How to Achieve a Benchmark Interest Rate for Crypto?

- Core Thesis: The cryptocurrency market lacks a unified benchmark interest rate. Although multiple rate candidates exist (such as perpetual funding rates and lending rates), no single metric simultaneously meets the criteria of “broad coverage, term structure, and governance independence,” leaving the entire financial system without a credible pricing anchor.

- Key Elements:

- Explosive growth in the perpetual contract market: BitMEX reports that the quarterly weekly trading volume in the "perpetual traditional assets" category surged from $526 million to $30.7 billion, an increase of 5,756%.

- A qualified benchmark must meet specific standards: based on real transactions, deep and broad market to prevent manipulation, governance independence, and possessing a term structure—similar to traditional finance's SOFR (based on trillions of dollars in US Treasury repo transactions).

- LIBOR was abolished due to the manipulation scandal involving quoting banks. Its replacement, SOFR, is based on actual transaction data and managed by the New York Fed, resolving conflicts of interest.

- Bitfinex’s FRR (Flash Return Rate) is based on real-term funding transactions and has a natural term structure. However, it is operated by a single exchange and shares the same parent company, iFinex, with Tether, posing concentration and conflict of interest risks.

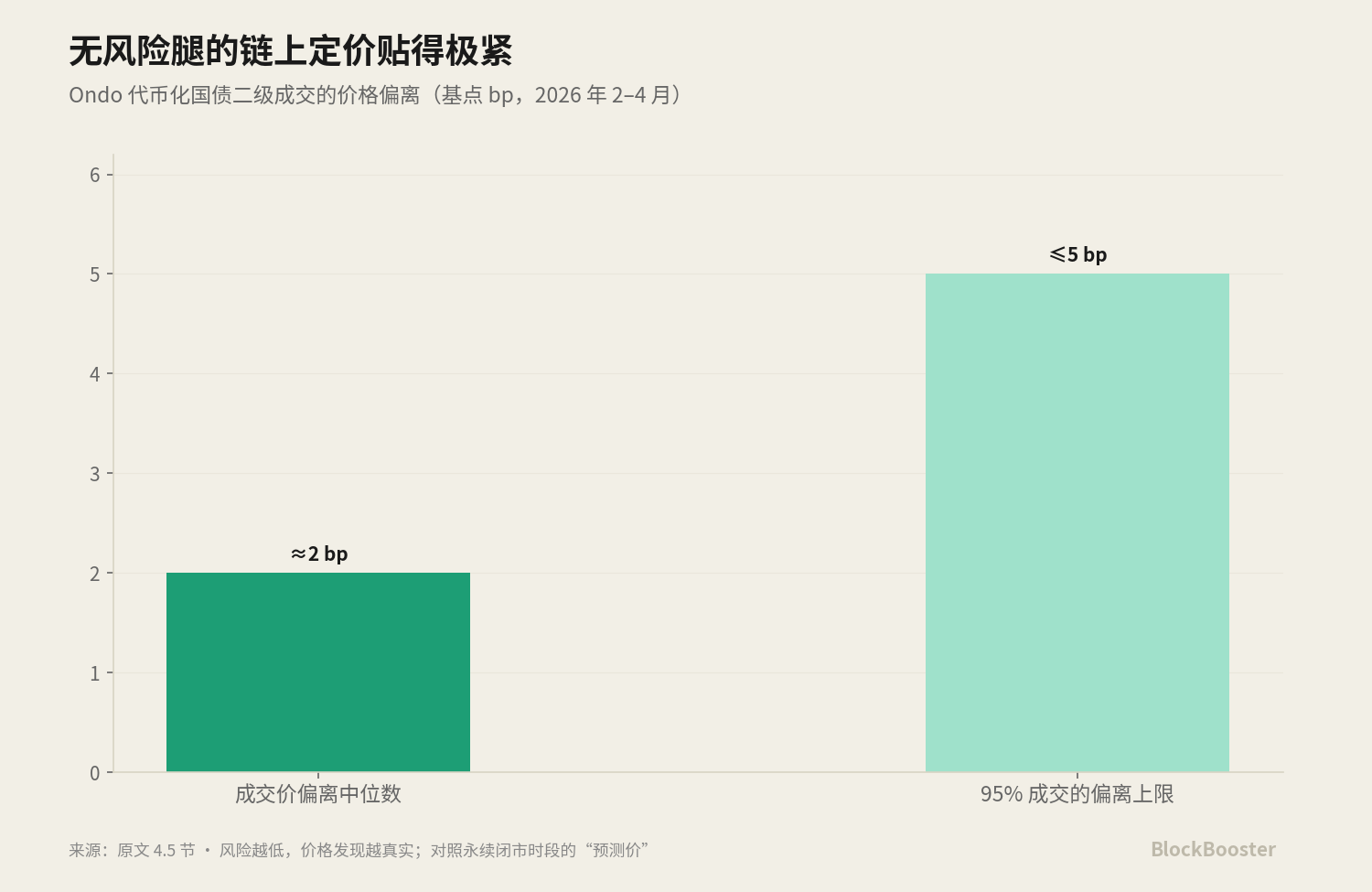

- Tokenized Treasury yields (such as BUIDL) closely track US Treasury bond yields, making them a candidate for a "crypto risk-free rate." Their secondary market pricing is precise, with deviations of only 2-5 basis points.

- Existing interest rate spreads reflect structural risks: the spread between perpetual funding rates and Treasury yields is attributed to leverage volatility; Aave rates include smart contract risk; and the Bitfinex FRR premium reflects exchange and stablecoin counterparty risk.

Original Author: @BlazingKevin_, Blockbooster Researcher

1. Crypto Has No "Base Rate"

Leverage and financing in the crypto world — trillions of dollars in leveraged positions, collateralized lending, and yield products — operate without a unified benchmark rate curve.

