Meta « Bán Sức Mạnh Tính Toán » Khiến Phần Cứng AI Sụp Đổ? Phố Wall Giải Mã: Đừng Hoảng, Điều Này Không Có Nghĩa Là Dư Thừa Sức Mạnh Tính Toán, Đây Không Phải Là Bước Ngoặt Của Ngành

- Quan điểm cốt lõi: Kế hoạch cho thuê sức mạnh tính toán dư thừa của Meta không phải là tín hiệu cho thấy ngành dư thừa sức mạnh tính toán, mà là sự cân bằng thực tế của gã khổng lồ giữa đầu tư AI và lợi nhuận tài chính; Điều này tác động trực tiếp đến các công ty đám mây mới như CoreWeave, nhưng tạo ra bộ đệm EPS cho các cổ đông của Meta. Xu hướng nhu cầu phần cứng AI cần được xác nhận trong mùa báo cáo tài chính.

- Các yếu tố chính:

- Meta đang xem xét cung cấp mô hình lưu trữ/truy cập API hoặc cho thuê "sức mạnh tính toán thô", tin tức này khiến cổ phiếu CoreWeave giảm 13%, Nebius giảm 15%, phản ánh lo ngại của thị trường về cạnh tranh và việc cắt giảm chi tiêu vốn.

- Mô hình của Morgan Stanley cho thấy chi tiêu vốn năm 2027 của Meta (175 tỷ USD) sẽ không bị cắt giảm do việc cho thuê sức mạnh tính toán tạm thời; nếu mở rộng kinh doanh đám mây, nó thậm chí có thể đẩy chi tiêu lên cao hơn.

- "Phần dư" sức mạnh tính toán của Meta không tương đương với sự dư thừa của toàn ngành; Bernstein chỉ ra rằng tin tức Google hạn chế việc sử dụng tính toán của Meta do giới hạn dung lượng, ngụ ý rằng sức mạnh tính toán thuộc về "tái phân bổ" chứ không phải là "dùng không hết".

- UBS cho rằng việc cho thuê sức mạnh tính toán bên ngoài có thể cung cấp thu nhập ngắn hạn cho Meta, giảm bớt kỳ vọng EPS không đổi vào năm 2027; mỗi 250MW sức mạnh tính toán cho thuê có thể mang lại khoảng 8% tiềm năng tăng EPS.

- CoreWeave đối mặt với rủi ro lớn nhất: Meta là khách hàng chiếm hơn một phần ba hợp đồng của họ, khi gia hạn hợp đồng trong tương lai, Meta có thể chuyển từ bên có nhu cầu thành đối thủ cạnh tranh trực tiếp, gây áp lực lên khả năng thương lượng dài hạn.

- Nguyên nhân chính khiến mảng phần cứng giảm điểm là do giao dịch quá đông đúc và giảm đòn bẩy; bước ngoặt nhu cầu AI cần xem xét liệu chi tiêu vốn của các nhà cung cấp đám mây và ARR ứng dụng AI có tăng tốc trong mùa báo cáo tài chính tháng 7-8 hay không.

- Ba ngân hàng đầu tư duy trì xếp hạng mua vào đối với Meta (giá mục tiêu 775-865 USD), tất cả đều không điều chỉnh định giá dựa trên việc bán sức mạnh tính toán, cốt lõi vẫn dựa vào đổi mới sản phẩm quảng cáo và AI.

Original Author: Long Yue

Original Source: Wall Street News

A piece of news about Meta selling off its surplus computing power has simultaneously brought several most sensitive issues in the AI trading narrative to the table: Is there really a shortage of computing power? Will Meta revise down its capital expenditure? Can the Neocloud still make money?

Wall Street News mentioned that Meta is formulating cloud business plans, potentially offering two types of services: one is managed model/API access, similar to AWS Bedrock; the other is leasing out "raw computing power," akin to a Neocloud model.

Upon the news, shares of CoreWeave, a star next-generation GPU cloud service provider, plummeted 13%, Nebius fell 15%, and the AI hardware sector including chips suffered a heavy blow. If Meta starts selling computing power, investors will naturally ask three things:

First, did Meta buy too much computing power?

Second, is Meta no longer heavily investing in models and AI products?

Third, is the demand curve for AI hardware and Neocloud about to change?

