英伟达路演剧透:季收近千亿,为何仍敢谈「增长加速」?

- 核心观点:英伟达增长仍在加速,但驱动力正从少数头部AI实验室和超大规模云厂商,转向网络、CPU、主权AI、工业与企业客户等多元化新来源。其竞争壁垒已从GPU性能扩展到全栈AI平台能力,并将通过提升股东现金回报,兼具高增长与价值股属性。

- 关键要素:

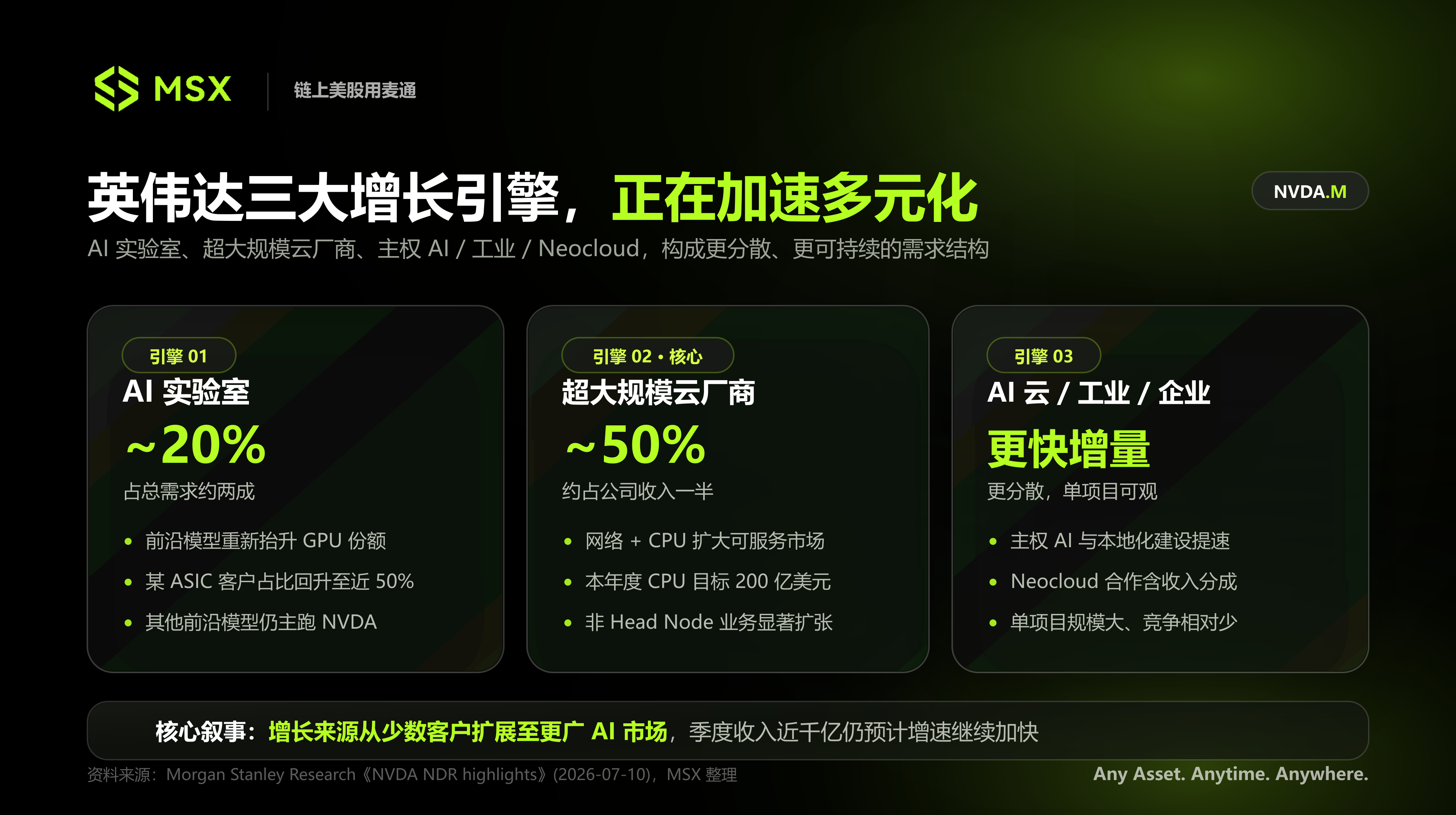

- 增长来源多元化:英伟达需求划分为AI实验室(约20%)、传统云厂商(约50%)及新兴客户(AI云、工业、主权AI)。一家主要依赖ASIC的头部客户,其英伟达算力占比已升至近50%,显示平台综合成本优势。