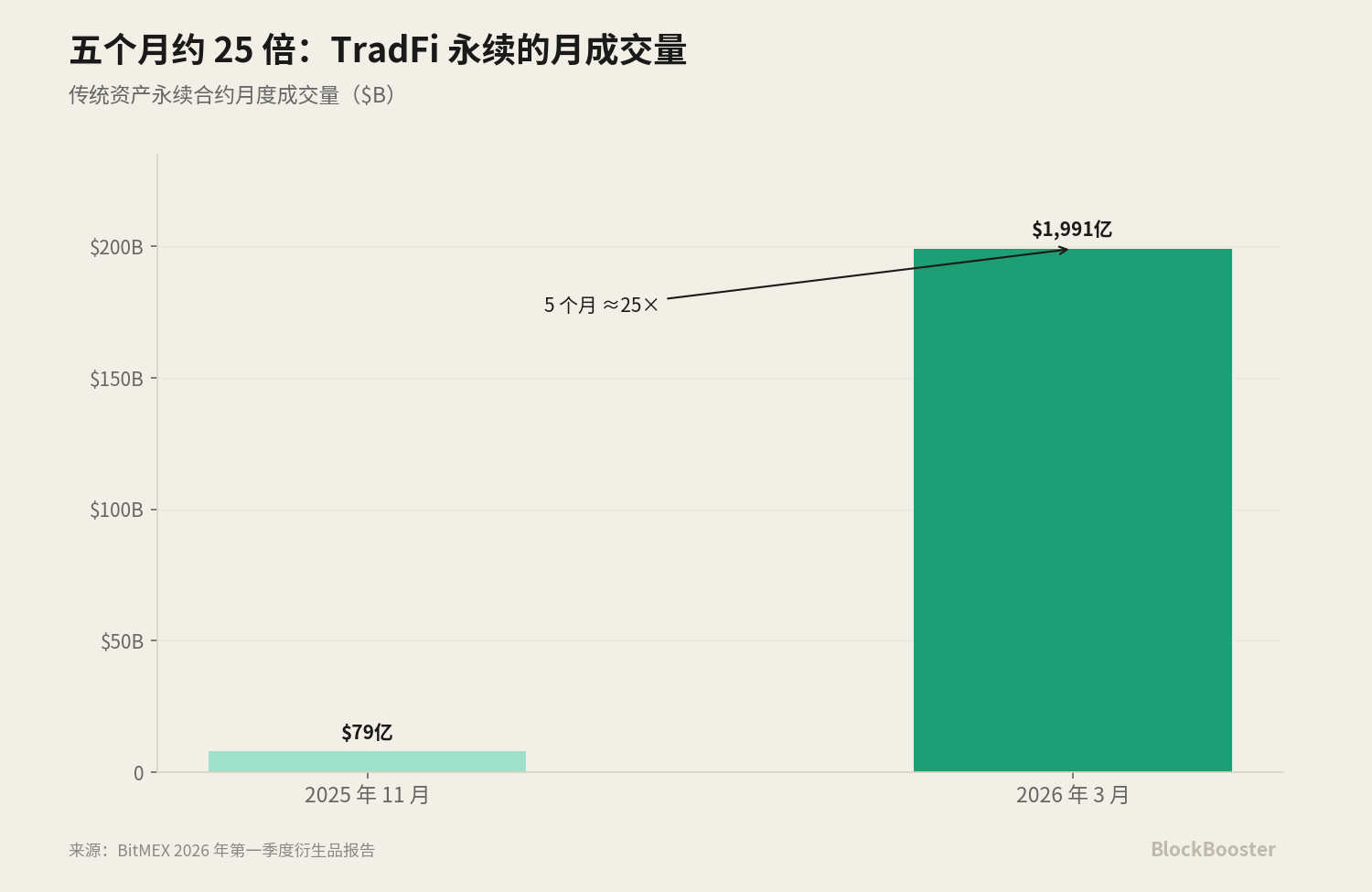

According to BitMEX's Q1 2026 derivatives report, in the nascent "traditional asset perpetuals" sector alone, average weekly volume surged from approximately $525.8 million at the end of 2025 to $30.7 billion by mid-March 2026, a quarterly increase of about 5,756%. Its monthly volume skyrocketed from $7.9 billion in November 2025 to $199.1 billion in March 2026, a roughly 25-fold increase in five months.

