From mNAV Premium to a $100 Billion Vision: Michael Saylor's Journey into a Bitcoin Credit Empire

- 核心观点:MicroStrategy创新融资模式,推动比特币积累。

- 关键要素:

- 永续优先股融资60亿美元。

- 散户投资者占比高达25%。

- 持有比特币超62万枚。

- 市场影响:可能重塑数字资产企业融资方式。

- 时效性标注:中期影响。

Original author: Lesley

In the history of Wall Street financial innovation, few have excelled like Michael Saylor, transforming personal beliefs into corporate strategy and, in turn, reshaping the financing model of an entire industry. The chairman of Strategy (formerly MicroStrategy) is driving an unprecedented financial experiment: replacing traditional equity and debt financing with perpetual preferred stock to fund his aggressive Bitcoin accumulation strategy.

According to Bloomberg, Strategy has successfully raised approximately $6 billion in capital from the market through four rounds of perpetual preferred stock issuance this year. The latest round, "Stretch" (STRC), raised $2.5 billion. Michael Saylor described STRC as Strategy's "iPhone moment," emphasizing its potential to provide Bitcoin vaults with scalable and low-volatility access to capital markets.

This previously obscure business intelligence software company has leveraged such massive capital simply through its unwavering belief in Bitcoin. As of August 18, Strategy held 629,400 Bitcoins, with a total investment of $33.139 billion, worth over $72 billion at current market prices.

Top 100 publicly listed companies holding Bitcoin worldwide (Source: bitcointreasuries.net)

Even more striking is that retail investors accounted for nearly a quarter of the latest perpetual preferred stock issuance—a figure virtually unimaginable in the traditional corporate preferred stock market. However, behind this financial engineering effort lies a radical evangelist who once urged fans to "sell their kidneys for Bitcoin" and a legion of retail investors willing to follow his convictions.

To understand this financial experiment that could reshape the digital asset industry, we need to start from the beginning.

The Story and Mechanism of Perpetual Preferred Stocks

Perpetual preferred stock is a hybrid financial security with no fixed maturity date, combining the guaranteed returns of bonds with the perpetual nature of stocks. The issuing company does not need to repay the principal, only pays the agreed-upon dividends periodically, allowing the company to use investor funds indefinitely.

From an investor's perspective, purchasing perpetual preferred shares is equivalent to obtaining a "permanent right to receive dividends" - the returns mainly come from continuous dividend income, rather than the recovery of the principal at maturity of traditional bonds.

