6 months to decide the outcome? SemiAnalysis: Meta could surpass Google to become the "third pole" of AI

- Key Takeaway: SemiAnalysis's report makes a bold prediction that Meta's Super Intelligence Lab could surpass Google within the next six months, becoming the strongest contender behind OpenAI and Anthropic. This judgment is based on three factors: large-scale talent and data deals, reinforcement learning data production, and computing power expansion.

- Key Elements:

- Large-scale Deals and Talent Acquisition: Meta invested $14.3 billion in Scale AI. By bringing in its founder and integrating the SEAL team (Safety, Evaluation, Alignment), it is shoring up its evaluation, alignment, and post-training capabilities, coupled with compensation packages worth hundreds of millions of dollars to attract talent.

- Reinforcement Learning Data Production: Meta has reassigned approximately 3,000 engineers as full-time RL task creators, utilizing internal real-world workflows (such as code fixes, tool calls) to generate long-tail training data, thereby improving the model's practical capabilities in agent scenarios.

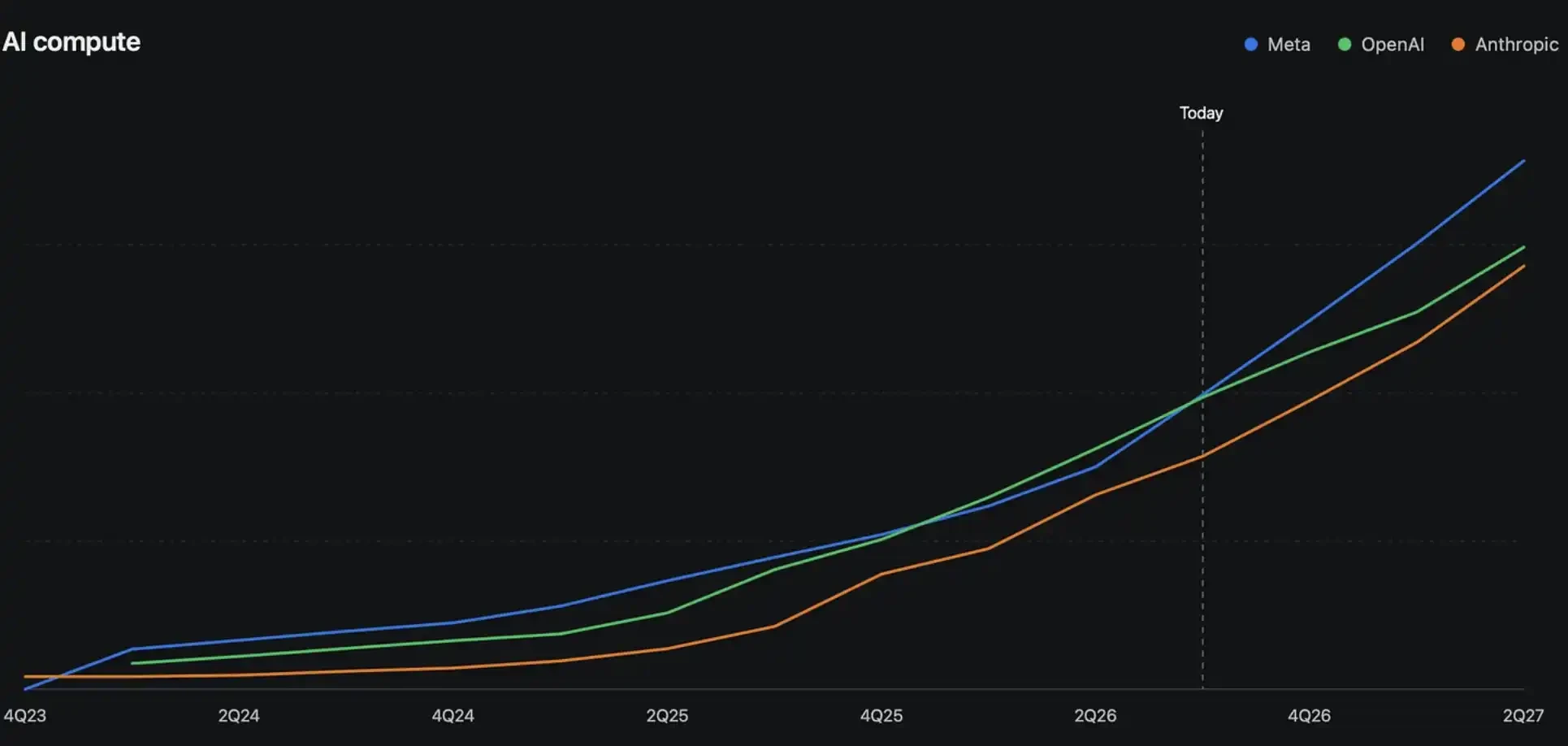

- Computing Power Infrastructure Expansion: Meta signed contracts for over 5GW of data center capacity in the first half of the year, with the bulk of the incremental capacity allocated to the Super Intelligence Lab. This large-scale deployment of computing power accelerates model training, post-training, and agent loops, trading infrastructure investment for iteration speed.

- Current Models Not Yet Leading: The Muse Spark 1.1 model has not yet reached the frontier in most benchmarks, while the larger model, codenamed Watermelon, is still in training. The report primarily bets on the speed of catching up over the next six months rather than current results.

- Controversy over Google's Resource Allocation: SemiAnalysis believes that a significant portion of Google's computing power serves its cloud business and third-party APIs, and the concentration of resources dedicated to frontier model training is lower than external expectations. This creates an opportunity for Meta's focused investment to surpass them.

TL;DR

- SemiAnalysis bets that Meta could surpass Google within the next 6 months, becoming the strongest contender after OpenAI and Anthropic.

- This judgment is based on three fronts: the $14.3 billion Scale AI deal, RL data production, and multi-GW compute power expansion.

- Muse Spark 1.1 still hasn't matched frontier models. Whether Meta can catch up to Google depends on the performance of its next-generation model.

