Gate 研究院:存储三巨頭市值集體破萬億

- 核心觀點:美光科技市值突破萬億美元,標誌著存儲行業正從傳統週期性硬體升級為 AI 算力的關鍵戰略資源,本輪增長由 HBM 等高階產品及長期供貨協議(LTA)驅動的結構性重估主導,而非簡單的週期反彈。

- 關鍵要素:

- 美光市值約 1.17 萬億美元,過去一年股價累計漲幅超 800%,主要受益於 AI 伺服器及數據中心對 HBM、DDR5 等高階存儲需求的持續拉動。

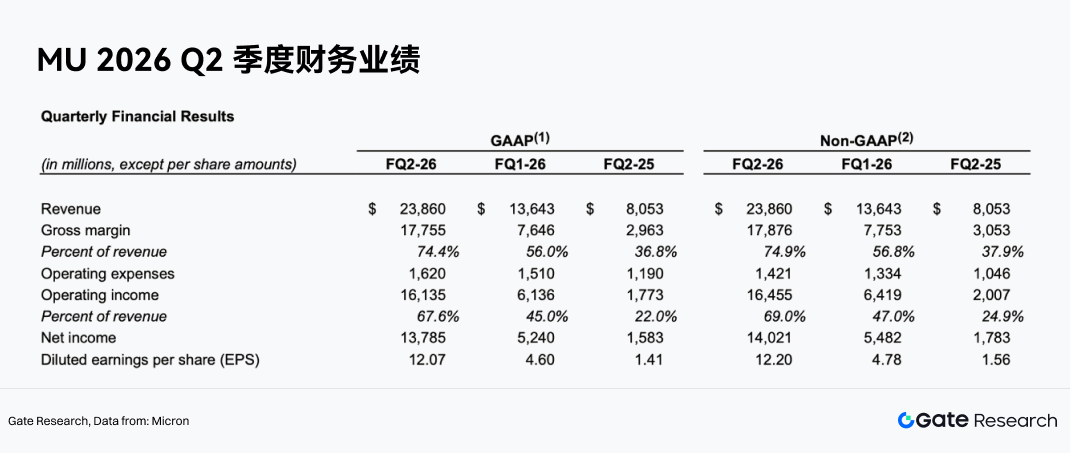

- FY2026 Q2 業績創紀錄:收入達 238.6 億美元,Non-GAAP 毛利率躍升至 74.9%,核心驅動力來自 AI 數據中心業務,其合計收入超 134 億美元。

- 產品結構升級是關鍵:HBM 等高階產品具備更強定價權,預計其 ASP 將同比上漲約 50%,推動利潤率和盈利穩定性顯著超越傳統 DRAM 週期。

- 長期供貨協議(LTA)正在改變商業模式:新型 LTA 不僅鎖定採購量,還部分鎖定價格(期限 3-5 年),提升了收入可見度與跨週期盈利能力。

- 行業供給持續緊張:DRAM 與 NAND 預計分別供不應求至 2028 年 Q2 和 2027 年 Q4,HBM 產能受限於工藝與良率,供給釋放緩慢,支撐價格彈性。

- Gate 平台已推出相關交易服務:用戶可使用 USDT 交易美光等美股現貨、永續合約及槓桿 ETF,實現數位資產與股票配置的統一管理。

Summary

- The total market capitalization of the global storage sector has experienced explosive growth, with the three giants Samsung Electronics, SK Hynix, and Micron Technology all surpassing the trillion-dollar mark.

- The continuous growth in demand for AI large model training and inference is significantly increasing data centers' demand intensity and value for storage products such as HBM, DDR5, and enterprise SSDs.

- Micron Technology has recently officially joined the trillion-dollar market cap club, becoming one of the most closely watched revaluation targets in the AI storage supply chain. According to data from StockAnalysis as of June 3, 2026, Micron's market cap is approximately $1.17 trillion.

- The core driver of the current storage sector rally is not a traditional DRAM cycle rebound, but rather the market beginning to reprice the structural value within AI servers, HBM, long-term agreements (LTAs), and the tight supply-demand dynamics of the storage industry.

- Gate has officially launched stock trading, allowing users to directly trade stocks and ETFs from major securities markets within the platform using USDT. The stock contracts section now offers perpetual contracts, supporting USDT settlement and 1-20x leveraged two-way trading. Gate has also introduced leveraged ETF tokens, providing investors with long exposure to stocks.