- ASIC非零和竞争:客户选择取决于单位Token的综合计算成本与部署效率,而非单芯片价格。英伟达通过CUDA、网络、CPU、互连等构成的平台能力构建护城河。

- 产品路线图稳定:英伟达否认Rubin Ultra推迟至2028年,确认仍计划于2027年出货,仅部分机架方案将调整,核心技术方向(800V电力、光互连)不变。

- 存储与电力为供给侧约束:存储短缺预计持续数年,英伟达通过调整内存配置与系统架构,提高有限供应下的系统交付效率,而非需求转弱信号。

- 向价值型资产转型:管理层预计将50%或以上现金流用于股东回报(股票回购与现金分红),旨在吸引成长型资金以外的价值型投资者。

- 摩根士丹利评级:维持“增持”评级和288美元目标价,预计2026-2029年收入将分别达2159亿至7839亿美元,并认为其风险收益比在半导体板块中具吸引力。

Original Report: Morgan Stanley Research – "NVDA NDR Highlights Diversified Growth Opportunities", July 10, 2026

Compilation & Organization: DaiDai

Editor: Frank

Key Takeaways:

- NVIDIA believes growth is accelerating, but the drivers are shifting: Demand is no longer solely reliant on top AI labs and hyperscalers. Networks, CPUs, Neoclouds, Sovereign AI, as well as industrial and enterprise clients, are becoming new incremental sources of growth.

- ASICs and GPUs are not a zero-sum game: For one leading frontier model client previously reliant mainly on ASICs, NVIDIA's computing share has increased to nearly 50%. In numerous real-world workloads, clients ultimately compare not just chip price, but the comprehensive cost per token and deployment efficiency.

- Vera Rubin roadmap not delayed for now: NVIDIA denied rumors of Rubin Ultra being postponed to 2028, confirming plans for shipment in 2027. While some rack solutions will be adjusted, key directions like the 800V power architecture and cross-rack optical interconnects remain unchanged.

- Memory and power remain supply-side constraints, not signals of weakening demand: NVIDIA estimates memory shortages could persist for years. It plans to improve system delivery efficiency under limited supply by adjusting memory configurations, networking, and system architecture.

- Morgan Stanley continues to rank NVIDIA as its top semiconductor pick: The report maintains an "Overweight" rating and a $288 price target. It believes that as the company increases its cash return ratio, NVIDIA is transitioning from a pure high-growth asset to one that increasingly embodies the value attributes of a large-cap tech stock.

When a company's quarterly revenue begins to approach $100 billion, the market typically becomes less concerned with how much more it can grow, and more focused on how long that growth can last.

This is precisely the scrutiny NVIDIA faces today.

Recently, debates surrounding NVIDIA have centered on three main issues: whether global AI infrastructure investment is nearing its peak; whether the push for in-house ASICs by cloud giants like Google, Amazon, and Meta will gradually erode GPU market share; and whether the next-generation Vera Rubin product roadmap faces delays or adjustments.

In early July, Morgan Stanley organized several Non-Deal Roadshows (NDRs) with NVIDIA in California. NVIDIA CEO Jensen Huang, CFO Colette Kress, along with management and the investor relations team, directly engaged with institutional investors. They addressed the market's most pressing concerns regarding growth, competition, and products, aiming to explain how the company's next phase of growth drivers are evolving.

In its post-meeting report, Morgan Stanley characterized the tone of these meetings as "positive." NVIDIA's management offered an even more aggressive assessment: Even as quarterly revenue approaches $100 billion, the company's current growth rate is expected to continue accelerating.

The core support for this assessment does not hinge on a single client suddenly increasing purchases. Instead, it stems from NVIDIA's transformation from a company primarily reliant on GPU cycles and a handful of top clients to a full-stack AI platform encompassing compute, networking, CPUs, models, and cloud infrastructure.