In its latest report, SemiAnalysis makes a bold call: Meta’s super-intelligence lab is not yet a frontier model winner, but if talent, reinforcement learning data, and compute power expansion all materialize, it has a chance to overtake Google in the next 6 months, becoming the most competitive player after OpenAI and Anthropic.

This is not to say Meta has already caught up. Meta released Muse Spark in April, and according to Axios on July 9, Muse Spark 1.1 has opened its API to developers, priced at $1.25 per million input tokens and $4.25 per million output tokens. Axios notes that this is not the "quantum leap" model Meta had hoped for, and a larger model codenamed Watermelon is still in training.

What SemiAnalysis is betting on is something else: after the setback with Llama 4, Zuckerberg is restructuring the AI organization more aggressively, pouring money, talent, internal engineering resources, and data center capacity into the super-intelligence lab. The core disagreement in the report is whether Google can still hold its position as the third pole of AI.

Current Models Aren't Strong; the Report Bets on a 6-Month Catch-Up Pace

After the debut of Muse Spark, Meta’s super-intelligence lab has not replicated the open-source leadership feeling from the Llama 3 and Llama 3.1 era. According to SemiAnalysis's tests and judgments, Muse Spark and its subsequent versions still struggle to be called frontier models in most benchmarks and general agent scenarios.

This is also where the report requires the most caveats. Details like Muse Spark 1.1 being roughly equivalent to Opus 4.6 or GLM 5.2, or its internal token usage not being migrated for now, are based on the author's testing and model assessments, not Meta's official statements. At least from public information, Meta has yet to produce a model that can directly challenge OpenAI and Anthropic.

But SemiAnalysis is focused on the slope. After the failure of Llama 4, Meta's super-intelligence team underwent a large-scale reorganization, and the short-term organizational chaos is being absorbed. The report judges that if the next round of model training and reinforcement learning data production starts to reflect in the products, Meta's position might be higher than the current leaderboard suggests.

The $14.3 Billion Scale AI Deal Secures the Scarcest Resource for Frontier Models: Talent

Meta's most prominent move is its $14.3 billion investment in Scale AI. As reported by Fortune, Forbes, Reuters, and other media, Meta used this deal to bring in Scale AI founder Alexandr Wang, having him join or lead super-intelligence related teams.