- Micron's trillion-dollar market cap is not the result of a single earnings cycle, but a manifestation of the combined effects of AI storage value revaluation, HBM product upgrades, the LTA mechanism, and improved industry supply-demand dynamics.

The AI-Driven Storage Sector

In the past, the storage industry was often viewed as a typical, strongly cyclical sector, with corporate profitability highly dependent on supply-demand fluctuations and price elasticity. However, in the AI era, storage is transitioning from a supporting component in general hardware to a critical resource within computing infrastructure.

Large model training and inference not only require more powerful GPUs and interconnection capabilities but also storage systems with higher bandwidth, larger capacity, and lower latency. Whether it's HBM on the GPU side or DDR5 and enterprise SSDs on the server side, their importance is markedly increasing. For cloud vendors and data center clients, storage is no longer just a cost item but a key variable influencing model training efficiency, inference throughput, and overall deployment costs.

The changes driven by AI application expansion are not merely about increased shipments of storage chips, but more importantly, a higher proportion of high-end products. Compared to regular DRAM, HBM offers higher bandwidth, greater integration, and higher added value; enterprise SSDs also benefit from enhanced data center workloads. As product mixes shift towards high performance, the revenue structure, profit margin structure, and valuation frameworks of leading manufacturers may all undergo changes.

Unlike the traditional historical logic of "raising prices to expand production," high-end storage products like HBM are constrained by manufacturing processes, yield rates, advanced packaging, and customer certification cycles, leading to relatively limited supply release speed. Meanwhile, core customers increasingly prefer to lock in capacity and a portion of prices through long-term agreements. This gives leading manufacturers greater revenue visibility and bargaining power than in the past, endowing the current boom with more distinct structural characteristics.

Micron Technology, Inc. (NASDAQ: MU) was founded in 1978 and is headquartered in Boise, Idaho, USA. It is a leading global provider of semiconductor memory and storage solutions. The company designs, manufactures, and sells DRAM, NAND Flash, NOR Flash, HBM, SSDs, and storage products for data centers, mobile devices, automotive, industrial, and consumer electronics. Using it as a case study is not to focus the article on a single stock, but because Micron, in its product portfolio, customer structure, earnings sensitivity, and market pricing, relatively typically reflects the evolutionary direction of the AI storage track.

Micron Technology

In the global memory chip industry, Micron, along with Samsung Electronics and SK Hynix, is a major DRAM supplier and a significant player in the global NAND market. As demand for large model training and inference continues to grow, AI servers' need for high-bandwidth memory (HBM), high-capacity DDR5, and enterprise SSDs is rapidly increasing. Memory chips are no longer just supporting components in general-purpose computing devices but are gradually becoming one of the key bottlenecks in AI computing infrastructure. Especially in GPU clusters, the bandwidth, capacity, and power consumption of HBM directly impact the performance release of AI chips. Consequently, Micron has been reincorporated into the core supplier base of the AI semiconductor supply chain. This report views Micron Technology as a key representative enterprise in the AI storage supply chain, analyzing its trillion-dollar market cap breakthrough, long-term agreements, HBM growth, valuation restructuring, and related stock trading support on Gate.

Fundamental Analysis and Investment Logic

According to Gate market data, as of June 3, 2026, Micron Technology's stock price was $1,056. Based on approximately 1.1 billion diluted shares outstanding, the company's total market capitalization is approximately $1.17 trillion. Over the past year, Micron Technology (MU) has shown a clear pattern of oscillating upward before ultimately breaking out sharply. The stock price started from around $110, strengthening gradually with expectations for AI storage demand, steadily rising to above $400. After a period of consolidation, it entered a main upward leg driven by the explosion in HBM and AI data center demand, surging continuously from May to June, hitting a high of $1,076, accumulating a gain of approximately over 8 times from the year's low. Over the past year, Micron's stock price rose from about $110 to around $1,056, accumulating gains of over 800%, and the company's market cap simultaneously broke through $1 trillion, reflecting the market's ongoing revaluation of AI storage demand and HBM business prospects.

From a business structure perspective, Micron currently focuses on four main application areas: first, Data Center and Cloud Computing, including AI servers, enterprise servers, and networking equipment; second, Mobile, including smartphones and tablets; third, Storage, including enterprise and client SSDs; and fourth, Embedded, including automotive, industrial, and consumer electronics applications. With continued expansion in AI data center capital expenditure, storage demand related to data centers is becoming Micron's fastest-growing business direction with the highest profit elasticity.