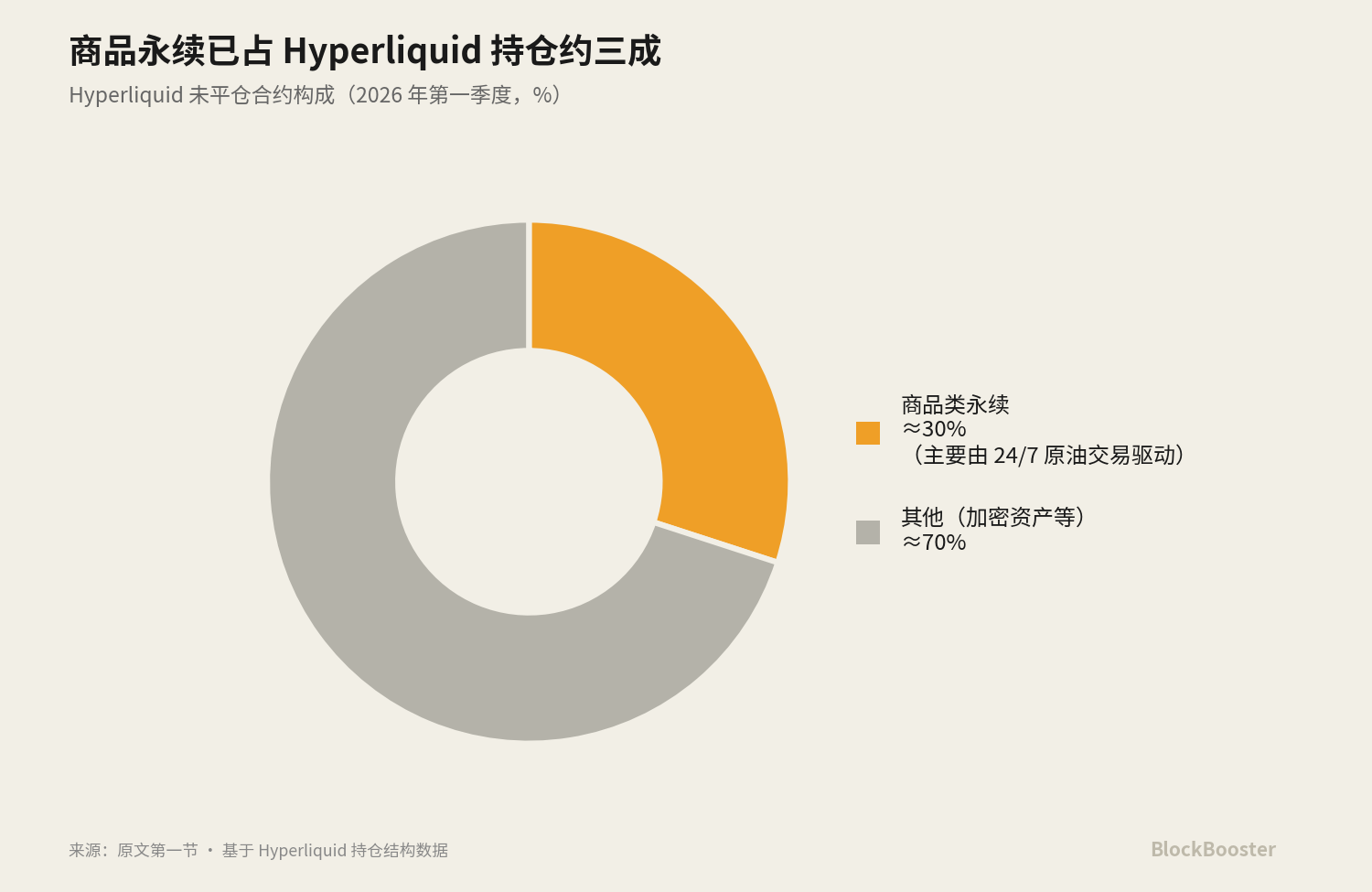

Based on DefiLlama's 30-day snapshot, Hyperliquid processed approximately $172.63 billion in perpetual volume, with open interest around $9.13 billion. In Q1 2026, commodity perpetuals accounted for roughly 30% of Hyperliquid's open interest, primarily driven by demand for 24/7 crude oil trading.

