当市場「提前定價了完美」,三星業績再好也不夠好了

- 核心觀點:儘管三星電子第二季營業利潤暴增19倍刷新歷史紀錄,甚至超越輝達,但因市場已提前定價「完美」預期,財報落地觸發資金出貨,股價單日暴跌,凸顯「買預期,賣事實」的交易邏輯。

- 關鍵要素:

- 業績「看起來完美」:第二季營業利潤89.4兆韓元(約584億美元)超預期,營收翻倍至171兆韓元,但股價一度跌8%,SK海力士等晶片股同步承壓。

- 市場焦點轉移:投資者不再僅關注利潤增速,而是轉向自由現金流改善的可持續性及股東回報政策,悲觀預期認為高估值已無安全邊際。

- 宏觀背景預警:Meta暗示收斂AI資本支出,觸發高貝塔動能股疫情以來最大兩日拋售,儲存晶片板塊高估值邏輯面臨系統性重估。

- 結構性問題浮現:代工及邏輯晶片業務虧損或擴大,且因薪酬協議計提特別獎金準備,若不扣除該成本,營業利潤將更超預期。

- AI需求支撐景氣度但邊際趨弱:儲存供應短缺至少延續至2027年,但Counterpoint警告75-80%的高利潤率可能招致監管壓力。

Original Author: Dong Jing

Original Source: Wall Street CN

Samsung Electronics delivered a historic report with a 19-fold surge in profits, yet saw its stock price plummet in a single day. This is not because the performance was insufficient, but because the market had already priced in "perfection." The earnings release merely served as a signal for capital to take profits.

On July 7, a Wall Street CN article reported that Samsung Electronics' second-quarter operating profit surged approximately 19 times year-on-year to 89.4 trillion Korean Won (approximately $58.4 billion), not only breaking the quarterly historical record but also surpassing Nvidia's operating profit of $53.536 billion in the previous quarter, making it the company with the highest quarterly operating profit in the world. Revenue doubled to 171 trillion Korean Won, both exceeding the average analyst expectations. However, after the earnings release, Samsung's stock price once fell by up to 8% in a single day, South Korea's KOSPI index fell by 6%, and SK Hynix fell by over 7%.

Another Wall Street CN article pointed out that the logic of "buy the rumor, sell the news" played out clearly once again. On the eve of the earnings release, the U.S. Philadelphia Semiconductor Index rose 2.2% in a single day, the S&P 500 rose 0.7%, and the Nasdaq 100 rose 1.3%. As the good news materialized, capital quickly withdrew.

Brian Cho, a portfolio manager at Causeway Capital Management, stated bluntly that what the market truly wants to see is whether the improvement in free cash flow can form a sustainable step-change, and how management treats shareholder returns — the pricing logic has shifted from "how fast are profits growing" to "can these profits be turned into real cash distributed to shareholders."

Furthermore, the sharp reversal in market sentiment has its macro background. Last week, Meta first hinted at tightening capital expenditures, triggering the largest two-day sell-off in high-beta momentum stocks since the COVID-19 pandemic. Samsung's decline also pressured fellow chip stocks SK Hynix and Micron, and the high valuation logic of the entire memory chip sector is facing a systematic revaluation.

Impressive Performance, but Not Enough

As reported in the Wall Street CN article, Samsung's second-quarter operating profit is expected to reach 89.4 trillion Korean Won, a sequential increase of 56% from the previous quarter. Analysts had forecast an average of 84.2 trillion Korean Won. During the same period, revenue reached 171 trillion Korean Won, surpassing the market estimate of 169.2 trillion Korean Won and representing an increase of about 129% year-on-year. The company plans to release its full financial report on July 30, which will disclose net profit and segment data for each business division.

The core driver of this growth is the sustained tight supply of memory chips. The strong demand for High Bandwidth Memory (HBM) from AI data centers has led manufacturers to shift production capacity towards high-end products, causing supply shortages of traditional DRAM and NAND memory chips and driving up prices across the board.

According to HSBC data, the average selling price (ASP) of DRAM rose by over 40% quarter-over-quarter in Q2, while NAND prices rose by over 50%. Citigroup Research data is similar, showing a sequential increase of 44% and 53% for DRAM and NAND average prices, respectively, in the same period.

However, while the revenue of 171 trillion Korean Won was higher than the average analyst estimate, it fell short of some institutions' optimistic forecast of 173.9 trillion Korean Won. Against a backdrop of already elevated valuations, this slight shortfall was enough to trigger profit-taking.

The spotlight on the memory business has obscured several cracks in the company's overall structure. Analysts predict that losses in Samsung's foundry and Logic System Integration (LSI) business may have widened further in this quarter, partly due to bonus expenses being proportionally allocated to the overall costs of the semiconductor division.

