Suzhou’s 30 million yuan investment from 18 years ago has grown into the veins of AI

- Core Thesis: Using the growth journey of Zhongji Innolight (formerly Suzhou Innolight Technology) as a central case study, this article explains how Suzhou, through a systematic, long-term industrial investment strategy, captured the key supply chain node of optical modules in the AI computing power wave. This has driven urban industrial upgrading, capital appreciation, and talent aggregation, creating a sustainable “flywheel effect.”

- Key Elements:

- During the 2008 financial crisis, Oriza Holdings invested 30 million yuan in the niche field of optical module startup Suzhou Innolight Technology. Eighteen years later, this investment transformed into the A-share giant Zhongji Innolight, with a market value exceeding 1.5 trillion yuan, surpassing Moutai.

- Suzhou has precisely bet on the optical communication industry chain within the AI sector. Besides Zhongji Innolight, it has nurtured companies like TFC Communication and Yuanjie Technology, which cover the entire spectrum from optical chips and components to modules and testing.

- Suzhou’s investment logic lies in "selecting projects while squatting on the ground": in the early stages, through mechanisms like the Technology Investment Promotion Center and chain-anchor funds, it leverages market-based methods and knowledgeable talent for long-term布局 in niche tracks such as biomedicine, nanotechnology, and voice AI.

- Suzhou's pragmatism stems from its "poor origins" with a weak industrial base. Through methods like "Sunday Engineers" and self-funded development zones, it integrated into Shanghai's industrial chain, building a solid industrial foundation and an entrepreneurial spirit of self-reliance and risk-taking.

- As companies grow, Suzhou’s 4.89 trillion yuan in industrial output and comprehensive range of categories provide natural data and application scenarios for industrial AI. Computing power becomes a public service, feeding back into the industry, forming a positive cycle of mutual empowerment between the city and its enterprises.

Original author: Sleepy, Daria

Original editor: Cozzy

The most lucrative investment in Suzhou was made during the global financial crisis.

In the autumn of 2008, as Lehman Brothers collapsed, venture capital across China nearly ground to a halt. Firms cut losses, investors waited on the sidelines, and the primary market entered a deep freeze. It was in this window that Yuanhe Holdings, the state-owned venture capital platform of the Suzhou Industrial Park, invested approximately 30 million RMB in a startup company.

The founder was Liu Sheng, a Tsinghua University undergraduate, Georgia Tech PhD, and a veteran of North America's optical communications industry, having worked at Lucent Technologies and Opnext. In 2008, he returned from Silicon Valley, registered InnoLight Technology in Suzhou, and aimed to produce high-speed optical modules.

In the 2008 investment landscape, optical modules were not just a niche; hardly any investors were looking at this sector. Domestic optical communication companies were all crowded into the telecom market and low-to-medium-end manufacturing. According to a LightCounting report, only one Chinese company, WTD, ranked among the top ten global optical module suppliers in 2010, later merged into Accelink Technologies, barely making the list's tail end. Back then, the judgment that "cloud computing data centers would require a massive number of high-speed optical modules" was far from any consensus.

Eighteen years later, that investment grew into Zhongji Innolight. Just before the Dragon Boat Festival in June 2026, its stock price surged to 1,367.88 yuan, giving it a total market capitalization of 1.5 trillion yuan, ranking among the top ten in A-shares and surpassing Kweichow Moutai.

The Blood Vessels of AI

Optical modules are crucial to the entire AI industry. Without them, AI is just a pile of heat-generating silicon chips. To transmit signals from a chip through optical fibers between data centers, you need optical modules.

Compute power is the heart; optical modules are the blood vessels.

