SemiAnalysis' Deep Dive into CXMT: $50 Billion Revenue and an IPO in a Super Cycle

- Core Thesis: Leveraging Qimonda's technological heritage, long-term capital support from Hefei's state-owned assets, and talent acquisition from both domestic and international sources, CXMT (ChangXin Memory Technologies) has become the world's fourth-largest DRAM manufacturer. It is now preparing for the largest semiconductor IPO in Chinese history, whose performance surge is primarily driven by price spikes during the DRAM super cycle, rather than substantial technological or market share leadership.

- Key Elements:

- CXMT is valued at approximately $27 billion and plans to raise RMB 29.5 billion, primarily for DRAM technology upgrades. In Q1 2026, its revenue reached $7.3 billion with an operating profit margin of around 70%.

- The company achieved its first annual profitability only in 2025, with revenue surging 156% year-over-year to $8.6 billion. The main driver was ASP growth (up 57% QoQ in Q1 2026), not a significant increase in bit shipments.

- CXMT's DDR5 cost per bit remains over 30% higher than Samsung, SK hynix, and Micron. However, its gross margin has neared industry levels (37.8% in 2025), with profit improvement driven by the pricing environment rather than competitiveness.

- By the end of 2026, CXMT's wafer capacity is expected to reach 350,000 wafers per month, approaching Micron's level. However, its HBM capacity (~5,000 wafers per month) and technology (difficulty in mass-producing HBM3 8-hi) represent its biggest weakness.

- The IPO equity structure is complex, with 74% of net profit attributable to minority interests. Hefei state-owned assets hold over 30% of the shares. The company controls its fabs through a concert party agreement but declares no de facto controlling shareholder.

- Alibaba, listed as a nearly 4% shareholder, provides endorsement on the demand side, a difference from leading manufacturers that rely on global market demand.

Original Authors: Ray Wang, Myron Xie, Dylan Patel et al.

Original Translation: TechFlow

Introduction: ChangXin Memory Technologies (CXMT) is preparing for its IPO on the STAR Market, which is poised to become the largest semiconductor IPO in Chinese history. Founded in 2016, the company started by acquiring the patents and talent of the bankrupt German DRAM manufacturer Qimonda. Backed by capital injections from the Hefei government, which tolerated losses for nearly a decade, CXMT achieved its first-ever profit in 2025. In the first quarter of 2026 alone, it reported a record quarterly revenue of $7.3 billion. This in-depth report by SemiAnalysis deconstructs CXMT's technology roadmap, financial data, HBM challenges, and IPO structure, making it essential reading for understanding the position of China's memory chip industry.

As early as the end of 2024, the SemiAnalysis team was the first to describe the enormous demand for memory driven by AI inference and agent workflows in their newsletter. They have since published multiple in-depth reports on memory and have consistently tracked CXMT and China's computing ecosystem. With CXMT set to go public in the coming months, a dedicated deep dive is necessary. CXMT is likely to become China's largest semiconductor IPO, marking a significant milestone for this leading domestic memory manufacturer. From here on, the competition between CXMT, Samsung, SK Hynix, and Micron will only intensify.

The Silicon Valley Returnee

CXMT's founder, Yaming Zhu, graduated with a bachelor's degree in physics from Tsinghua University in 1994 before pursuing electrical engineering at Stony Brook University in New York. After working for years in Silicon Valley, he became a project lead at MoSys (Monolithic System Technology) around 2001. In 2005, Zhu returned to China with a set of SRAM patents and $100,000 in seed funding, founding GigaDevice, which later became one of the world's top NOR Flash suppliers. However, the global NOR Flash market is significantly smaller than DRAM or NAND Flash. Zhu's ambitions were larger, and he chose the DRAM赛道.

DRAM is not a game for fabless companies. It consumes immense capital, is protected by high patent barriers, and is heavily reliant on manufacturing capabilities. By 2016, the industry had consolidated to just three survivors: Samsung, SK Hynix, and Micron. The moat built by four decades of patents and capital seemed impenetrable to new players. Zhu's SRAM patents and GigaDevice's NOR Flash business could neither provide DRAM cell design nor DRAM processes, nor could they circumvent the patent fortress of the incumbents. Therefore, when Zhu and the Hefei city government launched the DRAM project "Project 506" (later CXMT) in 2016, the core technology had to be sourced externally.

The source was a long-dead German company.

