Missing the wave of the stock and crypto boom, Korean crypto exchanges are forced to trade "shitcoins"

- Core Viewpoint: Due to strict regulations, Korean crypto exchanges cannot list diverse products such as derivatives and tokenized stocks, making their revenue heavily dependent on spot trading fees. Against a backdrop of declining performance, exchanges are forced to list speculative "shitcoins" with names similar to SpaceX's stock ticker to attract trading volume, reflecting how protective regulations can actually exacerbate market risks and the operational difficulties of exchanges.

- Key Elements:

- In Q1 2024, Upbit's revenue fell 54.6% year-on-year to 234.6 billion KRW, while Bithumb's revenue dropped 57.6% to 82.5 billion KRW, resulting in a net loss, marking a collective decline in performance.

- Over 97% of Korean exchanges' revenue comes from spot trading fees, but they are prohibited from offering tokenized stocks, futures, derivatives, and ETFs, resulting in an extremely narrow business scope.

- Overseas exchanges such as Coinbase, Binance, and Bybit have transformed into "everything exchanges," listing products like tokenized stocks. Within 24 hours of SpaceX's tokenized stock listing, trading volume in the crypto market reached $9 billion.

- Korean exchanges cannot participate in the SpaceX listing boom. Their only competitive move is to list attention-grabbing speculative tokens like Spacecoin and SPX6900 at the right time.

- The original intent of regulation was to protect investors, but by depriving exchanges of revenue sources, it makes them more inclined to list high-risk assets when the market shrinks. At the same time, it pushes investors towards overseas platforms like Binance, resulting in regulatory ineffectiveness and revenue leakage.

- South Korean financial institutions are pushing for the integration of securities firms and exchanges by taking stakes in crypto exchanges (e.g., Hanwha Investment & Securities increasing its stake in Dunamu, Mirae Asset acquiring Korbit). However, the possibility of traditional exchanges transforming into "everything exchanges" is extremely low.

原文来自Four Pillars

编译 / Odaily 星球日报 Golem(@web 3_golem)

Editor’s Note: On June 16, South Korean exchange Bithumb listed a memecoin called Spacecoin, followed by Upbit listing an outdated meme coin, SPX6900. The community widely believes that the reason the two major Korean crypto exchanges listed these tokens is that they happen to have tickers similar to SpaceX’s stock code, and the exchanges sought to capitalize on the hype around “memecoins” to attract trading volume.

Against the backdrop of a weakening crypto market and South Korean crypto investors turning to stock trading, the Q1 2026 earnings of Korean exchanges collectively declined, prompting them to urgently take measures to salvage the situation. However, unlike overseas exchanges that can transform into “everything exchanges” by listing a large number of tokenized stocks to meet crypto traders’ demands, South Korea classifies tokenized stocks as securities, thus banning crypto exchanges from engaging in such transactions. It also prohibits Korean crypto exchanges from trading crypto futures, derivatives, or spot exchange-traded funds (ETFs).

South Korea’s regulatory measures aimed at protecting investors have, paradoxically, pushed crypto exchanges towards the most speculative corners of the market. With revenue streams and new product lines such as derivatives, tokenized stocks, and prediction markets all forbidden, exchanges, in order to boost trading volume on their platforms, tend to choose to list attention-grabbing and more speculative “memecoin” tokens.

