白天 theo dõi SK Hynix, tối giao dịch cổ phiếu Mỹ: "Cẩm nang hướng gió châu Á" mới cho thị trường AI toàn cầu?

- Quan điểm cốt lõi: Với tư cách là đầu tàu lưu trữ AI trong khung giờ giao dịch châu Á, biến động giá cổ phiếu của SK Hynix đã trở thành chỉ báo dẫn dắt cho nhóm cổ phiếu công nghệ Mỹ (đặc biệt là Chỉ số Bán dẫn Philadelphia), xuất phát từ vị thế cốt lõi trong chuỗi giá trị toàn diện về HBM, DRAM, NAND và SSD doanh nghiệp. Việc niêm yết tại Mỹ được kỳ vọng sẽ thúc đẩy sự chuyển đổi định giá của công ty từ "cổ phiếu chu kỳ Hàn Quốc" sang "tài sản hạ tầng AI toàn cầu".

- Các yếu tố then chốt:

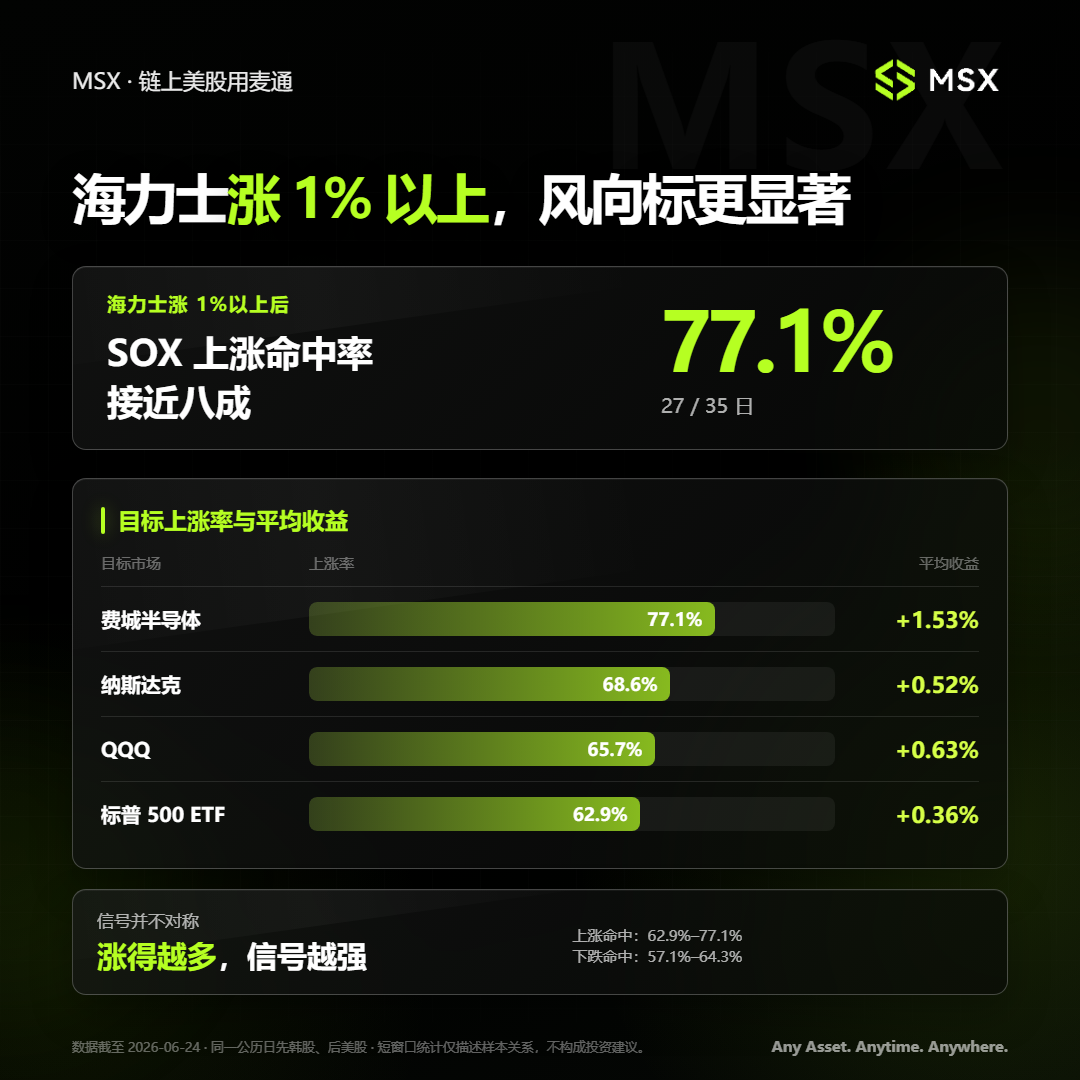

- Kiểm chứng dữ liệu: Khi SK Hynix tăng hơn 1% trong một ngày, xác suất Chỉ số Bán dẫn Philadelphia tăng điểm vào tối hôm đó lên tới 77,1%. Mối tương quan tập trung chủ yếu ở giai đoạn mở cửa gap của thị trường chứng khoán Mỹ, cho thấy tín hiệu từ Hynix có tác động trực tiếp và đáng kể đến giá mở cửa của thị trường Mỹ.

- Vị thế ngành: SK Hynix chiếm khoảng 58% thị phần HBM toàn cầu, là nhà cung cấp cốt lõi cho NVIDIA. Đồng thời, thông qua việc mua lại mảng kinh doanh NAND của Intel, họ đã xây dựng một chuỗi cung ứng lưu trữ AI hoàn chỉnh bao gồm HBM, DRAM, NAND và SSD doanh nghiệp.

- Niêm yết tại Mỹ: SK Hynix có kế hoạch niêm yết trên Nasdaq vào tháng 7 năm 2025, dự kiến huy động khoảng 29,4 tỷ USD. Đây sẽ là một trong những đợt phát hành cổ phiếu lớn nhất lịch sử toàn cầu, nhằm giải quyết vấn đề "chiết khấu Hàn Quốc" và hạ thấp rào cản tiếp cận cho các nhà đầu tư quốc tế.

- Tái định giá: Trên thị trường chứng khoán Mỹ, SK Hynix sẽ được so sánh trực tiếp với Micron và các công ty khác, và có thể được định vị lại như một "tài sản hạ tầng AI toàn cầu" thay vì một cổ phiếu chu kỳ lưu trữ truyền thống, qua đó có khả năng đạt được hệ số định giá cao hơn.