In the frontier model competition, this deal is more than just buying a data labeling company; it looks like an aggressive talent acquisition. Scale's safety, evaluation, and alignment team, SEAL, is seen by SemiAnalysis as a vital source for Meta to bolster its evaluation, alignment, and post-training capabilities.

Reuters also mentioned that Meta offered AI engineers compensation packages worth hundreds of millions of dollars. This figure indicates that Meta has prioritized super-intelligence at the company level, not just as ordinary AI product iteration. For a large tech company, the real challenge isn't allocating a budget, but aligning research, products, infrastructure, and management towards a single goal.

SemiAnalysis cites Alexandr Wang's recent statements on a podcast, saying that true frontier labs often first believe super-intelligence is near, and then let business decisions follow that judgment. The report interprets Meta's recent actions as an alignment with the OpenAI/Anthropic-style AGI priority.

3,000 Engineers Shifted to RL, Turning Internal Work into Training Data

Beyond talent, reinforcement learning tasks and real work data constitute the second front.

Today, model capability improvements no longer rely solely on pre-training corpora. More critical is whether a model can complete tasks in environments close to real work: understanding context, using tools, executing tests, fixing errors, and iterating based on results. Codebase fixes, product analysis, and internal tool calls are all closer to the real difficulty of white-collar work than standard exam questions.

SemiAnalysis states that Meta has reassigned approximately 3,000 engineers to become full-time RL task creators. This figure needs to be taken in the context of the report, but if executed well, Meta's advantage becomes clear: it’s not simply outsourcing the purchase of synthetic data, but turning its own engineering organization into a training task production line.

This type of data is especially important for agents. Many RL tasks seem difficult, but the actual prompts describe steps in too much detail, inconsistent with real work habits. Screen recordings, daily workflows, tool invocation logs, and internal evaluation systems might be more suitable for training models capable of automating white-collar work.

This is also one reason the report favors Meta catching up to Google. Google has DeepMind, Gemini, TPUs, and its cloud business, but Meta is concentrating its internal organization, data, and engineering capabilities on a single model objective.

