AC exits Sonic board, DeFi godfather pulls another vanishing act

- Core Thesis: Andre Cronje (AC)'s exit from the Sonic board to focus on his new project, Flying Tulip, reflects how the value of crypto projects often relies on founder reputation rather than fundamentals, with secondary market investors bearing the brunt of the downturn as industry capital accelerates its outflow.

- Key Elements:

- Following AC's exit from the Sonic board, the S token plunged from a yearly high of $1.03 to $0.028, and the on-chain TVL evaporated by 98% from a peak of $1.14 billion to approximately $20 million.

- In his statement, AC precisely delineated his responsibilities, stating he was only in charge of technical support for Sonic, while decisions regarding tokenomics and migration were not under his leadership. He revealed that for the past 18 months, his primary focus was on the Flying Tulip project, which is valued at $1 billion.

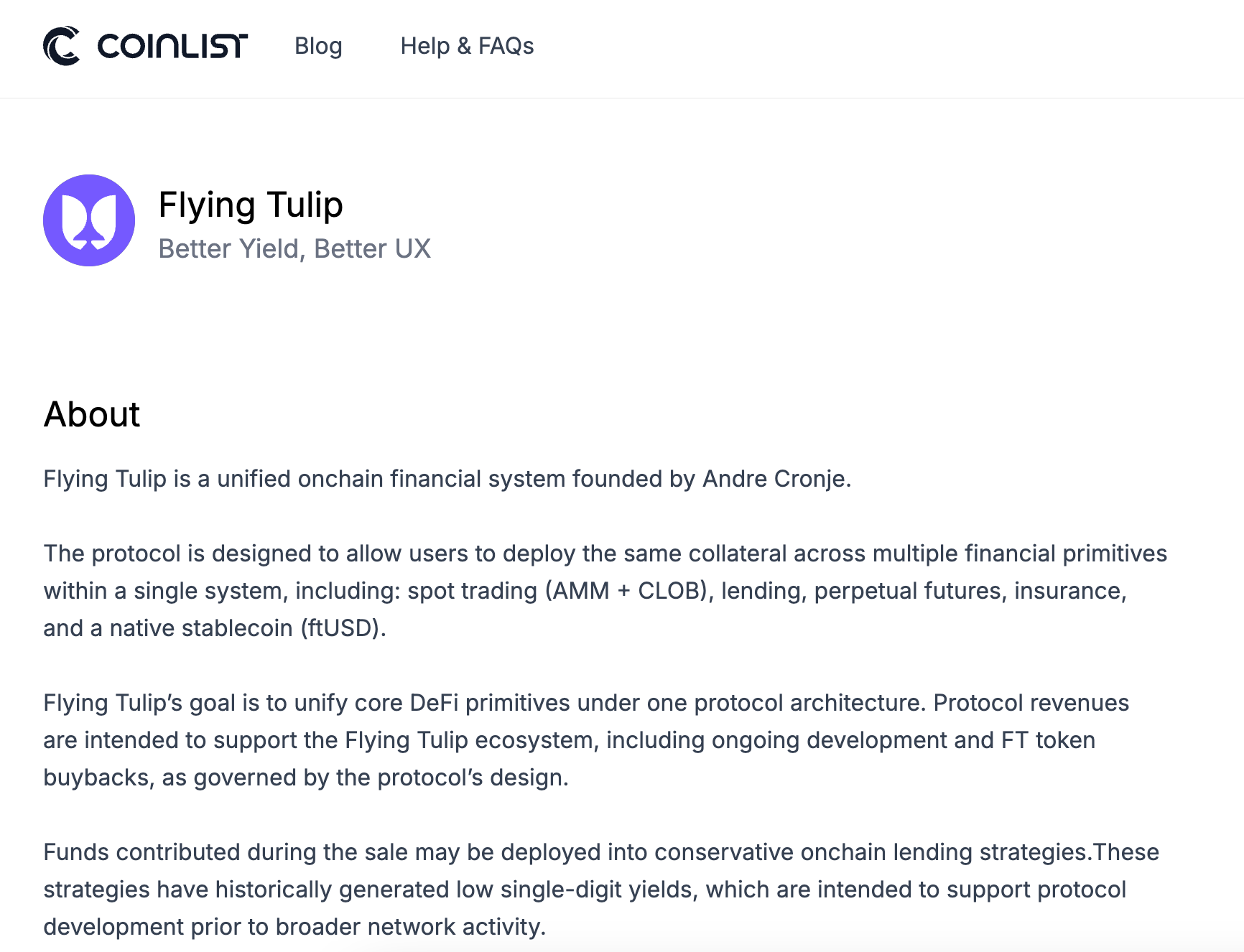

- Flying Tulip's ftPUT NFT grants primary holders a perpetual put option, allowing them to burn the token at any time and redeem their principal at the original price. However, secondary market buyers are not protected by this mechanism.