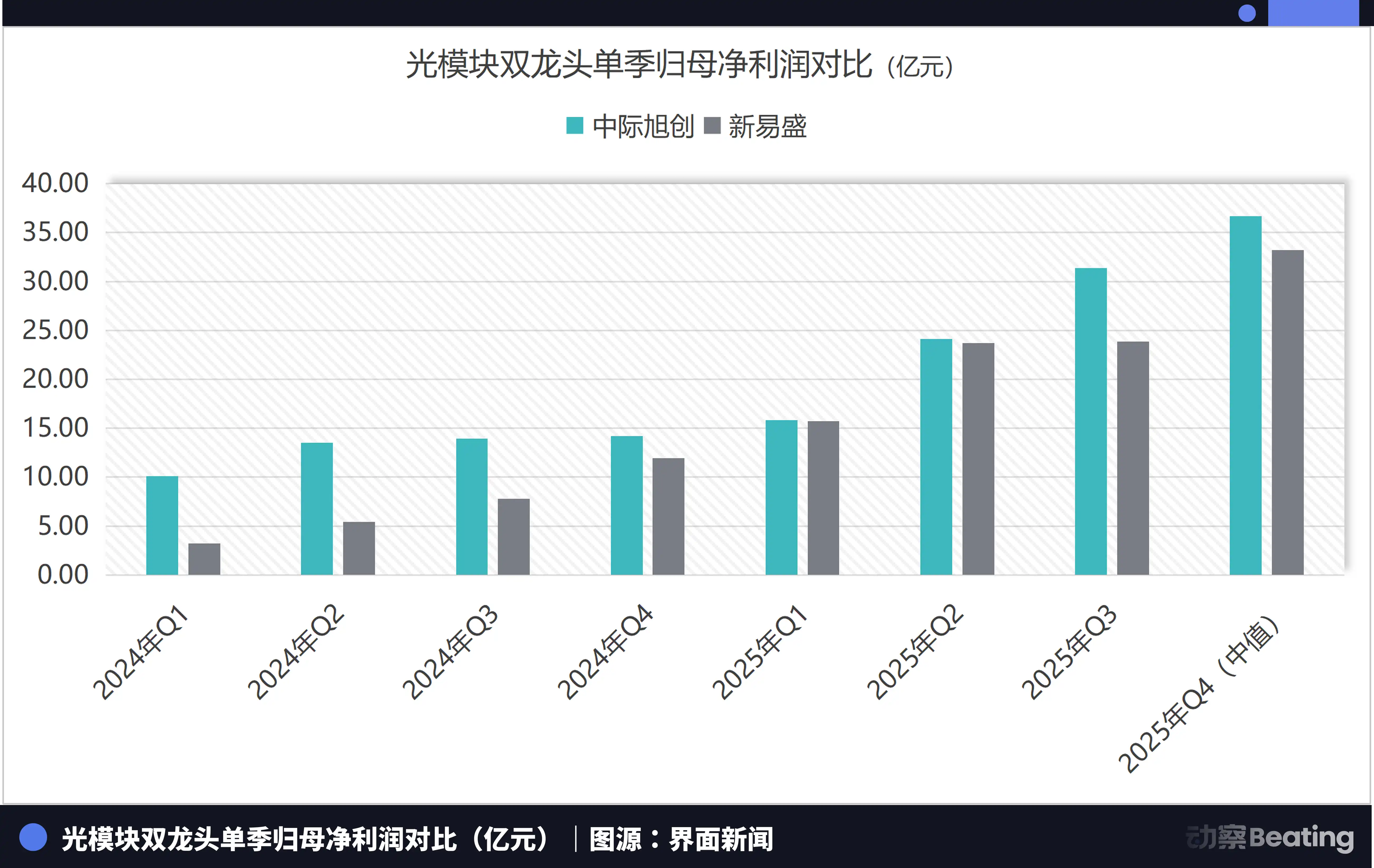

In A-shares, Eoptolink, Zhongji Innolight, and TFC Communication are known as the "Yi Zhong Tian" (a play on the three names). These three optical module giants capture the most critical segment of the global AI compute supply chain. Two of the three are based in Suzhou. Zhongji Innolight's Suzhou operational headquarters is in the Suzhou Industrial Park, and TFC Communication's operational headquarters is also there.

Furthermore, Suzhou-based company Lianxun Instruments, which manufactures high-end optical communication testing instruments, saw its stock price surge over twenty times its IPO price less than two months after listing in 2026, claiming the title of A-share stock king. Yuantjie Technology, a leader in active optical chips and a portfolio company of Zhongji Innolight, saw its stock price touch 1,712 yuan just before the Dragon Boat Festival, quadrupling in six months.

