Anthropic 衝擊 1 兆:除了 Pre-IPO,還有哪些隱藏的「Claude 概念股」?

- 核心觀點:Anthropic 估值飆升至近一兆美元,成為首家衝擊這一級別的 AI 新創公司,其企業級應用路徑帶動了股權、算力和企業軟體三大類「Claude 概念股」的價值重估,為公開市場提供了間接的投資機會。

- 關鍵要素:

- Anthropic 估值從 2025 年 3 月的 615 億美元暴漲至 2026 年的近一兆美元,預計 2026 年 Q2 收入達 109 億美元,並有望實現盈利,企業級程式碼和 Agent 應用是其核心敘事。

- Zoom 是公開市場中估值彈性最大的「影子股」,因其 5100 萬美元早期投資,按當前估值可能帶來 20-40 億美元帳面收益,占其市值的 7%-15%以上。

- 算力生態受益者包括雲端廠商(AWS、Google Cloud)、AI ASIC 供應鏈(Broadcom)以及 Neo-cloud(CoreWeave),其中 Broadcom 因 Google TPU 合作與 Claude 增長直接關聯。

- 企業軟體平台如 Salesforce、SAP、Snowflake 和 ServiceNow 將 Claude 嵌入產品作為原生智慧引擎,代表更具可持續性的分發收益。

- Anthropic 股權價值相對於自身市值的不對稱性是「影子股」核心邏輯,Zoom 和 SK Telecom 等中小市值公司比 Amazon 等巨頭更具估值彈性。

The first trillion-dollar AI startup is about to be born.

