Rate Cuts? Wait Until 2027?

- Core View: The military conflict between the US and Iran and the resulting disruption to shipping in the Strait of Hormuz have exacerbated US inflation by pushing up energy prices, forcing the Federal Reserve to reassess its monetary policy path. Expectations for rate cuts in 2026 have significantly weakened, creating political pressure for the Trump administration ahead of the midterm elections.

- Key Elements:

- The conflict caused Brent crude oil prices to surge from around $70 per barrel to a peak of $118. The national average gasoline price in the US exceeded $4 per gallon for the first time in four years, with the gasoline price index contributing to about three-quarters of the month-on-month increase in the March CPI.

- The energy shock, transmitted through transportation and supply chains, has increased costs across a wide range of sectors including food and logistics. Analysis estimates that high oil prices could persistently elevate the US CPI inflation rate by 1 to 2 percentage points.

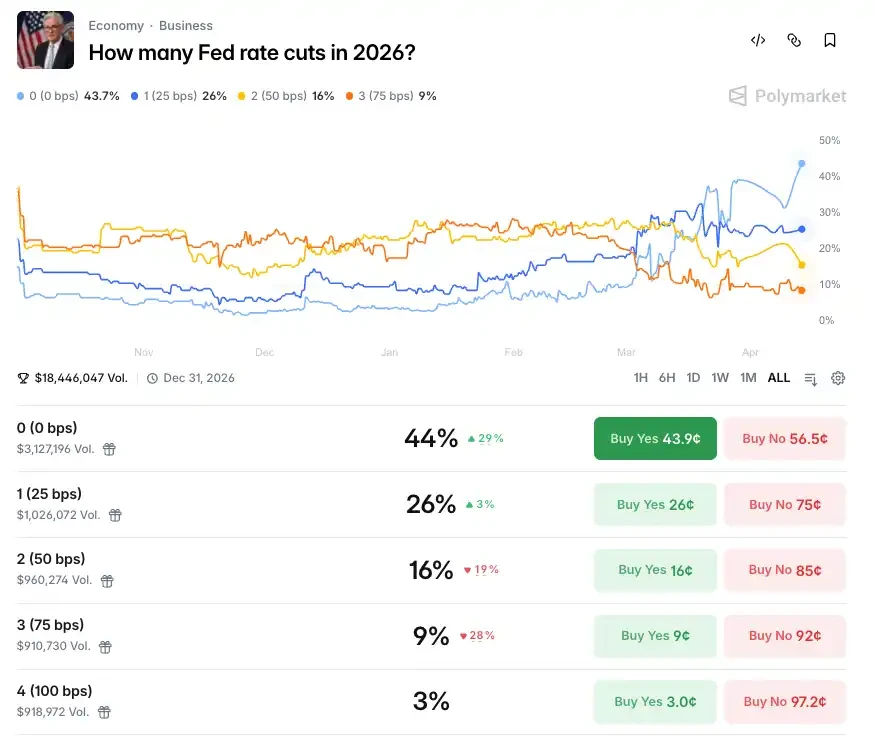

- Market expectations for Fed rate cuts in 2026 have sharply reversed. Data from prediction platforms shows the probability of "zero rate cuts" for the full year has surged from 4% before the conflict to approximately 44%, with the probability of no action throughout the year exceeding 70%.

- The Trump administration faces a political need to stimulate the economy via rate cuts to aid the midterm elections, conflicting with the Fed's policy dilemma of being unable to cut rates due to inflation pressure, creating a tight time window.

- Iran has presented extremely high demands in negotiations and may adopt a stalling strategy, aiming to leverage the US domestic political cycle (midterm elections) as a pressure point, intensifying the deadlock.

The price sign at the gas station is the fastest way for ordinary Americans to understand inflation.

In March, the national average retail gasoline price surpassed $4 per gallon for the first time in nearly four years. Not because of OPEC production cuts, not because of a decline in shale oil output, but because of a war. A war that erupted in the Persian Gulf, over ten thousand kilometers away from the U.S. mainland.

The recent breakdown in negotiations means we will continue to bear the war's impact, such as the possibility that interest rates may not be cut this year.

Could a War Push Inflation Back to 2022 Levels?

On February 28, the United States and Israel jointly launched a military strike against Iran. This event redraws the timeline for the U.S. economic trajectory in 2026.

Brent crude oil surged from around $70 per barrel before the conflict to $118 per barrel by late March. Although prices have since retreated, they remain elevated at around $96 per barrel recently. This over 50% increase in oil prices hinges on a crucial waterway: the Strait of Hormuz.

Iran has effectively blockaded shipping through the Strait of Hormuz, a chokepoint for roughly one-fifth of the world's oil supply. Reports indicate the blockade largely remained in place even during negotiations.

