美股「版本之子」最新調倉:20%押注Anthropic,90億做空輝達,子彈打向電力與記憶體

- 核心觀點:被視為全球最激進 AI 投資人的 Leopold Aschenbrenner,其最新倉位調整並非看空 AI 泡沫破裂,而是強調從「晶片優先」轉向「能源、網路、機房建設優先」的基礎設施輪動信號。他做空 NVIDIA 等熱門晶片股,同時重倉電力、記憶體、資料中心網路及 Anthropic 等更深層資產。

- 關鍵要素:

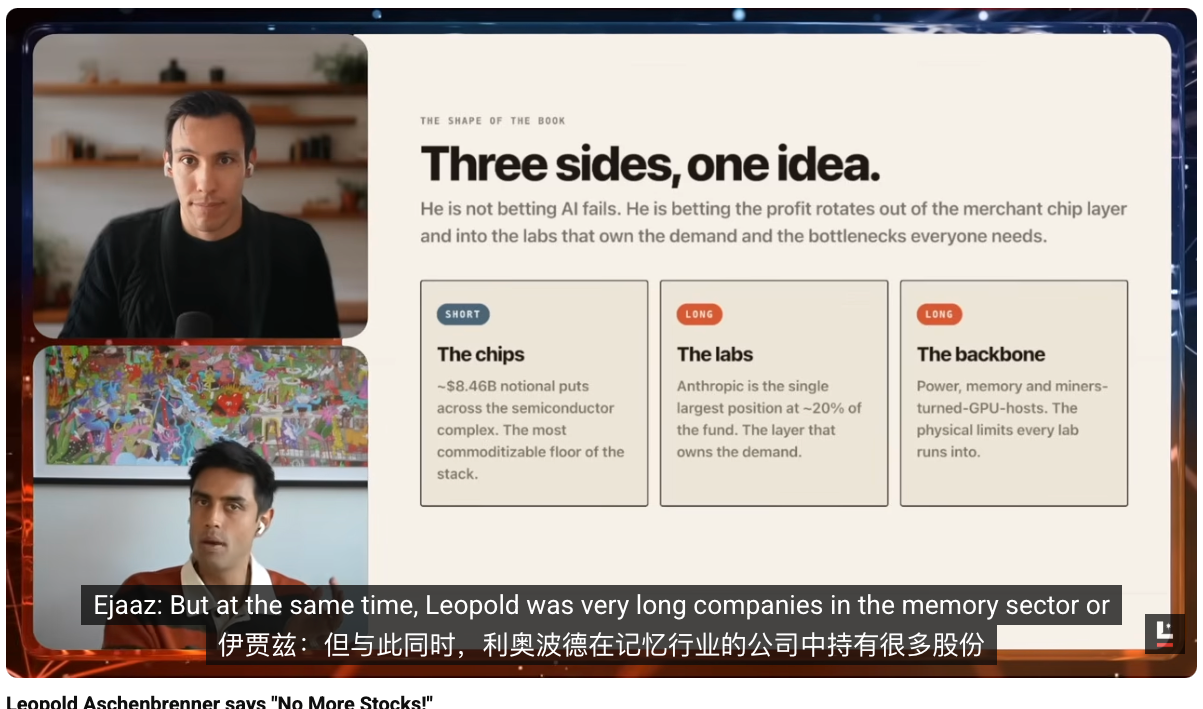

- Leopold 用約 90 億美元名義倉位做空 NVIDIA、ASML 和 Oracle,判斷半導體等「賣鏟子」交易過於擁擠。

- 他將資金轉向電力、記憶體、資料中心網路等下一個基礎設施瓶頸,並重倉 Anthropic(占約 20% 倉位)這類直接「挖礦」的模型資產。

- NVIDIA 完成 250 億美元債券融資,儘管帳上現金充裕且增加回購分紅,但這被視為 AI 賽道融資方式轉變的信號,非缺錢,而是利用廉價資金。

- 真正的瓶頸已從 GPU 轉向電力供應、記憶體產能、資料中心的實體建設能力及審批監管,誰有能力建出資料中心誰就能賺錢。

- 光模組和光纖是資料傳輸的下一階段升級方向,而銅在短距離高頻寬傳輸中仍是關鍵材料,兩者組合需求強勁。

- 能源被視為最穩妥的長期押注,因為無論 AI 需求是否放緩,全球對電力的剛性需求將持續增長。

- Leopold 的基金規模從約 2 億美元起步,一年半內通過公開和私人投資膨脹至約 200 億美元,其策略對市場信號有放大效應。

Organized & Compiled: Shenchao TechFlow

Speakers: Josh Kale, Marketing at AnthropicAI; Ejaaz Ahamadeen, Former Product Manager at Coinbase

Podcast Source: Limitless Podcast

Original Title: Leopold Aschenbrenner says "No More Stocks!"