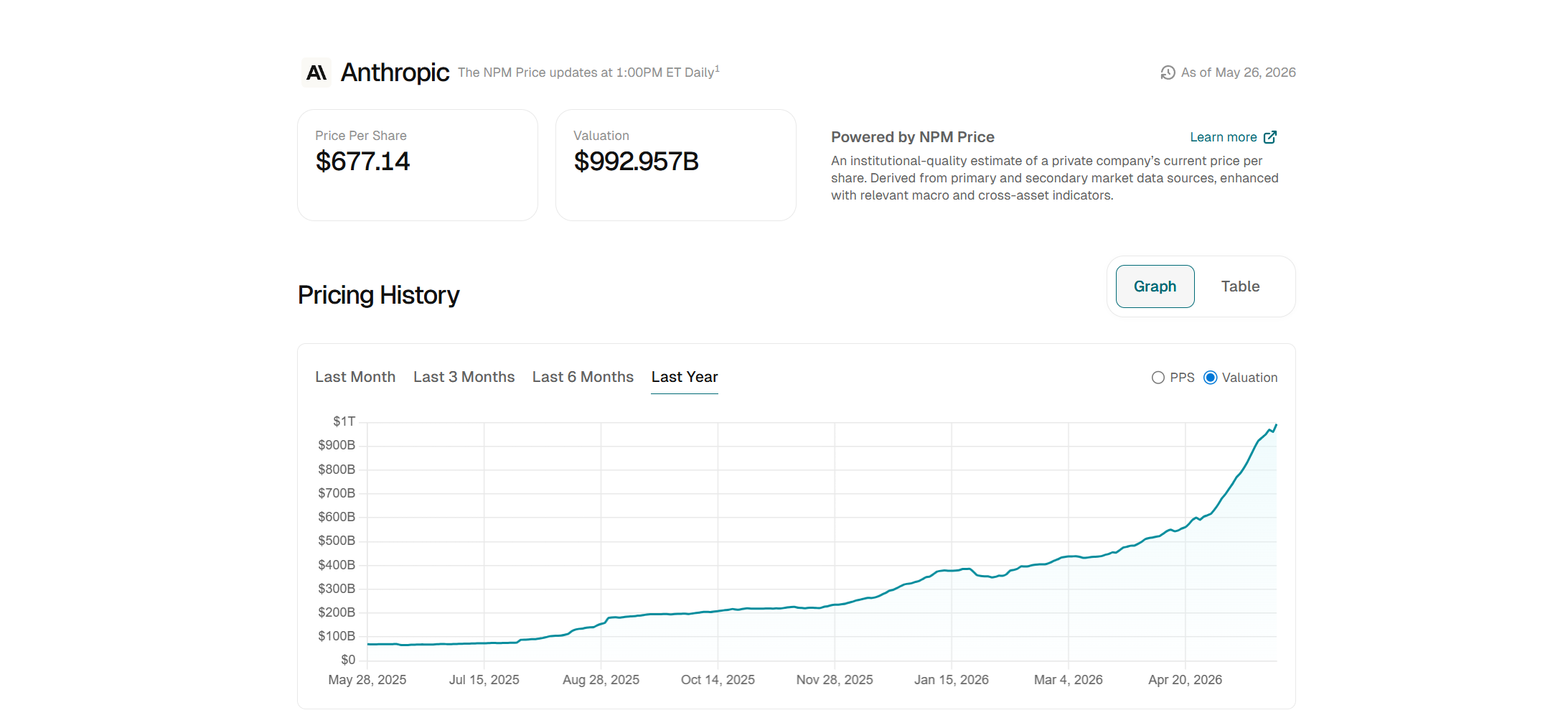

As of press time, according to Nasdaq Private Market (NPM) data, Anthropic's valuation has surged from $650 billion in early May to approximately $992 billion, just a stone's throw away from the trillion-dollar mark.

Of course, it needs to be clarified first that the NPM valuation is not the same as Anthropic's latest official funding round valuation, nor is it simply a pending order price on a certain platform. It synthesizes multiple data points, including secondary market transactions, bid and ask prices, and the previous funding round, to provide an estimate closer to the fair value in the current private market.

In other words, Anthropic has not yet officially confirmed a "trillion-dollar valuation" through an official funding announcement, but the private market has already started pricing it within the range of trillion-dollar assets.

This also brings up a more practical issue. Besides Pre-IPO channels like MSX, it is difficult for ordinary investors to buy Anthropic directly. Are there other ways in the public market to capture the spillover opportunities from the rising valuation of Claude?

The answer may not only lie in traditional "AI stocks."

1. Why is Anthropic the first to break the trillion-dollar mark?

Undoubtedly, Anthropic's valuation surge has become one of the most explosive stories in the global capital markets in 2026.

Looking at the numbers alone, it's a very steep curve:

- In March 2025, Anthropic completed a $3.5 billion funding round at a post-money valuation of $61.5 billion;

- By September 2025, the valuation had risen to $183 billion;

- In February 2026, it completed another $30 billion funding round, reaching a valuation of $380 billion;

- According to recent media reports, it is now conducting a new funding round at over $900 billion, surpassing OpenAI's valuation of approximately $852 billion;

Coupled with the nearly trillion-dollar pricing signal from private market data like NPM, on the surface, this is the capital market paying for AI once again. Deeper down, the change lies in the capital market beginning to redefine the ceiling for frontier model companies.

This is not entirely the same as the early ChatGPT-style consumer explosion. OpenAI's strengths lie in consumer-grade entry points, developer ecosystems, and brand mindshare, while Anthropic's advantages are increasingly concentrated in enterprise scenarios, especially code, Agent automation, and high-security industry applications. For the capital market, this means Claude is not just a chatbot but has become a foundational infrastructure that can be embedded into the daily production processes of enterprises.

This shift is directly reflected in revenue and profit expectations. According to recent media reports, Anthropic expects revenue of $10.9 billion in the second quarter of 2026, a significant increase from $4.8 billion in the first quarter, and aims for an operating profit of $559 million in the quarter. If this performance materializes, Anthropic will become one of the few frontier AI companies that approaches profitability despite high computing power investments.

This is also a core difference in its current narrative compared to OpenAI.

Of course, Anthropic is not charging forward alone in a market without competition. Recently, OpenAI has been continuously repairing its product performance and reputation in scenarios like Coding and Agentic Workflow through Codex+5.5. While models like Gemini have seen a dip in reputation, they haven't withdrawn from the model arms race either.

In other words, Anthropic's high valuation is not a result of "the game is over," but rather the market is temporarily willing to pay a higher premium for its enterprise growth curve, the performance of products like Claude Code, and its clearer commercialization path.

