6월 CPI 발표: 폭탄은 터지지 않았지만, 후진은 멈추지 않았다

- 핵심 관점: 5월 CPI는 '근원 인플레이션 통제 불능, 6월 즉시 금리 인상'이라는 꼬리 위험을 제거했지만, 명목 CPI 고공행진과 '더 오래, 더 높은' 금리 기대는 여전히 시장을 압박하고 있다. 현재는 분할 매수 창구가 열리는 시기이지, 전량 매수하여 반등을 쫓을时机가 아니다.

- 핵심 요소:

- 미국 5월 근원 CPI는 전월 대비 0.2% 상승에 그쳐 예상치를 하회했으며, '인플레이션의 두 번째 통제 불능'과 6월 즉시 금리 인상이라는 극단적 시나리오를 배제했다.

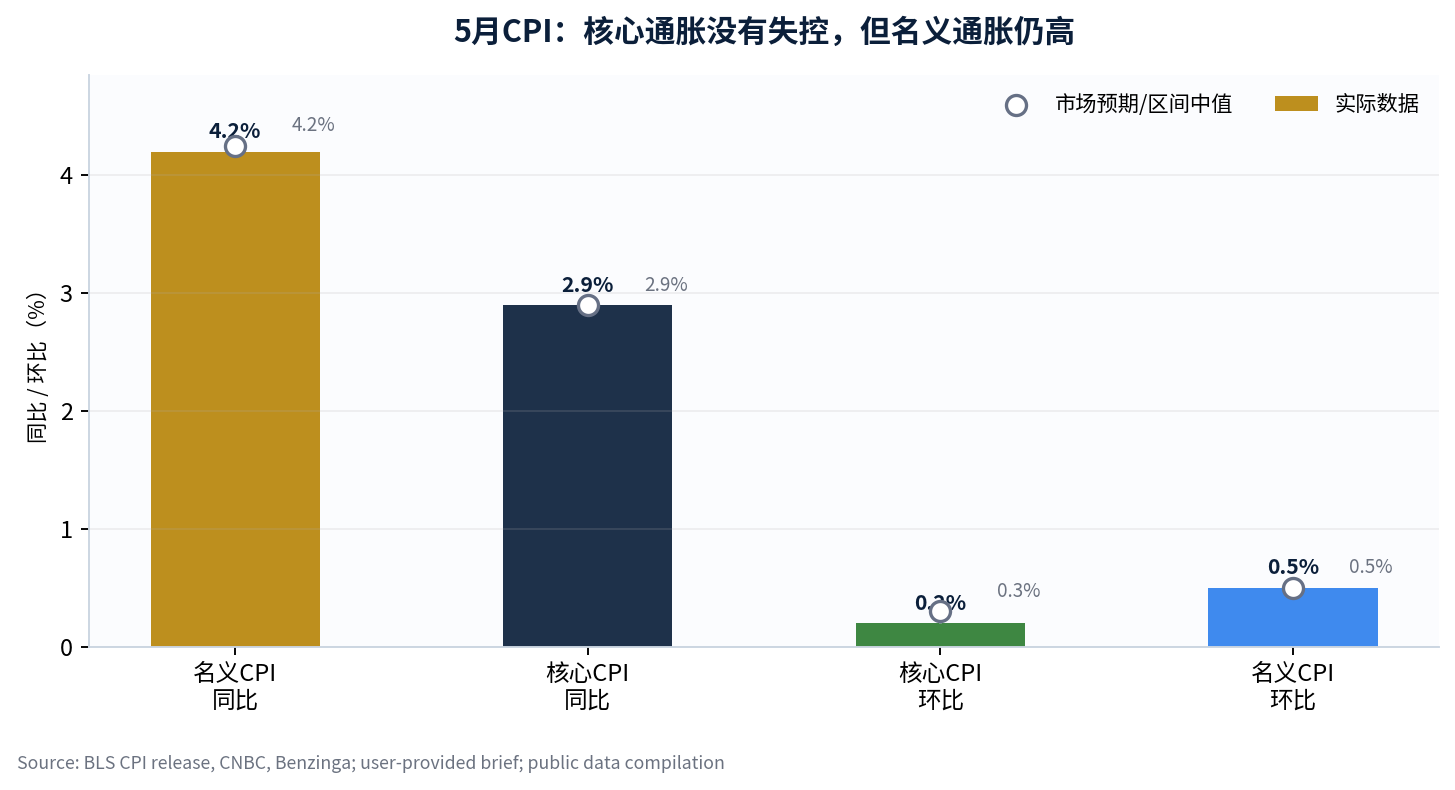

- 명목 CPI는 전년 동월 대비 4.2%로 3년래 최고치를 기록했다. 에너지와 지정학적 갈등으로 채권 시장은 매파적 기조를 유지했고, 올해 안에 한 번 더 금리를 인상할 확률은 약 66%로, '단기적 동결, 장기적 인상'이라는 가격 결정의 분열을 형성하고 있다.

