高盛半导体财报季前瞻:SOX暴涨后,AMD和AMAT还能涨吗?

- Quan điểm chính: Goldman Sachs cho rằng lợi nhuận quý II của ngành bán dẫn vẫn có dư địa điều chỉnh tăng, nhưng nhóm ngành này đã tăng mạnh (SOX tăng 87,8% trong một quý), không còn phù hợp để tăng trưởng diện rộng; Chi tiêu vốn AI, DRAM/HBM, đóng gói tiên tiến và công cụ EDA là những chủ đề cốt lõi, trong khi sự phân hóa giữa các cổ phiếu sẽ gia tăng.

- Yếu tố then chốt:

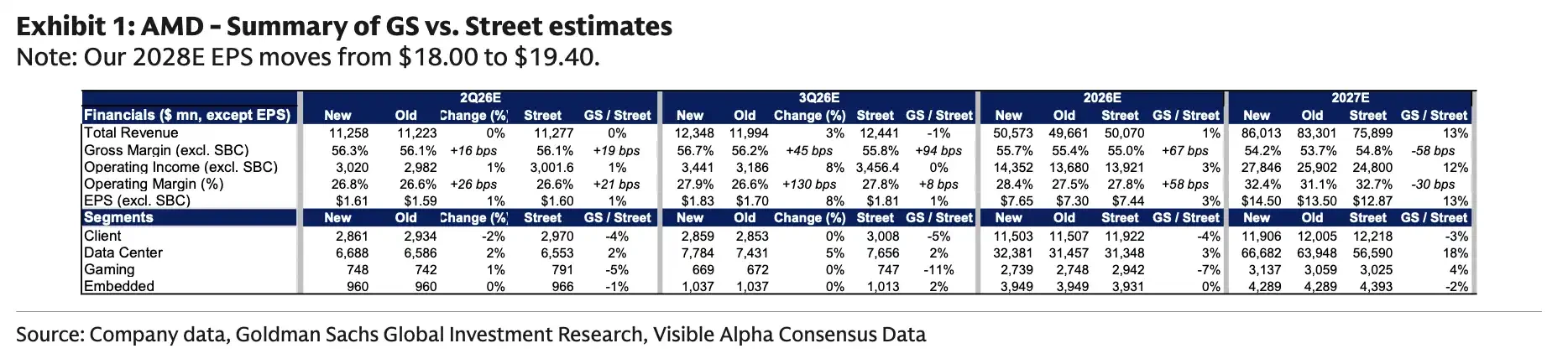

- Chi tiêu vốn AI thúc đẩy lĩnh vực điện toán: CPU máy chủ AI, các dự án ASIC của nhà cung cấp dịch vụ đám mây và card tăng tốc AI hỗ trợ doanh thu trung tâm dữ liệu của các công ty như AMD. Dự báo EPS năm 2027 của AMD được nâng lên 14,50 USD, cao hơn 13% so với kỳ vọng thị trường.

- Bộ nhớ và thiết bị hưởng lợi từ nhu cầu trung hạn: Cung cầu DRAM/HBM thắt chặt, giá HDD được cải thiện; Tầm nhìn đơn hàng của các công ty thiết bị kéo dài đến năm 2028, giá mục tiêu của Applied Materials được nâng lên 645 USD, dựa trên đầu tư DRAM thúc đẩy tăng trưởng năm 2026.

- Phân hóa rõ rệt ở mảng bán dẫn tương tự: Goldman Sachs ưa thích các công ty có mức độ tiếp xúc cao với lĩnh vực công nghiệp, hàng không vũ trụ - quốc phòng và trung tâm dữ liệu (như ON Semiconductor), và thận trọng hơn với các mã phụ thuộc vào điện thoại thông minh hoặc chu kỳ ô tô truyền thống.

- Cần thận trọng với ARM và KLA Corporation: ARM đối mặt với áp lực từ thị trường điện thoại thông minh yếu kém và chi phí hoạt động cao, duy trì xếp hạng bán ra; KLA Corporation chịu ảnh hưởng khi chi tiêu WFE nghiêng về DRAM, có thể hoạt động kém hơn so với các công ty cùng ngành.

