CARDS 5.35억 달러 FDV의 잔혹한 진실: 순수익은 4300만 달러에 불과, 수익률 반토막

- 핵심 관점: CollectorCrypt(CC)는 실물 수집 카드와 NFT를 결합한 온체인 블라인드 박스 플랫폼으로, 6억 3500만 달러의 누적 수익 중 90.6%가 즉시 재매입 형태로 사용자에게 반환되어 순수익은 4300만 달러에 불과합니다. 플랫폼은 소수의 고빈도 이용자에 의존해 운영되며, 토큰 가치 포착(재매입+소각)은 순수익의 3.4%에 그칩니다. 수집가 시장은 아직 형성되지 않았으며, 2차 거래는 거의 없습니다.

- 핵심 요소:

- CC의 누적 총수익은 6억 3500만 달러이지만, 90.6%가 카드 재매입 형태로 반환되어 순 유지율은 6.7%에 불과합니다. 일간 활성 사용자는 약 420명이며, 수익은 수십 개의 지갑에 집중되어 있습니다.

- 각 채널의 2차 거래 총액은 500만 달러 미만입니다. eBay 비중은 2025년 1분기 1.23%에서 2026년 2분기 0.10%로 지속적으로 감소하여, 사용자 행동이 수집가 모델과 괴리되어 있음을 보여줍니다.

- 거래량이 고급 카드팩으로 쏠리면서 순이익률이 11.2%에서 5.8%로 반토막 났으며, 구조적인 수익성 압박으로 인해 성장의 한계 수익이 감소하고 있습니다.

- 토큰 가치 포착(소각+재매입) 총액은 140만 달러로 순수익의 3.4%에 불과한 반면, 동일 채널의 운영 지갑에서는 4570만 달러의 USDC가 출금되어 가치 흐름의 현저한 불균형을 보여줍니다.

- 약 5억 3500만 달러의 FDV는 순수익의 7.3배에 해당하며, 내부자 물량의 72%가 2027년 11월까지 잠겨 있어 유통 시가총액은 1억 1000만 달러(유동비율 20.5%)에 불과해, 토큰 이코노미는 잠금 해제 압력에 직면해 있습니다.

Original Author: Four Pillars (@FourPillarsFP)

Original Translation: AididiaoJP, Foresight News

Key Takeaways

- Collector Crypt (CC) has generated a cumulative total revenue of $635 million, with 90.6% returned to users via instant card buybacks, resulting in a net revenue of $43 million and a retention rate of 6.7%.

- Total secondary trading volume across all channels is less than $5 million, with eBay's share dropping from 1.23% to 0.10% (declining for six consecutive quarters).

- Total token value capture (burn + buyback) amounts to only $1.4 million, representing 3.4% of net revenue, while the operational wallet has off-ramped $45.7 million in USDC.

- As volumes tripled towards higher-tier card packs, the net profit margin halved from 11.2% to 5.8%. With each step up in denomination, the blended profit margin is further compressed.

- At the current FDV of approximately $535 million, this corresponds to 7.3 times net revenue for a "casino" with continuously compressing margins, only about 420 daily active players, a circulating supply ratio of 20.5%, and 72% insider supply locked until November 2027.

Introduction

You deposit $1000 into Collector Crypt, open a Grail pack, and receive a tokenized Pokémon card with a platform valuation of $1015. It looks like you made a profit. Turbo mode automatically activates, selling the card back to the protocol at a 93% buyback rate, and $944 is credited to your account instantly. The entire cycle takes just a few seconds.

This cycle, rapidly repeated by hundreds of wallets, has generated $635 million in volume and created an FDV of approximately $535 million for the CARDS token. This article will dissect the composition of this volume, whether the collector economy priced into the token is materializing, and what share of revenue the token actually captures.

Note: Collector Crypt (CC) is an on-chain gacha (blind box) platform that combines physical collectible cards (primarily graded cards like Pokémon and sports cards) with NFTs. Users deposit USDC to purchase random card packs at various price points ($25 to $2500+). Upon opening, they receive an NFT card backed by a physical graded card. The platform offers an 85%~93% instant buyback (Turbo mode enabled by default), allowing users to sell the card back to the platform for USDC within seconds, creating a rapid cycle.