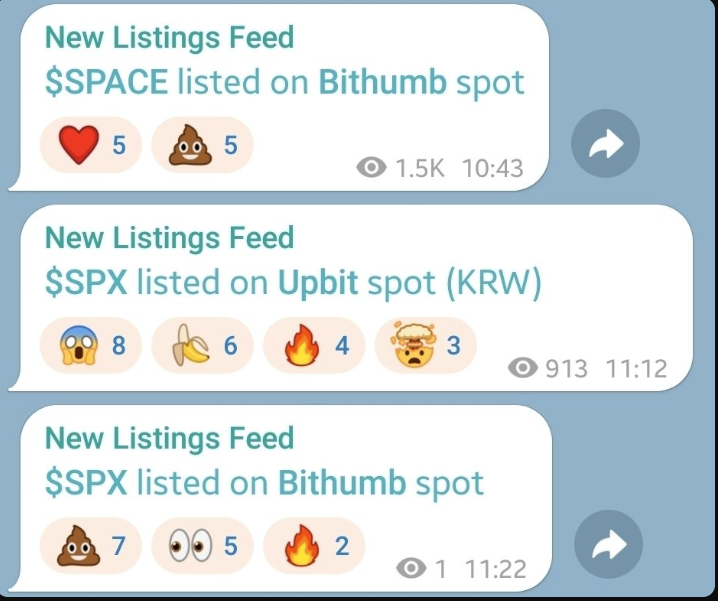

Upbit and Bithumb List “Pseudo-SpaceX Stocks,” Shocking the Korean Community

Bithumb and Upbit listed tokens with tickers similar to SpaceX’s stock code

On the morning of June 16, the hottest topic in the Korean community was Bithumb’s listing of the obscure project token Spacecoin (SPACE) and Upbit’s listing of the meme coin SPX6900. One might ask, isn’t this just an ordinary token listing announcement? What truly stirred the community’s reaction was not the listings themselves, but the token names and the timing.

Four days prior, on June 12, SpaceX went public on the Nasdaq under the ticker SPCX. As is well known, SpaceX’s IPO set historical records, and with stock-related topics now dominating the Korean crypto community, SpaceX became the hottest topic in the field over the weekend.

Therefore, following the listing announcements from Upbit and Bithumb, suspicions began circulating within the community that the names and codes of the tokens listed by these two exchanges were deliberately similar to SPCX, aiming to ride the wave and generate trading volume. Although this connection might merely be a coincidence, this interpretation not only seems plausible but also reflects the current state of Korean exchanges.

Today, overseas platforms like Coinbase, Binance, and Bybit allow users to trade SpaceX and other foreign stocks directly on their exchanges. However, due to regulatory restrictions, Korean exchanges cannot offer such products, so they may have to settle for listing a token that at least shares a name similar to SpaceX.

But this incident shouldn’t just be dismissed as a joke; it vividly illustrates the difficult position Korean crypto exchanges face in competing with their overseas counterparts.

The Current State of Korean Exchanges

Overall Decline in Performance, Even Suffering Losses

The Q1 2026 performances of Korea’s two major exchanges were lackluster.

Upbit Q1 2026 Performance Source: FSS DART

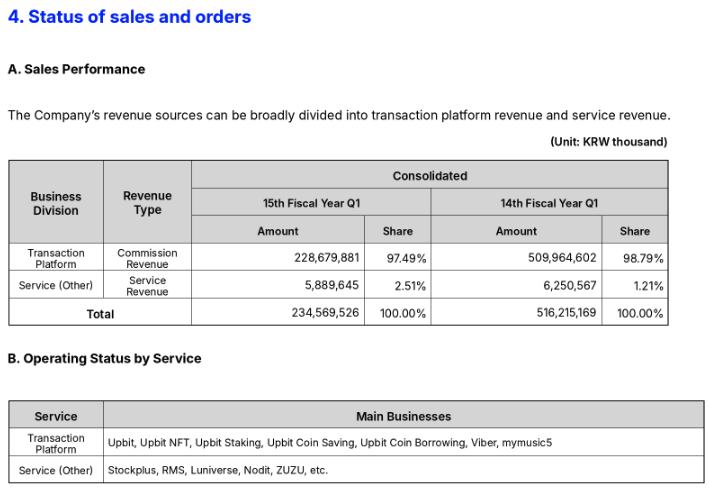

According to quarterly reports filed through the Financial Supervisory Service’s electronic disclosure system on May 15, Dunamu, which operates Upbit, reported consolidated revenue of 234.6 billion KRW, a 54.6% year-on-year decrease. Operating profit fell 77.8% to 88 billion KRW, and net profit dropped 78.3% to 69.5 billion KRW. Upbit’s fee income decreased 55.2% to around 200 billion KRW, while operating costs rose 22% during the same period, squeezing profit margins.