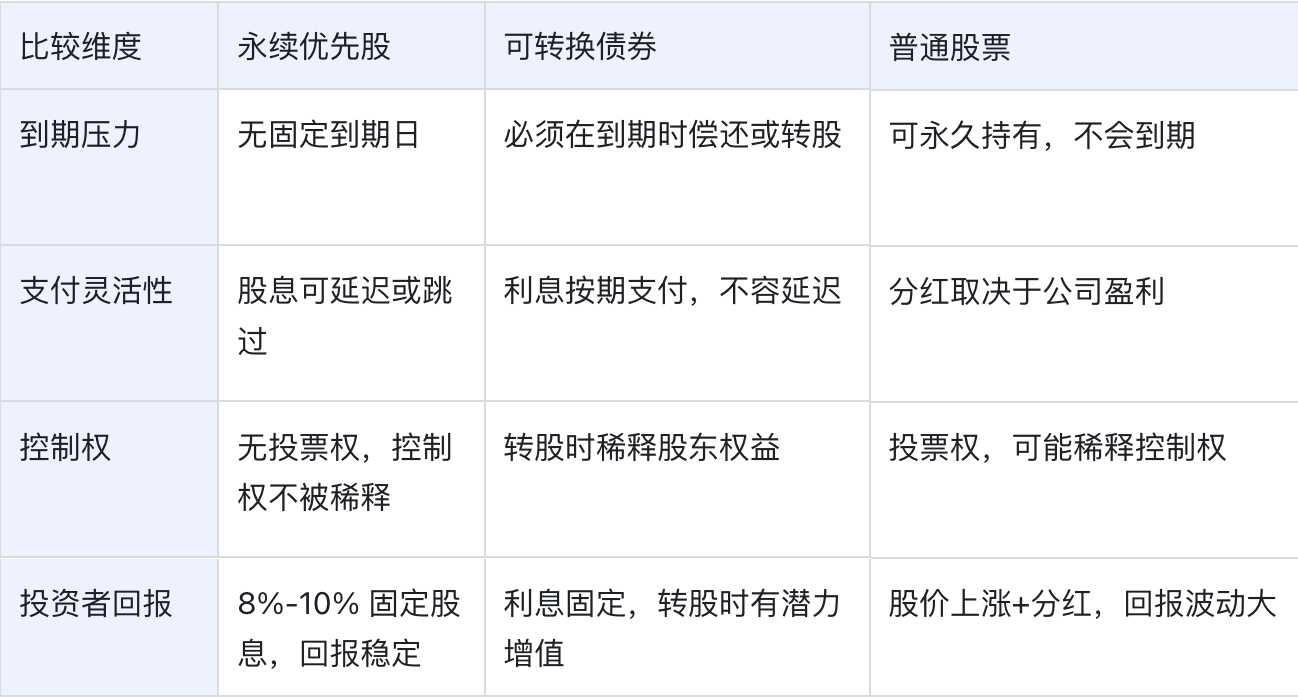

The following table compares perpetual preferred stock, convertible bonds, and common stock across several key dimensions:

In summary, perpetual preferred stock is a "third type of financing instrument" between debt and equity:

• For businesses, it allows them to lock in capital for a long period without having to repay principal, alleviate cash flow pressures with flexible dividend arrangements, and avoid equity dilution from issuing additional common shares;

• For investors, although they rank below debt in the capital structure, perpetual preferred stock generally offers higher, more guaranteed returns and is paid ahead of common stock in the event of a company's liquidation.

Because of this, it combines flexibility on the financing side with stable returns on the investment side, and is becoming an increasingly important option in corporate capital operations.

Although perpetual preferred shares provide Strategy with a flexible financing method, their market volatility, liquidity and structural risks cannot be ignored.

• Market volatility and liquidity risk: Bitcoin price volatility directly affects Strategy’s ability to repay and refinance. The burden of dividend payments increases with the scale of financing. According to Saylor’s “HODL” strategy, the sale of Bitcoin further limits the company’s channels for obtaining cash flow.

• Structural risks of the financing model: Dividend payments for non-cumulative perpetual preferred shares are at the issuer’s discretion, which may lead to refinancing difficulties when market confidence is shaken; over-reliance on retail investors, if retail enthusiasm fades, attractiveness to institutional investors becomes a challenge.

• Market bubbles and systemic risks: The crypto asset treasury company model may show signs of a bubble. Once market demand dries up, companies that rely on this financing model may face the risk of a broken capital chain, which may trigger wider market fluctuations.

Since the beginning of 2024, Saylor has raised over $40 billion in equity and debt financing. So far this year, Strategy has raised approximately $6 billion through four perpetual preferred stock offerings. Saylor even claims it could theoretically raise as much as $100 billion to $200 billion. These four offerings demonstrate a clear evolution in strategy and distinct market positioning.

Last month, Strategy launched STRC (Stretch), a floating-rate perpetual preferred stock designed to provide stable pricing and high returns to income-seeking investors seeking indirect Bitcoin exposure. STRC, with a $100 par value per share, will pay a monthly dividend and initially yield an annualized yield of 9%.

Saylor's launch of STRC (Stretch) is centered around its accessibility. Unlike STRK, STRF, and STRD, instruments he earlier championed as innovative but overly complex or volatile, STRC is more like a yield-enhanced savings account. By focusing on short-term investments and low price volatility, it eliminates the risk associated with long-term volatility while offering higher returns than bank deposits. Its overcollateralization with Bitcoin ensures that STRC will trade close to its $100 par value even during Bitcoin price fluctuations, providing investors with a more stable and attractive investment option.

Why choose perpetual preferred stocks? A fundamental shift in business models

As the bottleneck of traditional financing models becomes apparent, perpetual preferred shares have become a key option for Strategy to fundamentally transform its business model in the context of compressed mNAV premiums and the exploration of new sources of funds.

1. Traditional financing models encounter bottlenecks: mNAV premium compression

Strategy’s perpetual preferred stock experiment stems from a real challenge: mNAV premium compression.

The so-called mNAV premium refers to the phenomenon in which Strategy's stock price consistently outperforms the net asset value of its Bitcoin. This premium was once the core of Saylor's "financial magic"—the company was able to raise funds at a price higher than the actual value of Bitcoin, effectively "buying the coin at a discount." However, Brian Dobson, Disruptive Technology Equity Research analyst at Clear Street, noted, "The mNAV premium has compressed in recent weeks, and Strategy management is understandably concerned about creating too much dilution."

