Deconstructing the Semiconductor "Chemical Key" Hydrofluoric Acid Concept Stocks: The Industry Chain Has Been Fully Priced, Divergence Has Just Begun

- Core Viewpoint: Driven by AI capacity expansion and rising supply chain costs, the price of electronic-grade hydrofluoric acid continues to rise, and A-share related sector stock prices have surged significantly. Investors need to be wary of diverging fundamentals among individual stocks. Most companies' profits come primarily from non-semiconductor businesses or rely on expectations; only a few companies with G5 production capacity and customer certifications have genuine performance support.

- Key Elements:

- Electronic-grade hydrofluoric acid is indispensable for precisely dissolving silicon oxide in chip manufacturing. G5-grade products (suitable for 14nm and below processes) generate high profits due to technical barriers and customer certification hurdles (cycle of 2-3 years), with gross margins reaching 50%-60%, and a global supply gap for high-end products nearly 70%.

- The A-share first-tier companies, such as Do-Fluoride (G5 capacity of 40,000 tons/year, certified for TSMC's 3nm process, etc.) and Juhua Group (G5 capacity of 30,000 tons/year), have scale advantages. However, Do-Fluoride's 480% profit increase in Q1 2026 was primarily due to the price hike of lithium hexafluorophosphate (a lithium battery material), not hydrofluoric acid.

- Stock price increases for companies like China Juhua and Jianghua Microelectronics are significantly disconnected from their fundamentals. China Juhua reported only a profit of 6.37 million yuan in Q1, and the company's official announcements deny any direct business dealings or price hike agreements with Samsung regarding hydrofluoric acid.

- Crystal Clear Electronic Material is in a relatively favorable position. Its G5-grade electronic-grade sulfuric acid has begun mass supply to SMIC, with its revenue share rising from 5% to 20%. Backed by real orders, its stock price is only 7% away from its 52-week high.

- From a capital flow perspective, taking Do-Fluoride as an example, institutional desks have been continuously net sellers while retail/hot money desks are net buyers, showing typical signs of overheating sentiment in thematic stocks. The high turnover rate (around 20%) suggests significant profit-taking pressure.

- Short-term catalysts (price hikes by Korean manufacturers, interim earnings reports, CXMT's IPO) might support sentiment. However, the interim earnings season will be a key inflection point for fundamental verification, and stocks whose performance fails to match valuations will be the first to retreat.

Original Author: David

Electronic-grade hydrofluoric acid has recently become a hot commodity.

On July 1, Taiwan's Economic Daily reported that TSMC, Samsung, and SK Hynix are all scrambling to purchase this material, with supplier prices having already risen by 20% to 30%.