- Thách thức dài hạn: SK Hynix cần duy trì vị thế dẫn đầu công nghệ trong thế hệ HBM tiếp theo (HBM4), chứng minh tính bền vững của biên lợi nhuận cao từ HBM, và thành công trong việc biến Solidigm thành động lực tăng trưởng thứ hai để củng cố câu chuyện mới của mình.

In the past month, observing the Korean stock market alongside the US stock market reveals a rather interesting phenomenon.

SK Hynix during Asian trading hours increasingly acts as an early indicator for the US AI sector that night: If it surges during the day, Nvidia, Micron, and the Philadelphia Semiconductor Index often gap up that evening; if it pulls back first, US tech stocks will likely follow suit and cool down.

This correlation has become particularly evident, especially against the backdrop of recent剧烈波动 in global tech stocks.

The latest example occurred this morning after the US market close. Micron (MU) released explosively strong earnings and guidance that significantly exceeded expectations. When the Korean market opened, Hynix quickly absorbed this memory sector sentiment, surging over 10% during the session.

Of course, simply characterizing this phenomenon as "Hynix rises, US stocks rise" is not precise. After all, a stock worth trillions of dollars is unlikely to dictate the direction of a US capital market sized in the tens of trillions.

However, as global capital trades on the same set of expectations surrounding AI, an increasingly clear cross-market pricing chain has formed, with Hynix becoming the most sensitive "thermometer" within it.

This raises an even more pertinent question: Why Hynix? How did it become the "Asian session bellwether" for global AI trading? And as Hynix formally advances its US listing, how will Wall Street re-price it?