Micron's current trillion-dollar market cap breakthrough is not solely due to a traditional storage cycle rebound, but stems from the market's repricing of its strategic value within the AI infrastructure supply chain. FY2026 Q2 results showed record revenue, gross margin, EPS, and free cash flow, validating the inflection point in profitability driven by AI demand, tight industry supply, and high-end storage product upgrades.

The AI Era: Storage Upgraded from a Supporting Component to a Strategic Asset

In traditional computing architectures, memory chips are often viewed as supporting components alongside CPUs and GPUs, with industry pricing mainly influenced by cyclical supply and demand. However, in the AI era, especially with the continuous scaling of large model training and inference, memory bandwidth, capacity, and energy efficiency have become key bottlenecks for AI system performance release.

In its FY2026 Q2 earnings announcement, Micron explicitly stated that the record Q2 performance reflects the "strategic value of memory in the AI era." Company CEO Sanjay Mehrotra stated that in the AI era, memory has become a strategic asset for customers. This indicates that Micron's management has repositioned the company from a traditional memory supplier to a core participant in AI computing infrastructure.

The rapidly growing demand from AI servers for HBM, high-capacity DRAM, DDR5, and enterprise SSDs significantly increases the value contribution of storage products in the server BOM. As GPU cluster scales expand, customers are not only concerned with chip computing power but also increasingly focus on whether storage supply is stable, performance is matching, and deployment costs are controllable. This shift provides Micron with stronger bargaining power and higher earnings elasticity.

FY2026 Q2 Results Validate Demand Strength

Micron's FY2026 Q2 revenue reached $23.86 billion, a significant increase from $13.64 billion in the previous quarter and notably higher than $8.05 billion in the same period last year. The company's Non-GAAP net profit reached $14.02 billion, Non-GAAP EPS was $12.20, operating cash flow was $11.90 billion, and adjusted free cash flow was $6.90 billion.

More critically, earnings quality also improved simultaneously. FY2026 Q2 Non-GAAP gross margin reached 74.9%, a significant increase from 56.8% in the previous quarter and 37.9% in the same period last year; Non-GAAP operating margin reached 69.0%, expanding substantially from 47.0% in the previous quarter and 24.9% in the same period last year.

This demonstrates that Micron's profitability improvement is not solely driven by revenue growth. The leap in profit margins is a result of concurrent improvements in product pricing, product mix, and cost efficiency. For a memory company, a gross margin rise from the 30-40% range to over 70% signifies a material shift in the industry's supply-demand dynamics and the company's product portfolio.