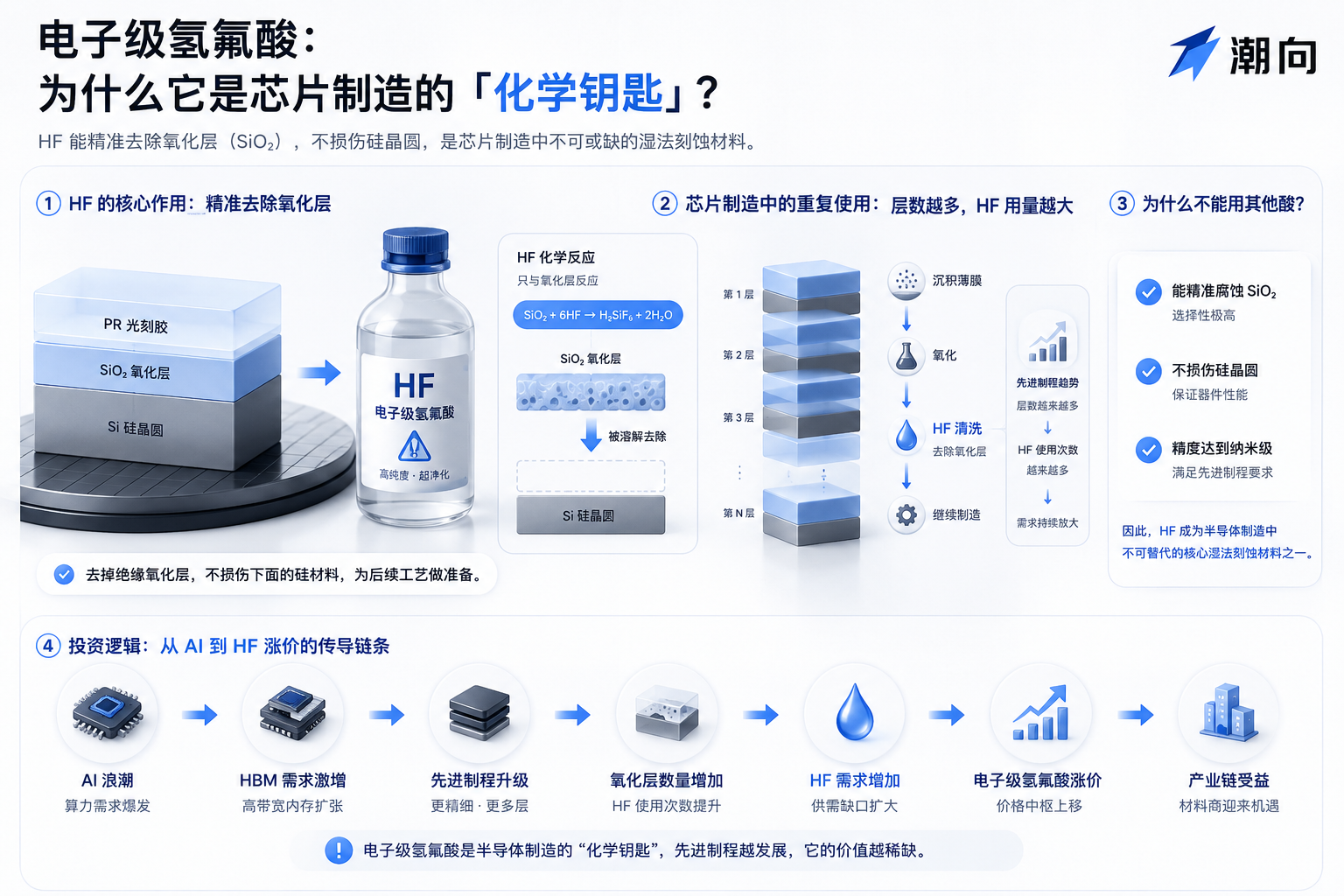

Simply put, during chip manufacturing, a silicon oxide film forms on the wafer surface, which must be precisely etched away using chemicals to continue the process. Electronic-grade hydrofluoric acid does exactly this:

It dissolves silicon oxide without damaging the underlying circuits, making it one of the most heavily consumed chemicals in wafer cleaning and etching processes. The industry calls it the "chemical key".

Producing hydrofluoric acid requires fluorite and sulfuric acid. Disruptions in shipping through the Strait of Hormuz have pushed up sulfur prices, driving sulfuric acid costs higher and raising production expenses accordingly. South Korean domestic material suppliers have been forced to significantly increase purchases of raw materials from Mainland China at a premium roughly 40% higher than the start of the year.

Following this logic, the A-share fluorine chemical sector began its rally in mid-May and has already seen substantial gains, with a number of related stocks trading near their 52-week highs.

Shortages, price hikes, import substitution... The market has largely seen and acknowledged these narratives.

At this point, it's crucial to discern which companies in this broad rally have real earnings to show and which are simply being driven by sentiment.

From Fluorite to G5: A Deep Dive into the Industry Chain

The raw material chain for electronic-grade hydrofluoric acid is short: fluorite (calcium fluoride) reacts with sulfuric acid at high temperatures to produce anhydrous hydrogen fluoride (AHF), which is then repeatedly purified to yield electronic-grade products of varying purity levels.

Purity grades are classified from G1 to G5 according to SEMI international standards. G5 is the highest grade, required for advanced processes at 14nm and below – the production lines run by TSMC, Samsung, and SMIC, as well as memory products like HBM that demand extremely high cleaning purity.

Profit distribution across this chain is highly uneven.

- Upstream, fluorite and anhydrous hydrogen fluoride are bulk commodities – high volume but thin margins, with prices fluctuating with sulfur and non-ferrous metal cycles.

- Midstream, standard electronic-grade hydrofluoric acid (G1 to G4) faces many competitors, transparent pricing, and average profitability.

- The real money is in the G5 segment: according to industry data cited by East Money, spot prices for G5 products range from 180,000 to 200,000 CNY/ton, with leading companies enjoying gross margins of 50% to 60%. The global supply gap for high-end G5 is nearly 70%, and spot supply remains persistently tight.

The reason G5 commands such high profits lies in two key barriers.

- Technology: Purity must reach 7N to 11N (99.99999% to 99.999999999%). The refinement capability of the production process directly determines product usability.

- Certification: Entering the supply chains of TSMC, Samsung, and SK Hynix requires a certification cycle typically lasting two to three years. Only after passing can mass supply begin. With these two barriers combined, only a handful of companies globally can meet these requirements simultaneously.

Japanese companies have long dominated this position.

Stella Chemifa, Morita Chemical, and Central Glass together account for nearly 40% of global high-end capacity, boasting the best technical indicators globally. South Korea's Soulbrain and ENF Technology focus mainly on mid-to-low-end G3 to G4 grades, with negligible domestic G5 capacity and 90% of their anhydrous hydrogen fluoride raw material imported from China.