Breaking down the AI data center, Suzhou didn't just bet on a few companies; it captured a chain of interconnected positions.

Further upstream are optical chip companies like Yuantjie Technology. Downstream sits the optical device domain specialized in by TFC Communication. Zhongji Innolight packages these devices into high-speed optical modules, supplying global data centers. Lianxun Instruments then provides the testing equipment to ensure these high-speed optical communication devices run stably.

According to a Xinhua Daily report, the total market cap of A-share listed companies from Suzhou has exceeded 4 trillion yuan, ranking fourth nationally, behind only Beijing, Shanghai, and Shenzhen.

Hangzhou's "Six Little Dragons" made it to the Spring Festival Gala and trending topics. Shenzhen's humanoid robots are dancing. Shanghai's three GPU companies are telling a grand story of domestic substitution. These stories are engaging, novel, and visual—a 15-second short video can etch a name in memory.

But Suzhou tells a different kind of story.

An optical fiber manufacturer in Wujiang saw its 2026 sales revenue grow over 35% year-on-year, with production capacity already booked into 2027. Multiple companies in Suzhou's industrial chain jointly invested to construct the nation's first mass production line for 8-inch silicon photonics chips. Suzhou's optical communication industry has coalesced into a hundred-billion-yuan cluster, with companies establishing over 50 innovation consortia. In the first quarter of 2026, the industry's scale grew over 60%.

In this AI compute explosion, real money first flowed into the places building the "blood vessels."

For Suzhou, the growth of an optical module leader brings more than just market capitalization. It pulls along suppliers, testing equipment makers, optical chip companies, funds, and talent. Its orders become production capacity for upstream and downstream firms. Its listing becomes credit for the local capital market. Its judgment on the industry, in turn, provides leads for Suzhou's next round of investment attraction and business development.

Beyond the book gains from the investment, what Suzhou truly earned is a continuously rolling industrial chain.

When the world suddenly discovered optical modules in 2024 and rushed into the secondary market to grab shares, Suzhou's name was already written on InnoLight's earliest business registration documents, a shareholder since 2008.

Picking Projects on the Ground Floor

Why was Suzhou able to make this bet?

Some say it was foresight, the ability to spot talent, a visionary perspective. But these are all 20/20 hindsight statements.

You need to stand tall to have vision. Suzhou wasn't standing tall; it was squatting on the ground, examining projects one by one, interviewing people individually, and then making a judgment.

The person who made that decision for the city was Dai Yu, the Yuanhe Holdings executive in charge of the InnoLight project. Years later, in a media interview, she recalled that the initial contact with InnoLight came through the industrial park's "Leading Talent Program." A large number of high-end talents were returning to China with projects. Yuanhe screened them one by one and chose to invest in InnoLight.

Yuanhe later used three different funds across various stages, plus a debt platform, to make round after round of follow-on investments. It also brought in Data Capital from the Dongshahu Fund Town to co-invest. Restructuring documents show that the Yuanhe system held over 7% of InnoLight's equity in total.

From the initial investment on the eve of the 2008 financial crisis to InnoLight's backdoor listing via Zhongji Equipment in 2017, Yuanhe traversed an entire economic cycle.

Around 2011, InnoLight's 40G products passed Google's certification, leading to contact with Amazon and Huawei. In 2014, Google Capital led a $38 million Series C round, Google's first investment in China. InnoLight initially planned to list in the US, but the 2015 valuation winter for Chinese concepts stocks forced it to dismantle its VIE structure and seek a path back to A-shares.

In 2017, Zhongji Equipment acquired 100% of InnoLight for 2.8 billion yuan, completing the backdoor listing. Zhongji Equipment's controlling shareholder, Wang Weixiu, made the bold decision to grant significant autonomy to the InnoLight team. The New Fortune magazine described this decision as having "grand vision." By 2026, the net worth of Wang Weixiu and his son Wang Xiaodong had soared to 97.8 billion yuan, jumping from 161st to 30th in the wealth rankings. The owner of a small company making motor winding equipment, by acquiring a Suzhou-based optical module startup and having the wisdom to delegate management, saw his personal wealth approach 100 billion yuan.