Bithumb Q1 2026 Performance Source: FSS DART

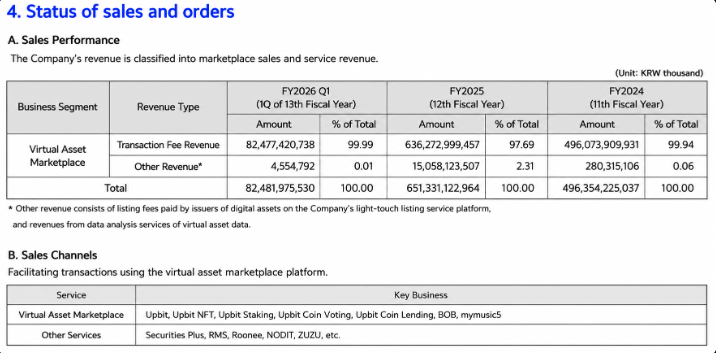

Bithumb’s situation was even more severe. In Q1, its revenue fell 57.6% to 82.5 billion KRW, operating profit plummeted 95.8% to 2.9 billion KRW, and the company recorded a net loss of 86.9 billion KRW, marking its second consecutive quarterly net loss. The direct cause of the loss was a collapse in trading volume, leading to an 87% drop in fee income. Additionally, the Korea Financial Intelligence Unit imposed a 36.9 billion KRW fine and a six-month partial business suspension for violating the Act on Reporting and Use of Specific Financial Transaction Information, factors also reflected in the Q1 results.

The biggest problem for Korean exchanges is that their revenue structure is almost entirely dependent on trading fees. Trading fees account for approximately 97.5% of Dunamu’s revenue and 99.99% of Bithumb’s revenue, making fees essentially their sole income source. However, rather than any negligence in the exchanges’ business operations, this structure is a consequence of the regulatory environment (detailed below) faced by Korean crypto exchanges.

Narrow Business Scope, Limited to Crypto Spot Trading

In reality, the business activities available to Korean crypto exchanges are restricted almost exclusively to crypto spot trading. Other areas are largely off-limits, whether through explicit regulations or tacit avoidance. Below are the businesses that Korean crypto exchanges are prohibited from engaging in:

- Tokenized Stocks: In June 2026, South Korea’s Financial Services Commission and Financial Supervisory Service began classifying tokenized stocks as securities rather than virtual assets. Regardless of the issuance form, securities are governed by the Capital Markets Act; under the Electronic Securities Act, only licensed electronic registration institutions can register electronic rights. If a crypto exchange that is not such an institution issues or circulates security tokens, it constitutes unlicensed business. In other words, tokenized stocks, which are rapidly developing overseas, are structurally disallowed assets for Korean exchanges, and this situation is unlikely to change.

- Futures and Derivatives: Korean crypto exchanges can only offer spot trading and cannot provide products like perpetual futures or options to domestic users. This is less an explicit legal prohibition than the lingering shadow of a past attempt. Coinone, one of Korea’s top five exchanges, operated a contract trading service with leverage up to 4x for about a year starting in December 2016. By the end of 2017, following government regulatory measures and a police investigation, the service was completely shut down. In 2018, police treated the unapproved service as gambling, referring CEO Cha Myung-hoon and others to prosecutors on charges of running a casino, and even arrested 20 users whose trading volume exceeded 3 billion KRW on gambling charges. The case concluded three years later in 2021 without prosecution due to lack of evidence. However, since then, no Korean crypto exchange has engaged in leveraged or futures trading.

- Implicit Avoidance Under Self-Regulation: Korean crypto exchanges are subject to self-regulation by the Digital Asset eXchange Alliance (DAXA), comprising the top five won-based exchanges. Their listing review criteria include opacity due to de-identification, potential for securitization, and possibility of money laundering. These standards effectively exclude privacy coins emphasizing anonymity and cause exchanges to avoid listing tokens that could be considered securities. For similar reasons, assets that might spark securities or gambling controversies, such as exchange tokens or prediction market tokens, are rarely seen on Korean exchanges.

In summary, almost all new areas that overseas exchanges are expanding into, such as crypto derivatives, tokenized stocks, privacy coins, and prediction markets, are restricted for Korean exchanges.

Korean Exchanges Have Fallen Behind in the Global Competition

Have Korean Exchanges Lowered Their Listing Standards?