What Exactly is This $635 Million?

90.6% of Cumulative Volume is Returned to Users Within Seconds

CC's core product is a gacha machine. Users deposit USDC, purchase random card packs ($25 to $2500, with a $5000 tier in the API but not yet publicly available), and receive an NFT card backed by a physical graded card. Each card has an "insurance value," and the platform offers an 85%–93% instant buyback.

Buyback is the default behavior, not an exception. All 33 machine configurations in the CC API have turboMode: true enabled. Cards are automatically sold back to the protocol, and users receive the net USDC (after the spread is deducted) within seconds.

According to Blockworks data as of June 13th, cumulative revenue is $635 million. Of this, $576 million was returned to users via card buybacks, resulting in a net revenue of $43 million and a retention rate of 6.7%. Here, "buyback" does not refer to token buybacks but rather the platform repurchasing the card it just sold, cycling the same deposit into the next draw.

On the ATH day of June 11th, the machines processed $10.6 million in volume, retained $881,000, for a retention rate of 8.3%.

The DeFiLlama adapter source code confirms this breakdown: dailyFees = pack_purchases + royalties - buybacks. This means the approximately $52 million annualized fee shown on the dashboard is already the net value after deducting buybacks. dailyVolume = pack_purchases, which is the gross spending before the cycle deduction. This is the number displayed on protocol volume rankings.

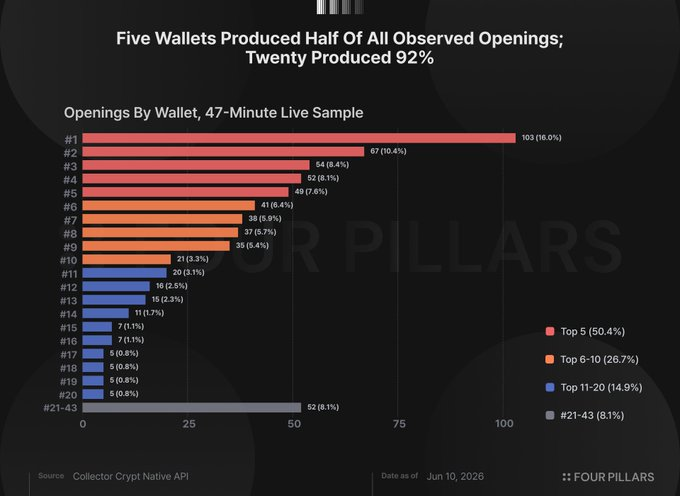

Volume is Highly Concentrated Among a Few Dozen Wallets

Blockworks reports a cumulative total of 23,333 users. In May 2026, the platform had approximately 420 daily active users, with a daily average volume of $3.3 million, translating to roughly $7,800 per person per day. Even if 400 of those 420 people each spent $1,000 daily, the remaining 20 wallets would still contribute $2.9 million, accounting for 87% of the total volume. Extreme concentration is a mathematical certainty given the average.

Actual activity confirms this. We polled CC's public win count 20 times over a 47-minute window on June 10th, de-duplicating by NFT address. The sample included 645 pack openings from 43 wallets. The top 5 wallets accounted for 50.4% of openings, the top 10 for 77.1%, and the top 20 for 91.9%. The single most active wallet contributed 103 openings, or 16% of the total.

This is only a 47-minute window, not a full-time distribution. But both the averages and the sample point in the same direction: this $635 million represents a casino with a 6.7% retention rate, fueled at industrial speed by a few dozen high-frequency players.

The Collector Market Has Not Yet Arrived

The Bull Case

The strongest bull narrative deserves stating: the buyback cycle is the product itself. The act of opening packs *is* the entertainment. The 85%–93% return rate means users lose money slowly, and the instant liquidity of physical cards in the vault represents a product innovation. As a piece of consumer design, this is defensible.

