SemiAnalysis:沒有看空輝達,「AI央行」或撬動7兆美元債務雪球

- 核心觀點:SemiAnalysis 最新分析指出,輝達正透過「後盾計畫」為 AI 算力租賃商提供最低收入保證,扮演類似「AI 央行」的角色,旨在撬動銀行放貸並擴大 GPU 買方基礎;預計到 2029 年,全球 AI 債務融資規模將突破 7 兆美元,成為僅次美國房貸市場的第二大資產支持債務市場。

- 關鍵要素:

- 輝達利用其 AA/Aa2 信用評級為 Neocloud 提供 GPU 租賃收入兜底(通常 6 年期),若市場需求不足,輝達承諾按預設價格購買算力,以此降低銀行放貸風險並推動 GPU 銷售。

- AI 基礎設施融資模式正從依賴雲巨頭現金流轉向大規模債務,形成「三位一體」困局:項目啟動需同時具備資本(貸款)、包銷合約(客戶)和數據中心(容量),三者缺一不可且易陷入循環。

- 在兜底結構下,Neocloud 需犧牲約 18%的上行收益(以 6 年平均抽成計)以換取項目可融資性;在最差情景下項目回報可能接近零,但貸款人僅要求該情景下能還債。

- 目前輝達兜底項目集中在亞太,包括澳洲 SharonAI(72MW 工廠,總兜底價值 48.8 億美元)和印尼 Firmus(360MW 集群,預計六年客戶收入 250-300 億美元)。

Original Author: Zhao Ying

Source: Wall Street Sights

On July 6, renowned semiconductor research firm SemiAnalysis posted six consecutive tweets on platform X, reporting that Nvidia's Kyber NVL144 rack system faced over 12 months of delays due to manufacturing issues with the PCB mid-plane. Asian AI hardware supply chain stocks plummeted in response.

Nvidia later responded, stating its "roadmap remains unchanged", but did not disclose specific progress details.

The controversy did not subside. On July 7, SemiAnalysis released a long-form paid report, turning its "critique" toward Nvidia. However, this time, it did not play the role of a "bear".

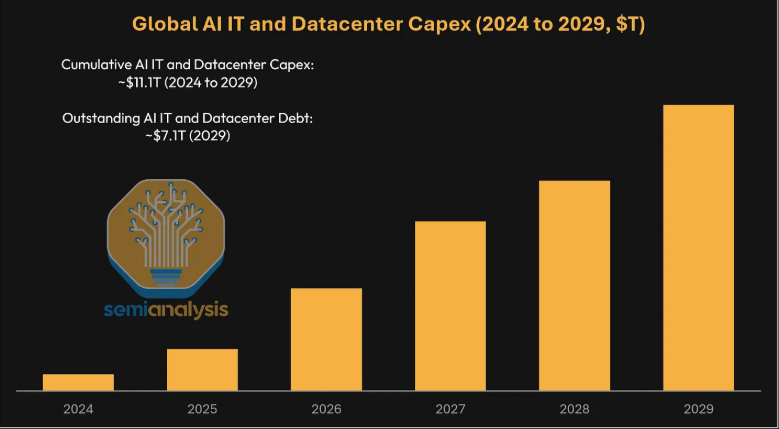

SemiAnalysis predicts: By 2029, the global scale of AI debt financing will surpass $7 trillion. What does $7 trillion signify? It would become the second-largest asset-backed debt market globally, trailing only the US residential mortgage market (approximately $13 trillion).

What is Nvidia's role in this? SemiAnalysis disclosed a strategic plan by Nvidia—the "backstop" plan. Nvidia is utilizing its own AA/Aa2 investment-grade credit rating to provide minimum revenue guarantees for AI computing power lessors, thereby encouraging banks to lend. In other words, Nvidia is acting as the ultimate lender and insurer for the entire AI ecosystem, booking significant sales while partially shouldering the risk of insufficient downstream demand. SemiAnalysis compares Nvidia to the "Central Bank of AI".

Regarding the discussions on platform X about whether SemiAnalysis is "bearish on Nvidia," the firm stated:

It has not released any positive or negative views on Nvidia's stock; it is merely accurately capturing supply chain and technical details. The market can make its own trades.

AI Debt Snowball: Topping $7 Trillion by 2029, Nearing the US Mortgage Market

SemiAnalysis believes that AI infrastructure construction is forming a multi-trillion dollar credit market. By 2029, outstanding AI-related debt could reach approximately $7.1 trillion, surpassing all other US asset-backed debt markets except for mortgage financing.