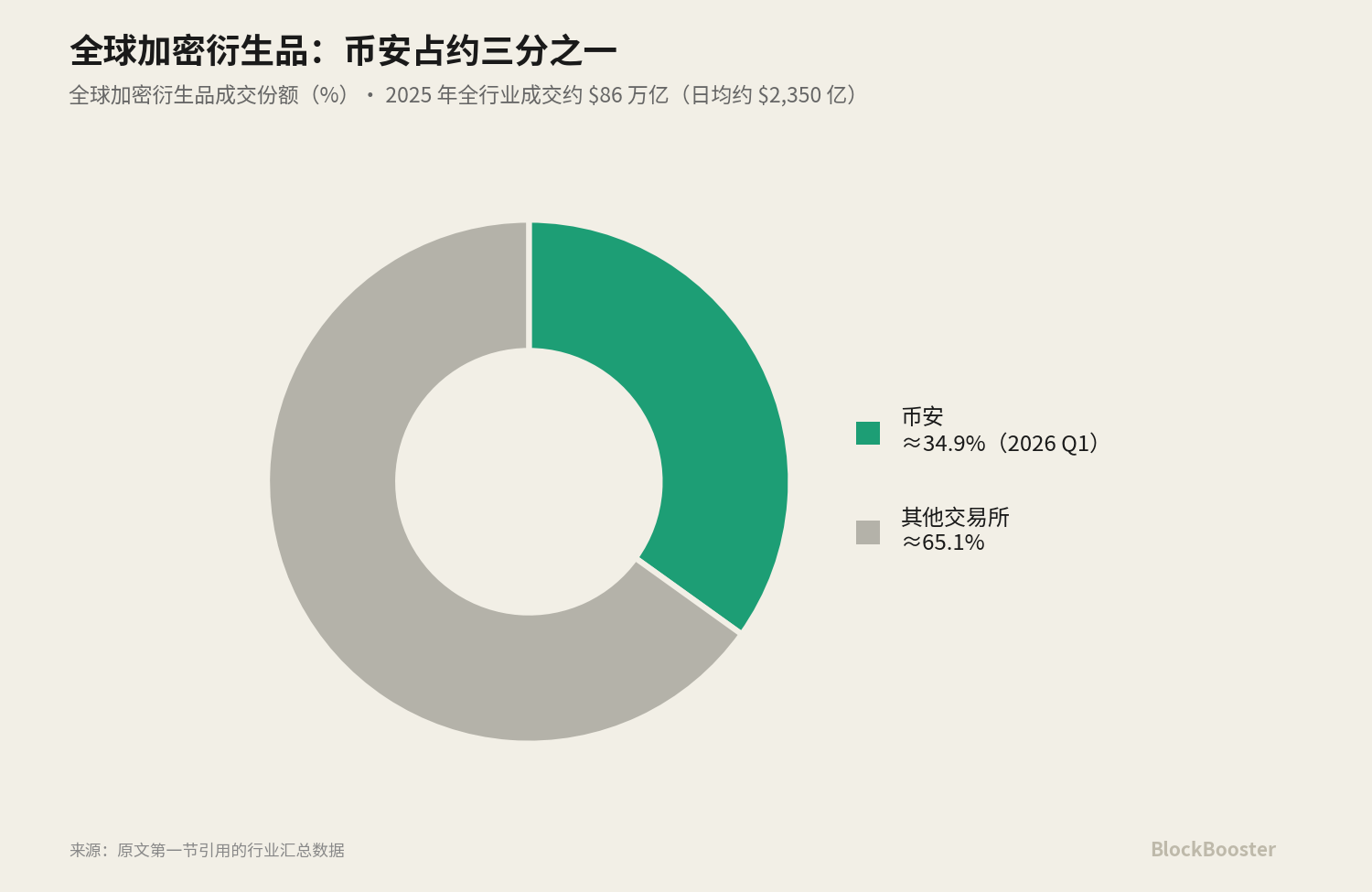

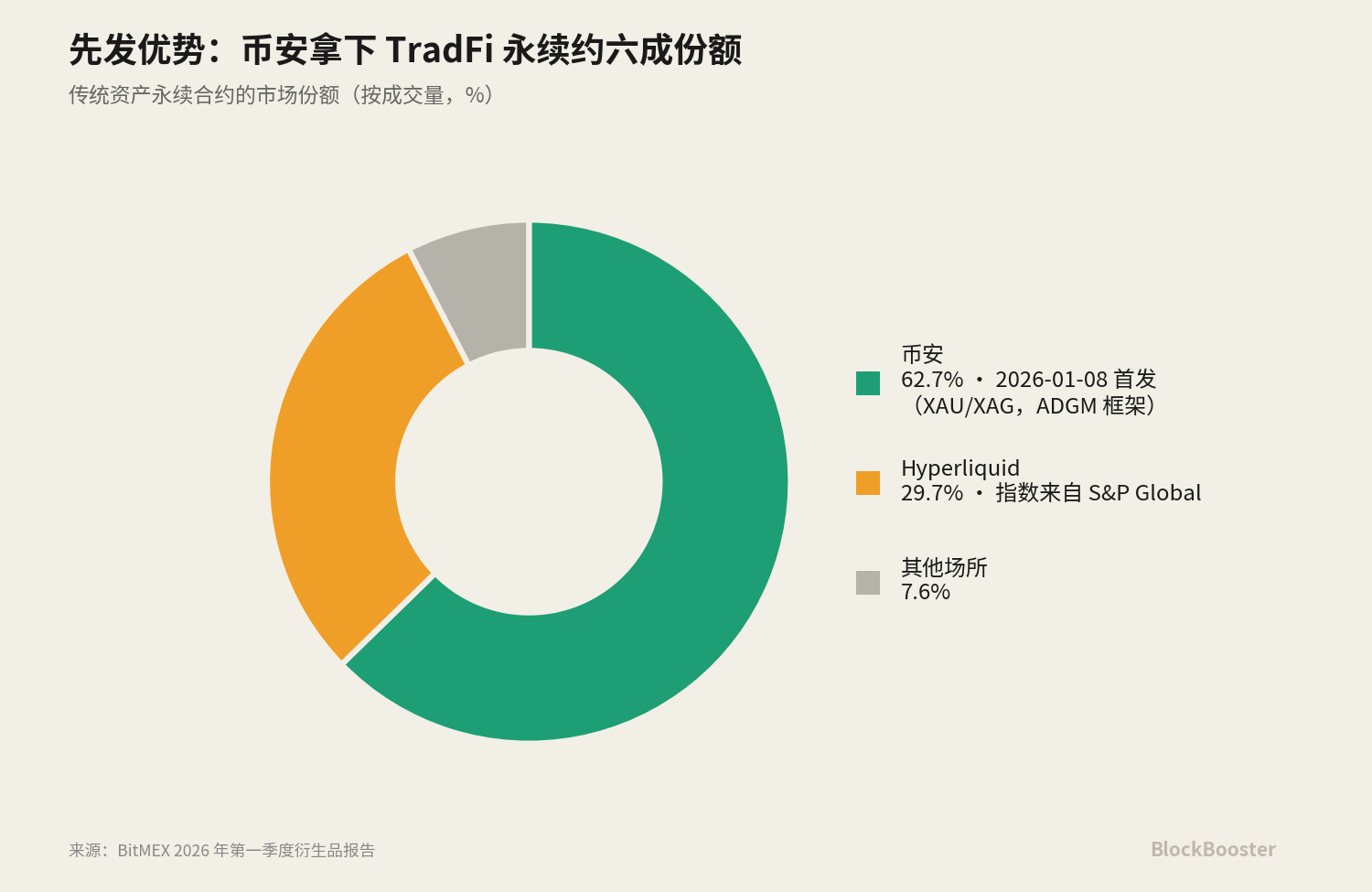

Regarding the "traditional asset perpetuals" line: Binance launched TradFi perpetual contracts on January 8, 2026, starting with gold (XAUUSDT) and silver (XAGUSDT). Leveraging this first-mover advantage, Binance captured approximately 62.7% of the TradFi perpetual market share, with Hyperliquid following at 29.7%.

Hyperliquid's index data for these traditional asset perpetuals comes from a partnership with S&P Global, and this collaboration (linking crypto perpetuals directly to traditional indices) is drawing regulatory scrutiny from the US CFTC.

Meanwhile, Ethena's USDe market cap was in the range of approximately $4.5 billion to $5.9 billion in early June 2026.

Each of these products quotes a "rate" or "yield" — perpetuals have funding rates, lending protocols have lending APRs, sUSDe has a staking yield, tokenized treasuries have coupons — but crypto, to date, lacks its own SOFR. There is no widely accepted benchmark curve that can serve as an anchor for pricing. Every exchange and every protocol is becoming a micro-financing market, quoting its own price, but without a public, credible reference system between them.

2. What Constitutes a Crypto "Base Rate"?

Let's first look at three different comparisons of rates:

- First group: Benchmark financing rate vs. product yield vs. derivative implied rate. **The APY of sUSDe is a product yield — it's the return to holders; the perpetual funding rate is a derivative implied rate — the fee paid between longs and shorts to keep the