1. NVIDIA Is Redefining Its Sources of Growth

According to NVIDIA's management segmentation during this meeting, the company's future demand primarily stems from three markets: AI labs, traditional hyperscale cloud providers, and emerging clients including AI clouds, industrial sectors, enterprises, and sovereign AI.

This implies that the familiar market narrative of "AI labs training large models, cloud providers purchasing GPUs" can no longer fully explain NVIDIA's next phase of growth.

1.1 AI Labs: ASIC Clients Are Also Increasing GPU Usage

Currently, AI labs account for approximately 20% of NVIDIA's total demand.

A notable detail from the roadshows was that a leading frontier model client, previously reliant mainly on proprietary ASIC development, initially had a low utilization rate of NVIDIA's platform. However, NVIDIA's share of its relevant computing power has now risen to nearly 50%.

This at least demonstrates that ASIC substitution for GPUs is not a one-way street.

As model scale, inference loads, and system complexity continue to increase, clients need to compare not just the price per chip, but the ultimate cost per token generated by the entire system. In many real-world workloads, NVIDIA believes the lowest unit token cost still comes from its complete platform.

Other leading frontier models also still primarily run on NVIDIA's platform. For NVIDIA, the opportunity with AI labs extends beyond following model training scale growth; it also includes regaining market share from clients who previously leaned towards in-house chips.

1.2 Hyperscale Cloud Providers: Expanding from GPUs to Networking and CPUs

Under the new business scope, traditional hyperscale cloud providers remain one of NVIDIA's most important sources of demand, accounting for roughly half of the company's revenue.

However, the primary constraint in the cloud provider market is gradually shifting from chip supply to land, power, and physical space. This means clients haven't stopped wanting to invest, but it's becoming increasingly difficult for them to rapidly build new data centers in the traditional way.

In this context, NVIDIA is expanding its value share within each data center – beyond GPUs, the company is growing its addressable market through networking equipment, CPUs, interconnects, and rack-level system solutions.

During the meetings, management reiterated its $20 billion CPU-related revenue target for the current fiscal year, hinting that a significant portion of this demand comes not from Head Nodes responsible for cluster control and scheduling, but from independent compute racks powered by the Vera CPU.

Vera is not a general-purpose CPU purely chasing more cores; it is optimized for single-threaded workloads and memory access within AI data centers. The direction it represents is that NVIDIA is no longer just selling accelerator cards but is moving further into CPUs, networking, interconnects, and complete system solutions.

This explains why Morgan Stanley believes both cloud providers' in-house ASIC development and NVIDIA's continued growth can coexist. As long as major cloud providers continue to develop and deploy custom chips, and ASIC suppliers like Broadcom maintain high growth, GPU and ASIC competition doesn't have to be zero-sum if the entire AI computing market expands rapidly enough.

Morgan Stanley expects both NVIDIA's and Broadcom's AI-related businesses to maintain very high growth rates over the next year, suggesting the market may not see drastic share shifts in the short term.

1.3 Sovereign AI, Industry, and Neoclouds: More Fragmented, Potentially More Vast

Compared to AI labs and hyperscale cloud providers, the demand from sovereign AI, industrial enterprises, and Neoclouds is more fragmented and projects often take longer to initiate. However, this may be the most noteworthy incremental market for NVIDIA in its next phase.

Geopolitics, data sovereignty, and supply chain localization are driving more countries and regions to build independent AI infrastructure. Concurrently, enterprises in finance, retail, biotechnology, and manufacturing are beginning to integrate AI from a general-purpose tool into a part of their internal production systems.

These types of projects typically require longer cycles for initiation, approval, and deployment. However, once they enter the implementation phase, the scale of individual projects can be substantial, and they often face less direct chip competition compared to the top cloud provider market.

Neoclouds offer another growth model.

These new types of cloud providers, centered around GPU computing power, are absorbing demand that traditional cloud providers cannot immediately fulfill. NVIDIA's partnerships with some Neoclouds may involve co-investment, credit support, and potentially revenue-sharing mechanisms.