According to information from the trading desk, on July 1st, Wall Street investment banks including UBS, Morgan Stanley, and Bernstein quickly dissected this event. This may not be a collapse of the AI fundamentals, but rather a pragmatic move by a giant to find a balance between computing power constraints and financial returns. This also cannot be simply equated to "Meta no longer needs computing power." However, it has different implications for different assets.

For Meta, leasing out computing power could be a transitional bridge for revenue and EPS. UBS judges: "Selling cloud computing power or model access rights could theoretically generate near-term revenue faster than waiting for Meta Business Agents and Meta AI chatbots to scale, and alleviate concerns about EPS plateauing or contracting in 2027."

For Neocloud companies like CoreWeave, this represents potential competitive pressure.

For the chip and server supply chain, the market is more concerned about whether the subsequent capital expenditure pace will change.

"Having Surplus to Rent Out" ≠ "Industry Computing Power Glut"

The market's shortest chain of reasoning is: Renting out computing power = Computing power glut = Downward revision of capital expenditure.

Meta may have periodic surplus computing power to rent out, but this does not automatically equate to a glut across the entire industry. Different institutions also use different capacity metrics, which cannot be directly added together.

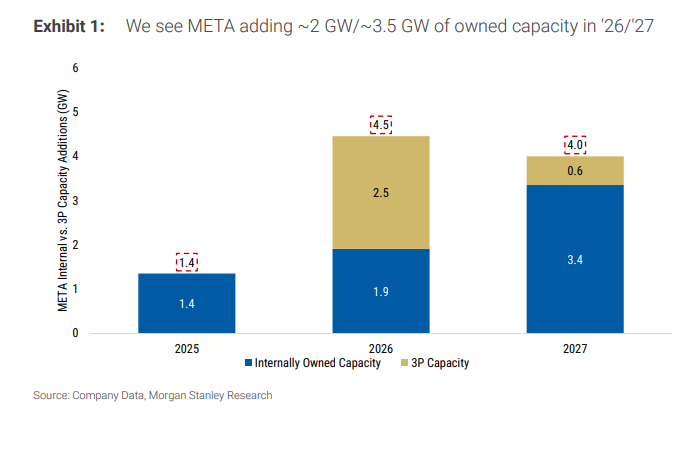

In Morgan Stanley's model, Meta is expected to add approximately 2GW and 3.5GW of self-operated IT capacity in 2026 and 2027 respectively, based on ~3GW at the end of 2025. In comparison, large cloud providers like Amazon and Google are expected to add IT capacity on the scale of 5GW and 9GW respectively in 2027. In other words, even if Meta takes a portion of its own capacity to rent out, it is unlikely to single-handedly change the overall landscape of cloud provider construction over the next three years.

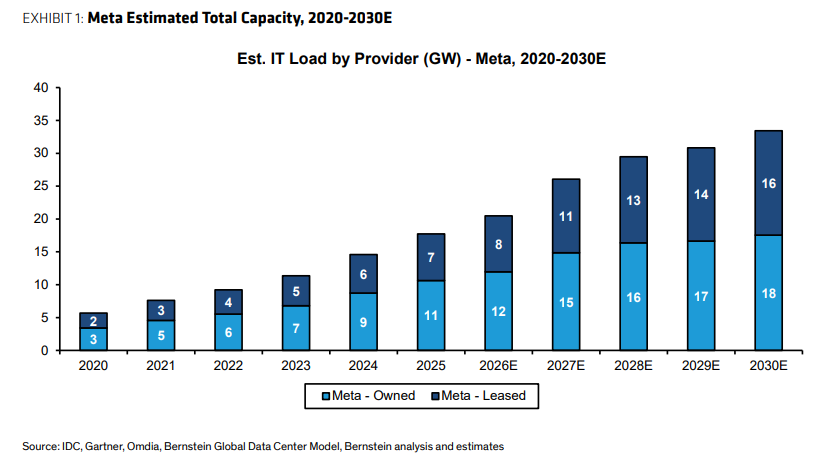

Bernstein uses a broader total data center footprint metric: Meta's current global capacity is estimated at ~20GW, and it will bring another ~14GW online in the coming years, including a mix of owned and leased assets. While this number looks large, it is not "all rentable AI computing power," nor does it represent the same generation of GPUs, the same type of workload, or the same price curve.