This is not just an oil price issue. The gasoline price index accounted for nearly three-quarters of the increase in all CPI items for the month, with a month-over-month surge of 21.2% and a year-over-year increase of 18.9%. Every fill-up, every bill, punishes ordinary American families in concrete, incremental ways. Starting last week, the national average retail gasoline price broke above $4 per gallon for the first time in nearly four years.

The energy shock is rippling through the entire economy.

Rising diesel prices push up food transportation costs; fertilizer, a key export commodity shipped through the Strait of Hormuz, faces supply disruptions that could increase costs for farmers and consumers. CPI data shows food prices rose 2.7% year-over-year.

It's not just food. Amazon will impose a 3.5% fuel and logistics surcharge on third-party sellers in the U.S. and Canada, while carriers like UPS and FedEx have also raised fuel surcharges since the Iran conflict began. The tentacles of inflation reach into every corner.

Based on the correlation between year-over-year oil price changes and U.S. CPI inflation from 2020-2025, if Brent crude averages between $85-$100 per barrel throughout 2026, the year-over-year oil price increase could reach 30% to 50%, potentially adding 1 to 2 percentage points to the U.S. CPI inflation rate.

And this is just the beginning. Even if a ceasefire holds, considering the difficulty of rapidly repairing damaged energy infrastructure and disrupted supply chains, oil prices, while off their peaks, are likely to remain above pre-conflict levels in the medium term, potentially lifting CPI year-over-year figures for months.

Capital Economics economist Ryan noted that some inflationary effects from energy prices might take months to work their way through supply chains to consumers, with an impact that "could be very broad."

A single war pushed U.S. inflation from 2.4% in February back up to 3.3% in March, meaning the month-over-month CPI increase was 0.9%, the "largest single-month increase since June 2022."

(Note: In June 2022, due to the Russia-Ukraine war, COVID-19, and a delayed Fed response, CPI year-over-year hit 9.1%, the highest level since 1981.)

The Door to Rate Cuts is Half-Shut

Before the war, the market assumed the Trump administration had a carefully scripted political playbook:

On January 30, 2026, Trump formally nominated former Fed Governor Kevin Warsh as the next Fed Chair. The Powell era ended. The market quickly began pricing in a clear rate cut path under the new leadership. After Warsh's nomination, most market futures traders expected two rate cuts this year.

The political interpretation of this personnel move was quite clear. Bloomberg Economics' U.S. Economic Research Director Wilkes stated that regardless of who was ultimately nominated, they would face skepticism, with people believing they must have promised to execute the U.S. President's directives at the Fed, the first and foremost being to aggressively push for significant cuts in the federal funds rate regardless of inflationary consequences.

Therefore, in nearly all economic analyses and macro forecasts at the beginning of the year, the Fed's actual monetary easing pace in 2026 was expected to be faster than market predictions, with 2 to 3 rate cuts totaling 50 to 75 basis points for the year.

But after the war, the data changed dramatically.

Polymarket currently assigns a 44% probability to zero rate cuts in 2026, compared to just 4% before the war erupted. Since the war began, the probability of no cuts this year has steadily climbed, with the market consistently pricing zero cuts as the most likely outcome since late March. Additionally, the probability of a single 25-basis-point cut is currently 26%. Another prediction platform, Kalshi, sets the probability of a zero-cut scenario at 38.5%, with trading volumes on these platforms reflecting real-money bets.

The recently released minutes from the Fed's March 17-18 FOMC meeting showed that most officials worried the war could harm the labor market, necessitating rate cuts; simultaneously, many policymakers emphasized inflation risks, which might ultimately require rate hikes. The Fed held rates steady at 3.5% to 3.75% in March.

A single set of meeting minutes contained the possibility of both rate cuts and hikes. This might be one of the most awkward positions in Fed history.

Persistently strong inflation has led some economists to believe the Fed will not cut rates this year. Federal funds rate futures pricing still shows a probability exceeding 70% for no change this year.

Chris Zaccarelli of Northlight Asset Management pointed out that the war's duration and the situation in the Strait of Hormuz are crucial. If the supply shock is temporary and the economy can withstand it, the Fed has a chance to cut rates this year. But if the inflation shock is more persistent, they may have to hold steady all year.

EY-Parthenon Chief Economist Gregory Daco cautiously predicted that looking towards Q4 and year-end 2026, factors might emerge to push the Fed towards monetary easing, but that would be for bad reasons. He also raised the realistic possibility that the Fed's next move could be a rate hike.

This is no longer a matter of "rate cuts being delayed by a few months." This is a policy crisis where the script has been completely torn up.

The Republican Party's Situation is Quite Severe

Trump's governing logic has always been highly pragmatic. Rate cuts are never just monetary policy; they are one of the pillars of Trump's political agenda.