Broadcast Date: June 17, 2026

Key Takeaways

Leopold Aschenbrenner, considered one of the world's most aggressive AI investors, has taken approximately $9 billion in notional short positions against NVIDIA, ASML, and Oracle in public markets, while simultaneously shifting capital into deeper AI infrastructure and model assets like power, memory, data center networking, and Anthropic. The two hosts believe this doesn't signal the bursting of the AI bubble, but rather a rotation signal within infrastructure trades from "chip-first" to "energy, network, and data center construction-first," a market implication that is rapidly amplifying, especially following NVIDIA's just-completed $25 billion bond financing and Anthropic's valuation increase.

Highlights of Key Insights

Leopold's Core Trading Logic

- "The classic 'picks and shovels' trade in AI has become too crowded, and Leopold's recent position changes are signaling exactly that."

- "His judgment isn't that AI infrastructure has peaked, but that certain layers within the infrastructure stack, particularly semiconductors and traditional hot targets, have become overly crowded."

- "If the question becomes where the capital will rotate next, there are two answers. The first and most direct is it flows to the next real infrastructure bottlenecks: power, memory, and data center networking. The second answer points to the mysterious investment that was only revealed a few weeks ago."

- "His bets have always been very infrastructure-oriented, investing in optical companies and power-related companies alike."

- "If he's cautious on NVIDIA, the capital flows to power and memory; simultaneously, he wants to invest directly in the 'mine' itself, not just keep buying 'shovels.' Anthropic is his most favored mine."