- 반도체 섹터의 레버리지 해소가 심화되면서 SMH와 MU는 고점 대비 각각 약 10.5% 및 17.4% 하락했다. 반면 VIX는 22.22로 마감하며 공포 임계치를 돌파하지 못해, 이는 시스템적 붕괴가 아님을 시사하지만 과밀 포지션이 완전히 청산되지는 않았음을 의미한다.

- SOXS 자금 유입과 SMH 풋옵션 거래량 증가는 기관들이 CPI 호재를 이용한 반등세에서 하방 위험을 헤지하고 있으며, 전면적인 매수에 나서고 있지 않음을 보여준다.

- 전략적 제안: FOMC 회의 전에는 높은 베타와 순수 스토리텔링 종목의 비중을 줄이고, 회의 후에는 EPS 증거가 있는 AI 선두주자, 특히 클라우드 자본 지출의 직접 수혜 부문에 대해서만 분할 매수한다.

Roger Lee | BIT US Stock Special Analyst

21 years of experience in investment banking, asset management, and financial institutions, with a long-term focus on the AI industry chain, US stock macro liquidity, and options strategy research.

Investment Summary

My conclusion is straightforward: The May CPI report defused the "out-of-control core inflation, immediate June rate hike" bomb, but it hasn't brought the US stock market's reversal to a complete stop. Now is not the time for a full-position rebound chase, but rather to use phased deployment and rotation from weak to strong stocks while waiting for the FOMC outcome.

This sentence is the core of how I view last night's market reaction. The US May headline CPI was 4.2% YoY, core CPI was 2.9% YoY, and the core CPI month-over-month was only 0.2%. The data itself did not confirm "secondary inflation失控." However, headline CPI still hit a three-year high, and energy items and geopolitical conflicts continue to push the bond market in a hawkish direction. Therefore, the market did not directly convert the positive CPI news into a stock market rally. [1] [2]

My view is that the current market is not about "blindly buying all dips after negative factors are priced in," but rather that "extreme tail risks have decreased, but crowded trades are still actively reducing risk." SMH has retraced approximately 10.5% from its recent peak, MU around 17.4%, MTUM around 7.5%, and the VIX closed at 22.22, not yet breaking through the panic threshold of 25. This indicates the market isn't experiencing a systemic collapse, but rather semiconductors and high-beta sectors are still in a deleveraging phase. [5]

1. Fact Check: CPI Didn't Explode, But Why Didn't the Market Rise?

The key to the US May CPI wasn't the headline YoY figure itself, but whether core inflation was spreading broadly into the services sector. The original text mentions headline CPI YoY at 4.2%, core CPI YoY at 2.9%, core CPI MoM at 0.2%, and headline CPI MoM at 0.5%. Public reports and official data indicate that energy prices were one of the core drivers pushing headline inflation up. The fact that the core CPI MoM was below the market expectation of 0.3% means that the worst-case scenario—where "the oil price shock is fully spreading to the services sector"—has not materialized, at least for now. [1] [3]