1. Hynix by Day, US Stocks by Night: Superstition or Signal?

From a timing perspective, the Korean market, operating during Asian hours, naturally sits between the previous night's US market close and the next US market open.

This means that when the Korean market opens, investors have already digested the previous night's US market performance and simultaneously trade on new earnings reports and macroeconomic developments released after the US close.

By the time the Korean market closes, US investors, in turn, incorporate the performance of Asian semiconductor companies, along with pre-market trading and stock index futures, as a reference for the day's risk appetite.

Therefore, theoretically, a relay pricing chain spanning two trading time zones does exist between Hynix and US stocks: The US market initially sets the baseline sentiment the night before, Hynix confirms or corrects it during the Asian session, and the US market absorbs the incremental information released by the Asian market at its next open.

To validate this intuition, MSX Maitong conducted a backtest using joint trading days of the Korean and US markets, analyzing the concurrence rate, correlation, and conditional hit rate between Hynix and major US indices.

First, looking at the direction of price movements over the past month, the concurrence rate between Hynix and the Philadelphia Semiconductor Index reached 70%, meaning that out of 20 joint trading days, they moved in the same direction on 14 days.

In comparison, Hynix's concurrence rate with the NASDAQ Composite Index was 65%, with QQQ was 60%, and with the S&P 500 ETF was 55%.

These results first indicate that Hynix is not a broad-based signal equally effective for all US stock assets. It exhibits a clear industrial gradient, with the strongest correlation being with the Philadelphia Semiconductor Index, followed by the tech-heavy NASDAQ and QQQ, and finally spreading to the S&P 500, which represents the overall US market.

This aligns perfectly with Hynix's industrial attributes.

Capital first trades memory and semiconductor sentiment through Hynix. This risk appetite then transmits to the entire AI tech sector, and only when the momentum is strong enough and the impact broad enough does it further diffuse to the broader US stock market.

In other words, Hynix functions more as a semiconductor sentiment outpost than as a macro-level predictor of the US stock market.

Analyzing the daily return correlation over the past three months reveals this same industrial gradient. The correlation coefficient between Hynix and the Philadelphia Semiconductor Index is 0.363, with QQQ at 0.344, and with the NASDAQ Composite Index at 0.313.

It's important to emphasize that these numbers do not mean a 1% rise in Hynix mechanically leads to a 0.363% rise in the SOX. Rather, they measure the degree to which the two return series move in the same direction over the sample period — a value closer to 1 indicates a stronger tendency to rise or fall together; closer to 0 indicates a weaker linear relationship.

Objectively, 0.3 to 0.4 represents only a moderate positive correlation. However, considering the significant noise inherent in daily financial market data, this is already a highly significant and valuable signal.

Further data cleaning and filtering by MSX revealed a distinct "strong volatility trigger" characteristic — when Hynix rises more than 1% in a single day, the hit rate for the Philadelphia Semiconductor Index rising that night is 77.1%. Out of 35 qualifying samples, the index rose 27 times, with an average gain of 1.53%.

Under the same conditions:

- The NASDAQ Composite Index's upward hit rate was 68.6%, with an average gain of 0.52%;

- QQQ's upward hit rate was 65.7%, with an average gain of 0.63%;

- The S&P 500 ETF's upward hit rate was 62.9%, with an average gain of 0.36%;

These results are undoubtedly more explanatory than simple directional concurrence rates.

When Hynix fluctuates only slightly, its movement may be mixed with significant noise from domestic Korean capital, currency effects, and index weighting adjustments. However, a single-day rise exceeding 1% often signals that the market is actively trading a more definitive piece of industry information.

Interestingly, this signal is not perfectly symmetrical. In the current sample, after a significant rise in Hynix, the upward hit rates for major US indices ranged from 62.9% to 77.1%. Conversely, when Hynix fell significantly, the corresponding downward hit rates for US indices were only approximately 57.1% to 64.3%.

This suggests that, at least within the current sample period, Hynix's upward signal is temporarily more reliable than its downward signal.