- The funds raised by Flying Tulip are untouchable and are entirely deposited into lending protocols to generate an annualized interest of around 4% for operational expenses. The team has no initial token allocation.

- Within the five months prior to AC's departure from Sonic, the CEO and Head of Business both resigned, leading to a complete management overhaul. The new team admitted that "as the token price falls, community sentiment also declines."

Original Author: Ku Li, TechFlow from Shenzhen

The feeling of being in crypto this year is probably like watching U.S. stocks hit new highs every day, then opening your own position, staying silent for three seconds, and closing it.

BTC is down nearly 20% year-to-date, ETH is even worse, and we won't even mention the altcoins. Under such market conditions, a 90% drop for any public chain token isn't news. What's even colder than the prices is the sense of people leaving and the warmth fading away.

On June 19th, DeFi godfather AC and two other founding directors together resigned from the board of Sonic Labs. The S token was trading at 0.028 at the time, a mere fraction of its year-high of 1.03, and the on-chain TVL had dropped from a peak of 1.14 billion last May to 20 million. According to DefiLlama data, that's a 98% evaporation.

The reaction within the crypto circle to AC leaving was muted. After all, he had already 'quit' once in 2022 before returning. This exit statement also sounded standard, saying he 'still is bullish on Sonic' but would no longer be involved in business decisions.

But the next part is what stings.

He said his main focus for the past 18 months has been on Flying Tulip. This project raised $200 million in a private round last August at a $1 billion valuation, and then opened a public sale on CoinList in February this year. Investors include names like Brevan Howard, DWF Labs, and Susquehanna.

In other words, during the time S fell from 1.03 to 0.028, AC was busy setting the stage for a brand new billion-dollar project.

What stings even more is Flying Tulip's token design.

Investors in the primary round received an NFT called ftPUT, which is essentially a perpetual put option. If the token loses value, they can destroy it at any time and redeem their principal at the original price. The CoinList public sale page clearly states that FT (divisible tokens, i.e., the normal coin) bought on the open market do not come with this right; only primary participants have it.

In contrast, S holders who bought on the secondary market are stuck with whatever price it drops to. 0.028 is 0.028. No floor, no redemption, nobody gives you a way out...

Not My Problem

AC's exit statement was posted on X, short, but every sentence seems carefully worded.