perpetual price anchored to the spot price;** while the benchmark financing rate should be a public reference that countless other products can cite and use for pricing. **Product yields and derivative implied rates are not benchmarks — they are 'downstream' of the benchmark, the result of various premiums and structures layered on top of the benchmark.**

- Second group: Overnight rate vs. term rate. **Perpetual funding rates settle every 1 or 8 hours, essentially an overnight rate — it only reflects the cost of capital 'from now until the next settlement point', without a term structure. It cannot tell you the price difference between 'borrowing for 30 days' and 'borrowing for 90 days'. Just as SOFR itself is an overnight rate and relies on futures markets to construct Term SOFR with a term structure. A rate without a term structure cannot support any medium-to-long-term fixed-income market.

- Third group: Real lending rates vs. algorithmic/implied rates. Real bilateral lending transactions (e.g., Bitfinex's margin financing book, where actual lenders and borrowers are matched) and algorithmic utilization-based pricing (e.g., Aave, where rates are automatically calculated by a formula based on pool utilization) are two fundamentally different price generation mechanisms. The former is voted on by market participants with real money, the latter is a curve coded by protocol designers.

From these three distinctions, we can extract the criteria a "qualified benchmark" should meet:

Based on real transactions, underlying market is sufficiently broad and deep (difficult for a single participant to manipulate), governance independent (no conflict of interest between the administrator and the priced market), ideally with a term structure (can support medium-to-long-term pricing).

(SOFR's underlying is the real transaction volume of overnight repurchase agreements backed by U.S. Treasury bonds, with average daily volume "often exceeding $1 trillion". This is the real transaction volume of overnight repos. It is completely different from the notional volume of futures supporting Term SOFR.)

Using SOFR's logic to examine crypto reveals structural isomorphism. The Bank for International Settlements, in its research, has analogized on-chain collateralized lending markets to "crypto-native money markets," whose operational mechanisms resemble traditional tri-party repos — over-collateralization, marking to market, overnight rollovers. Since on-chain lending is structurally a repo-style secured financing, using the design of SOFR (a benchmark built on real repo transactions) to judge crypto benchmarks is an appropriate isomorphic reference.

3. What are the Characteristics of SOFR? Why was LIBOR Discontinued?

LIBOR (London Interbank Offered Rate) was once the bedrock of global finance. At its peak, approximately $300 trillion in financial contracts (including interest rate swaps, mortgages, student loans, corporate bonds, etc.) relied on LIBOR across five currency zones. But LIBOR had a fatal design flaw: it was not based on actual transactions, but on daily 'self-reported' estimates of borrowing costs from a small panel of banks.