This might be related to the sample period coinciding with an upward phase in the AI memory cycle. In a market where capital favors long AI opportunities, a significant Hynix rally is more easily interpreted as reconfirmed industry demand, acting as a direct catalyst like Micron's earnings report today.

A decline in Hynix, however, could stem from short-term profit-taking, technical adjustments in the Korean market, or stock-specific capital flows, not necessarily implying a simultaneous deterioration in the global AI fundamentals.

A third set of data further reveals the specific timing when Hynix's signal operates.

If we decompose US stock daily returns into two parts:

- Opening Gap: The change between the day's open and the previous day's close;

- Intraday Return After Open: The change between the day's close and the day's open;

We find that the correlation between Hynix and US stocks is almost entirely concentrated in the opening gap phase.

Specifically, the correlation coefficient between Hynix's daily return and the Philadelphia Semiconductor Index's opening gap is 0.497, with QQQ at 0.483, the NASDAQ Composite Index at 0.435, and the S&P 500 ETF at 0.405.

As mentioned earlier, a correlation coefficient near 0.5, amidst noisy daily cross-market returns, means that the stronger Hynix performs during the day, the more likely the SOX and QQQ are to open higher that night; the weaker Hynix performs, the more likely US semiconductor and tech stocks are to open lower.

However, once the US market actually opens, this connection almost immediately dissipates. The correlation between Hynix's daily return and the intraday return of the SOX is only 0.051, with QQQ at 0.055, the NASDAQ Composite at 0.054, and the S&P 500 ETF at 0.081 — essentially zero.

The stark contrast between these two phases indicates that the information conveyed by Hynix during the Asian session is largely absorbed into the opening price of the US market in one go. Once the US market is open, domestic US data, news, and intraday liquidity take over pricing, and Hynix's explanatory power rapidly diminishes.

Combining these three data sets yields a relatively complete transmission chain:

Hynix first confirms memory and semiconductor sentiment. The SOX receives this signal most directly at the US market open. The impact then diffuses to QQQ and the NASDAQ before potentially transmitting to the S&P 500. Within this, the SOX validates the signal's industry-specific nature, QQQ and the NASDAQ indicate whether it has spread to the core AI theme in US stocks, and the S&P 500 serves as a broad market control.

From this perspective, the linkage between Hynix and the US AI sector does not imply the former unilaterally "drives" the latter. Instead, it appears as two markets continuously pricing the same set of industrial variables, albeit in different time slots.

Hynix gains a time advantage by opening earlier. Furthermore, its core position within the AI memory supply chain gives it a higher information density than typical Asian tech stocks.

This leads to a more crucial question: Why is Hynix uniquely capable of fulfilling this role?

2. Why Hynix Specifically?

The fundamental reason Hynix has achieved this market status isn't merely that the Korean market opens earlier; it's that Hynix has become one of the indispensable "critical few" in the AI infrastructure landscape.

As is well known, in recent years, the market's discussion of AI has primarily centered on GPUs.

Nvidia provides the compute power, cloud providers build data centers, and power, networking, optical communication, and liquid cooling ensure the stable operation of compute clusters. In this narrative, while important, memory has long been viewed as a relatively traditional cyclical component.

But as model scale, training data, and inference demands continue to grow, the challenge for AI systems is no longer just "having enough GPUs." This has redefined memory's role in AI:

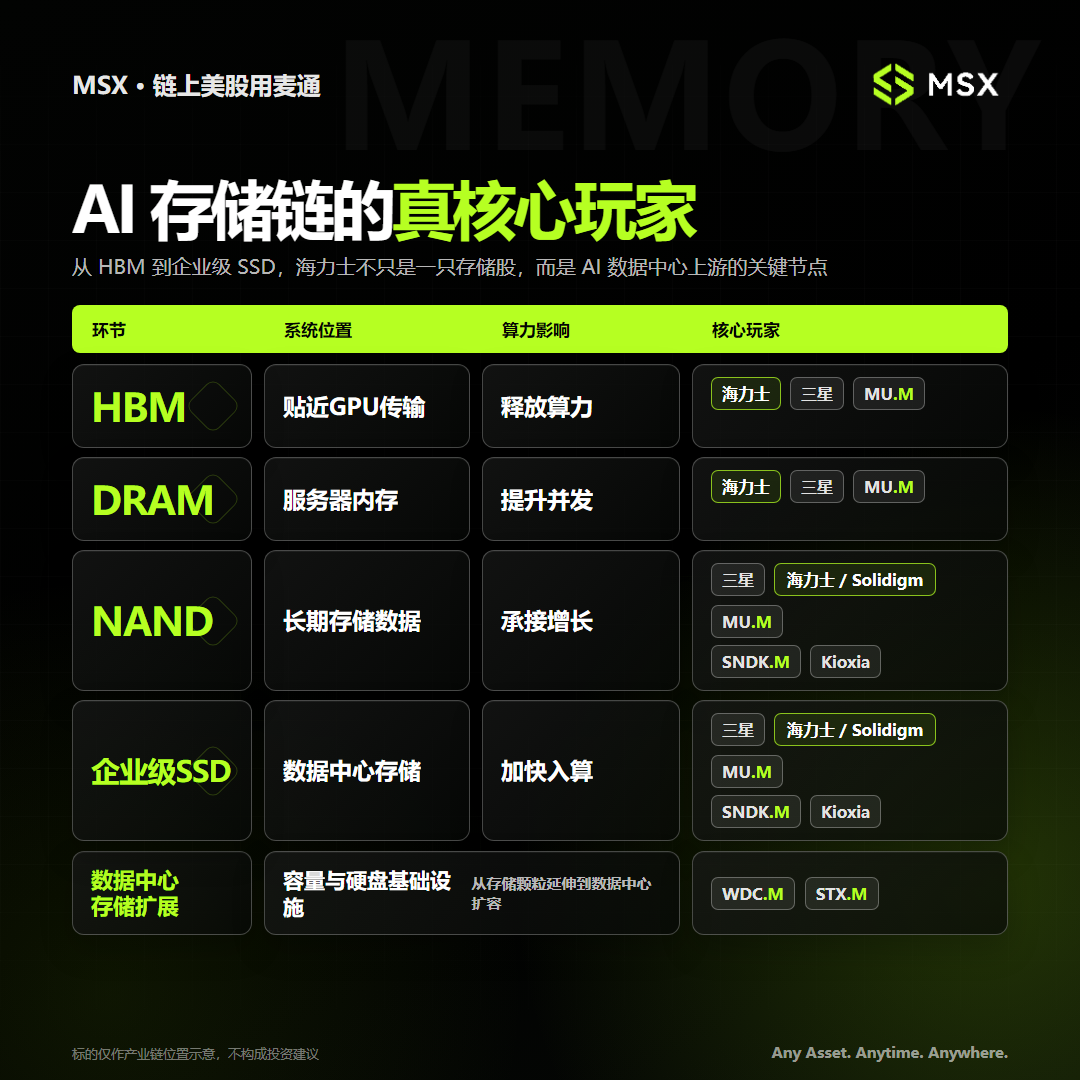

- HBM sits adjacent to the GPU, responsible for high-speed data delivery, determining whether expensive AI chips can fully unleash their compute power;

- Server DRAM serves as the working memory, impacting server concurrency capabilities and task throughput;

- NAND handles the long-term storage of models, training data, and inference data, absorbing the growth in total data volume driven by AI;

- Enterprise SSDs reside in the data center storage layer, accelerating data entry into computing systems through higher capacity and faster read speeds;

To put it more bluntly: the GPU determines "can it compute," HBM determines "can the compute power be fully unleashed," DRAM determines "how many tasks can be handled simultaneously," while NAND and enterprise SSDs determine "where the vast amounts of data are stored and how quickly they can be accessed."

And Hynix spans almost every layer of this AI memory chain, achieving a "grand slam."