In 2025, Zhongji Innolight reported revenue of 38.2 billion yuan and a net profit of 10.8 billion yuan, doubling year-on-year. In Q1 2026 alone, quarterly revenue reached 19.5 billion yuan, up 192% year-on-year, with net profit hitting 5.7 billion yuan, up 262%. The tree has grown into a forest. Innolight, through its subsidiaries, has invested in a chain of industrial players like Jingyan Intelligent, Aoke Optoelectronics, and Laixin Optoelectronics, and also contributed funds to Yuantjie Technology, the new A-share king.

Looking back at Suzhou's investment record over the past two decades, Innolight is not an isolated case. In 2006, when "innovative drugs" were not yet a capital market keyword, Suzhou established BioBAY. Today, it houses hundreds of pharmaceutical companies, with over thirty having gone public. In the same year, when nanotechnology was far from industrialization, Suzhou began attracting national-level nanoscience research institutions. In 2008, a Suzhou investment team went to Cambridge, UK, and persuaded the voice AI startup AISpeech to relocate to Suzhou. That was nine years before the national "New Generation Artificial Intelligence Development Plan" was issued.

Biomedicine, nanotechnology, voice AI, optical modules. Four sectors, all invested by Suzhou when others couldn't see the potential.

Underpinning this strategy is a system that is not particularly glamorous but exceptionally robust. In 2006, the Suzhou Industrial Park established the country's first specialized technology investment attraction center. By 2022, all personnel in the investment attraction department held master's degrees or higher, mostly in science and engineering. Suzhou currently has 212 investment promotion agencies and over 2,000 full-time staff. Among these, 119 are state-owned companies, free from bureaucratic constraints, hiring with market-based salaries, and able to directly invest in enterprises – precisely the functions the government wants to perform but can't achieve through administrative means.

For investment decisions, Suzhou also pioneered the "Chain Leader Fund," allowing the industry chain's leading companies to act as fund managers, with government money following their lead. In the biomedical chain leader fund, Innovent Biologics and Jiangsu Alphamab directly serve as managers, participating in project selection and post-investment management. Over a dozen such chain leader funds have accumulated investments exceeding 20 billion yuan.

So, Suzhou wins its bets not due to luck, but by turning "gambling" into a stable system. Screening projects with knowledgeable people, relying on industry veterans for judgment, and betting with patient capital over a decade or more.

This is more than just foresight.

Three Generations

This persistent, painstaking effort was born from poverty.

In the early days of reform and opening up, Suzhou's industrial foundation was very weak. Equipment was old, the industrial structure was backward, and both raw materials and sales channels were difficult to secure. So, they had to make whatever they could and learn from whoever they could.

The "Shanghai Sunday Engineers" phenomenon was a product of that era. Suzhou's township enterprises would invite engineers from Shanghai's state-owned factories to guide production during their weekends off. By 1988, there were over 15,000 township enterprises. In 1992, the output value of township industries accounted for over 70% of the city's total.

Yet, even having achieved this, when the nation designated Special Economic Zones and Economic and Technological Development Zones, Suzhou didn't get any.

Policy dividends could not be waited for.

The people of Kunshan simply decided not to wait. They pooled together 500,000 yuan to establish the country's first self-funded development zone, bearing all the risk themselves, and went to Shanghai to place investment ads. By adopting the clear, somewhat humble positioning of "doing what Shanghai doesn't want to do" and "Shanghai handles zero-to-one, Suzhou handles one-to-ten," Suzhou wedged itself into the Shanghai-dominated industrial chain and completed its initial industrial accumulation.

Later, Suzhou learned "door-knocking investment" from Singapore, setting up investment offices globally and proactively approaching companies one by one. By 2012, the actual utilized foreign capital in Suzhou accounted for 8.1% of the national total, a 131-fold increase from 1990.

Later, production costs rose, environmental capacity reached its limit, and labor-intensive industries began to move out. Once again, Suzhou had no choice but to face the pains of industrial transformation head-on.