This flaw was fully exposed after the 2008 financial crisis. Regulatory investigations revealed that traders at several major global banks had systematically manipulated LIBOR quotes to benefit their derivative positions.

The manipulation scandal directly led to LIBOR's abolition.

Replacing it is SOFR (Secured Overnight Financing Rate). SOFR's design is almost a "reverse engineering" of every LIBOR flaw: it doesn't use self-reported estimates, but is based on real transactions in the U.S. Treasury repo market; it takes the volume-weighted median of transactions from three repo markets (tri-party, GCF, and bilateral repos cleared via FICC's DVP service), offering a broad, deep scope resistant to single-participant manipulation; it is administered by the New York Fed, adhering to IOSCO principles, with no conflict of interest between the administrator and the priced market.

However, SOFR has an "inherent shortcoming": it is an overnight rate without a term structure. The market needs not only "today's overnight cost" but also the "expected funding cost over the next three months" to price medium-to-long-term loans. Hence, CME launched CME Term SOFR — a set of forward-looking rates covering tenors of 1 month, 3 months, 6 months, and 12 months.

It uses trading data from SOFR futures to reverse-engineer the market's expectation of the future SOFR path, thereby "constructing" a forward-looking term curve. (The representative notional volume for SOFR futures used to construct Term SOFR was approximately $2.3 trillion per day in Q4 2023.)

4. Some Candidate Rates for Discussion

There are many candidates in the market referred to as "rates" or "yields". Let's break them down one by one; the discussion can focus on why some rates are clearly unsuitable as benchmark rates and which ones have room to evolve.

A thread running through all the analyses is — "who has the power to decide?": is it market weighting, algorithmic utilization, or governance setting?

4.1 Perpetual Funding Rates (Hyperliquid / Binance)

The perpetual funding rate is the implied price of leverage, driven by the basis between the spot and perpetual price: it is essentially an overnight rate, without a term structure.

When the spot market for a TradFi underlying is closed (e.g., stocks, precious metals on weekends), exchanges cannot obtain a real spot price to calculate the funding rate. Binance's approach is to freeze the index price at the last spot price and switch to an EWMA mark price with a ±3% cap; Hyperliquid also switches to EWMA on weekends and sets volatility caps per product. During closed-market hours, the "anchor" of the perpetual price is essentially a predicted value, not a real transaction price. When the market reopens and the real price gaps beyond this cap, limit-up/limit-down occurs. Thus, prices during closed hours are predictions, not a real anchor for arbitrage.

On May 29, 2026, the US CFTC approved KalshiEX's Bitcoin perpetual contract (BTCPERP), the first truly perpetual regulated Bitcoin perpetual within the US, and simultaneously released a policy statement on perpetual contracts, staff guidance on 24/7 trading and clearing, and a no-action position regarding Coinbase offering perpetuals via Deribit. The significance is that a regulated, centrally cleared perpetual means its funding rate and basis are generated in a compliant, clearing-enabled environment — this could be a future candidate seat for a "crypto SOFR". This, along with the aforementioned CFTC scrutiny of the Hyperliquid-S&P Global index partnership, signals that "regulation is approaching crypto benchmarks."

4.2 Bitfinex Margin Financing + FRR

This is crypto's native USD term financing market.

The mechanism is as follows: Bitfinex operates a peer-to-peer margin financing market where lenders lend funds to margin traders to earn interest. The key design point is that financing tenors range from 2 to 120 days (commonly 2, 7, 30 days), and matching requires both rate and tenor alignment. This means Bitfinex's financing book naturally constitutes a real lending curve from the short end to the long end: 30-day money and 120-day money have different prices, determined by real supply and demand matching. This is one of the very few real lending markets in the crypto world that inherently possesses a term structure.

And the FRR (Flash Return Rate) is the reference rate for this market: the FRR is the average rate of all active fixed-rate financing weighted by their size, updated hourly. Essentially, it is "Bitfinex's version of a benchmark reference rate" — an index reflecting the current average borrowing cost in the market. Lenders can directly choose to lend at the FRR, allowing their rate to automatically track the market.

Bitfinex charges a fee of approximately 15% on lending income (18% for hidden orders); the minimum order amount is $150. FRR is quoted as a daily rate, annualized from this daily rate: Bitfinex USD FRR is approximately 0.0136%/day, annualizing to about 5.1% — in the same range as candidates like tokenized treasuries, Aave, and SSR.