Signals from NVIDIA's Financing

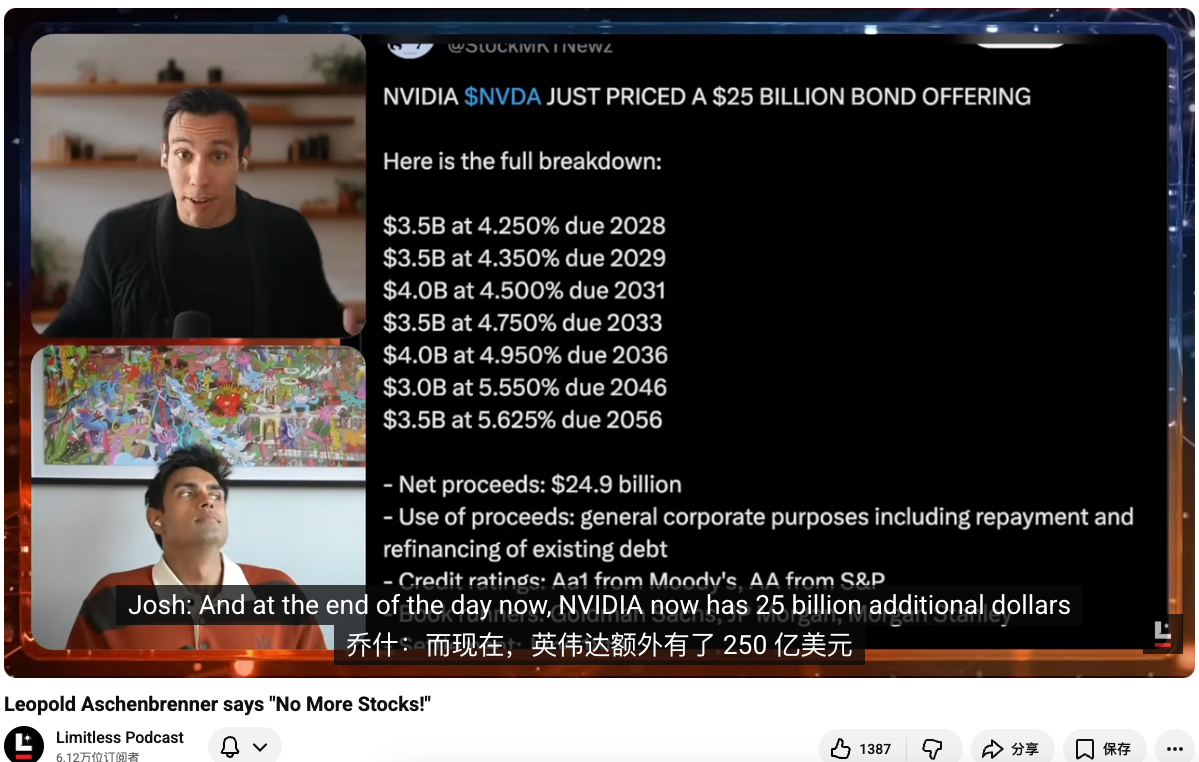

- "The question isn't whether NVIDIA will continue to make money, but why a company with extremely high margins and plenty of cash on hand would borrow an additional $25 billion externally."

- "If a company is aggressively buying back stock and massively increasing dividends in the same month it's borrowing money, it's clearly not borrowing because it's short on cash. A more plausible explanation is that this is cheap capital, and the financing methods for this AI cycle are undergoing a subtle shift."

The Next Wave of AI Infrastructure Dividends

- "The real bottleneck is no longer just GPUs, but power, memory, data center networking, and the capacity to actually build these things."

- "No matter how much money you raise, you can't build data centers fast enough, expand memory chip capacity enough, or immediately scale up the grid, power lines, and related infrastructure. There aren't enough people on the ground, and approvals, regulations, and various procedures are holding you back."

- "Whoever can build the data centers will capture the profits."

Optical Modules, Copper, and Fiber Optics

- "As GPU clusters grow larger, copper wires get hotter, energy loss increases, and efficiency deteriorates. Fiber optics then become the next upgrade path under these conditions."

- "For high-bandwidth, short-distance transmission, copper is almost the only material everyone really wants to use. The switch to fiber optics only happens when copper becomes unsuitable, such as over long distances or when heat generation is too high. So, the market currently has very strong demand for a combination of copper and fiber."

- "Copper futures have been performing strongly recently, essentially because everyone needs it. It's the most critical base material for short-distance, high-bandwidth transmission, and fiber optics is the next step."

- Copper remains the most critical material for short-distance, high-bandwidth transmission, but once distances lengthen or temperatures get too high, switching to fiber is necessary.

- "The next wave of capital will land on infrastructure companies that don't sound very sexy."

Why Energy is the Safest Bet

- "I've always been bullish on energy because even if AI demand slows down, energy itself remains a global necessity, and this demand will only increase."

- "The single trend guaranteed to rise in any scenario is our demand for energy, electricity, and power. These companies are the ones I'm most willing to hold long-term."

- "The entities I most want to follow are those that Jensen is investing in while also aligning with Leopold's logic. So, the ticker I'm currently closest to copy-trading is Marvell."

- "The best long-term positions aren't necessarily the hottest chip companies, but the power infrastructure that is indispensable regardless of the macro scenario."

Leopold's AI Investment Portfolio

Josh Kale:

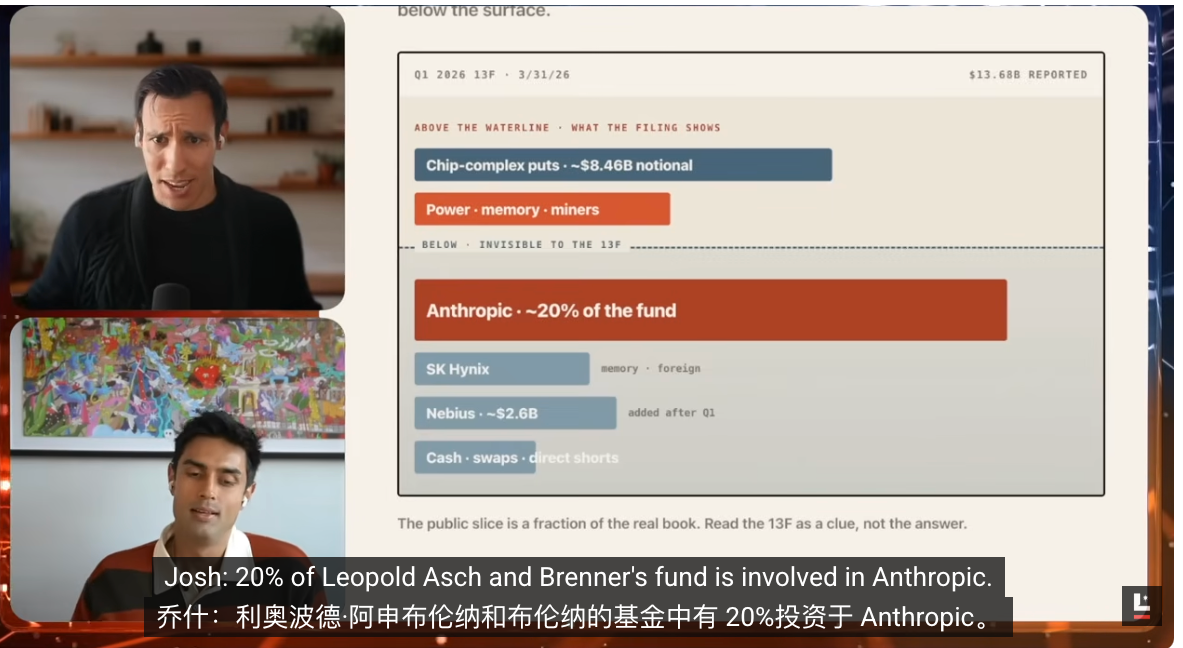

Leopold Aschenbrenner, the 24-year-old solely focused on AI investing, is now almost regarded by the market as the world's most powerful AI investor. Rumors suggest his fund's notional position size exceeds $20 billion. When we saw Ejaaz's post a month ago, the fund size was only $13.7 billion, meaning it's basically doubling every quarter.

This time, we've obtained several significant new changes in his recent investment moves. Last time we discussed his portfolio, the most surprising aspect was that he was shorting a company almost everyone knows, the world's highest market cap and hottest AI stock, NVIDIA. Many couldn't figure out why he would establish a short position of over $9 billion against such a company.

Now we have a new clue that might explain this. NVIDIA is actually raising capital, and through bond issuance. On the surface, this seems unreasonable. Why would a behemoth with massive scale and extremely high profit margins like NVIDIA need to obtain an additional $25 billion in cash just completed? Today, we want to combine it with Leopold's portfolio to discuss why he's making so much money, what he's looking at next, and what NVIDIA's financing really means.

Ejaaz Ahamadeen:

Let me give you some background first. Leopold Aschenbrenner was a researcher at OpenAI. He raised a fund about 18 months to 2 years ago, initially quite small, around $200 million in my recollection. But based on his most recent 13F filing, the fund's public holdings are already worth $13.7 billion.

So naturally, the market is curious about his positions, core investment logic, and where his next big trade will be. To understand this, you need to know that a month ago, Leopold was very optimistic about the entire AI sector, especially the 'picks and shovels' logic, meaning NVIDIA GPUs and upstream hardware suppliers.

But about a month ago, the market discovered he wasn't so bullish on the semiconductor line. He still favored real bottleneck areas like memory and power, and possibly new types of cloud providers, but he specifically turned bearish on the world's most valuable company, NVIDIA. More specifically, he established bearish positions totaling roughly $9 billion in NVIDIA, ASML, Oracle, and several other core beneficiaries of AI infrastructure.

The Logic Behind Shorting NVIDIA

Ejaaz Ahamadeen:

When this news came out, many started to worry if the AI bubble was about to burst. Superficially, NVIDIA's GPUs are still selling like hotcakes, and demand hasn't visibly weakened, so what's the problem?

Then we dug up a few more new clues, the most important being that NVIDIA just raised $25 billion externally through bond financing. This means it's not just using its own cash on hand but is adding leverage. This raises the question: Why would the world's most profitable company with the highest margins and strongest cash flow borrow $25 billion from outside?

Josh Kale:

And they initially planned for only $20 billion but expanded it to $25 billion, with subscriptions exceeding 3 times. Last time we discussed this portfolio, we said not to worry about a bubble yet because, despite massive capital expenditures, these companies' revenues are high enough that they could theoretically support expansion through their own balance sheets.

But this is NVIDIA's first significant off-balance-sheet financing since 2021, instead of using its own cash. I recall it has about $12+ billion in cash on hand now. When you put this all together, there's a strange tension: Leopold is shorting, while NVIDIA seems to have unlimited cash and profits but is still issuing debt. So what's happening?

Dissecting NVIDIA's Bond Financing

Josh Kale: Ejaaz, can you break down the trade itself? Because this isn't ordinary financing; it's a bond issuance. Essentially, NVIDIA now has another $25 billion on its balance sheet, and the interest rate seems very low.