Chinese manufacturers have broken through G5 in recent years, with domestic effective capacity now surpassing Japan, making it the world's largest high-end supply base. Based on G5 capacity and customer certifications, A-share related stocks can be broadly divided into three tiers:

Tier 1: Large-scale G5 production with certifications from major international customers

- Do-Fluoride New Energy (002407) – China's largest G5 capacity at 40,000 tons/year, certified by TSMC (3nm), Samsung, SK Hynix, and SMIC. Global market share is approximately 25%.

- Zhongju Xincang (688549) – G5 capacity of 30,000 tons/year (plus another 30,000 tons at the under-construction Qianjiang base). Backed by Juhua Group and the National Integrated Circuit Industry Investment Fund, it is tied to SMIC, Hua Hong, and ChangXin Memory Technologies, and has entered SK Hynix's supply chain.

- Sanmei Chemical (603379) – Total electronic-grade hydrofluoric acid capacity of 50,000 tons/year, with G5 accounting for over half. Certified by leading Japanese and Korean manufacturers, with a high export ratio.

- Befar Group (601678) – Existing G5 capacity of 6,000 tons/year, operating at over 100% capacity. A new 17,000 tons/year high-end capacity is expected to start production in 2027, supplying Yangtze Memory Technologies and ChangXin Memory Technologies.

Tier 2: Primarily G4, with ongoing upgrades to G5

- Jianghua Microelectronics (603078) – A veteran manufacturer of wet electronic chemicals, offering hydrofluoric acid covering G2 to G4 grades. It serves domestic display panel and mature process production lines, while simultaneously developing G5 capabilities.

- Jingrui Electronic Materials (300655) – Electronic-grade hydrofluoric acid capacity of 22,000 tons, mainly G4. Its G5-grade electronic-grade sulfuric acid has already begun supplying SMIC in volume (this company will be mentioned again).

Upstream Resource: Fluorite

- Jinshi Resources (603505) – The only pure fluorite resource leader on the A-share market, with reserves exceeding 20 million tons and supporting 300,000 tons of anhydrous hydrogen fluoride capacity, giving it pricing power on the cost side.

The profit model along this industry chain can be summed up in one sentence:

Upstream makes money from resources, midstream makes money from scale, and G5 makes money from barriers to entry. In the current price hike cycle, the G5 segment has the greatest profit elasticity and is also the most heavily speculated part of the market.

Similar Gains, But Fundamentally Different Logics

The chart below is quite clear: almost all stocks across the entire chain are trading near their 52-week highs. However, upon closer inspection, their themes and narratives differ significantly.

Do-Fluoride: Profit is Real, But Not from Hydrofluoric Acid

Public data shows that Do-Fluoride reported a net profit attributable to parent company of 376 million CNY in Q1 2026 (+480%), with non-recurring net profit of 380 million CNY (+1,724%). This single quarter exceeded its total for the full year 2025.

Huaan Securities upgraded its rating to Buy, forecasting net profits of 1.724 billion, 2.335 billion, and 3.260 billion CNY for 2026, 2027, and 2028 respectively, corresponding to P/E ratios of 29, 22, and 16 times.

Where does the profit come from?

According to a report by Sina Finance, the new energy materials segment (primarily lithium hexafluorophosphate, LiPF6) accounted for 34.97% of revenue in the first three quarters of 2025, with gross margins soaring from 8.62% to 19.53%, making it the biggest profit driver. Lithium hexafluorophosphate is a raw material for lithium battery electrolytes and is unrelated to semiconductors.

The price of LiPF6 rose from 47,000 CNY/ton in July 2025 to 130,000 CNY/ton in Q1 2026. As the world's second-largest supplier (shipments of about 50,000 tons, market share ~20%), Do-Fluoride captured the full elasticity of this price increase. Some brokerages estimate this single product could contribute over 2 billion CNY in net profit for 2026.

Regarding hydrofluoric acid, Do-Fluoride itself stated on an investor relations platform in November 2025: "The market price for semiconductor-grade hydrofluoric acid is stable, with small fluctuations."

The market is buying Do-Fluoride under the "leader in hydrofluoric acid price hikes" label, but its Q1 profit explosion relied on the LiPF6 price surge, which has little connection to semiconductors. Moreover, LiPF6 prices have already begun to retreat.

Zhongju Xincang: Up 4x, But Company Denies Market-Applied Labels

Zhongju Xincang rose from a 52-week low of 7.44 CNY to 39.74 CNY, the biggest gainer across the entire chain. It recorded a full-year loss of 16.59 million CNY in 2025. It only turned profitable in Q1 2026, with a net profit attributable to parent of 6.37 million CNY.