In May of this year, Samsung reached a compensation agreement with its chip division employees, linking performance bonuses to operating profit and stipulating that, subject to meeting specific profitability targets, 10.5% of the semiconductor division's annual operating profit would be set aside for special bonuses. Some analysts point out that without this provision, Samsung's operating profit would have exceeded market expectations even further.

AI Demand Supports Memory Boom, but Marginal Signals Weaken

The core logic driving this super-cycle in memory chips remains intact: the massive global expansion of AI data centers has spurred strong demand for high-end memory chips, and memory shortages have become a key bottleneck for AI development.

Several industry executives, including Nvidia CEO Jensen Huang and OpenAI COO Brad Lightcap, have warned about this. Major manufacturers are prioritizing the supply of high-end memory products, leading to simultaneous shortages of traditional memory products. Analysts predict that the supply shortage is likely to persist at least until 2027.

Market research agency Counterpoint estimates that the average operating profit margin for the three major memory manufacturers — Samsung, SK Hynix, and Micron — will remain in the 75% to 80% range in the second quarter of this year. The agency noted in its report that some view such high profit margins as "excessive," and warned that "if this situation persists, memory manufacturers may face regulatory pressure."

Furthermore, a Wall Street CN article mentioned that signals from the upstream of the industry chain are more noteworthy than the financial results themselves. Meta recently hinted at setting a cap on AI capital expenditures, which the market interpreted as an early warning that tech giants' AI infrastructure investment might have peaked, directly triggering one of the most violent two-day sell-offs in high-beta momentum stocks since the COVID-19 pandemic.

Jean Boivin's team at the BlackRock Investment Institute put the issue more directly: the core of the AI bubble debate is not current valuations, but whether future earnings can be sustained at extraordinary levels. If AI cannot translate its current scarcity into real productivity improvements, the current lofty earnings expectations will face a correction.

Samsung Lags Behind SK Hynix, South Korea Bets on AI Chip Dominance

From a national strategic perspective, the South Korean government views Samsung and SK Hynix as core pillars in the race for global AI leadership. Samsung Group and SK Group plan to each build two chip factories in southwestern South Korea, with a combined investment scale of 800 trillion Korean Won, to rapidly expand production capacity. South Korea aims to double its memory chip production capacity within five years, and Samsung has announced it will invest over $70 billion in capacity expansion and R&D by 2026.

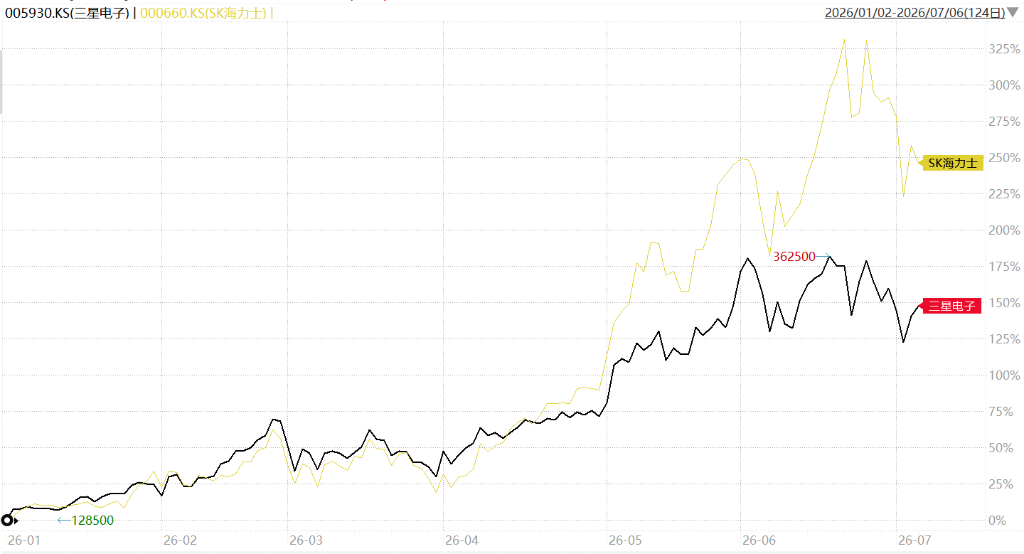

In terms of stock performance, Samsung has gained approximately 165% year-to-date, but significantly lags behind rival SK Hynix's gain of about 260%. The gap between the two mainly stems from differences in product mix — SK Hynix's business is highly concentrated on high-end memory chips catering to AI computing demand, whereas Samsung's product portfolio is more diversified, spanning chips and consumer electronics. This divergence sends a clear signal: on the current track, focus is more favored by capital than sheer scale.

Samsung's full financial report will be released at the end of this month, and the segment data for each business division will tell the market how much real value has been generated from this wave of AI capital expenditure. That number will become an important benchmark for the next phase of the AI hardware investment thesis.