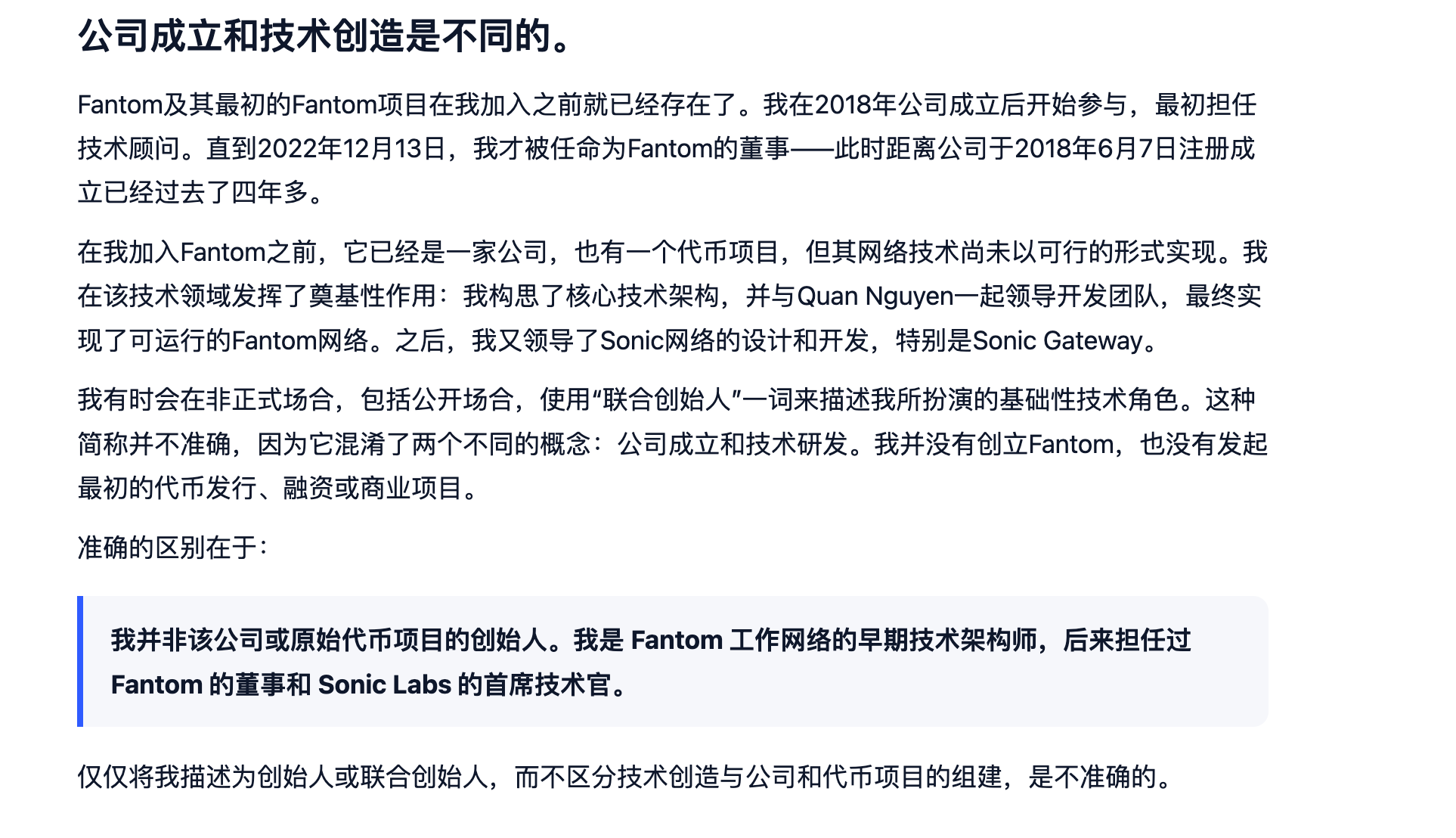

He said he joined Fantom in 2018 as a technical advisor and only officially became a director in December 2022. He is not the founder of Fantom, never was, just the earliest technical architect. He was responsible for the underlying technology, including the core system of Sonic and the cross-chain gateway.

Then comes the crucial part, which roughly translates to:

"I take responsibility for the technical decisions I led, but decisions regarding the migration, airdrop, tokenomics, and the handling of the old network—I was neither the initiator nor the decision-maker.".

In one sentence, he detached himself from the 97% drop in the S token. The technology was my doing, and the technology is fine. As for why the coin you bought fell from one dollar to three cents, that was someone else's decision.

The author won't judge whether this claim holds water, but must admit the clean break is admirable.

Most project founders, when they exit, either stay silent, hoping the issue fades, or issue a vague statement full of 'we' and 'the team,' blurring all responsibility. AC is different. He drew the boundary of his responsibility with extreme precision, so precise that it's hard to refute, because he indeed didn't handle the tokenomics.

And this wasn't a spur-of-the-moment decision.

In March 2022, AC announced his exit from the crypto industry, citing regulatory pressure and burnout. At that time, Fantom's TVL evaporated by nearly a third within a week, drawing widespread criticism from the community. A few months later, he quietly returned, focusing on Sonic's technical reconstruction.

Left saying he was tired, returned without a sound, and upon leaving again says, 'I've actually been busy with other things for the past 18 months.'

On Sonic's side, in the six months before he left, executives changed one after another. CEO Mitchell Demeter, hired just last September, resigned in February this year, along with the head of business. After the CEO left, the board took over management for a few months, and now the board has also stepped down, replaced by a new CEO, Matt Visser, who has never managed a frontline public chain before.

In five months, the entire management layer was swapped from top to bottom. Sonic's official statement didn't sugarcoat it, directly stating, 'The coin price has fallen, and community sentiment has also fallen. We won't pretend otherwise.'

This kind of 'giving-up honesty' is rare in the crypto industry. But the problem is, the ones telling the truth are the new team, the one leaving is the person with the valuable name.