The DRAM Foundation: The Qimonda Legacy

That dead company was Qimonda. Qimonda filed for bankruptcy in January 2009, a victim of the global financial crisis and the subsequent memory price crash. However, it was then Europe's leading DRAM manufacturer. As a subsidiary of Infineon, with roots tracing back to Siemens, Qimonda offered a rare alternative: a deep DRAM patent portfolio and a memory cell architecture that existed outside the Samsung-Hynix-Micron triad.

In June 2015, Polaris Innovations, a subsidiary of the Canadian patent licensing firm WiLAN, purchased approximately 7,000 Qimonda patents and applications from Infineon for around €30 million. In December 2019, Polaris and CXMT signed an agreement licensing a large batch of these DRAM patents. CXMT executives have publicly stated that they received approximately 2.8TB of Qimonda technical documentation, which became the bedrock of CXMT's DRAM business.

A key technology inherited and developed by CXMT from Qimonda is the 46nm-class BWL (Buried Wordline) memory cell, which it has pushed towards the 10nm-class. BWL is a core architectural innovation. Traditional designs route the access transistor's gate along the wafer surface; BWL buries the gate into a trench beneath the bitline. This offers three benefits: it allows the memory cell to shrink to a 6F² layout (versus the traditional 8F²); it extends the channel length to suppress short-channel leakage current (which affects data retention) without sacrificing surface area; and it reduces parasitic capacitance between the gate and bitline. Buried wordlines combined with stacked capacitors form the architecture used by all three major memory manufacturers today. Qimonda, which had stubbornly stuck to the trench capacitor approach, paradoxically retained the technical reserves for stacked/BWL technology—precisely what CXMT acquired.

Talent: From Frozen Blueprints to Living R&D Capability

Beyond patents, the more enduring asset CXMT gained from Qimonda's collapse was its engineers. Qimonda had an R&D center in Xi'an employing 400-500 engineers, one of its largest R&D bases outside Germany. Although the entire Xi'an center was acquired by Unigroup after Qimonda's bankruptcy, the broader diffusion of talent benefited CXMT.

CXMT also successfully attracted a senior engineer from Qimonda's German headquarters: Karl-Heinz Kuesters. Kuesters spent 24 years at Siemens, Infineon, and Qimonda as Vice President of Technology and Advanced Development. The pre-production line he oversaw was precisely the stacked capacitor approach—the architecture CXMT actually uses. He joined CXMT as a technical advisor; EE Times dubbed Kuesters CXMT's "trump card." What Kuesters brought was the tacit know-how that no patent or 2.8TB of documentation could convey: two decades of experience leading DRAM development, enabling him to tell CXMT's engineers which Qimonda designs to keep, which to discard, and how to take a lab-proven memory cell into mass production. This kind of integration and yield judgment exists in no patent literature.

The same pattern held for the US. CXMT's Vice President for Future Technology Evaluation, Ping Er-xuan (the public expositor of the "46nm to 10nm-class" roadmap), came not from Qimonda but from a US career at Micron, SanDisk, and Applied Materials, bringing deep expertise in memory and materials technology.

CXMT also heavily recruited from South Korea and Taiwan. South Korean prosecutors have indicted former Samsung employees for allegedly leaking technology, with reports indicating dozens of Korean engineers have worked at CXMT. The situation is similar in Taiwan, where CXMT has consistently poached top equipment and process engineers with attractive salaries.

This is the crux of understanding CXMT's trajectory. Qimonda's patents were always a finite, depreciating asset. What allowed CXMT to progress from G4 to G5 and towards HBM was the aggregated talent pool—locally cultivated engineers, Chinese engineers returning from stints at foreign companies, and a small number of foreign experts—not documents. The legacy was a starting point; talent transformed that acquired legacy into an engine of independent R&D. But this engine operated at a loss for nearly a decade. The question was: who had the patience to keep fueling it?

The Patience of State-Backed Venture Capital

CXMT's success can hardly be separated from the strong support of Chinese local and central governments. The Hefei city government is a classic case study. As a hub for China's tech innovation, Hefei has incubated several successful companies over the past two decades using its "patient government venture capital" model: BOE (a global leader in display panels), NIO (a leading EV maker), and now CXMT.

The Hefei government did two crucial things for CXMT.

First, it helped build a local supply chain around CXMT's factories. Hefei's strategy: take large equity stakes in the core "chain leader" company, then attract the rest of the industry chain. It did this for BOE in display panels, for NIO in EVs, and replicated the same playbook for CXMT starting in 2016. Surrounding CXMT's factory complex in Hefei Airport Economic Zone, the government cultivated a dense local industrial cluster. Packaging and testing houses Pei Dun and Xin Feng are located right next to CXMT's facilities; over 99% of Xin Feng's revenue comes from CXMT. Guanggang operates an on-site bulk gas plant supplying most of CXMT's needs. Zhicheng Technology's subsidiary Zhi Wei Semiconductor provides wafer reclaim capacity in Hefei's Xinzhan High-Tech Zone. State VC has also taken direct controlling stakes in upstream chip molding equipment manufacturer Wenyi Technology.