In the HBM arena, Hynix remains one of the world's most core suppliers. As of the first quarter of 2026, Hynix held approximately 58% of the global HBM market share, with Samsung and Micron each holding about 21%. It is also one of the most important HBM suppliers for Nvidia's AI accelerators.

The key difference between HBM and traditional standardized memory is its lack of easy substitutability by customers.

Simultaneously, Hynix is not solely an HBM company. As early as 2020, it announced the acquisition of Intel's NAND and SSD business for approximately $9 billion. The first phase closed in 2021, establishing Solidigm in the US, focused on enterprise SSDs and data center storage. In March 2025, the second phase closed, with Intel's remaining NAND technology, intellectual property, and related personnel officially transferring, finalizing the multi-year acquisition.

This deal not only filled a critical gap in Hynix's enterprise storage capabilities but also provided it with two interconnected yet distinct growth curves:

- One curve revolves around HBM and server DRAM, participating in the expansion of AI accelerators and servers;

- The other curve revolves around NAND and enterprise SSDs, catering to the storage demands of training data, model weights, inference caches, and data centers;

Ultimately, Hynix today acts like a high-purity AI memory asset. Its profits, capital expenditures, and market expectations are tightly bound to the memory cycle's景气度.

This business concentration undoubtedly maximizes its stock price elasticity. Thus, the three conditions for Hynix becoming the Asian session bellwether form a closed loop:

- First, it opens earlier in the day, allowing it to digest Asian session information before US markets;

- Second, it is sufficiently core to the industry, spanning almost all four layers of the memory chain: HBM, DRAM, NAND, and enterprise SSDs;

- Third, its business purity and stock price elasticity are high enough to rapidly amplify global capital's assessment of the AI memory cycle;

Therefore, when Hynix experiences significant volatility, the market is not just trading the rise or fall of one Korean company. It is trading expectations about whether AI server shipments can continue to grow, whether memory supply remains tight, and whether global capital remains willing to pay higher valuations for AI hardware.

However, the issue is that Hynix's capital market identity, primarily confined to Korea, has not fully kept pace with its evolving global industrial status.

The recently initiated US listing aims to change this.