While the market is more focused on whether NVIDIA is taking on credit risk for its clients, the flip side is that revenue sharing means NVIDIA could capture a portion of the long-term value from downstream GPU cloud services. Morgan Stanley believes this suggests NVIDIA might not just sell hardware to Neoclouds in the future, but could gradually become a major stakeholder in large GPU cloud networks.

2. ASICs, Rubin, and Memory Constraints – What Truly Affects Growth?

To be realistic, the biggest controversy NVIDIA currently faces isn't whether AI will still grow, but whether chip competition, product roadmaps, and supply constraints will erode the company's market share in this growth cycle.

Based on information from these roadshows, NVIDIA's response is that these issues are all real, but they haven't changed the company's core growth trajectory.

2.1 ASICs Will Grow, But It Doesn't Necessarily Mean GPU Loses Share

For stable, mature, and sufficiently large workloads, ASICs can indeed offer lower chip costs and higher customization efficiency. However, model architectures, inference methods, and development tools are still evolving rapidly. Clients require flexibility, a robust software ecosystem, and system delivery capabilities simultaneously.

Therefore, the decisive factor for client choice isn't the price of a single chip, but the total cost of ownership after accounting for the synergistic performance of model training, inference, networking, memory, and software.

NVIDIA's moat is no longer just GPU performance; it's the platform capability constituted by CUDA, networking, CPUs, interconnects, complete systems, and modeling tools.

2.2 Rubin Roadmap Sees No Material Delays

The roadshows also addressed recent controversies surrounding the Vera Rubin product roadmap.

NVIDIA denied market rumors that Rubin Ultra had been delayed to 2028, confirming that the product is still planned for shipment in 2027. However, management acknowledged that some rack form factors will be adjusted, with the original Kyber rack solution being replaced by what they termed a "superior" design.

This change may support larger single-rack Scale-up domains but does not signify a change in the core technology direction. Key technologies like the 800V power architecture and cross-rack optical interconnects remain on track as planned.

For NVIDIA, attempting more aggressive system designs with each product generation is part of maintaining its lead. What truly needs observation is not whether the roadmap has been adjusted, but whether the company can correct course before mass production and manage large-scale delivery risks.

Morgan Stanley believes that Vera Rubin will still be a major product cycle driving NVIDIA's growth over the next 12 months.

2.3 Memory Shortages: Another Issue Easily Misread by the Market

Management estimates that memory supply constraints could persist for several years.

If the AI industry aims for order-of-magnitude token growth annually, but memory supply cannot expand correspondingly, simply adding more GPUs will not solve the problem. The configuration relationships between compute, networking, and memory must be redesigned accordingly.

One possible adjustment is reducing the LPDDR5 configuration per rack to allow limited memory supply to support more rack deliveries. Another direction involves leveraging networking, caches, and faster on-chip memory to reduce reliance on traditional DRAM in certain scenarios.

During the meetings, management also mentioned technologies using SRAM as a primary memory architecture. While SRAM is typically more expensive than DRAM, its low latency and high bandwidth could offer system-level value for specific inference workloads.

In the short term, these statements might affect market sentiment towards some memory companies, but the underlying logic is not a weakening of memory demand. Quite the opposite: NVIDIA needs to continually adjust its architecture precisely because it expects memory supply to chronically struggle to fully meet the demands of AI computing growth.

Therefore, for the memory industry, what's truly worth watching is not whether NVIDIA reduces a certain memory type's per-system configuration, but how the value of memory in AI systems will be redistributed among HBM, LPDDR, SRAM, caches, and networks.

2.4 The Importance of Nemotron and Open Models

Beyond hardware, NVIDIA is also strengthening the role of open models and enterprise AI software.

Using professional scenarios like circuit design as examples, management pointed out that general-purpose closed-source models may not meet enterprise requirements for specialized knowledge, data security, and workflow control. What enterprises truly need is often not just to call an external model, but to build a controllable and customizable AI system based on their own data and experience.

This is the significance of open models like Nemotron.

They allow enterprises to train, fine-tune, and deploy models around their specific business needs, while retaining control over the models, data, and infrastructure. For NVIDIA, open models are not just a software product; they are a crucial entry point connecting GPUs, networking, inference frameworks, models, and enterprise applications.