- EDA và Qualcomm hưởng lợi từ sự lan tỏa của AI: Cadence được thúc đẩy bởi các công cụ AI tác nhân và nhu cầu EDA, hướng dẫn doanh thu có thể được nâng lên; Mảng kinh doanh trung tâm dữ liệu của Qualcomm được đưa vào câu chuyện tăng trưởng, với mô hình doanh thu FY27-28 được đặt ở mức 5-8,2 tỷ USD.

TL;DR

- Goldman Sachs expects most semiconductor sub-sectors still have room for upward revisions in Q2, but the SOX has already surged approximately 87.8% in a single quarter.

- AI capital expenditure, DRAM/HBM, advanced packaging, and EDA tools are the main drivers of this round of earnings upgrades.

- Goldman Sachs favors AMD, AMAT, and ON, is more cautious on ARM and KLAC, and maintains a neutral stance on Qnity after its price increase.

Before the semiconductor earnings season, stock prices have already run significantly. A review of the Nasdaq Q2 performance shows the PHLX Semiconductor Index rose 87.8% in Q2, marking its best quarterly performance since its inception in 1994 and far exceeding the broader U.S. stock market during the same period. In a Q2 semiconductor outlook report, Goldman Sachs assessed that while fundamentals still have room for upward revision, the sector post-rally is no longer suitable for a 'buy everything' approach. AI servers, memory, advanced packaging, and design software remain the strongest themes, while weak smartphone demand, shifts in equipment spending structure, and export restrictions will amplify stock-specific divergences.

Semiconductors Still Have Room for Upgrades, but the AI Chain is Beginning to Differentiate

Goldman Sachs reports that Q2 results or subsequent guidance for companies in computing, memory storage, semiconductor equipment, and some analog chipmakers could still exceed market expectations.

The main theme in the computing sector remains AI servers. Demand for server CPUs, cloud providers' ASIC projects, and the ramp-up of AI accelerators continue to support data center revenue expectations for companies like AMD. Memory and storage benefit from tight DRAM/HBM supply-demand dynamics, improving HDD pricing, and positive NAND cycle expectations, with limited near-term pressure from new supply.

The equipment chain's focus is more medium-term. AI servers require more HBM and advanced packaging, and memory manufacturers' capacity expansion and technology upgrades will drive demand for deposition, etching, and other process steps. Some equipment companies already have order visibility extending into 2028.

The analog semiconductor recovery is not broad-based. Goldman Sachs prefers companies with higher exposure to industrial, aerospace & defense, and data center markets, and is more cautious on names more reliant on smartphones or traditional automotive cycles.

This divergence is also reflected in Goldman Sachs' tactical choices. The report favors Applied Materials, AMD, and ON Semiconductor, while being more cautious on ARM and KLA. For semiconductor materials and electronic solutions company Qnity, Goldman Sachs still sees upside from improving wafer fab utilization and execution but believes risk/reward has become more balanced after the stock price increase, a judgment primarily based on the report's tone.

AMD and Applied Materials are Goldman Sachs' Two Most Distinct Long Picks

AMD is one of Goldman Sachs' clearest long cases in the computing chain. Goldman Sachs' model shows its 2027 EPS estimate for AMD has been raised to $14.50, approximately 13% above the consensus estimate. The 2027 data center revenue forecast is $66.682 billion, about 18% higher than market expectations.

Supporting this view are strong server CPU demand, improving data center business gross margins, and operating leverage from the subsequent ramp-up of AI chips. AMD previously announced that its Advancing AI 2026 event will be held and live-streamed in San Francisco on July 23, 2026. Beyond the earnings season, the market will focus on whether AMD can provide a clearer AI server roadmap, customer progress, and revenue trajectory at this event.

Goldman Sachs' model shows AMD's 2027E EPS at $14.50, higher than the market's $12.87. 2027E data center revenue is $66.682 billion, exceeding the market's $56.590 billion, with server CPU and MI450 ramp being key drivers.

Applied Materials represents the end of the equipment chain with stronger order visibility. Goldman Sachs raised its price target for Applied Materials from $520 to $645, based on 32x a normalized EPS of $20. The report's key assumption is that strong DRAM investment will drive its best-in-class growth in 2026, with WFE demand visibility extending to 2028.

DRAM is the key focus here. Rising demand for HBM and high-performance memory from AI servers will drive memory manufacturers' capacity expansion and process upgrades. Equipment companies benefit from longer order cycles and higher revenue visibility. The risk is also clear: if cloud vendors or memory makers slow capital expenditures, market expectations for medium-term revenue could quickly be revised downward.