Market calculations also include a more aggressive back-of-the-envelope approach: using contracts and capacity planning like Google/Anthropic, AWS/Anthropic/OpenAI, and Microsoft/OpenAI as anchors, the total AI computing power of several cloud providers in the future could be around 20GW or even higher; OpenAI's own Stargate project, and its ~10GW scale arrangements related to Nvidia and Broadcom, are also factored into the demand side observation. The purpose of this metric is not to provide precise predictions, but to illustrate one point: Meta's partial leasing out is insufficient to prove a global glut in AI infrastructure construction.

More counter-intuitively, Bernstein also mentioned that over the weekend, there were reports that Google was limiting Meta's compute usage due to its own capacity constraints. If this claim holds true, Meta, on one hand, is still seeking external computing power, and on the other hand, preparing to sell part of its own computing power in the future. This looks more like a reallocation of 'different generations, different use cases, and different time windows,' rather than simply 'having too much to use.'

This Isn't the First Time Meta Has Put "Selling Computing Power" on the Table

On May 27, 2026, a shareholder asked Meta whether it would build a cloud business to compete with AWS, Azure, etc. Zuckerberg replied:

"Of course, it's definitely something we're considering... We haven't done it yet because we think we can use this computing power ourselves. But obviously, if we reach a stage where we feel we've overbuilt, it's an option we have. That's part of the reason we're confident enough to continue investing in building."

Earlier, on October 29, 2025, Zuckerberg discussed a similar logic:

"We're pretty confident we can absorb a very large portion of any computing power we don't need... Of course, we might overbuild. If we do... we see a lot of new demand both internally and externally. Almost every week, people from outside the company come to us hoping we'll set up an API service or asking if they can get different types of computing power from us. We haven't done that yet. But obviously, if you reach the stage of overbuilding, this can become an option."

This explains why UBS calls it "not new news."

For Meta Shareholders, Selling Computing Power is More Like an "EPS Bridge," Not a New Core Business

For Meta, the most direct benefit of leasing out computing power is converting long-term AI investments into near-term revenue.

In UBS's table, Meta's diluted EPS for 2026 and 2027 is approximately $32.6 and $33.0, respectively. The market's concern is that EPS in 2027 might be flat or even compressed compared to 2026. Leasing out computing power or selling model access rights could provide a revenue and profit buffer, at least until Meta Business Agents and Meta AI chatbots truly scale.

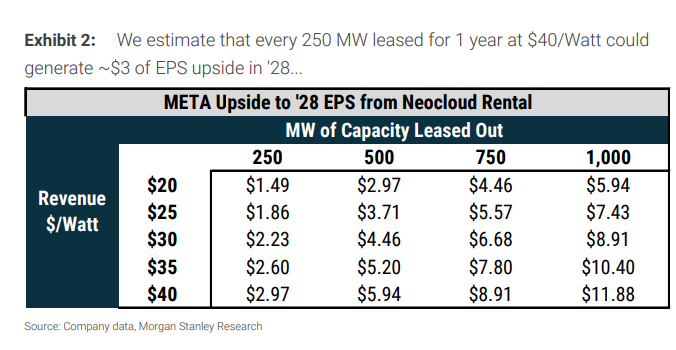

Morgan Stanley's sensitivity analysis is even more intuitive: Leasing out 250MW of computing power for one year at $40/Watt could potentially add about $2.97 to Meta's 2028 EPS, representing roughly an 8% upside. If the capacity expands to 500MW, 750MW, or 1000MW, or if the price is different, the EPS sensitivity would continue to increase or decrease.

This is also why the market hasn't simply interpreted this as bearish. From a Meta shareholder's perspective, Zuckerberg has effectively created an additional fallback option: if internal AI products can't consume all the computing power in the short term, it can be sold to external AI labs first to recover some of the investment.

The market has also drawn a parallel to xAI leasing computing power to Anthropic: 500MW corresponds to $1.25 billion per month, translating to roughly $300 billion per GW per year. If this pricing holds, the implied returns are very high, suggesting that high-quality computing power remains tight in some scenarios. It's not evidence that "no one wants computing power," but rather evidence that "idle capacity windows can be snapped up at high prices."

However, this can only be called a bridge, not the main narrative. Morgan Stanley still places the key to Meta's valuation on front-line product innovation: whether Meta AI, business agents, messaging business, diffusion offerings, subscriptions, etc., can generate more sustainable engagement and revenue growth. Selling computing power can supplement EPS but cannot automatically lift the valuation multiple.