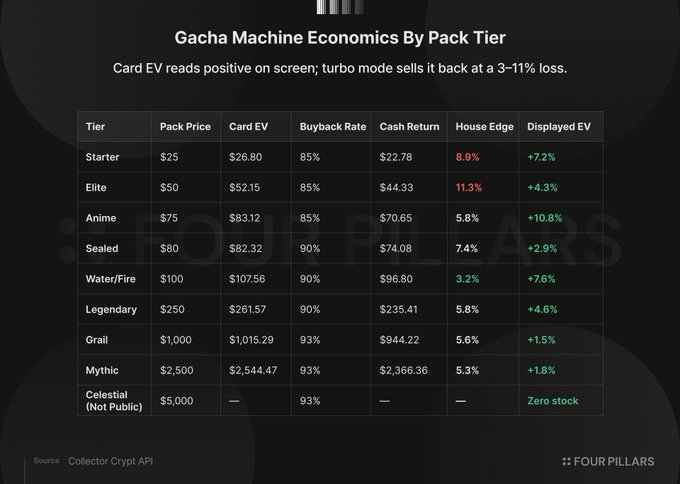

However, the machine configurations reveal the direction of design optimization. CC independently controls two variables: the insurance value assigned to the card, and the buyback rate for the automatic turbo sale. The tier ranges and vault inventory are configured so the probability-weighted expected card value is higher than the pack price. The buyback rate then discounts this value below the price.

For example, a $1000 Grail pack displays an expected card value of $1015, presenting the user with a +1.5% proposition. Turbo mode activates at a 93% buyback rate, returning $944 in cash. The card EV is above the pack price, the pack price is above the cash return; the user sees the former comparison, and the platform profits from the latter. All tiers share the same structure, with the edge varying from 3.2% to 11.2%.

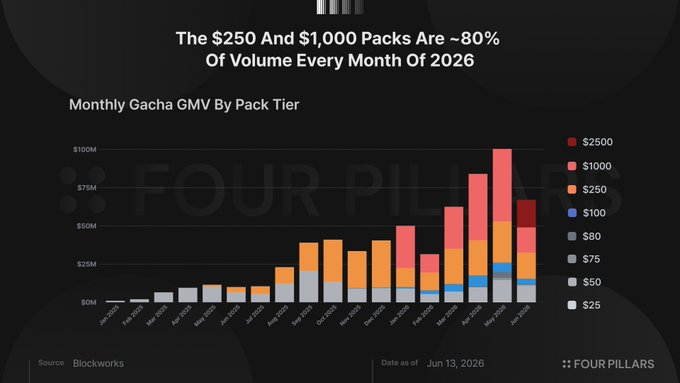

Spending patterns confirm the user type. In each month of 2026, the $250 and $1000 tiers together accounted for roughly 80% of total volume (79.4% in Jan, 80.6% in Mar, 79.4% in Apr). Collectors would buy specific cards at specific prices to complete specific sets. A distribution dominated by $1000 random packs is the distribution of high-roller players.

Secondary Trading Below 1%, eBay Share Down 12x

If collectors were using this platform, they would trade with each other, and cards would flow into the broader market. CC data tracks both on and off-platform activity, and both are near zero.

On-platform, cumulative marketplace royalties total $133,000. Of the $6.9 million in lifetime marketplace volume, only $823,000 represents genuine peer-to-peer trades, the rest being buyback flows and legacy V1 volume.

Off-platform, Blockworks tracks eBay sales of CC vault cards. The cumulative total is $3.4 million, but the trend is the key finding. As a share of gacha flow, eBay was 1.23% in Q1 2025, 0.46% in Q2, 0.89% in Q3, 0.30% in Q4, 0.17% in Q1 2026, and 0.10% in Q2 2026. Over the same period, gacha volume grew approximately 25x. The absolute value of the collector channel barely moved, while its share plummeted 12-fold.

Of the $635 million in card value generated by the platform, only $18.5 million worth of cards were redeemed for physicals, a 2.9% share. The remaining 97% was sold back to the protocol via automatic buybacks, mostly within seconds.

Combining all channels (eBay + peer-to-peer marketplace trades), genuine secondary activity totals less than $5 million, against a gacha throughput of $635 million. The standard bull rebuttal is "it's early," but the quarterly eBay sequence answers this. The platform is not on an early trajectory towards collector behavior; it has been demonstrably moving away from it for six consecutive quarters.