The Cicada Shell Strategy

Looking back at AC's trajectory over the past few years, you can see a pattern.

In 2020, he wrote Yearn Finance, a flagship product of DeFi Summer, with TVL once reaching tens of billions of dollars. He let it go without much management. Yearn later ran on its own, doing fairly well, but his involvement was minimal.

Then he moved on to Fantom's technical architecture, and Fantom had a rally. In March 2022, he announced his exit from the industry, and Fantom subsequently entered a prolonged downtrend, later rebranding as Sonic for a relaunch. He returned with the title of CTO. Sonic initially saw TVL surge past one billion, then collapsed all the way down to where it is now.

Each time, he extracted himself right at the peak of hype or at the start of a cooldown to work on the next thing. Each time, the holders of the old project bore the brunt of the decline after he left.

Flying Tulip is the fourth project he's currently working on. The author believes that this time, he might have truly absorbed the lessons from all previous experiences and built them into the token design.

If you participate in the Flying Tulip public sale on CoinList, spending $0.10 to buy an FT, you don't get the token itself. Instead, you receive an NFT called ftPUT, and the token is locked inside this NFT. This NFT *is* that perpetual put option. You have three choices.

First, do nothing. The token stays in the NFT, untradeable, but the redemption right remains. Whenever you want to exit, destroy the token and redeem your USDC or ETH at the original price. No matter how low the FT price drops on the secondary market, your principal has a floor.

Second, withdraw the token from the NFT to trade freely. But the moment you withdraw it, the redemption right is permanently voided. The principal corresponding to the withdrawn amount is released to the protocol for buyback and burn.

Third, partially withdraw, partially keep. Tokens remaining in the NFT continue to have protection; those withdrawn are exposed.

In an interview with The Block, AC himself said a very interesting thing, roughly meaning that because of the perpetual PUT, the money raised cannot actually be spent at all.

The actual funds raised are zero. So where do operating expenses come from?

All the raised funds are deposited into lending protocols like Aave and Ethena for a conservative strategy, targeting an annualized yield of around 4%. Assuming a full raise of one billion dollars, this would generate roughly $40 million in interest annually, used to support the team, development, and buybacks. The team has no initial token allocation; all FT must be bought back from the open market using protocol revenue.

The author must admit that this design is quite ingenious within DeFi. It addresses the worst problem in the crypto industry over the past few years: project founders taking the money and running, or spending it recklessly, leaving investors with nothing. AC's solution essentially ties his own hands. The funds cannot be touched, the team gets no pre-allocated tokens, and investors can exit anytime.

But as ingenious as it is, this protection only exists in the primary market. Once FT is listed on an exchange, tokens bought on the secondary market do not come with the ftPUT. This sentence is written in bold on the CoinList page.

Public market buyers see the same token but receive completely different treatment.

A Microcosm of the Industry

Money is flowing out of the crypto market this year; that's no secret.

BTC is down nearly 20% year-to-date, and the median decline for altcoins is far steeper. People in this space look at the Nasdaq hitting new highs, then switch back to their own portfolios. The feeling needs no description from me.

For many, their real strategy this year has been gradually moving their positions into U.S. stocks and stablecoin yield products. On-chain activity is visibly shrinking.

In this environment, AC's exit from Sonic is just the tip of the iceberg. The entire L1 track is experiencing a similar story: shrinking TVL, user loss, founding team churn, or outright disappearance. Sonic is just the sample because of its fame and extreme price drop.

But AC's case has a layer that other projects don't.

Flying Tulip's current valuation is about one billion dollars. Sonic's current market cap is about one hundred million. Same person, same period, one billion versus one hundred million, a tenfold difference. What's the difference? The difference lies in which side AC's name is attached to.

This is a fact in the DeFi industry that few are willing to admit openly.

The valuation of many projects is not built on revenue, users, or technological barriers. It's built on the name of a certain person. When the name is there, the money is there. When the name leaves, the money follows.

The bear market has torn off this veil. In a bull market, all L1s go up, and you can't tell if it's fundamentals or a name propping them up. When the tide goes out, what remains becomes very clear.

There's one more detail the author finds most interesting.

Flying Tulip's initial deployment chain is Sonic. AC left Sonic's board and no longer participates in any business decisions, yet his new project's first stop is on Sonic. He left, but his business is still there.

The captain got off the ship but opened a new shop on the dock, selling items more expensive than what was on the ship.