Capital Expenditure May Not Be Revised Down; Becoming a Full Cloud Provider Could Actually Be More Expensive

The market's biggest fear is that Meta's 2027 capital expenditure will be revised down, causing the entire AI hardware chain to lower expectations.

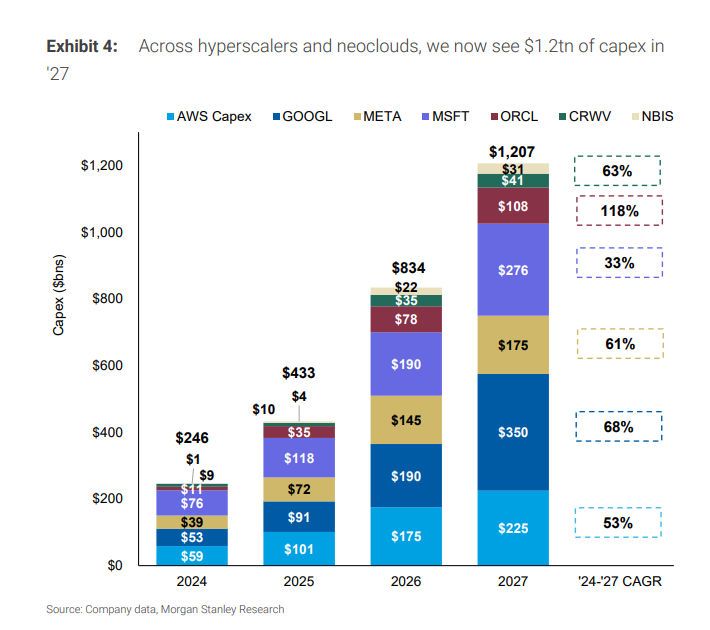

However, Morgan Stanley's model currently assumes Meta's capital expenditure will rise from $145 billion in 2026 to $175 billion in 2027 and $205 billion in 2028. This model is premised on Meta primarily building capacity for its own front-line products, rather than creating a complete hyperscale cloud service provider.

If Meta truly expands its external cloud service, especially building a model/API platform (rather than temporarily renting out bare metal), capital expenditure could actually face upward pressure. A full-scale cloud business requires longer-term data center capacity, more complex software platforms, and the ability to deliver to enterprise customers.

Bernstein also views this issue from a post-2027 perspective. Meta is one of the most important "checkbooks" in the AI market; any change in construction pace will impact the supply chain. But "temporary leasing" and "permanent expansion of cloud business" have different implications for capital expenditure and should not be conflated.

The larger demand side remains inference and agent applications. A market review of H.Y. Computer & AI computing power cited OpenAI's recent article on Codex/agentic AI as a demand signal: personal non-developer users grew 137 times, organizational users grew 189 times, and internal OpenAI users grew 12 times. This perspective emphasizes that the expansion of new use cases may continue to drive up demand for inference computing power.

So the key point of this divergence isn't "Will Meta sell computing power?" but "Is the AI demand curve still steepening?" If overseas ARR accelerates, inference applications grow, and cloud provider CapEx continues to be revised up, then Meta's leasing of computing power looks more like opportunistic asset monetization. If subsequent earnings seasons show collective CapEx downgrades, then this event will become a signal of an industry inflection point.

Selling Bare Metal is Easy; Building a Complete AI Cloud is Very Hard

Meta's potential business has two paths with vastly different difficulty levels.

The first path is selling "bare metal" or raw chip capacity, similar to a neocloud. Customers buy GPU/compute resources, and Meta doesn't immediately need to build a complete suite of enterprise software, developer tools, model platforms, and sales systems.

The second path is offering managed models/API access, similar to AWS Bedrock or Google Vertex AI. This is not a business you can do just by having data centers and chips. It requires model capabilities, a software stack, developer experience, enterprise customer sales, and service support to all be up to par.

Morgan Stanley's model is more cautious about the second path. It notes that Meta's Muse model family does not perform prominently on TerminalBench and SWE Bench Verified, benchmarks relevant to coding ability and third-party usage scenarios. If Meta wants to compete with frontier models like Gemini, subsequent models need significant improvement.

This is also why the deduction that "Meta selling computing power = Meta exiting the model game" is unstable. The potential plans already include model/API access. Front-line products like Meta AI, business agents, messengers, diffusion offerings, and subscription revenue remain the core of long-term valuation. The question isn't whether Meta will do models, but whether it can turn its model capabilities into a cloud service compelling enough for external customers to pay for.