Turbo mode eliminates the dwell time that collector platforms depend on for monetization—browsing, comparing, collecting—the time that builds secondary markets. The design optimization is for cycle speed, not discovery. These are two different products.

Token Utility

CC's revenue flows through three layers. Users deposit USDC to buy gacha packs, receive random card NFTs, and in nearly all cases, automatically sell them back at an 85%–93% buyback rate. The platform retains the 7%–15% spread as net revenue. Secondary revenue lines include a 2% royalty on marketplace trades and a 2% fee when users redeem NFTs for physical cards. All net revenue flows into the operational treasury, used for card inventory purchases, USDC off-ramping, and, since June 2026, a small token buyback program.

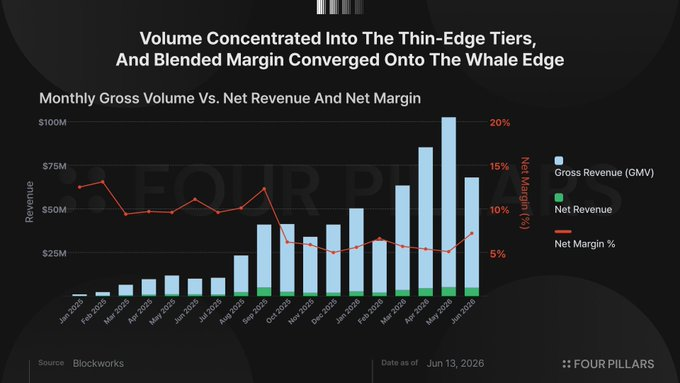

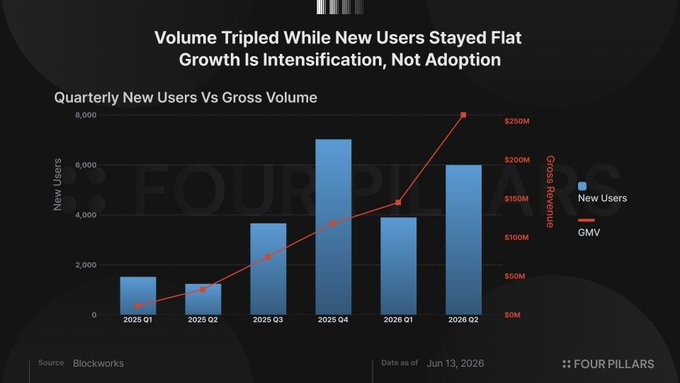

Volume Triples, Profit Margin Halves

According to Blockworks daily data, gross volume in Q3 2025 was $75 million with a net profit margin of 11.2%; Q4 saw $116.3 million in gross volume with a 5.7% margin; Q1 2026 had $145.9 million in gross volume and a 5.9% margin; Q2 up to June 13th had $256 million in gross volume with a 5.8% margin.

The compression is structural. The thinnest margins are in the highest volume tiers—around 5% for the $250 and $1000 packs—compared to 9%–11% for the $25 and $50 tiers. High-volume players will not cycle six-figure sums of capital at an 11% spread. As volume concentrates in higher tiers, the blended margin converges towards the higher-tier edge. The marginal dollar of growth comes from the players the platform retains the least.

The $2500 Mythic pack, launched on June 10th, has a 6.4% profit margin. The API already lists a $5000 Celestial pack (with zero inventory). With every step up in denomination, gross volume continues to grow, pulling the blended margin down towards the lower bound of the higher tiers.

User data confirms that growth is intensification, not adoption expansion. New users over the past four quarters were 3,668; 7,013; 3,886; and 5,982 (Q2 up to June 13th), remaining roughly flat, while volume more than tripled. In May 2026, 2,593 new users joined, but daily active users increased from ~280 in April to 420 in May. Most new users churn within days.

Token Value Capture: $55,900 Burn + $887,000 Buyback

Since its launch, 294,203 CARDS tokens have been burned, representing 0.015% of the supply, valued at approximately $55,900 over 9.5 months. CC's documentation doesn't specify the mechanism triggering the burn, and the downward trend aligns with a collapse in market activity. In May 2026, 372 tokens were burned; in June, 21 tokens were burned, worth $4.

