloud revenue continued to expand, and IaaS growth was particularly strong. The significant increase in RPO also enhanced the visibility of future revenue. For a company transitioning to AI cloud infrastructure, such data should normally support the narrative that "demand is real."

The company's guidance was also aggressive. It expects both revenue and cloud business to maintain high growth in the next fiscal quarter, with a total revenue target of $90 billion for fiscal 2027. Conference calls and media briefings also mentioned large-scale AI infrastructure contracts, data center delivery progress, and customer collaboration leads, including OpenAI. Clients haven't stopped placing orders, and the demand for AI computing power hasn't suddenly vanished.

The market now focuses not just on order size, but also on the capital consumption behind those orders.

AI cloud is not a capital-light software business. To meet the demands of frontier model companies and large enterprise clients, Oracle must build data centers, purchase or access GPUs, configure networks, power, and cooling systems, and invest significant cash upfront before fully recognizing customer revenue. The larger the orders and the more visible the future revenue, the heavier the upfront investment.

This is the reason "good news becomes a reason to sell." RPO growth indicates future work, but also requires the company to build the capacity. High cloud revenue growth proves strong demand, but simultaneously reinforces market expectations for continued increases in capital expenditure. Investors begin translating the same data into a different question: is this company going to need a much heavier balance sheet to achieve this growth?

Oracle officially disclosed that its free cash flow for fiscal 2026 was -$23.7 billion. The company completed $43 billion in debt financing and $5 billion in equity financing during fiscal 2026. For fiscal 2027, the company expects to raise approximately $40 billion through a combination of debt and equity, including the previously announced $20 billion at-the-market (ATM) equity offering program, and stated it does not anticipate issuing more debt in calendar 2026.

There is also a countervailing piece of information to factor into the valuation. The company stated that customer prepayments or self-supplied GPUs for large AI contracts total $75 billion, which can reduce the amount of capital Oracle needs to raise itself. In other words, the pressure isn't that "Oracle foots the entire bill upfront," but rather that the market needs to confirm whether the remaining financing, depreciation, and operational burdens are still too heavy after accounting for customer prepayments and self-supplied hardware.

Growth still has value, but the market is starting to demand proof that the value of growth exceeds its cost.

AI Infrastructure is More Like a Power Plant Than a Software Subscription

The easiest mistake investors can make with AI infrastructure is treating it like traditional software growth.

The ideal model for a software company is that after the product is built, the marginal cost of acquiring new customers is low, allowing revenue growth to translate quickly into profit. AI cloud is more like a combination of a power plant, a highway, and a warehouse. Before customers can actually use it, the company must first have server rooms, chips, electricity, and networks. Once customers start using it, costs like depreciation, maintenance, energy consumption, and upgrades take effect.

This creates a timing mismatch: cash flow pressure appears first, while profit realization comes later.

Think of it like a restaurant that receives a huge number of reservations and decides to open more locations. The reservations indicate good demand, but opening new locations requires renting space, renovating, buying equipment, and hiring staff. The more reservations, the faster the expansion, and the tighter the upfront cash flow. These reservations only turn into profit when the new locations are full, table turnover rates are stable, and the average spending per customer covers rent and labor costs.

AI data centers follow similar logic, only with much larger amounts, longer cycles, and higher uncertainty.

Oracle is dealing with frontier model companies and large enterprise customers. Their computing needs may be very real and could grow for a long time. But the infrastructure provider must bet upfront: how many GPUs to buy, how much capacity to build, how much electricity to secure, and at what prices to sign long-term contracts. If future utilization ramps up slower than expected, cloud service prices decline, or electricity and hardware costs exceed expectations, today's impressive orders may not quickly transform into high-quality cash flow.

This is also why the market is particularly sensitive to capital expenditure.

Capital expenditure itself is not a bad thing. For cloud providers, expanding capacity is a necessary condition to capture AI demand. NVIDIA, Microsoft, Amazon, Google, and Meta are all on the same chain: someone sells chips, someone builds the cloud, someone trains models, someone integrates models into products. In the past, investors were willing to believe the entire chain would benefit from the expansion of AI demand.