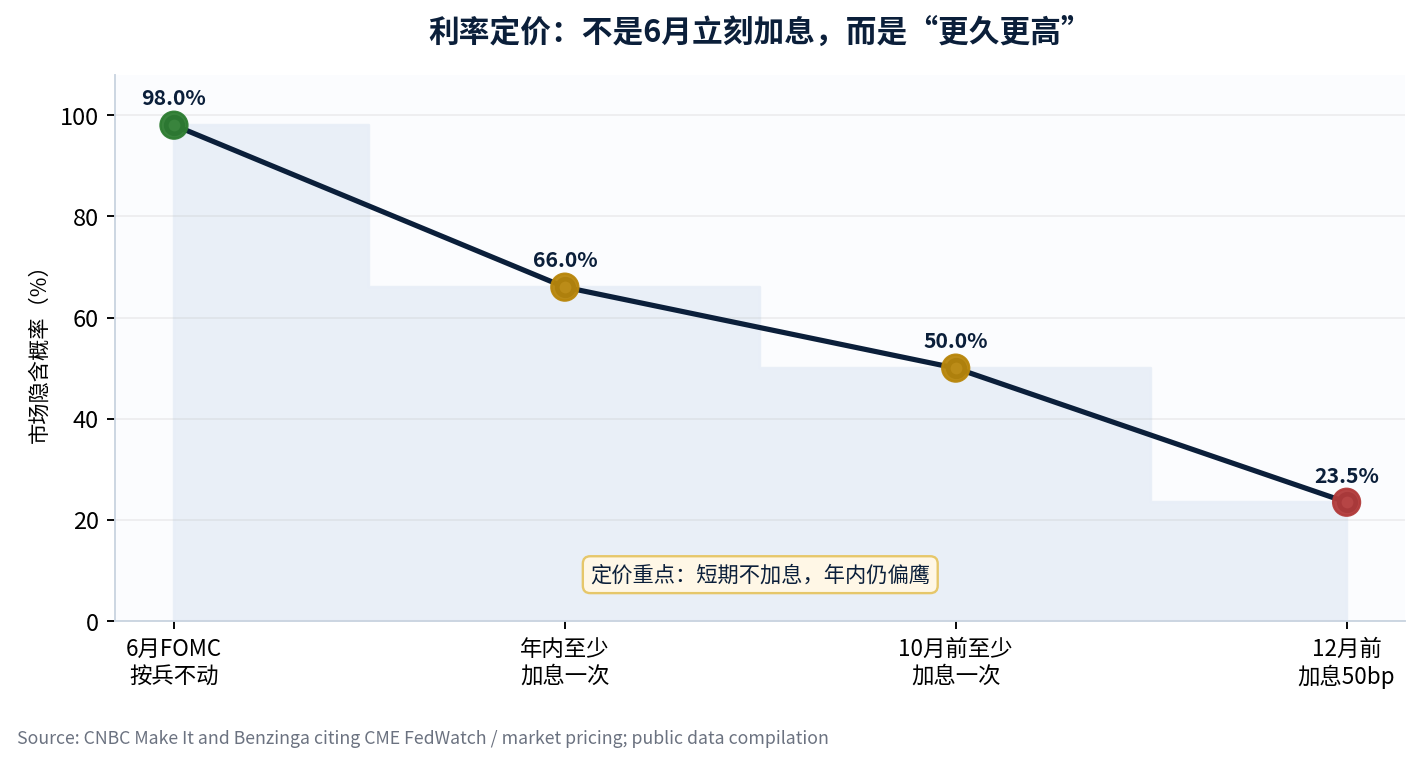

The market didn't rally sharply because equities and bonds are looking at different things. Equities see that core inflation is not out of control, and the AI earnings theme has not been disproven by macroeconomic data for now. Bonds see that headline inflation remains high, oil prices and geopolitical conflicts are uncertain, and the probability of another rate hike this year has risen again. CNBC and Benzinga's recaps of CME FedWatch and market pricing show that the probability of the Fed holding steady at the June FOMC meeting is close to 98%, but the probability of at least one rate hike this year is around 66%. This is precisely the pricing divergence of "no hike now, but higher for longer." [2] [4]

2. Bond-Equity Divergence: The Real Pressure Comes from "Higher for Longer"

The implication of this CPI report is not "immediate rate hike," but "rate cut hopes continue to be suppressed." If the core CPI MoM had been significantly higher than expected, the market would have directly priced in a June or July hike. This extreme scenario has now been ruled out, but the high headline CPI, oil price shocks, and employment resilience prevent the bond market from prematurely betting on easing. The damage to tech stocks is not an immediate fundamental invalidation, but a discount rate constraint on the valuation side.

My assessment is that the bond-equity divergence won't end in a single day. Equities can bounce because core CPI came in lower than expected, but if the 10-year Treasury yield continues to rise, or if Fed communication shifts "another rate hike" from a risk scenario to a baseline scenario, high-valuation tech stocks will continue to face valuation compression. Therefore, leading up to the FOMC, one should not interpret the positive CPI news as a signal to "immediately go all-in chasing highs."

3. Semiconductor Hedging: Surging Hedging Demand Indicates the Reversal Isn't Over

The user's original text points out that the capital inflow into SOXS and the expansion of put option volume for SMH are the most important micro signals in the post-CPI market. My understanding is: institutions are not selling off all AI assets, but are using the rebound to lock in downside risk. In other words, they acknowledge that CPI has defused one bomb, but they don't believe the crowded semiconductor positions have been fully washed out.