It is precisely because of this scarcity that Anthropic has become one of the most watched targets in the Pre-IPO market.

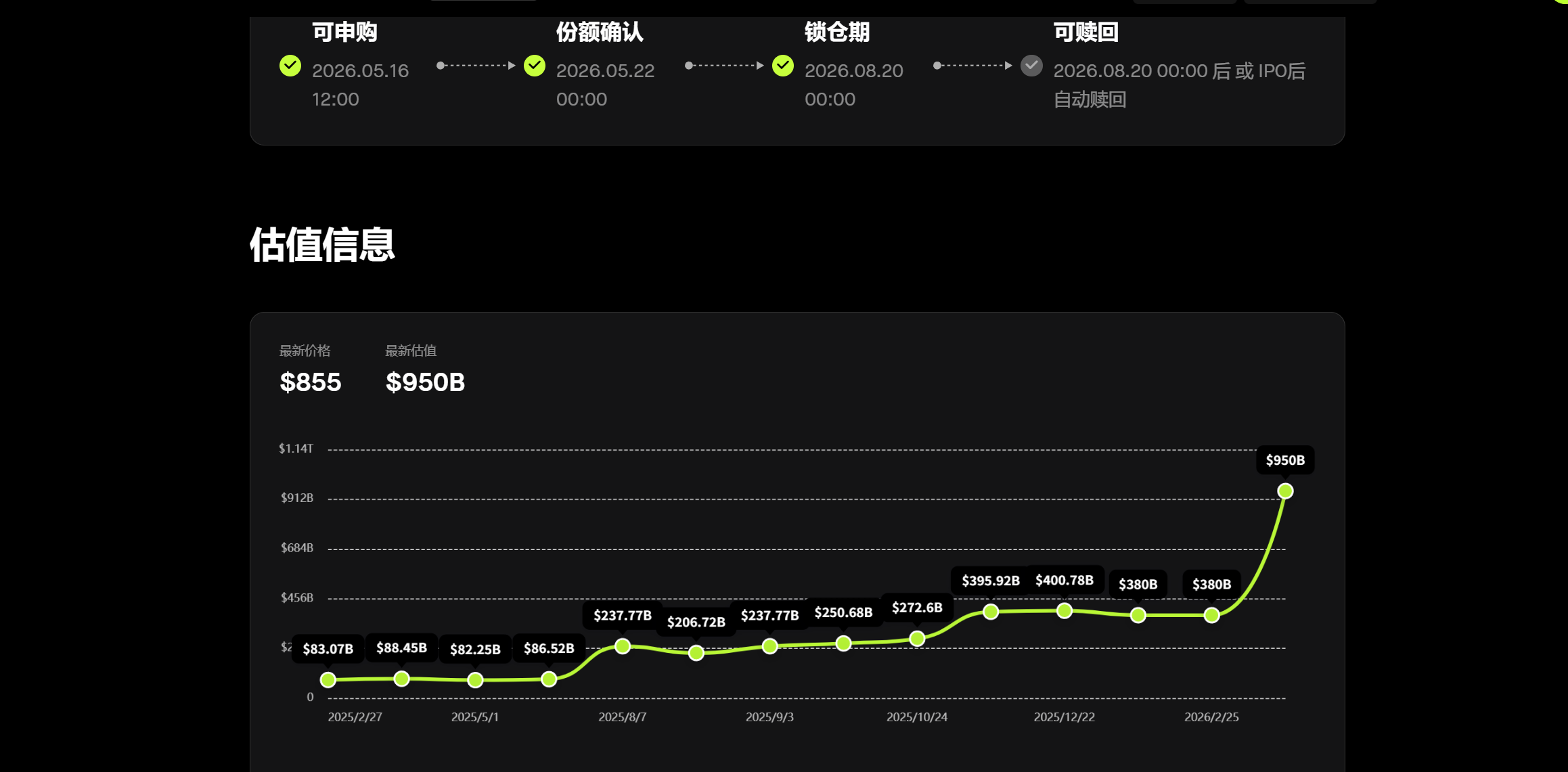

The recently concluded second phase of the MSX Maitong Pre-IPO included Anthropic as one of its two targets, with a subscription price of 855U, corresponding to a valuation of approximately $950 billion. For many ordinary investors, this type of Pre-IPO product indeed provides an entry point closer to private market pricing when Anthropic is not yet listed and the primary market threshold is extremely high.