Second, Hefei's state capital was prepared to endure losses for a long time. Unlike private equity funds that must deliver returns to LPs on schedule, Hefei's state VC is ultimately backed by municipal and development zone state entities, with no exit clock. They continuously funded a company that didn't achieve its first annual profit until 2025, accumulating total losses of approximately RMB 36.65 billion over nearly a decade. For "Project 506" launched in 2016, roughly 80% of the initial funding (RMB 14.4 billion out of 18 billion) came from Hefei state capital. While diluted in subsequent funding rounds, Hefei state entities never sold down or exited. At the time of the IPO, the largest shareholder, Hefei Qinghui Jidian, holds 21.67%, and state-linked VCs collectively hold over 30%. The willingness to treat a wafer fab as a decade-long bet rather than a fund-cycle return was the catalyst that both technology and talent depended on.

From Legacy to Independence

Combining these three threads clarifies CXMT's first decade. Qimonda provided the foundation: a licensed patent pool and memory cell architecture from outside the dominant triad. Talent provided the engine: key individuals like Kuesters and Ping, plus returnees from US industry giants and controversially sourced talent from Korea, turned frozen blueprints into a process capable of continuous improvement. Then, the Hefei government provided what the first two needed but couldn't generate themselves: capital, patience, and a localized supply chain. None were dispensable.

Next, we discuss CXMT's financials, technology, and equipment ecosystem.

The Next Step After a Decade: IPOing into a Super Cycle

While CXMT's story over the past decade is impressive, it may only be the early chapters of a longer narrative. The company is preparing for one of China's largest semiconductor IPOs in recent years, potentially the most globally watched semiconductor listing this year. In December 2025, the Shanghai Stock Exchange formally accepted CXMT's application for listing on the STAR Market. Prior to that, market rumors of an impending listing persisted throughout 2024 and 2025. The latest development is that CXMT submitted its registration application to the China Securities Regulatory Commission on May 27, and is currently in the final review stage.

CXMT's IPO prospectus disclosed a wealth of previously unavailable information. Combined with SemiAnalysis's Memory Model, we can make more precise judgments about CXMT's current position and future trajectory.