This debt primarily comes from two types of capital expenditure. One is AI IT CapEx, including GPUs, networking, storage, and supporting CPUs. The other is AI data center CapEx, covering the facilities, power, and cooling infrastructure required to house these GPUs.

Previously, cloud giants like Google, Amazon, Meta, Microsoft, and Oracle mainly relied on their own cash flow to build AI clusters. However, over the past year, Oracle, Meta, and even Google have started using more debt. As project scales continue to grow, market constraints are no longer just about obtaining GPUs or finding data center space, but about whether sufficient cheap, long-term funding can be secured.

SemiAnalysis concludes that the financing methods for AI CapEx are changing. Cloud giants have limited balance sheets. If all AI clusters rely on endorsements from a few investment-grade cloud vendors, new projects will eventually hit credit bottlenecks.

The "Trinity" Dilemma: Capital, Customers, and Data Centers, All Indispensable

SemiAnalysis breaks down AI project financing into a "trinity": capital, offtake contracts, and data centers.

First is capital. Lenders typically require long-term take-or-pay contracts from investment-grade cloud vendors, or similar credit guarantees, before they are willing to lend. In other words, lenders value the creditworthiness of the underlying customer, not the Neocloud itself.

Second is offtake. To secure customers, Neoclouds often need to prove they can pay GPU deposits and lock in equipment. However, to obtain equity funding, they need to prove they already have customers and loans. This creates a chicken-and-egg problem in the early stages of a project.

Third is data centers. Neoclouds either need to use customer contracts and financing to convince data center operators to lease capacity, or build their own data centers. The latter is more capital-intensive and takes longer.

This model locks the market into a "5-year, cloud-giant endorsed" template. The problem is that many VC-backed AI startups and inference service providers need short-term, large-scale computing power, not 5-year long-term contracts. Inference providers, in particular, are unwilling to bear long-term price and demand risks, often preferring to forgo computing power rather than sign leases exceeding 1 year.

Nvidia, the "AI Central Bank": Leveraging AA-rated Credit to Pry Open the Entire Market

Nvidia introduced the "backstop plan" to fill this financing gap.

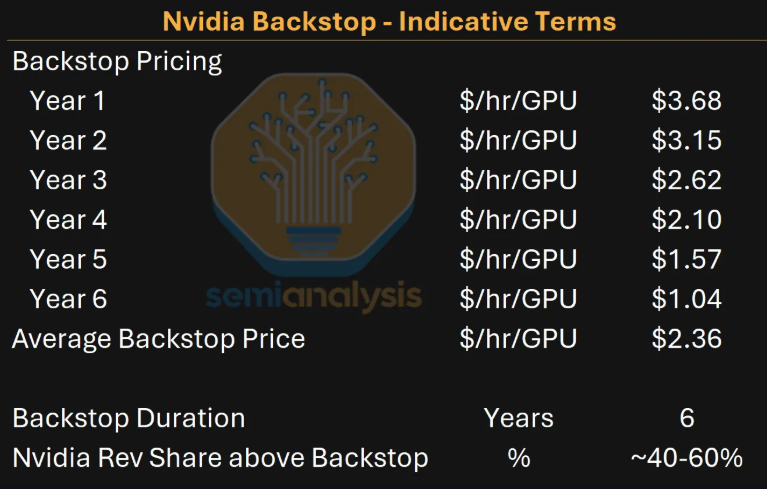

According to SemiAnalysis, Nvidia provides GPU rental income guarantees to Neoclouds. If third-party customer demand is insufficient, Nvidia commits to purchasing computing power at a predetermined price. If the Neocloud rents out computing power at a higher price, Nvidia shares a portion of the excess revenue.

These arrangements are typically for 6-year terms, offering a minimum revenue guarantee for the underlying GPU capacity based on a pre-agreed price curve. The Neocloud can still rent computing power to any customer and offer more flexible lease terms. Nvidia's guarantee is triggered only when market demand is insufficient and capacity cannot be rented at market prices.

This is the origin of the "AI Central Bank" metaphor. Nvidia isn't actually issuing currency, but in the AI computing power credit system, it acts as a sort of ultimate buyer and credit endorser. Lenders can evaluate the worst-case scenario for a project based on Nvidia's AA/Aa2 credit rating, making them more willing to lend.

For Nvidia, this helps expand the buyer base for its GPUs. If the market can only rely on a few mega-cloud vendors signing 5-year offtake contracts, GPU demand will quickly hit financing constraints; these cloud vendors are also hedging against Nvidia's systems with their own custom chips. Supporting Neoclouds and more enterprise clients essentially opens new financing channels for GPU demand.