But Pre-IPO is not the only angle of observation.

When Anthropic's valuation approaches a trillion dollars, the market may need to reprice not just Anthropic itself, but an entire shadow chain surrounding Claude: who invested in it, who supplies its computing power, who brings it into enterprise software, and these entities could potentially be revalued by capital.

So, besides Pre-IPO, which companies stand on the chains of Claude's equity, computing power, and enterprise distribution?

2. If You Can't Buy Anthropic, What Will the Market Buy?

If categorized by "how close they are to Anthropic," Claude concept stocks can be roughly divided into three types: First are equity shadow stocks that directly participated in Anthropic's investments. Second are cloud and chip companies that meet Claude's computing power demands. Third are software platforms that integrate Claude into enterprise workflows.

These three types of companies are all called "Claude concept stocks," but their benefit mechanisms are entirely different:

- Equity shadow stocks rely on the book value revaluation from Anthropic's rising valuation;

- The computing power chain relies on orders from the expansion of Claude's training and inference demands;

- Enterprise software platforms rely on whether Claude can become a native capability within their own products;

1. First Tier: "Shadow Stocks" with Direct Investments Accessible in the Public Market

Public information shows that Anthropic has undergone 7 funding rounds from Series A to G since its inception. Major shareholders include Google, Amazon, Nvidia, Microsoft, Sequoia, Blackstone, and GIC. After the Series G round (post-money valuation ~$380 billion), the shareholding ratios of major investors are: Amazon (9%), GIC (8%), Microsoft (7%), Coatue Management (6%), Google (6%), Nvidia (5%). Founders and team hold 21%, and the employee option pool holds 19%.

However, the most prominent "hidden shadow stock" is not tech giants like Amazon, Google, or Microsoft, which invested billions, but Zoom.

Zoom announced a strategic partnership with Anthropic back in 2023 and invested approximately $51 million through Zoom Ventures (when Anthropic's valuation was only $4.1 billion). The collaboration was to integrate Claude into the Zoom platform, gradually covering various product lines like Team Chat and Meetings.

The interesting part is that although Zoom's investment amount was small back then, even considering subsequent funding dilution, the value of this stake has reached the $2-4 billion range or higher. Compared to Zoom's current market cap of about $29 billion, this single investment accounts for 7% to 15% or even more of its market cap.

For giants like Amazon and Google, such an investment might just be a non-core item on their financial statements. But for Zoom, the meaning is entirely different—Zoom's current market cap is around the $30 billion level. If the valuation of its Anthropic holdings reaches tens of billions of dollars, it becomes a significant variable sufficient to influence the market's understanding of its asset value.

This is what makes Zoom so special – a small temple housing a big Buddha.

Over the past few years, Zoom's core video conferencing business growth has gradually slowed, and its market imagination has significantly diminished compared to the pandemic era. However, if you combine the Anthropic equity, Claude integration, and the AI transformation of enterprise-level customer service centers and collaboration scenarios, Zoom is no longer just a video conferencing company with slowing growth. It is a super shadow stock in the public market that unexpectedly holds an early ticket to Claude.

A similar equity shadow logic can be extended to SK Telecom.

SK Telecom announced an additional $100 million investment in Anthropic in 2023, partnering to develop multilingual large language models for the telecommunications industry. Compared to Zoom, SK Telecom's peculiarity is that it is a traditional telecom operator with a relatively small market cap, so the book value of its Anthropic stake could have a more pronounced impact on its overall valuation.

For this reason, overseas markets have also once viewed SK Telecom as a stranger but more direct Anthropic shadow asset.

2. Second Tier: Computing Power Ecosystem, from Cloud Vendors and AI ASICs to Neo-cloud

However, beyond Zoom and SK Telecom, a larger Claude industry chain lies hidden in the computing power layer.