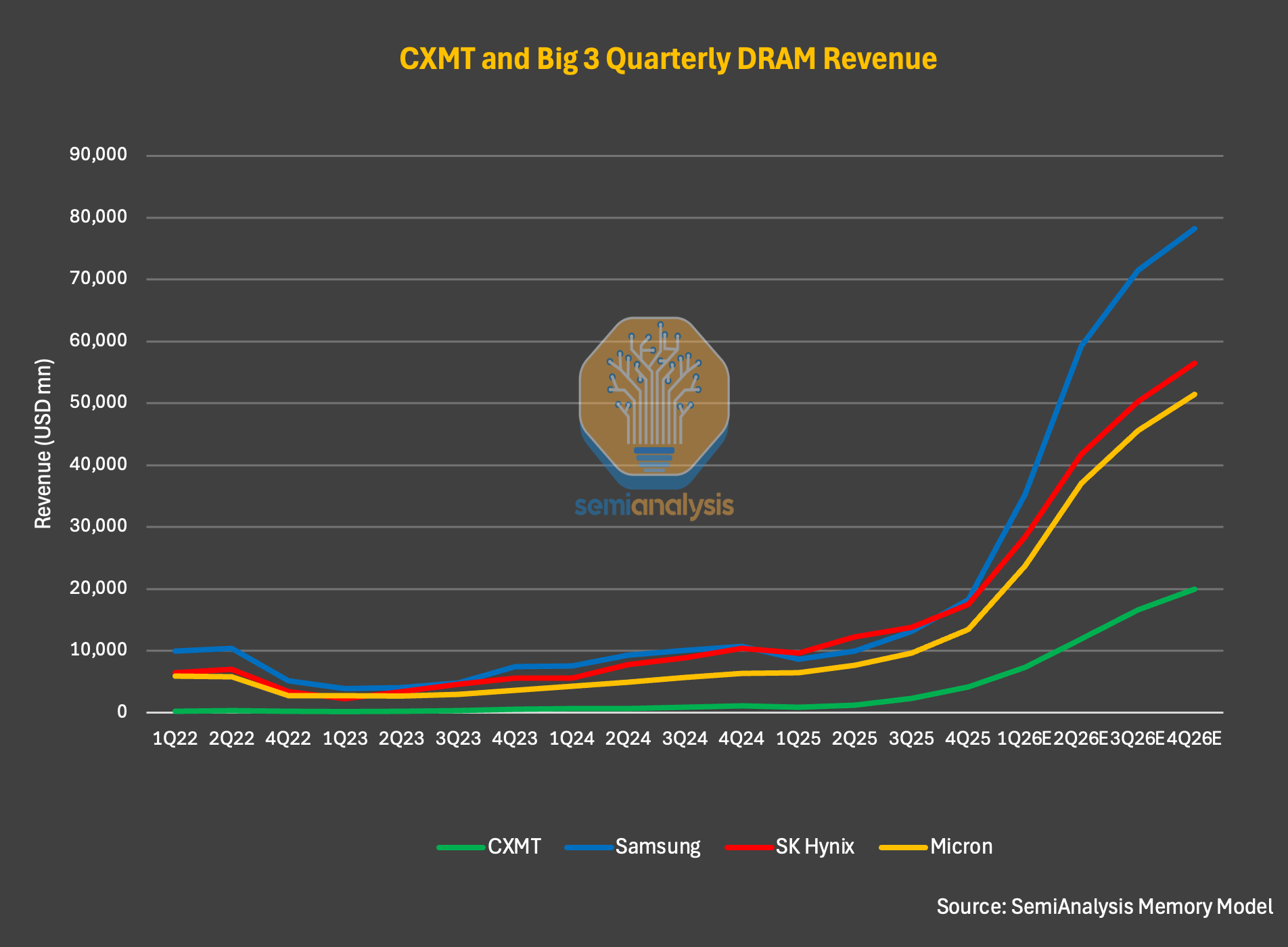

At a high level, by almost any metric, CXMT is the world's fourth-largest DRAM manufacturer and is widening its lead over second-tier memory players. For the full year 2025, CXMT's revenue grew 156% year-over-year to approximately $8.6 billion, up from $3.3 billion in 2024 and $1.2 billion in 2023. Net profit also turned positive for the first time, reaching $1.0 billion. Even so, CXMT's 2025 revenue pales in comparison to the DRAM revenues of Samsung (~$72.3 billion), SK Hynix (~$52.1 billion), and Micron (~$37.2 billion).

Figure: Global DRAM Revenue Comparison (Source: SemiAnalysis Memory Model)

In Q1 2026, CXMT reported revenue of $7.3 billion, up approximately 700% year-over-year, with a single quarter's revenue nearly matching the full year 2025 level. Operating margins also expanded sharply to around 70%.

SemiAnalysis believes this is just the beginning. Based solely on the prospectus disclosure, the company's first half of 2026 revenue is projected to be up 7x year-over-year, exceeding $16 billion. For the full year 2026, SemiAnalysis estimates CXMT's revenue could surpass $50 billion. If realized, this means the company has more than doubled its revenue annually since 2023, with a year-over-year increase of over 6x in 2026.

The driver of this explosive growth is less about technology or market share gains and more about the cycle itself. Looking closely at the data: in Q1 2026, CXMT's bit shipments grew only 11%, but its ASP (Average Selling Price) rose approximately 57%. In Q3 and Q4 of 2025, quarter-over-quarter ASP increases were 63% and 68%, respectively. The real performance booster was the explosive price increase, not a significant capture of market share from competitors. In terms of bit shipments, SemiAnalysis's model shows CXMT's market share growing from 9% in 2025 to 12% in 2027. A 3-percentage-point increase may seem small, but in a market SemiAnalysis predicts will be worth nearly $1 trillion by 2027, it is enormous.

Figure: CXMT ASP vs Bit Shipment Trends (Source: SemiAnalysis Memory Model)

The Misconception of 'Chinese Memory Disrupting the Market'

For readers not deeply following CXMT or the memory market, a more interesting finding is CXMT's pricing relative to industry leaders. Based on data from the Memory Model, CXMT's DRAM ASP challenges a common misconception: that Chinese memory is structurally cheaper and will flood the market, depressing global prices. While this may have held true in some past instances, it is not accurate in the current cycle.

Take Q1 2026 for example; CXMT's DRAM ASP was only about 5-10% lower than Samsung, SK Hynix, and Micron. SemiAnalysis expects this direction to hold