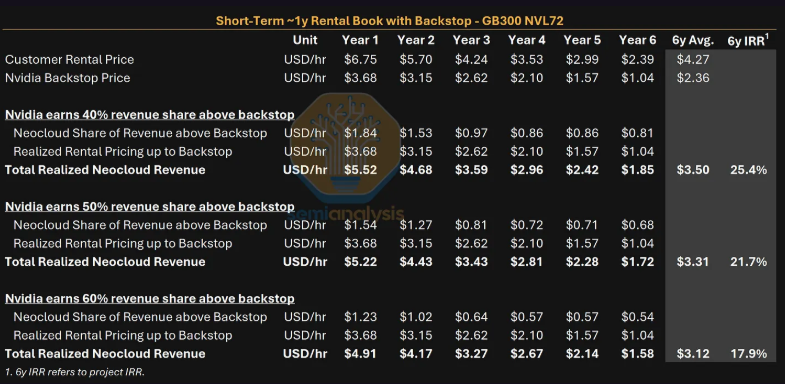

Deconstructing the "Backstop Plan" Structure: How Much Nvidia and NeoCloud Earn

SemiAnalysis emphasizes that Neoclouds do not use Nvidia's credit for free. Under the backstop structure, Neoclouds must sacrifice some upside potential in exchange for project bankability.

In an illustrative price curve, the 6-year average backstop price is $2.36 per GPU per hour. Assuming the 1-year lease price for GB300 in the first year is $6.75 per hour, and the first-year backstop price is $3.68 per hour, the difference between the customer price and the backstop price is $3.07. If Nvidia takes 40% of the amount exceeding the backstop price, Nvidia gets $1.23, Neocloud gets $1.84. The Neocloud's actual first-year revenue is $5.52 per hour, lower than the $6.75 without the backstop.

Over six years, in this scenario, Nvidia takes roughly an 18% cut on average. The Neocloud's project IRR also declines. With Nvidia's backstop and mainly 1-year short-term leases, the project IRR is 25.4%; without the backstop, but still able to secure financing and rent, the IRR could reach 40.7%.

The key is the worst-case scenario. If demand is low, the Neocloud can only rent computing power back to Nvidia, resulting in project returns near zero, or slightly negative. Lenders do not require the project to be profitable in the worst case, only that it can still service its debt. Therefore, whether the debt is viable increasingly depends on the reliability of Nvidia's backstop.

This is the core issue investors should focus on: Nvidia's arrangement helps drive GPU sales and Neocloud expansion in the short term, but if computing power demand falls short of expectations, Nvidia will have to absorb the revenue shortfall. The debt may not be directly on Nvidia's books, but the safety net of the financing model is increasingly centralized around Nvidia's credit.

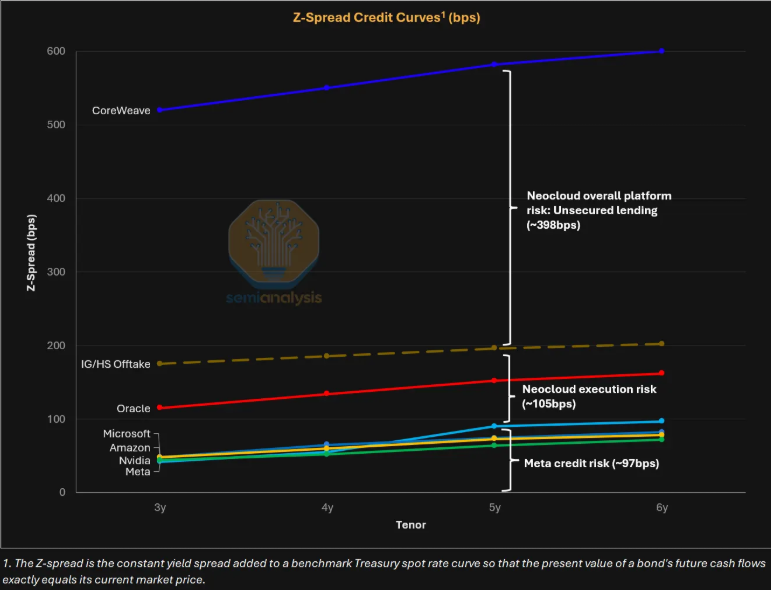

GPU Financing Pricing Essentially Depends on Who Provides the Endorsement

SemiAnalysis states that the pricing in the current GPU financing market depends primarily on who signed the long-term offtake contract, not on the Neocloud's own credit.