The crucial aspect is its volatility: the historical range for USD lending fluctuates wildly between roughly 3%–20% APR, strongly correlated with leverage demand.

This daily rate curve unfolds across different tenors from 2 to 120 days, forming a native USD financing curve with a real term structure in crypto.

Bitfinex and Tether share the same parent company, iFinex, with overlapping management. This gives Bitfinex the most abundant USDT liquidity in the entire crypto world — a reason why its financing market is so deep; but it also concentrates counterparty risk and stablecoin issuer risk within the same complex. Borrowing from Bitfinex, using Bitfinex's matching, denominated in Tether, with the same parent company as a backstop in extreme scenarios — this is a highly self-contained structure.

Although Bitfinex's financing market is the oldest and deepest native USD term financing market in crypto, its absolute scale (the size of the financing order book and daily matching volume) is still much smaller compared to the trillions of dollars of flow in the aforementioned perpetual markets.

Comparing FRR with LIBOR and SOFR: on the dimension of "based on real transactions," FRR is actually cleaner than LIBOR. FRR is calculated from real, executed fixed-rate financing weighted by size, reflecting real market behavior. However, FRR originates from a single exchange's order book (concentration), is operated by the same parent company iFinex that also controls Tether, the largest stablecoin (conflict of interest), and this operator is also the lender of last resort for its own market (further concentration and conflict). Therefore, FRR, on the dimensions of concentration and conflict of interest, hits upon the very things SOFR was designed to eliminate.

4.3 DeFi Lending Rates (Aave / Morpho)

This is the epitome of algorithmic utilization-based pricing: rates are not determined by bilateral matching but are automatically calculated by a preset formula based on the pool's utilization rate — higher utilization leads to higher rates. It fluctuates in real-time with borrowing demand.

Aave's mainnet USDC deposit rate fluctuates with utilization between roughly 3.5%–6%; USDC vaults curated on Morpho yield approximately 5%–7% after curator fees.

4.4 MakerDAO / Sky Savings Rate (DAI's DSR / USDS's SSR)

This is a "policy-like rate" directly set by protocol governance. DAI's DSR (Dai Savings Rate) and USDS's SSR (Sky Savings Rate) are widely cited, functionally similar to a policy rate set by a central bank — they are not determined by market matching nor triggered by algorithmic utilization, but by a governance vote of Sky.

DSR/SSR's governance setting, FRR's market weighting, and Aave's algorithmic utilization represent a comparison of three fundamentally different rate generation mechanisms.

Governance setting vs. Market weighting vs. Algorithmic utilization — each of these three mechanisms has its own credibility issues and manipulation risks, and a mature market's benchmark should ideally come from the one least susceptible to manipulation (market-weighted real transactions of sufficient breadth and depth). In current numerical terms, the SSR was lowered by governance from 4.75% at the end of April 2026 to around 3.6%–3.75% by early June (the "governance setting" mechanism moves in tandem with the Fed's path); the circulating supply of USDS is approximately $11 billion.

4.5 Tokenized Treasury Yields (BUIDL / BENJI, etc.)

This is the ~4–5% "risk-free leg," a candidate qualifying as a "Crypto risk-free benchmark." BlackRock's BUIDL, Franklin Templeton's BENJI, etc., bring the coupon yield of US Treasuries on-chain. In current terms, major tokenized treasury tokens (BUIDL, USDY, USDM, USYC, etc.) paid approximately 4.1%–4.7% APY in April 2026, closely tracking the 3-month U.S. Treasury yield. Its yield can almost directly benchmark the traditional risk-free rate.

The secondary market pricing for this "risk-free leg" of tokenized treasuries is extremely tight — taking Ondo's tokenized treasury as an example, between February and April 2026, the median deviation of its traded price was only about 2 basis points, with 95% of trades falling within 5 basis points. This indicates that when the underlying asset is sufficiently standard and risk-free, on-chain price discovery can be very precise; in contrast, the "price" of high-risk instruments like perpetuals during closed-market hours is highly speculative — the lower the risk, the more real the price; the higher the risk, the more the pricing resembles guesswork.

4.6 Ethena sUSDe

This is a securitized product combining perpetual funding rates + collateral yield. Its APY is highly dependent on the funding rate levels in the perpetual market, making it essentially a repackaging of implied rates, rather than a benchmark itself.

Placing the seven candidates together: they each measure different things (leverage sentiment, real lending, algorithmic utilization, governance policy, risk-free coupons, institutional arbitrage