NVIDIA aims to build not just a set of high-performance computing hardware, but a complete AI technology stack that enterprises can fully control and deploy.

3. How Does Morgan Stanley Value NVIDIA?

Another important goal of these roadshows was to expand NVIDIA's coverage among value-oriented investors.

As is well known, over the past few years, NVIDIA has been primarily viewed as a quintessential high-growth asset. However, as the company's market cap and institutional holdings have expanded significantly, many growth funds are already heavily invested in NVIDIA, with some nearing their internal single-stock holding limits. Consequently, NVIDIA's capacity to increase allocations solely from growth-oriented capital is becoming limited.

Therefore, NVIDIA needs to offer the market a different valuation logic.

Management indicated that starting from the current phase, the company will allocate 50% or more of its free cash flow to shareholder returns. In this context, increasing stock buybacks and cash returns allow NVIDIA to maintain its high-growth attributes while increasingly embodying the value characteristics of a large, mature technology company.

In other words, NVIDIA wants the market to use two frameworks simultaneously for its valuation: On one hand, it remains an AI infrastructure company capable of sustaining high growth; on the other hand, it is becoming a mega-cap tech platform capable of generating and returning massive cash flows.

Based on this assessment, Morgan Stanley continues to rank NVIDIA as its top semiconductor pick, maintaining an "Overweight" rating and a $288 price target, outlining three risk/reward scenarios:

- Base Case: Price target of $288, based on ~22x FY2027 (calendar year) EPS estimate of $13.08. The report forecasts NVIDIA revenue growth of 82.0% in 2026 and 52.4% in 2027 (CY).

- Bull Case: Price target of $330, based on ~23x FY2027 EPS estimate of $14.00. Core assumptions include continued high growth in the data center business, with networking, Vera Rubin systems, and software revenue driving a higher premium for NVIDIA's full-stack AI computing platform. Further upside could come from the scaling of AI PC, autonomous driving, and robotics businesses, as well as an increased revenue share from high-margin software and AI services.

- Bear Case: Price target of $160, based on ~16x FY2027 EPS estimate of $10.00. Key risks include data center supply catching up to demand faster, leading to a significant deceleration in AI infrastructure growth; clients reducing dependence on NVIDIA through in-house ASICs; AMD or other competitors regaining market share; and tariffs/export controls having a higher-than-expected impact on revenue.

From a financial forecast perspective, Morgan Stanley estimates NVIDIA's GAAP revenue for 2026–2029 to reach $215.938 billion, $393.005 billion, $598.809 billion, and $783.877 billion, respectively; gross margins of 71.3%, 74.4%, 72.5%, and 72.0%; and EPS of $4.61, $8.96, $13.08, and $17.63, respectively.

The core judgment behind these forecasts is that, even though NVIDIA's revenue base is already massive, the expansion of AI infrastructure is still expected to drive its revenue and profit at a relatively high growth rate for several years. Networking, CPUs, software, and system-level solutions will contribute more incrementally beyond GPUs.

Of course, Morgan Stanley acknowledges that memory, networking, and other supply chain segments might possess higher earnings flexibility at certain stages. In fact, during past semiconductor cycles, Morgan Stanley has rotated its top pick away from NVIDIA towards companies like SanDisk and Micron.

However, from a risk/reward perspective, Morgan Stanley believes NVIDIA remains one of the most attractive core assets in the semiconductor sector.

On one hand, the company's current valuation multiple might be constrained by its mega-cap status and index weighting. On the other hand, compared to other computing semiconductor companies like AMD and Broadcom, NVIDIA does not command a particularly obvious valuation premium. Morgan Stanley believes that as growth sources further diversify and cash returns increase, the valuation gap between NVIDIA and some peers should eventually narrow.

However, market positioning does not present a uniformly optimistic picture. The report shows that active institutional investor ownership has reached 50.9%, indicating a high base of holdings from growth funds. Simultaneously, Morgan Stanley's quantitative model places NVIDIA in the 4th quintile for both the next 3-month and 24-month outlook, meaning it has not yet entered the quintile most favored by quantitative capital (1st quintile being most favored, 5th least