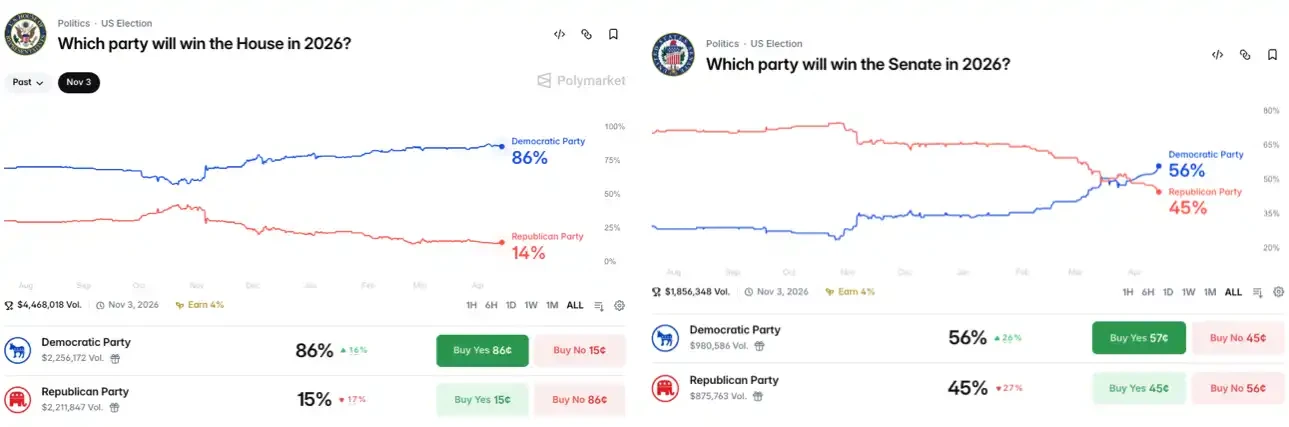

The reasoning is straightforward. Rate cuts lower borrowing costs, stimulate consumption, boost the stock market, and make ordinary people feel that money is easier to come by. And that feeling translates into votes. With the reality of midterm election pressure at year-end, as of writing, Polymarket data shows the probability of Democrats winning the House is as high as 86%, and their probability of winning the Senate has reversed from a disadvantaged 36% before the war to a leading 56%.

The Republican Party's situation is already quite severe.

Left: House of Representatives, Right: Senate

The problem is that the political fundamentals for the midterms were largely locked in by June. From now on, the time window is rapidly closing.

To focus energy on the upcoming midterm elections, Trump needs to quickly achieve conflict de-escalation to stabilize capital markets and secure political achievements.

Otherwise, the inflation resulting from rising oil costs will become starkly evident in the U.S. economy and in American consumer spending, which would be a blow to Trump's midterm prospects and his public approval ratings.

This is precisely why Trump is so urgently seeking negotiations with Iran.

Iran Employs Delay Tactics

And Iran sees this clearly.

Negotiations that opened in Islamabad on April 10 collapsed just two days later. On April 12, U.S. Vice President Vance announced in Islamabad that the talks had broken down over Iran's nuclear weapons issue, and the U.S. delegation left Pakistan to return to Washington.

The failure of the talks was no accident.

The gap in conditions was on the table even before talks began. Analysis suggests U.S. demands include: Iran must unconditionally open the Strait of Hormuz, must cease all nuclear activities, the quantity and types of Iranian missiles must be restricted to prevent any from reaching Israel, and Iran must sever all ties with proxy groups. Iran's conditions for the U.S. are equally steep: demanding the complete withdrawal of all U.S. forces from the entire Middle East, a halt to all U.S. and Israeli military actions in the region, the lifting of all economic sanctions imposed on Iran over the past 47 years, and war reparations from the U.S.

These are not two sets of close proposals. These are demands from two parallel universes.

Some U.S. think tanks believe Iran may choose a "protracted game," using the midterm elections as a "pressure point" against the U.S.

Understanding this requires grasping a fundamental asymmetry between the U.S. and Iran: Trump has a term limit; Iran does not. As an authoritarian state, the Islamic Republic has existed for nearly half a century without the pressure of electoral turnover. Iran does not need to accomplish anything by the end of 2026. It only needs to wait. Wait for Trump's midterm election window to close, wait for the Republican Party to face pressure in the House, wait for the political cost in Washington to become sufficiently high, wait for the U.S. to find its own reason to step down.

If Trump continues the conflict, sending ground troops into Iran would mean the U.S. is once again mired in this war, potentially entangled with Iran long-term. This does not align with U.S. national security strategy and would also impact many of Trump's own domestic and foreign policy agendas.

Trump himself acknowledged the negotiation difficulties. He stated that the talks were going well, with agreement on most issues, but the one truly important point—the nuclear issue—remained unresolved. The nuclear issue is precisely the red line Iran will not concede in the short term.

The current situation is this: Trump holds the desire for rate cuts, midterm election pressure, and the military burden of war with Iran, all pressing on a single clock that is accelerating towards November. Iran doesn't need to win. It only needs to hold out, to let these negotiations continue to drag on.