But as capital expenditure grows larger, the market starts to distinguish between "spending money to buy growth" and "spending money to buy profit."

If a company's data centers quickly reach full capacity, customers consistently renew contracts, cloud gross margins improve, and free cash flow recovers, then high capital expenditure is essentially locking in future profits. Conversely, if a company continuously increases investment but needs constant financing to support expansion, and profits are eaten up by depreciation, interest, and operational costs, then high growth will be discounted.

Oracle's decline this time essentially reflects the market reframing AI infrastructure from a "revenue story" back into a "return on assets" framework.

Public Markets Start to Re-evaluate AI Assets

Oracle is not an isolated case; it merely exposed a larger issue prematurely: public markets are starting to compare the quality of AI assets.

In the past, AI trading had a relatively simple hierarchy. Whoever was closest to computing power, closest to models, or best positioned to capture enterprise AI spending enjoyed a valuation premium. NVIDIA became a core holding due to GPU demand. Cloud providers saw revaluations by hosting training and inference workloads. Software companies told stories around AI features and subscription price increases.

Now, the sorting is becoming more granular. Investors are no longer just asking "who has an AI story," but "who can keep AI demand on their income statement and cash flow statement."

For NVIDIA, the market will look at whether customer capital expenditure is sustainable, because chip demand ultimately comes from the budgets of cloud providers and model companies. For Microsoft, Amazon, Google, and Meta, the market will assess whether AI investments translate into cloud revenue, advertising efficiency, subscription growth, or cost reduction. For an infrastructure expander like Oracle, the market's question is more direct: can data center investments generate sufficiently high utilization and returns?

This is also why potential large IPOs can have an impact.

If large private companies like SpaceX, OpenAI, and Anthropic eventually enter the public markets, they might not simply "suck out" liquidity from the Nasdaq—historically, large IPO windows have no stable pattern of impact on tech stock performance. However, they do introduce a real pressure: the public market will gain a new set of AI or tech assets with extremely high valuations, strong narratives, and profit paths that are yet to be validated.

When these assets are placed on the same shelf, investors will start comparing. Buying listed cloud providers means buying more certain cash flows and platform capabilities. Buying model companies means buying a more cutting-edge technological narrative and entry point. Buying infrastructure companies means buying the certainty of computing demand while bearing the pressure of capital expenditure. Buying NVIDIA means betting on the entire AI investment cycle continuing to lengthen.

If risk appetite is high, investors might buy all AI assets simultaneously, believing they are all on the same growth curve. But once interest rates, financing costs, or profit expectations change, the market becomes more selective. Companies with higher revenue certainty, more stable gross margins, and faster cash flow improvement are more likely to have their valuations protected.

Oracle's counter-intuitive decline happened right in the middle of this shift. The AI trade isn't over, but the phase of indiscriminate valuation boosting has become more fragile.

Next Steps Depend on Data Center Delivery

Oracle's sell-off cannot be directly interpreted as the AI bubble bursting. The demand-side data is still strong: cloud revenue, RPO, customer collaborations, and company guidance all suggest that demand for computing power from enterprises and model companies continues. A more accurate description is that the market is starting to decouple pricing for demand and returns.

The most important variable going forward will be the utilization and profit margins of data centers after they are delivered.

If projects are delivered as planned, customer usage ramps up quickly, cloud revenue continues to materialize, and gross margins are not significantly eroded by electricity, depreciation, and maintenance costs, market concerns about high capital expenditure will ease. Today's decline might just be a phase of revaluation: investors first demand a higher risk premium, and then re-evaluate the stock once cash flows are proven.

However, if subsequent earnings reports show that revenue growth still relies on even larger capital expenditure, financing needs continue to rise, free cash flow improves slowly, or equity financing leads to dilution, then Oracle's issue won't just be a stock-specific problem. It will become a sample for changing the valuation framework of AI infrastructure.

The next thing investors need to watch isn't whether AI orders are still increasing, but how much cash flow remains after those orders pass through the costs of data centers, GPUs, electricity, and financing.