Data Center and Cloud Business Become Core Growth Drivers

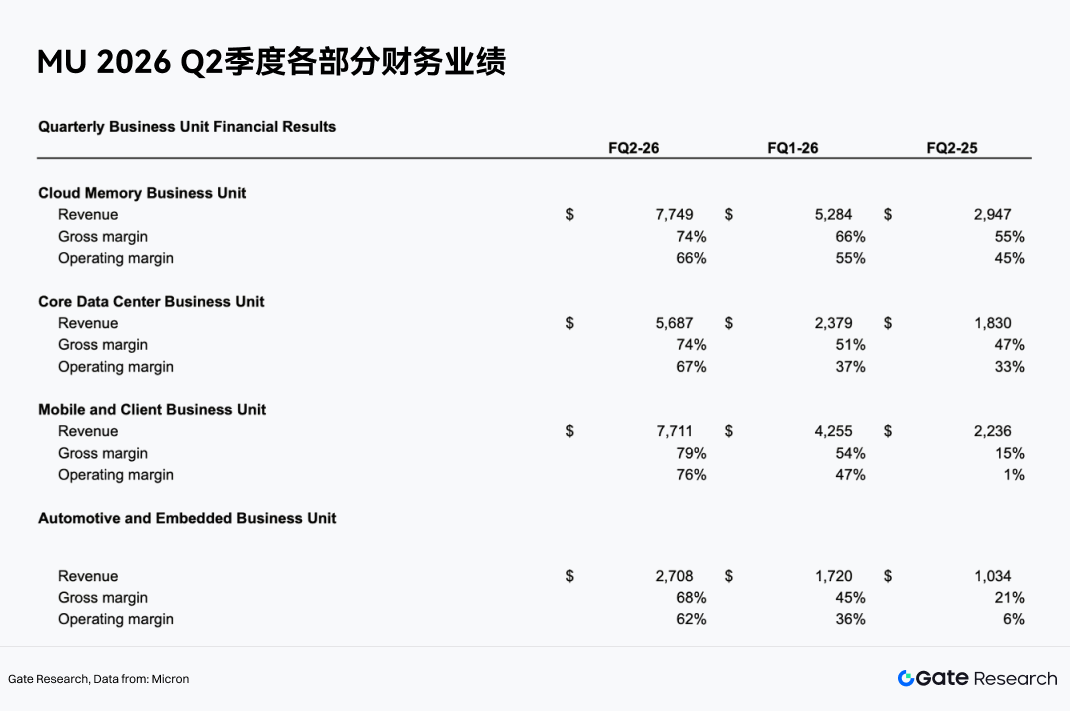

By business segment, Micron's FY2026 Q2 growth is highly concentrated in AI and data center-related areas.

The Cloud Memory Business Unit generated revenue of $7.749 billion, with a gross margin of 74% and an operating margin of 66%. The Core Data Center Business Unit generated revenue of $5.687 billion, with a gross margin of 74% and an operating margin of 67%. Combined, these two businesses generated over $13.4 billion in revenue and have become the company's most important growth engines.

This indicates that Micron's business focus is shifting from traditional consumer electronics cycles like PCs and smartphones to cloud computing, AI servers, and data centers. Compared to consumer electronics, AI data center clients are characterized by large-scale capital expenditure, high product performance requirements, and strong supply continuity needs, making them more likely to foster premium pricing for high-end products and long-term supply relationships.

HBM and High-End DRAM Drive Product Mix Upgrade

The product area where Micron benefits most obviously is HBM and high-end DRAM. HBM is a critical memory product for AI GPUs and accelerators, characterized by high bandwidth, high capacity, and high energy efficiency, with higher price per GB and gross margins than regular DRAM.

UBS expects Micron's HBM ASP to grow approximately 50% year-over-year in 2027, driving continued expansion in HBM revenue. As AI chip platforms iterate, demand for HBM capacity and bandwidth increases. Micron is well-positioned to gain a higher revenue share through HBM3E, subsequent HBM products, and advanced packaging capabilities.

The significance of the product mix upgrade is that Micron is no longer just following industry DRAM average price fluctuations but is gaining stronger pricing power through high-end products. As the HBM share increases, the company's overall gross margin and profitability stability will improve.

Tight Industry Supply Strengthens Price Elasticity

Micron's strong FY2026 Q2 performance also stems from tight industry supply. The results were collectively driven by a robust demand environment, tight industry supply, and the company's execution. Certain institutions predict that DRAM supply shortage will persist at least until Q2 2028, and NAND supply shortage until Q4 2027. In a supply-constrained environment, DRAM and NAND prices have sustained support, allowing Micron's revenue and profit margins to potentially remain at high levels.

More importantly, this cycle differs from the past. Previously, memory manufacturers often rapidly expanded production after price increases, eventually leading to oversupply and price drops. However, the demand growth rate for high-end memory from AI servers is rapid, and HBM capacity expansion is constrained by technology, yield rates, advanced packaging, and customer certification cycles. Therefore, supply release cannot easily catch up with demand quickly.

Long-Term Agreements (LTAs) Enhance Earnings Visibility

LTA, or Long-Term Agreement, refers to a long-term supply agreement. In the semiconductor memory industry, an LTA typically involves the supplier and core customer agreeing in advance on supply arrangements for a future period, including purchase quantities, delivery schedules, product specifications, and in some cases, a pricing framework. In the past, procurement agreements in the storage industry were more inclined towards "locking volume without locking price." Customers would commit to a certain purchase volume in advance, giving the supplier some demand visibility, but prices would still fluctuate rapidly with DRAM and NAND market supply and demand. Therefore, during industry downcycles, significant price drops would still directly impact the revenue and profits of memory manufacturers like Micron, Samsung, and SK Hynix.