Ejaaz Ahamadeen:

Let me lay out both interpretations. NVIDIA originally had about $13.7 billion in cash, so it could have spent its own money. Why raise external funds? The simplest analogy is buying a house. Many people choose to take a mortgage even if they could pay cash, because they can use their capital for other things, and if borrowing costs are low enough, it's actually more advantageous.

The interest rate environment hasn't been friendly in recent years, but if you're NVIDIA, one of the world's most valuable and sought-after companies, you can borrow on very favorable terms. The terms for this $25 billion bond offering range from 2 to 30 years, representing extremely cheap money, with yields close to US Treasury rates.

Moreover, the offering was oversubscribed, reportedly by about 4 times. In other words, there was $85 billion trying to get into this $25 billion deal. NVIDIA could essentially pick its investors. Officially, NVIDIA's explanation is that this is mainly a financial arrangement to repay and refinance some existing debt. Google did something very similar a few weeks ago and also in February this year. So, you can accept this explanation as financial optimization.

But the other side is hard to ignore: Over the past six weeks, NVIDIA, Amazon, Google, and a few other hyperscale cloud providers have almost all been adding external financing. Some issue bonds, others sell stock. Maybe Leopold's view isn't entirely without merit – could this be a sign of the bubble beginning to wobble, the house of cards starting to shake? However, looking purely at the financial structure, it doesn't yet point to danger.

Josh Kale:

I see it the same way. A $9 billion short on NVIDIA is a very significant position. But during our research, we also saw another thing: On May 18th, NVIDIA's board just authorized an additional $80 billion in buybacks and increased the dividend from $0.01 to $0.25 per share, a 25x increase.

If a company is aggressively buying back stock and massively increasing dividends in the same month it's borrowing money, it's clearly not borrowing because it's short on cash. A more plausible explanation is that this is cheap capital, and the financing methods for this AI cycle are undergoing a subtle shift. Everyone wants to participate in these capital operations. NVIDIA also realized that borrowing via bonds might be cheaper than other financing methods, so it just went ahead and did it. For now, at least, NVIDIA itself is still doing very well.

Why He Rebalanced

Josh Kale: This brings us back to another question. What is Leopold thinking? Why did his judgment change? The stock chart you showed illustrates that NVIDIA's recent performance hasn't been exceptionally strong, but it hasn't been terrible either. It's still near $5 trillion market cap, the world's largest company. A 7% drop in a month is nothing when other AI stocks are surging.

Ejaaz Ahamadeen:

I don't think NVIDIA is going away. I believe its GPUs, including the CPU product line just launched a few weeks ago, will perform very well. AI product demand is currently exponentially oversupplied, and NVIDIA is still the primary supplier of the core machines needed to meet that demand.

But I do feel that the classic 'picks and shovels' trade in AI has become too crowded, and Leopold's recent position changes are signaling exactly that. Looking at his latest 13F, his bearish positions are clearly bearish on the semiconductor line, including NVIDIA, ASML, Oracle, and several other infrastructure-level companies.

But simultaneously, he is heavily invested in areas like memory, power, and new types of cloud. This indicates his judgment isn't that AI infrastructure has peaked, but that certain layers within the infrastructure stack, particularly semiconductors and traditional hot targets, have become overly crowded.

If the question becomes where the capital will rotate next, there are two answers. The first and most direct is it flows to the next real infrastructure bottlenecks: power, memory, and data center networking. The second answer points to the mysterious investment that was only revealed a few weeks ago.

The Unexpectedly Exposed Anthropic Position

Josh Kale:

This surprised me the most. I only learned about it yesterday from you. My first reaction was disbelief. Leopold's fund, 'Situational Awareness', actually has 20% allocated to Anthropic equity? Rumors suggest this company constitutes about one-fifth of Leopold's fund. The Wall Street Journal and several other media outlets have reported this, and sources very close to the deal have confirmed it.

This becomes a completely unexpected card in his portfolio. 13F filings only disclose public market holdings, not private equity. Since Anthropic is a large chunk of non-public equity, this explains why the market estimates his portfolio value at $20 billion.

If 20% of the fund is in Anthropic, and he likely invested in early 2025, the returns in Anthropic over a year feel like seven years. This significantly alters our understanding of his entire investment portfolio.

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()