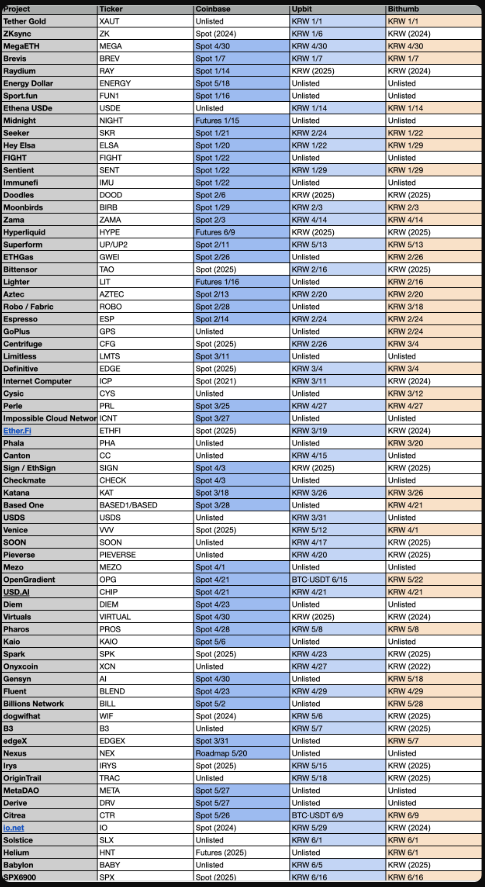

Recently, the community has accused Upbit and Bithumb of relaxing their listing review standards. The table below provides a comprehensive comparison of tokens listed by Coinbase, Upbit, and Bithumb in 2026:

Tokens listed by Coinbase, Upbit, and Bithumb in 2026 Source: Four Pillars (@c4lvin)

In terms of the number of tokens listed, Coinbase leads. Coinbase has listed many assets not available on the two Korean exchanges, and a significant portion of them are available for both spot and contract trading, offering trading opportunities earlier than other platforms. Just considering frequency and timing, Coinbase appears to be more aggressive.

In 2026, a considerable number of the new won-denominated tokens listed by Upbit had previously been listed on Bithumb, such as Bittensor (TAO), Internet Computer (ICP), Ether.fi (ETHFI), io.net, dogwifhat, Spark (SPK), and Babylon. Most of these tokens did not have substantial trading volume on Bithumb. They were not newly issued assets but tokens that had already been on the market for some time, only being added to Upbit’s platform later. This perhaps makes Upbit’s listings seem less fresh.

The perceived decline in token quality is not due to a lowering of the standards themselves, but rather the diminishing effect of listing on trading volume. In an environment where the trading volume generated by a single token listing quickly dries up and new assets worth listing are increasingly scarce, Upbit maintains its listing pace by adding tokens previously listed on Bithumb.

Ultimately, Korean users’ complaints are less about specific names and more about the perceived gap in convenience they feel compared to other markets, which offer newer products like tokenized stocks.

Korean Exchanges Excluded from the SpaceX Listing Feast

Meanwhile, major overseas exchanges are heading in the opposite direction. They are striving to break free from the limitations of virtual assets, aiming to become what is known as an “everything exchange” – a single application where all types of assets can be traded.

The most prominent example is Coinbase. In its Q4 2025 shareholder letter, Coinbase stated that besides cryptocurrencies and derivatives, it had begun trading stocks and ETFs within its application, opening access to around 3,000 assets for early users, with the goal of integrating traditional and digital assets into a unified portfolio experience. The letter also highlighted that Coinbase had become the first company in the industry to launch 24-hour US perpetual contract products, boosting its market share in derivatives.

Binance’s approach was more direct. From June 1, 2026, Binance opened US stock trading to eligible users, allowing them to trade over 7,000 US-listed stocks and ETFs directly. Additionally, Binance launched bStocks, which tokenize US stocks on a one-to-one basis, settle in stablecoins, can be withdrawn to users’ self-custody wallets, and support 24/7 trading.

Bybit joined the xStocks alliance and listed tokenized stocks created by a regulated Swiss issuer. These price-tracking tokens are backed by real stocks and are tradable 24/7 using stablecoins.

In short, overseas crypto trading platforms have made tokenized stocks a key promotional focus. The difference in the trading environment between Korea and abroad was most starkly illustrated during the SpaceX listing. For overseas exchanges, this listing served as a test of their tokenized stock capabilities, leading to the launch of pre-IPO contract products and tokenized stocks.