This shift forced Strategy to seek new financing paths. Traditional common stock issuance became significantly less efficient when the mNAV premium narrowed. While the convertible bond market offered lower costs, it eliminated retail investors, a key source of funding. The emergence of perpetual preferred stock was a necessary response to these constraints.

2. Discovering New Sources of Funding: Retail Investors’ “Faith-Driven” Model

More importantly, Saylor discovered an unprecedented financing opportunity: directly converting personal influence into corporate capital.

Michael Saylor currently has 4.5 million X Followers (Source: X Platform)

Michael Youngworth, Head of Global Convertibles and Preferred Strategy at Bank of America, admitted: "As far as I know, no company has ever capitalized on retail investors' enthusiasm like Strategy." In the latest STRC issuance, retail investors accounted for as much as 25%, which is almost unimaginable in the traditional corporate preferred stock market.

These retail investors adopt a faith-driven investment model for Strategy, providing the company with a relatively stable source of funding. Compared to institutional investors, they are less susceptible to short-term market fluctuations and are more willing to accept higher risk premiums. This unique investor structure has become a key competitive advantage for Strategy compared to traditional companies.

3. Strategic transformation and upgrading: from equity financing to a hybrid capital structure

The introduction of perpetual preferred shares actually marks a fundamental shift in Strategy's business model.

Under the traditional Strategy model, financing relies on rising stock prices, but this model is highly dependent on market sentiment and Bitcoin price fluctuations. The new model creates a relatively stable "middle layer" through perpetual preferred stock: preferred stock investors receive relatively certain dividend returns, while common stock shareholders bear more volatility risk. The company then receives perpetual funds with matching maturities to hold Bitcoin, a perpetual asset.

This redesign of the capital structure allows Strategy to better respond to market cycles. Even if Bitcoin prices fall and the mNAV premium disappears, the company can still maintain its financing capabilities through perpetual preferred shares.

4. Ultimate Goal: Building a $100 Billion BTC Credit Concept

Saylor’s ambitions go far beyond this. He speculates that “in theory, $100 billion… or even $200 billion could be raised,” with the goal of creating a large-scale “credit” system with Bitcoin as the underlying asset.

The core logic of this vision completely overturns traditional corporate financing: instead of relying on cash flow from products or services, it builds a self-reinforcing mechanism: "Holding Bitcoin → generating a stock price premium → financing to purchase Bitcoin → forming a positive feedback loop." Through multi-layered financing tools such as perpetual preferred stock and convertible bonds, Strategy seeks to transform volatile digital assets into a stable source of income, leveraging the mNAV premium to achieve arbitrage opportunities by "buying Bitcoin at a discount," ultimately building a financial empire centered around Bitcoin.

However, this financial experiment is fraught with risk. If successful, Bitcoin could transform from a speculative asset into a widely accepted financial collateral. But as short-seller Jim Chanos warns, an 8-10% perpetual dividend payout could become a heavy burden if Bitcoin declines. Yuliya Guseva of Rutgers Law School has even bluntly stated, "If market appetite dries up, this model will no longer be sustainable." Saylor is betting on the future of Strategy, betting on whether digital assets can redefine the fundamental rules of the modern financial system.

Conclusion: Innovation or Risk?

Strategy's perpetual preferred stock experiment represents a significant innovation in the financing model for digital asset companies. Michael Saylor cleverly combined personal influence, market sentiment, and digital asset investment through financial innovation to create an unprecedented path for corporate development.

From a broader perspective, Strategy's experiment represents a fundamental restructuring of the relationship between businesses and investors in the digital economy. Traditional corporate valuation systems—based on cash flow, profitability, and balance sheets—are completely ineffective here. Instead, a new value creation mechanism based on asset appreciation expectations and market sentiment is emerging. This is not only a financial innovation, but also a test of the boundaries of modern corporate theory.

Regardless of the ultimate outcome, Strategy's experiment has provided a replicable template for subsequent digital asset companies. It also serves as a wake-up call for regulators: When corporate financing increasingly relies on retail investor sentiment and asset bubbles, can traditional risk management frameworks still effectively protect investor interests? The answer to this question will determine the future direction of the digital asset industry.