Some in the market discussion also point to Muse Spark, closed-source strategies, and management adjustments as evidence that Meta remains at the table for models. However, these are better suited as follow-up items. At least from the framework of these three firms, the more certain conclusion for now is: the execution barrier for selling bare metal computing power is low, but the barrier for building a full-stack AI cloud is high.

Is CoreWeave the Biggest "Victim"? Customer Turns Potential Competitor

This impact falls most directly on new cloud/GPUaaS companies like CoreWeave.

Bernstein rates CoreWeave as Underperform with a $67 target price; Meta is rated Outperform with a $850 target price. Its logic is straightforward: If Meta provides cloud infrastructure externally, it could directly compete with CoreWeave.

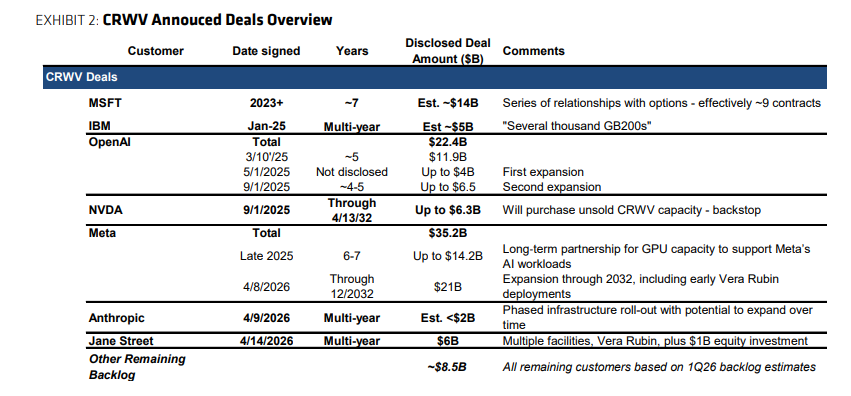

More troublesome is that Meta itself is a major customer of CoreWeave. By Bernstein's account, Meta currently has a $35.2 billion contract with CoreWeave, representing over one-third of CoreWeave's order backlog. Combined with Microsoft's ~$14 billion contract, nearly half of CoreWeave's orders come from clients who could become competitors upon future renewal.

The short-term risk isn't so direct. Existing contracts have strong constraints and won't be terminated immediately, so CoreWeave's short-term revenue and debt pressures may not deteriorate instantly.

The long-term problem is more difficult to handle. If customers build their own clouds and sell their own computing power, the bargaining power of new cloud companies decreases. Especially during renewals, CoreWeave faces not just a demand-side entity, but a potential supply-side entity with money, technology, and data center experience.

JPMorgan's trading desk noted that the market's reaction to CRWV falling 13% and NBIS falling 15% is relatively easy to understand: Meta seemingly transformed from a customer into a potential competitor overnight. For chip hardware, the impact is more indirect; for GPUaaS, the impact feels more like a stress test on the business model.

Why Hardware Fell First: Beyond Fundamentals, Crowded Positions

From a short-term trading perspective, the market isn't just trading on fundamentals.

JPMorgan's trading desk debate splits into two sides: one side is whether the Meta news represents a shift in the narrative around CSP CapEx and AI compute demand; the other side is that positions were too crowded, and deleveraging and profit-taking amplified the decline. Its bias leans towards the latter having higher weight. To truly judge whether a fundamental shift has occurred, one must wait for the upcoming earnings season commentary.

The position backdrop is not light. The main index rebalancing has just passed, the starting point for total flow and leverage ratios was high, and both long and short positions have increased over the past four weeks by +2 standard deviations; hedge funds often deleverage in July over the past five years, with changes typically ranging from -1 to -3 standard deviations. Semiconductor and memory holdings are near the 100th percentile.

This explains why one Meta news item could hammer the entire AI hardware chain. A crowded trade meeting a narrative that "computing power might not be scarce" naturally leads to selling first and asking questions later. Software, crowded shorts, and Chinese ADRs rising over 1.4 standard deviations on the same day also fits the pattern of short covering during a deleveraging process.

For subsequent reversal signals, the market is mainly watching a few things: Whether Meta clarifies; whether overseas AI application ARR accelerates; whether cloud provider CapEx continues to be revised up; whether Q2 earnings exceed expectations. The timeline is concentrated in July-August. For now, it looks more like an observation period rather than a period