If equity shadow stocks focus on the book revaluation from Anthropic's valuation rise, then computing power ecosystem stocks address another question: the larger Claude gets, the more enterprises invoke it, and the heavier the code and Agent scenarios become – who will handle the backend training, inference, and data center demands?

This chain cannot only look at NVIDIA, nor only at traditional cloud vendors. More accurately, Claude's computing power ecosystem can be broken down into at least three groups:

- The first group is cloud platforms like AWS, Google Cloud, and Azure;

- The second group is AI ASICs like TPU and Trainium, and their supply chains;

- The third group is Neo-clouds like CoreWeave, Nebius, Lambda, and Crusoe, which specialize in providing AI computing power for rent;

For example, Anthropic's binding with Amazon is the earliest and deepest. Amazon has invested billions of dollars in Anthropic, and AWS is one of Anthropic's most important cloud and training partners. They collaborate deeply on AWS Trainium, the Neuron software stack, Project Rainier, etc. For Amazon, Anthropic is not just a financial investment project but also a crucial lever for AWS to compete for cloud workloads in the generative AI era.

Google represents another route. Google invested early in Anthropic and has continuously expanded its cloud and TPU cooperation. In 2026, Anthropic, Google, and Broadcom expanded their collaboration, planning to obtain multi-GW level next-generation TPU computing power starting from 2027 to support Claude model and enterprise application expansion.

Objectively speaking, Anthropic uses both AWS Trainium and Google TPU, and also accesses the NVIDIA architecture through Microsoft Azure. This diversified computing power strategy, on one hand, reduces dependence on a single supplier, and on the other hand, allows more public market companies to become indirect beneficiaries of Claude's growth.

This also leads to a direction easily overlooked in the past: the AI ASIC chain.

In the past, when discussing AI computing power, the market most easily thought of NVIDIA GPUs first. However, as frontier model companies increasingly focus on inference costs, supply stability, and cost per unit token, the importance of cloud vendors' self-developed chips and custom ASICs is rising. Essentially, chips like AWS Trainium and Google TPU aim to provide a more controllable cost structure for large model training and inference outside of GPUs.

In this line, Broadcom is one of the companies most worth discussing within the Claude concept stock category. It is not a public equity investor in Anthropic, but it is one of the key chip and network suppliers behind the Google TPU ecosystem. If Anthropic's future growth indeed relies on larger-scale TPU deployment, then Broadcom becomes an unavoidable hardware and network node in this chain.

Extending further, Marvell, TSMC, advanced packaging, optical interconnects, and high-speed network chains can also be observed within the broader AI ASIC industry chain: Broadcom's connection to Claude is more direct because it stands at the intersection of the expanded cooperation between Google TPU and Anthropic. Other ASIC and semiconductor supply chain companies are more likely to experience industry beta from the expansion of AI computing power demand, not necessarily exclusive beneficiaries of Claude.

Microsoft and NVIDIA entered a clearer cooperative framework by the end of 2025. NVIDIA and Microsoft respectively committed to investing up to $10 billion and $5 billion in Anthropic. This is very interesting, meaning Microsoft is buying an "insurance policy outside of OpenAI" for its own AI ecosystem. NVIDIA's logic is more straightforward: regardless of whether Anthropic uses Trainium, TPU, or NVIDIA GPUs, as long as the frontier model competition continues to escalate, NVIDIA remains one of the hardest computing power cores to bypass.

However, on the Claude line, NVIDIA is not the only winner, because Anthropic emphasizes diversification of computing power sources more than many model companies.

Besides traditional cloud vendors and AI ASICs, there is a newer group of computing power beneficiaries: Neo-clouds. Simply put, these are new types of cloud vendors specializing in providing high-density GPU/accelerated chip computing power rental for AI training and inference. Unlike AWS, Azure, or Google Cloud, which offer a wide range of cloud services, they focus more on AI workloads, localized high-performance clusters, GPU-as-a-Service, and the elastic computing power needed by model companies.