Multi-GW Compute Expansion Brings Meta to the Frontier Table

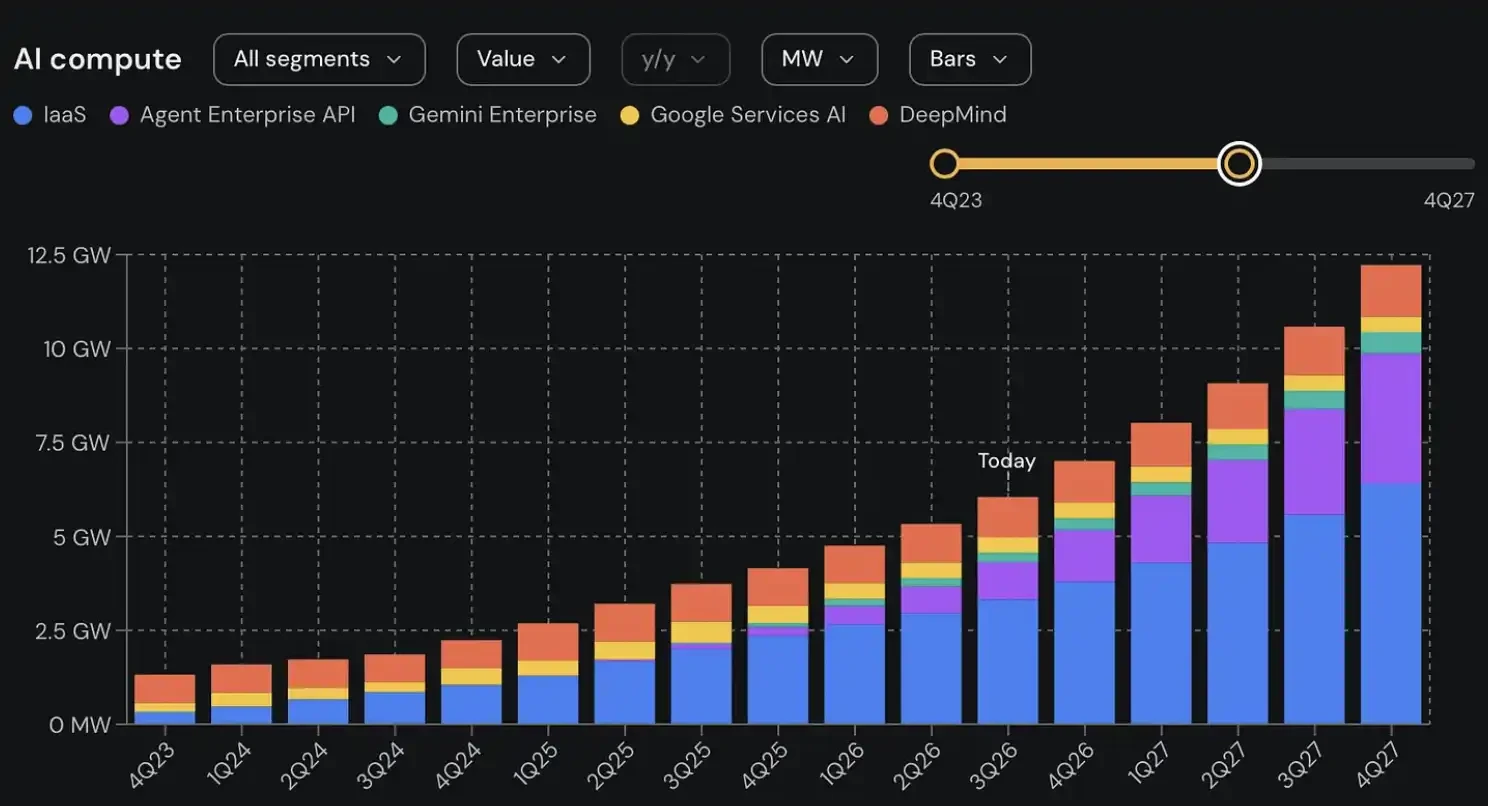

Compute power is the third front. In a July 2 article, SemiAnalysis stated that Meta signed contracts for over 5GW of capacity in the first half of this year, totaling nearly 10GW in deals since 2024, and judged that a large portion of the incremental capacity would still flow to Meta's super-intelligence lab.

For ordinary investors, the key isn't the specific data center design, but the direction of capital expenditure. Meta is expanding compute power not for conventional cloud services, but to prepare larger clusters for internal model training, post-training, and agent loops. The heavier the training and reinforcement learning, the more compute deployment speed affects model iteration speed.

The report also mentions infrastructure concepts like cross-regional connectivity and rapid data center deployment. These details are still part of SemiAnalysis's model projections, but the direction is clear: Meta is using infrastructure to buy time.

Google's controversy isn't whether it has compute power, but how it is allocated. SemiAnalysis expects a significant portion of Google's new data center capacity will serve its IaaS and third-party API businesses, and the resource concentration available to DeepMind for frontier training might be lower than the outside perception. Even if Google uses external financing or capital markets to build more AI infrastructure, the new capacity could be partially consumed by cloud customers.

Therefore, the report offers a more controversial judgment: the competition for the third spot in AI is no longer a secure position for Google, but could become a re-ranking among Meta, Google, and other high-compute players.

The Biggest Problem Remains: Meta Hasn't Produced a Frontier Model Yet

The most impactful, and riskiest, aspect of this report is that it bets on the next 6 months, not on results that have already happened.

Meta already has the $14.3 billion Scale AI deal, Alexandr Wang's joining, hundred-million-dollar compensation packages, multi-GW compute expansion, and the shift of internal engineering resources towards RL tasks. However, these are still conditions for catching up, not a model victory in itself.

Muse Spark 1.1 cannot yet prove that Meta has entered the position occupied by OpenAI and Anthropic. Larger models like Watermelon are still in training, and their actual capabilities, costs, availability, and developer feedback have yet to be tested by the market.

Google is not out of the game either. DeepMind, TPUs, Gemini, and its cloud business are still solid advantages. The real disagreement lies in that Google's resources must serve search, cloud, API customers, and internal models simultaneously, whereas Meta is concentrating more resources on its super-intelligence lab.

If Meta's next-generation model shows no significant improvement, the $14.3 billion talent acquisition and massive compute investment will become a heavier capital expenditure burden. Conversely, if the new model and agent products deliver, the third-place position in AI will truly become uncertain.