LTAs represent another key logic for Micron's valuation revaluation. The new type of LTA not only locks in purchase volume but also partially locks in price, with terms potentially lasting 3-5 years. This differs from past procurement agreements that only locked volume. For Micron, the value of LTAs lies in improving revenue visibility, reducing price volatility, and enhancing cross-cycle profitability. For cloud vendors and AI customers, LTAs can secure future memory supply and partially lock in costs, avoiding being forced to accept higher prices during supply tightness. If LTAs are widely adopted, Micron's business model could gradually transition from a traditional cyclical commodity company to a semiconductor supplier with long-term orders, stable cash flow, and higher customer stickiness.

Earnings and Cash Flow Support Valuation Restructuring

Micron's FY2026 Q2 adjusted free cash flow reached $6.9 billion, and the company's board approved a 30% increase in the quarterly dividend. This indicates that not only has profitability improved significantly, but cash flow quality has also markedly strengthened. In capital markets, stable and substantial free cash flow typically supports a higher valuation. Micron's valuation has been low in the past, mainly due to market concerns over the sustainability of its earnings. Now, if AI demand, LTAs, and HBM product mix upgrades collectively reduce cyclical volatility, Micron is positioned to move from a traditional cyclical memory stock valuation towards a valuation reflecting core AI semiconductor assets.

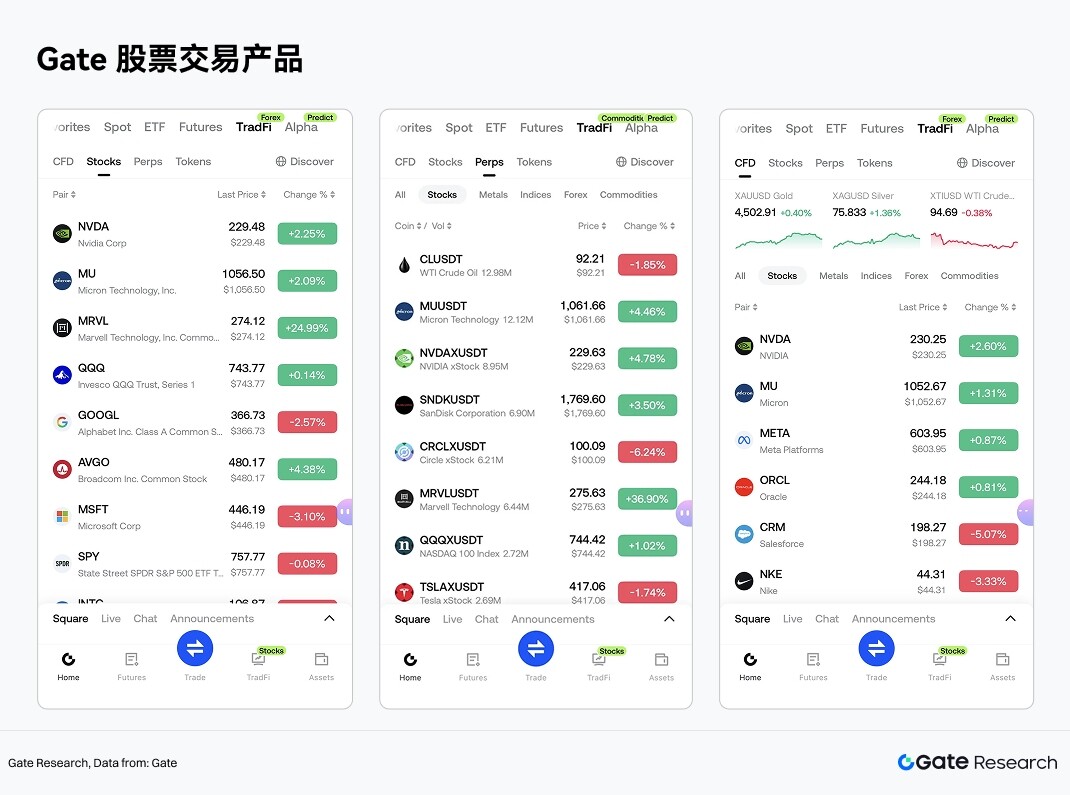

Gate Stock Investment Products

The most closely watched US stock track within the storage sector. Gate has also enabled US stock-related trading services in its TradFi segment. Users can participate in trading stocks and ETFs from major securities markets using USDT through a unified account system.