In this line, CoreWeave has the most direct relationship with Anthropic. In April 2026, CoreWeave announced a multi-year agreement with Anthropic, where Anthropic will use CoreWeave's cloud platform to run production workloads.

This also means that Claude's computing power ecosystem is not a binary choice of "cloud vendor vs. chip company," but a multi-layered structure: the bottom layer has different chip routes like NVIDIA GPU, Google TPU, AWS Trainium; the middle layer has traditional cloud platforms like AWS, Google Cloud, Azure; simultaneously, there are Neo-clouds like CoreWeave, Nebius, Lambda, and Crusoe serving as more flexible computing power leasing and delivery layers.

Therefore, to understand the Claude computing power ecosystem more comprehensively, Broadcom represents the AI ASIC and custom chip chain, CoreWeave represents the Neo-cloud computing power leasing chain, and Amazon, Google, and Microsoft represent the computing power entry points of traditional cloud platforms.

These three groups of companies collectively illustrate one thing: The higher Anthropic's valuation, the more the market reprices not just Claude itself, but also the increasingly complex network of computing power procurement, chip design, and cloud infrastructure behind it.

3. Third Tier: Software Platforms Integrating Claude into Enterprise Workflows

Beyond equity and computing power, there is a third category of companies that are easier to overlook: enterprise software platforms.

The most typical examples here are Salesforce, SAP, Snowflake, and ServiceNow.

Salesforce Ventures participated in Anthropic's early funding rounds and has continued to support subsequent rounds. More importantly, Claude has already entered Salesforce's product systems like Slack and Agentforce. Particularly in industries with higher security and compliance requirements, such as finance, healthcare, and the public sector, Claude has the potential to become one of the key models in Salesforce's enterprise AI solutions.

SAP's logic leans more towards core enterprise systems. In 2023, SAP announced strategic investments in generative AI companies including Anthropic, Cohere, and Aleph Alpha. In 2026, SAP announced an expanded partnership with Anthropic, planning to make Claude one of the primary reasoning and Agent capabilities within the SAP Business AI Platform, Joule, and Joule agents ecosystem.

This line is very significant because SAP connects to the most core enterprise systems: ERP, finance, HR, supply chain, and operations management. If Claude can enter SAP, it is not just entering a software entry point; it's entering the underlying business processes and data structures of global enterprises.

Snowflake and ServiceNow represent another type of enterprise AI distribution path.

Snowflake expanded its partnership with Anthropic, committing $200 million to jointly promote the Claude model into Snowflake Cortex AI, Snowflake Intelligence, and enterprise data analysis Agent scenarios. ServiceNow announced Claude as the default model for the ServiceNow Build Agent, used for application development, industry workflows, and internal employee efficiency improvement. ServiceNow also stated that it has deployed Claude for tens of thousands of employees.

These companies are not direct beneficiaries of Anthropic's valuation increase, but they represent another, more important direction: Claude is transforming from a standalone AI product into an inference engine and workflow engine within enterprise software.

For the public market, this might be a more sustainable thread. Equity shadow stocks have a ceiling on their book value flexibility, and computing power orders can be easily affected by CapEx cycles. However, if Claude truly becomes the default intelligence layer in enterprise software, companies like Salesforce, SAP, Snowflake, and ServiceNow also have the opportunity to alleviate market concerns about "AI disrupting SaaS."

Simply put, Anthropic's rise doesn't necessarily only signify a threat to traditional software companies; it could also mean that a batch of enterprise software companies have gained an opportunity to repackage their own valuation logic.

Furthermore, extending enterprise workflows further into government, intelligence, and defense scenarios, Palantir is also worth mentioning separately. It is becoming an important distribution platform for Claude to enter high-security-level scenarios within the US government: In 2024, Palantir, Anthropic, and AWS announced a partnership to integrate the Claude 3 and Claude 3.5 series models into Palantir AIP, serving US intelligence and defense agencies. Subsequently, Anthropic joined the Palantir FedStart program, promoting Claude for Enterprise into government departments under FedRAMP High and DoD IL5 standards.

3. How to See the Panorama of "Claude Concept Stocks"

Therefore, to create a clearer framework for "Claude concept stocks," one cannot simply look at who appears