CoreWeave serves as a reference. The yield on its 5-year unsecured bonds is about 10%. However, for its $8.5 billion DDTL 4.0 delayed draw term loan backed by Meta, the fixed-rate portion costs about 5.9%, only 90 basis points higher than Meta's 5-year bond yield of approximately 5.0%. This 90 basis point spread roughly represents the market's pricing for CoreWeave's execution risk.

If a Neocloud operates without long-term cloud giant offtake, financing costs increase significantly. For top-tier Neoclouds, unsecured financing might require paying an interest rate of about 10%, roughly 4 percentage points higher than endorsed financing. With a 70% to 80% loan-to-value ratio, the financing cost rises from 5.62% to 10%, and the pre-tax profit margin drops from 14.8% to 5.4%.

Nvidia's backstop would place pricing somewhere in between: a total yield higher than the roughly 5.9% on current cloud-giant-endorsed deals, but lower than the roughly 10% yield on CoreWeave's unsecured bonds. Banks focus most on the Debt Service Coverage Ratio (DSCR). For projects with Nvidia's backstop, loan sizing is usually based on the scenario where the backstop is triggered, requiring a minimum DSCR of 1.3x in the early years, corresponding to a typical loan-to-value ratio of 70% to 80%.

Public Projects Scale Up in Asia-Pacific, Backstop Model Begins Implementation

Publicly announced Nvidia backstop projects are currently concentrated in the Asia-Pacific region.

The first is the SharonAI 72MW AI factory in Australia. Announced in June 2026, it plans to scale up to 40,000 GB300 units under a 6-year backstop. SharonAI disclosed a total backstop value of $4.88 billion, translating to an average floor price of roughly $2.33 per GPU per hour over six years.

Another is Firmus's 360MW AI cluster on Batam Island, Indonesia, potentially located in DayOne's Kabil Industrial Tech Park. Announced on June 29, 2026, it indicates Nvidia's backstop is entering larger scales.

Firmus estimates 6-year customer revenue for this project at $25 billion to $30 billion, targeting AI-native companies, enterprise clients, and inference providers, offering various lease terms. However, Firmus still needs to finalize the data center provider or continue with self-building before deploying the GPUs.

SemiAnalysis also notes that Nvidia is not the only GPU manufacturer using backstop arrangements. AMD has offered similar arrangements to clients like AWS, OCI, DigitalOcean, Vultr, Tensorwave, and Crusoe since last year: if clients purchase more AMD GPUs and the Neocloud cannot fully sell the capacity, AMD is willing to lease some back under long-term contracts for internal software development.

SemiAnalysis Denies Bearish Stance, But Market More Sensitive to Its Signals

This article comes amidst controversy surrounding SemiAnalysis itself.

On the morning of July 6, SemiAnalysis posted consecutive tweets on platform X, claiming that Nvidia's Kyber NVL144 rack architecture faced a major delay, postponed by over 12 months until 2028. This news triggered pre-market concerns and caused declines in several AI hardware supply chain stocks in Japan, South Korea, and Chinese Taiwan. Nvidia subsequently responded that its product roadmap had not changed, denying any impact on core progress.

This made SemiAnalysis's subsequent article more susceptible to market interpretation as bullish or bearish on Nvidia. In response, SemiAnalysis stated on X that it had not released any positive or negative views on Nvidia stock, merely sharing information about the company's supply chain and technical details.

Crackerjack Finance countered the "bearish" interpretation, stating that SemiAnalysis's charts showed actual data for the second half of the year was 20% higher than market expectations, deriving an earnings per share of about $15 for the following year and a stock price target between $300 and $400. THE Grand Poobah commented that "the three-party circular financing seems insufficient anymore," pointing to market concerns over the increasing complexity of financing structures.

The issue is that AI-related assets have experienced years of appreciation, with valuations and expectations at high levels. Any supply chain risk signals or changes in financing structures will be rapidly amplified. SemiAnalysis's clarification shows it did not directly offer a stock view, but following the Kyber NVL144 incident, the market influence and credibility debate surrounding its supply chain revelations will continue to coexist.

For investors, the true meaning of this "long-form report" is this: The AI competition is no longer just about "who has the GPUs," but "who can assemble GPUs, debt, customer contracts, and data centers simultaneously." Nvidia's backstop mechanism could continue to amplify GPU demand, but it may also concentrate more of the tail-end pressure of the AI debt cycle onto Nvidia's own creditworthiness.