Within a 25-square-kilometer radius around Nanjing Road in the Taicang High-tech Zone, over 800 small and medium-sized foreign-invested enterprises form a complete automotive supply chain, capable of sourcing 70% of a vehicle's parts locally. In Shenze Town's Silk Road Nanhua Cross-border E-commerce Industrial Park, a single 20-story building houses 86 textile enterprises, covering everything from raw materials, fabrics, finished products to sales—upstairs and downstairs are the upstream and downstream.

These industrial clusters weren't planned; they grew organically, one enterprise, one order at a time, over decades.

In the 1980s, they used weekends to learn from Shanghai engineers. In the 1990s, they risked 500,000 yuan of their own money on a development zone. In 2008, they risked 30 million yuan on a niche returnee making optical modules.

When no one saw promise, they used their own money to buy what was then worthless. Three generations repeated the same action three times.

Visionaries choose their sectors from a height. Those with no choice squat on the ground, pick up what others discard, clean it off, and wait for it to become valuable. Suzhou's pragmatism is the survival strategy of a prefecture-level city that never received a special zone license. The strategy, used for thirty years, became ingrained. By 2008, when Dai Yu was faced with InnoLight's business plan, the cognitive circuit she used to make her judgment was the same one Kunshan people used thirty years prior when they scraped together 500,000 yuan.

This thing isn't valuable now. But it's worth the gamble.

So they bet.

The Flywheel Spins

And after winning the bet?

A single investment growing into a trillion-yuan company is just the first layer of return.

It begins to rewrite a city's industrial structure. The capital market becomes more active, the industrial chain more complete. AI finds real manufacturing scenarios. Young people have more reasons to stay.

The relationship between the city and the company reverses at this point. In the early days, Suzhou helped the enterprise onto the poker table. As the enterprise matures, it becomes Suzhou's reason for continuing to attract projects, talent, and capital.

The numbers in Suzhou's books look excellent. In 2025, the total output value of industries above a designated size was 4.89 trillion yuan, ranking second nationally. High-tech industry output value grew by 6.7%, accounting for 56.2% of the total, up 1.5 percentage points from the previous year. Twelve companies held their A-share IPOs, ranking first nationally and surpassing Beijing, Shanghai, Guangzhou, and Shenzhen. One out of every ten newly listed companies in the country came from Suzhou. The city's per capita disposable income for all residents was 80,796 yuan, exceeding 90,000 yuan in urban areas, trailing only Shanghai, Beijing, and Shenzhen nationally—all while being just a prefecture-level city.

Among the top ten GDP cities, Suzhou's service sector accounted for only 52.9%, the lowest proportion. While other metropolises have long been transitioning towards the service industry, Suzhou is still relentlessly manufacturing things.

Suzhou has 160,000 industrial enterprises, covering 34 of the 41 broad industrial categories and 514 sub-categories. It is one of the cities with the most complete range of industrial sectors nationally, and even globally. For industrial AI, this means data—high-quality, continuous, large-scale production data generated daily on the factory floor. For other cities trying to build industrial large language models, the first step might be to find data. Suzhou doesn't need to look. Its factories are the data source; models trained on this data can be validated and iterated on the same production lines. The production line is both the source for AI learning and the endpoint for AI to generate value.

On a base of 4.89 trillion yuan, even a one or two percentage point efficiency gain driven by AI represents tens of billions in absolute growth.

Suzhou has also turned computing power into a public service. The industrial park established a public computing power service platform. Companies submit their needs, get matched with providers within 24 hours, sign a contract within a week, and can receive a 20% subsidy. The platform's operations manager likens it to ordering takeout—choose the style, portion, and delivery time, then click to order. For a startup that can't afford the computing power of tech giants, the ability to "order takeout" like this can mean the difference between life and death.

Once the flywheel starts spinning, what do ordinary people gain?

Let's look at some data. In 2025, urban areas added 415,000 new jobs, accounting for nearly 30% of Jiangsu Province's total. Additionally, 283,000 college graduates chose to stay in Suzhou. They didn't come for the name of a talented founder; they came for the real opportunities to work, find housing, and build a life.

In the workshop of Bozhon Precision Industry Technology, AI