On May 15, the day its stock hit the daily limit up, the company issued an announcement regarding unusual price fluctuations, stating three key points: "The sales proportion of our electronic-grade hydrofluoric acid business is limited"; "There is no direct business relationship with Samsung Electronics regarding electronic-grade hydrofluoric acid products"; "We have not signed substantive price increase order agreements with related customers for the aforementioned products"...

Zhongju Xincang's main business is the overall supply of wet electronic chemicals, with hydrofluoric acid being just one category.

Before its capacity comes online and profits truly materialize, the current price of 39.74 CNY corresponds to a company that earned 6.37 million CNY in Q1. The gap between these is filled entirely by expectations.

Jianghua Microelectronics & Jingrui Electronic Materials: Business Alignment, But Distinguish Who Has Orders and Who is Waiting

Jianghua Microelectronics has risen over 200% in a year. Its core business is wet electronic chemicals, and it is currently developing G5-grade hydrogen peroxide and ammonia solutions.

Its advantage lies in a wide product line and broad customer coverage, supplying domestic display panels and mature process production lines. Moving into G5 signifies an upward shift from low-end to high-end, but its G5 products are still in the customer certification phase. Whether it can secure orders for advanced processes is not yet confirmed by publicly available information.

Jingrui Electronic Materials is up 130%, about 7% below its recent high, making it one of the least extreme positions in this group. It possesses something most of its peers lack:

Its G5 electronic-grade sulfuric acid is already supplying SMIC in volume, with its revenue share increasing from 5% to 20%. This is a solidified order. In an environment where the entire chain is largely priced on expectations, companies with genuine shipments are likely to be more resilient during market corrections.

The rest, such as Jinshi Resources, is up about 50%, the most moderate of the entire chain. As a fluorite miner, it profits from rising resource prices, with an indirect link to semiconductors. Higher fluorite prices increase the cost of anhydrous hydrogen fluoride, which then transmits to the prices of electronic-grade products. It acts more like a 'cost driver' for the entire chain rather than a direct beneficiary of end-demand.

Data Worth Watching

Short-term pricing of A-share thematic stocks often diverges from fundamentals. For the hydrofluoric acid sector, which has collectively rallied to its highs, near-term and medium-term focuses differ.

Short-term: Focus on Capital Flow and Sentiment, Ignore Fundamentals

Data from Do-Fluoride's recent daily limit-up events on the Dragon & Tiger Board reveal certain patterns.

On June 11, the stock hit its daily limit (closing at 38.19 CNY), with a turnover of 7.92 billion CNY and a turnover rate of 20.13%. The board showed net selling of 179 million CNY by institutional specialized seats, net buying of 226 million CNY by the "Chengdu faction" (a type of speculative capital), and net buying of 77.14 million CNY by "quantitative hitting limit" seats.

On June 22, it hit the daily limit again, with a turnover of 7.906 billion CNY, net institutional selling of 147 million CNY, and net buying by brokerage seat accounts of 490 million CNY. (Data from Shenzhen Stock Exchange public information, post-market data for respective dates.)

Both limit-up events exhibited the same structure: institutions selling, speculators buying.

On June 29, Do-Fluoride ranked No.1 on Tonghuashun's "Hot Stocks" list. Today, July 1, it hit the daily limit-up at the open, reaching a new 52-week high.

Experience suggests that when a thematic stock simultaneously meets the conditions of "ranking No.1 on the hot stock list," "consecutive daily limit-ups with massive turnover," and "continuous net selling by institutions," it often signals that sentiment has reached a very high temperature.

Possible upcoming catalyst points include:

Further price hikes by South Korean manufacturers in June-July (as anticipated by Korean media), the H1 2026 earnings reports for Do-Fluoride and Zhongju Xincang (around mid-August), and the IPO listing of ChangXin Memory Technologies (expected by the market between mid-July and early August).

If these events continue to generate discussion, short-term sentiment could be sustained. Otherwise, profit-taking pressure following huge turnover could quickly emerge.

Tide Direction Assessment

The supply-demand logic of this industry chain is solid. AI capacity expansion drives demand, Japanese companies are not expanding capacity, South Korea relies on imports, and prices are indeed rising.

However, the stock prices of the entire sector are undoubtedly at high levels. Leaders have surged three to five times. The Dragon & Tiger Board shows institutions selling while speculators buy. Sentiment indicators (No.1 hot stock, massive turnover, ETF premiums) are all maxed out.

At this juncture, the importance of industry logic is less than the odds of a payoff. Even a correct logic can be priced to the point of leaving no room.

If one must look for relatively better positions within this chain, Jingrui Electronic Materials