Unlike common stock tokenization or RWA mapping models in the market, Gate's stock service emphasizes market access capabilities and a compliant trading system. By connecting with compliant brokerages, Gate Stock provides users with stock and ETF trading services. These are not on-chain mapped assets or tokenized stock derivatives. Users can buy, hold, and sell stock assets through their Gate account. Related holdings, profit/loss, fund flows, and corporate action information can be viewed and managed uniformly within the account.

Regarding asset coverage, Gate Stock currently supports over 10,000 stocks and ETF assets, covering major securities trading markets and liquidity networks such as NYSE, Nasdaq, NYSE Arca, NYSE American, and BATS. Currently, Gate Stock supports intraday trading, with plans to gradually expand to 24/7 round-the-clock trading, providing global users with a more flexible entry point for US stock asset allocation.

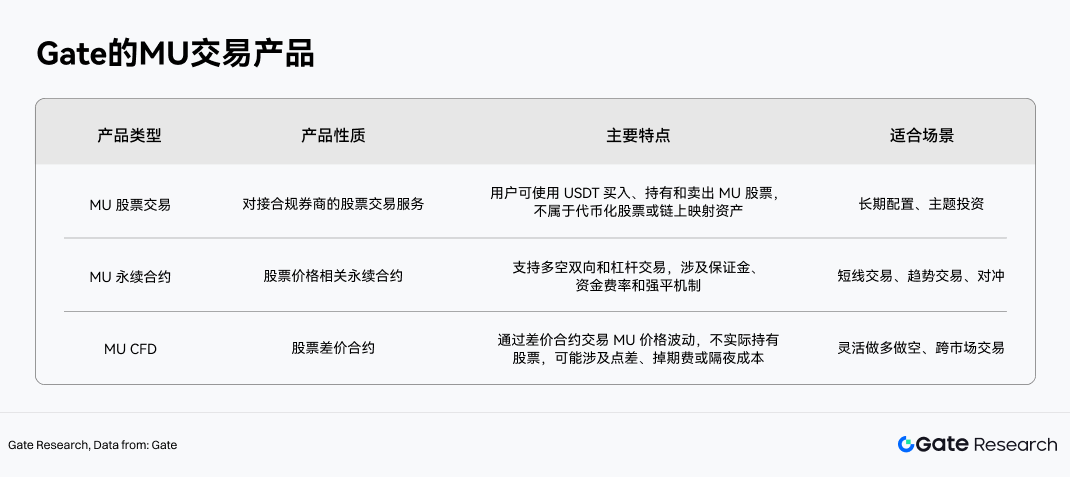

In terms of product structure, stock-related trading tools in Gate TradFi can be categorized into three types, using MU trading products as an example:

Among these, Gate's spot stock trading is independent from the traditional CFD system. Spot stock trading does not involve funding rates typical of perpetual contracts, nor does it incur holding costs like swap fees or overnight fees found in CFD products. Therefore, it is more suitable for users looking to allocate to US stocks for the long term. In contrast, perpetual contracts and CFDs are more geared towards trading instruments, suitable for making directional trades or managing risks related to Micron's short-to-medium-term price fluctuations.

Relying on a unified crypto asset account system, Gate further bridges the gap between digital asset trading and stock investment scenarios. After completing KYC and meeting regional access requirements, users can enter the stock section via the TradFi segment on the Gate App to view quotes, and complete a stablecoin transfer via the trading page or asset page to participate in trading. This means the application scenario for USDT is extending from crypto asset trading to global stock asset allocation.

From an industry trend perspective, Gate's launch of stock trading services provides users with a unified trading entry point for digital assets and traditional financial assets. For users focused on the AI semiconductor theme, the availability of real stocks, perpetual contracts, and CFDs allows them to engage in more flexible asset allocation and trading management around storage, AI, HBM, and semiconductor cycles within a single platform.

Risk Disclosure

From a sector research perspective, future judgments on the storage industry's prosperity and company quality can focus on four key dimensions: First, whether capital expenditure by AI servers and cloud vendors continues to expand; Second, changes in the penetration rate and ASP of high-end categories like HBM, DDR5, and enterprise SSDs; Third, the supply discipline and expansion pace of leading manufacturers like Samsung, SK Hynix, and Micron; Fourth, whether long-term supply agreements, customer certifications, and advanced packaging capabilities continue to strengthen industry barriers.

This means that the storage sector can no longer be fully understood using the past, simplistic "price cyclical stock" framework. For researchers, a more reasonable analytical approach is to view it as a