Goldman Sachs' model shows AMAT CY2027E total revenue of $45.972 billion, up 25% year-over-year. The DRAM segment is expected to be $12.4 billion, up 41% year-over-year, representing the main source of equipment upside.

ON Semiconductor is placed in a relatively positive context, not for significant upward revisions, but because near-term expectations have already been lowered. On June 25, the company announced a proposed all-stock acquisition of Synaptics, with an enterprise value of approximately $7 billion, expected to close by mid-2027, pending approvals including Synaptics shareholders. Goldman Sachs believes that after investor expectations have retraced, the potential for ON Semi's quarterly performance to slightly exceed expectations is more noteworthy.

ARM and KLA Show: The Bigger the Rally, the Harder to Ignore Earnings Flaws

Goldman Sachs maintains a Sell rating on ARM with a 12-month price target of $150, based on 50x a normalized EPS of $3. Pressure comes mainly from two areas: persistently weak smartphone demand and higher-than-expected operating expenses.

ARM is still seen by the market as a potential beneficiary of AI and high-performance computing, but the more direct revenue and profit pressures in near-term earnings still stem from mobile licensing revenue and cost expansion. For stocks already elevated by the AI narrative, the market will pay more attention to whether near-term revenue, margins, and guidance can be delivered.

KLA's pressure comes from the composition of equipment spending. Goldman Sachs expects its quarterly results and guidance to be modestly positive but still likely to underperform peers because WFE spending is shifting towards DRAM. DRAM requires less intensity of inspection and metrology equipment compared to logic chips and foundry. An overall uptrend in the equipment cycle does not mean all segments benefit equally.

Qnity falls somewhere in between. The company's Q1 announcement showed Q1 2026 net sales of $1.315 billion and raised its full-year guidance. Goldman Sachs remains positive on improving fab utilization and company execution but believes that after the stock price increase, further upside potential and downside risks are more balanced. For stocks that have already priced in a recovery, earnings reports need not only to deliver good results but also provide sufficiently strong next-stage guidance.

EDA and Qualcomm Also Drawn into Earnings Scrutiny by AI

AI expectations are not limited to the GPU, CPU, and memory chains; they are also spreading to chip design software and data center chips.

Cadence is one of the companies in the EDA chain favored by Goldman Sachs. Public information shows the company raised its 2026 revenue outlook to approximately 17% year-over-year growth after Q1 and launched an engineering solution with Nvidia for agentic AI chip and system design. Goldman Sachs further expects that driven by the monetization of agentic AI tools, IP business, and core EDA demand, the company's 2026 revenue guidance still has potential for upward revision.

Qualcomm's data center business is also back in focus. The company previously mentioned in its investor day materials that the data center business would contribute billions of dollars in revenue starting from FY27. Goldman Sachs' model sets Qualcomm's FY27 and FY28 data center revenue at $5 billion and $8.2 billion, respectively. For Qualcomm, this represents a growth narrative expanding from mobile chips to data centers, but orders, customers, and gross margins still need to be consistently delivered.

The question this earnings season needs to answer is straightforward: Can AI capital expenditure continue to allow semiconductor companies to raise their earnings estimates? Over the past quarter, stock prices have already reflected optimistic expectations. Going forward, the strength of server CPUs, ASICs, HBM, EDA, and equipment orders must be incorporated into revenue and profit models for 2026 and 2027 to sustain valuations after the rally.

Whether Upgrades Can Catch Up with Stock Prices Will Determine the Degree of Earnings Season Divergence

The key point of the Q2 semiconductor earnings season is not whether there is still upward market expectation, but whether the magnitude of the upside can cover the stocks' already-priced-in gains.

Goldman Sachs' outlook points towards a more divergent answer. AI capital expenditure, DRAM/HBM, advanced packaging, and the monetization of EDA tools are still lifting earnings expectations for some companies. After the SOX significantly outperformed the broader market, market tolerance for flaws is decreasing.

Weak smartphone demand will weigh on ARM, the shift in WFE towards DRAM will undermine KLA's relative advantage, and supply chain constraints, export restrictions, and geopolitical risks could also impact order fulfillment. Companies like AMD and Applied Materials, which still have room for model upgrades, will face questions about the pace of delivery. Companies that have already rallied significantly but have limited near-term fundamental flexibility are more likely to face pressure during the earnings season if their guidance is not strong enough.