3. The US Listing: More Than Just a Change of Venue

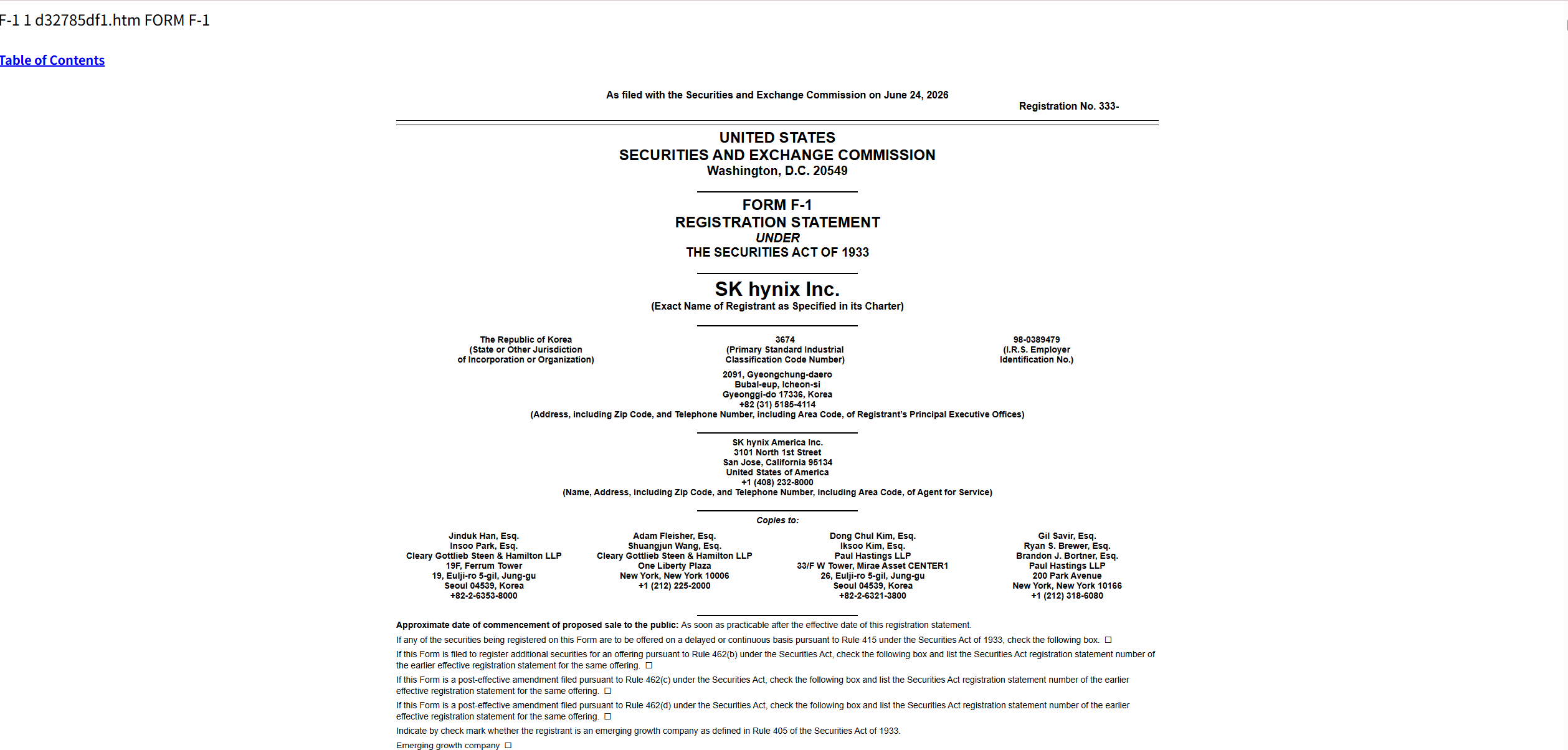

Coincidentally, on June 24, Hynix publicly filed an F-1 registration statement with the U.S. Securities and Exchange Commission (SEC), formally advancing its NASDAQ ADR listing under the proposed ticker "SKHY."

According to the currently disclosed plan, Hynix intends to issue up to 17.79 million new ordinary shares, with a potential fundraising size of approximately $29.4 billion. It plans to debut on the NASDAQ as early as July 10.

If completed at the current indicative price, this would become one of the largest stock offerings in global capital market history — surpassing the approximately $25.6 billion offerings of Alibaba in 2014 and Saudi Aramco in 2019, second only to SpaceX's record-breaking $85.7 billion offering in mid-June.

In other words, Had SpaceX not swooped in to set a new record in June, Hynix itself would have been positioned as the largest stock offering globally.

It's important to clarify that Hynix's move to the US is not a traditional IPO for an unlisted company. It is a secondary listing for a company already listed in Korea, accomplished through an ADR issuance of new shares.

Theoretically, simply changing the trading venue does not magically create new revenue or profit. Beyond the capital raised, the business itself might not seem to change immediately.

However, capital markets price far more than just current profits. What the US listing truly has the potential to change is Hynix's investor base, liquidity, capital expenditure capacity, and the narrative framework the market assigns to it.

The most direct change would be a potential transformation in Hynix's identity from a "Korean memory cycle stock" to a "global AI infrastructure asset."

For a long time, numerous large Korean companies, including Hynix, have been subject to the so-called "Korea Discount." Complex governance structures, foreign exchange risks, market liquidity, and barriers to international capital participation have made it difficult for Korean companies, even those with global competitiveness, to command valuations comparable to their US peers.

Of course, objectively speaking, this phenomenon is not unique to Korea; relative to the US market, all other markets face this. Upon entering the US capital market, Hynix would likely be placed in a different frame of reference — a key company in Nvidia's AI supply chain, a leader in the HBM market, an indispensable infrastructure supplier for AI data centers, and the owner of Solidigm and a US-based AI business platform.

For the same company, placed within different capital market narratives, the valuation multiples investors are willing to grant can be vastly different.