Within 24 hours of the launch of SpaceX-related products, the entire crypto market saw a trading volume of approximately $9 billion, with Binance alone accounting for $5.6 billion.

In contrast, Korean crypto exchanges were excluded from this feast. Whether tokenized stocks, perpetual contracts, or any product tracking SpaceX are not permitted for trading within Korea. While major exchanges worldwide engaged in multi-billion dollar trading around the same hot topic, Korean crypto exchanges had no channels to participate.

Korean Exchanges Are Suffocating Under Regulatory Pressure

For an exchange that cannot compete with the rest of the world in product variety, the only remaining battleground is the crypto market itself. With revenue dependent on spot trading fees, and unable to list derivatives or stocks, the sole way to increase trading volume is to list tokens that can capture investor attention at the right time.

South Korea’s strict regulation of crypto exchanges is intended to protect investors. It treats leveraged trading as gambling and prohibits it; it filters out security-type tokens with opaque rights structures; and it excludes assets easily used for money laundering or price manipulation from listing reviews.

However, as this protective mechanism gradually strips away exchanges’ revenue sources and product lines, listing crypto spots becomes their only remaining tool. And the more trading volume in the crypto market shrinks, the more Korean exchanges tend to list assets that command higher attention and are therefore more speculative. Protection at the product stage ultimately encourages the influx of speculative assets at the listing stage. The recent listing of tokens with tickers similar to SpaceX’s by the two major exchanges is a microcosm of this trend.

A deeper problem is that even this protective mechanism is not entirely effective. Korean investors wanting to buy perpetual contracts or tokenized stocks do not easily abandon their demand; they simply turn to overseas platforms like Binance, Bybit, and Hyperliquid.

In other words, Korean regulation itself does not eliminate investors’ high-risk trading appetite; it merely pushes high-risk trading to markets outside the reach of Korean authorities. When tax and cross-border information exchange (CARF) fully take effect in 2027, the scale of this offshore trading will become evident from the data. Ultimately, investors bear the speculative risk anyway while losing domestic regulatory safeguards, and Korean exchanges lose the revenue these trades would have generated.

This structure also makes Korean exchanges vulnerable. With a single product line, almost all revenue coming from trading fees, they are fully exposed to the cyclical fluctuations of trading volume. Coinbase diversifies its revenue across custody, stablecoins, tokenized stocks, and derivatives to buffer against market downturns, while Korean exchanges must weather the same cycles relying on a single product. As this gap accumulates quarter after quarter, it eventually translates into differences in investment capability and product competitiveness, which then manifest again, much like the disparity in convenience felt by domestic users.

Of course, the Korean government is also pushing forward with cryptocurrency regulation. A series of initiatives, including the second phase of the Digital Asset Basic Act, the institutionalization of Security Token Offerings (STOs), approval for corporate trading, and the issuance of won stablecoins and spot ETFs, are all scheduled to launch in 2026, demonstrating the government’s commitment. However, even if these new regulations are eventually implemented, they might not be operated by existing crypto exchanges but rather entrusted to licensed entities like securities companies and electronic registration institutions.

Therefore, the ongoing convergence is not about crypto exchanges transforming into securities companies, but rather securities companies and banks acquiring stakes in crypto exchanges and incorporating them into their systems. In 2026, Hanwha Investment & Securities increased its stake in Dunamu to 9.84%, becoming the third-largest shareholder; Hana Financial Group holds a 6.55% stake; and Samsung Securities, Samsung Card, and Samsung SDS hold a combined 4%. Korbit was acquired by the Mirae Asset Group; Korea Investment & Securities signed a strategic equity investment agreement to acquire a 20% stake in Coinone, becoming its third-largest shareholder. As financial regulators adopt a cautious stance on the separation of finance and crypto and tend to relax related restrictions, such alliances are rapidly increasing.

Will South Korea allow crypto exchanges to develop into “everything exchanges” like those abroad? This is highly unlikely.

But this article is not an argument for immediately abolishing regulations. Instead, it suggests that a protective framework designed for a certain era is now creating more hidden costs as the market rapidly trends towards asset convergence. Korean crypto exchanges operating under such a stringent environment will pass these costs on to users in a bear market like the current one, ultimately leading to the resurgence of “memecoins” with fleeting trading demand, as seen today, creating more victims.