On June 13th, Lukas Ruppert of Maelstrom published on-chain evidence linking token purchases to wallets associated with CC's operational infrastructure. Ruppert traced from CC's known operational center (DFEst) through Kraken to DCA bots, identifying linked wallets with pack-opening histories. He did not fully confirm team control but wrote, "If these wallets are indeed controlled by the team, the implications go far beyond the purchases themselves," noting the circumstantial evidence is strong.

The on-chain trail reveals two events. On May 12th, the CARDS Aggregator wallet paid $500,000 through a Fireblocks custodian to pre-seed investor GSR, receiving 4,045,013 CARDS at approximately $0.124 each. Subsequently, on June 10th and 11th, a newly created wallet funded via Kraken began market-buying CARDS via DCA bots, running two parallel streams of ~$625 and ~$587 every 2–6 minutes. By June 12th, the bots had deployed $159,000, accumulating 599,104 CARDS, with a remaining budget of $728,000.

Calculating all forms of token value capture: burn ($55,900), GSR settlement ($500,000), full DCA budget including undeployed funds ($887,000), totals $1.4 million. This represents 3.4% of the platform's cumulative $43 million net revenue. At the Q2 run rate of approximately $73 million annually, the entire DCA budget equals 1.2% of one year's net revenue.

The wallet identified by Ruppert as CC's operational center has off-ramped $45.7 million in USDC, including $8.5 million since May 2026. Regardless of whether these wallets are controlled by the team, the disproportionality is notable: $1.4 million flowing to the token, $45.7 million flowing out of it. The buyback may be the beginning of sustained value capture, but at the same time, the program has nothing on-chain, isn't automated, and isn't committed. It could stop tomorrow.

At a 5.8% net profit margin, a large-scale increase in token buybacks is a zero-sum game with operational wallet revenue. The buyback rate (85%–93%) determines the player's cost per cycle; lowering it would destroy volume. Therefore, the total profit margin is dictated by player tolerance. Within this margin, token buybacks and operational cash-outs compete for the same pool of funds.

Even taken at face value, with an annualized Q2 run rate of ~$73 million, the ~$535 million FDV implies a 7.3x multiple on net revenue. This is for a casino with continuously compressing margins, ~420 daily players, and a highly concentrated revenue base (a single wallet exiting could move daily volume by double-digit percentages).

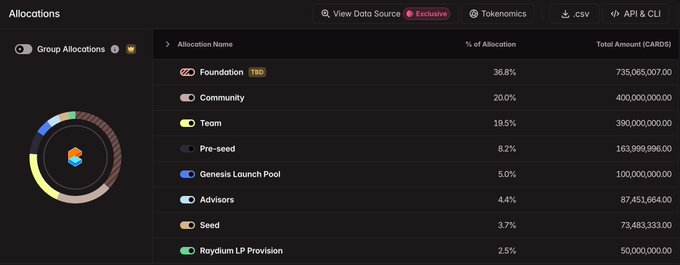

The ~$110 million circulating market cap reflects a 20.5% circulating supply ratio, with 410 million of the 20 billion total supply in circulation. The remaining 79.5% is locked according to a public schedule until November 2027. The next unlock on June 29th releases 28.84 million tokens distributed across four allocations. Insider allocations comprise 72% of supply (Foundation 36.75%, Team 19.5%, Pre-Seed 8.2%, Advisors 4.37%, Seed 3.67%), while Community gets 20%, Genesis Launch Pool 5%, and Raydium LP 2.5%.

Conclusion

CC has built a product that places physical cards in a vault and has found product-market fit with a small group of high-speed gamblers. Our view would change if marketplace royalties shifted towards genuine peer-to-peer trades, if the eBay share reversed its six-quarter downtrend, or if the buyback program scaled significantly beyond the current 3.4% of net revenue. None of this is currently visible.

What is currently visible is: total token value capture of $1.4 million, representing 3.4% of cumulative net revenue, against a $110 million market cap ($