美银最新研判:三大利空冲击后,内存涨价周期远未到「见顶时刻」

- 核心观点:7月2日内存股回调源于市场对AI内存周期是否见顶的质疑,但美银报告认为,当前短期供需数据仍偏强,而长期AI需求兑现及供给风险是市场分歧的关键。

- 关键要素:

- Meta算力出租、长鑫进入iPhone供应链及韩国800万亿韩元投资计划,是触发市场担忧的三条利空线索,但美银认为这些因素尚不足以证明周期已反转。

- 美银从供应链确认,Meta并未因AI服务器过剩而削减订单,其AI数据中心仍在积极采用先进内存,资本开支继续扩张。

- 长鑫进入iPhone供应链短期内更像苹果的谈判筹码,受限于技术、专利和认证门槛,短期内不会改变全球移动DRAM供需结构。

- 韩国800万亿韩元投资计划为长期产业规划,未来两三年内不会释放大量新增产能,对当前周期的影响有限。

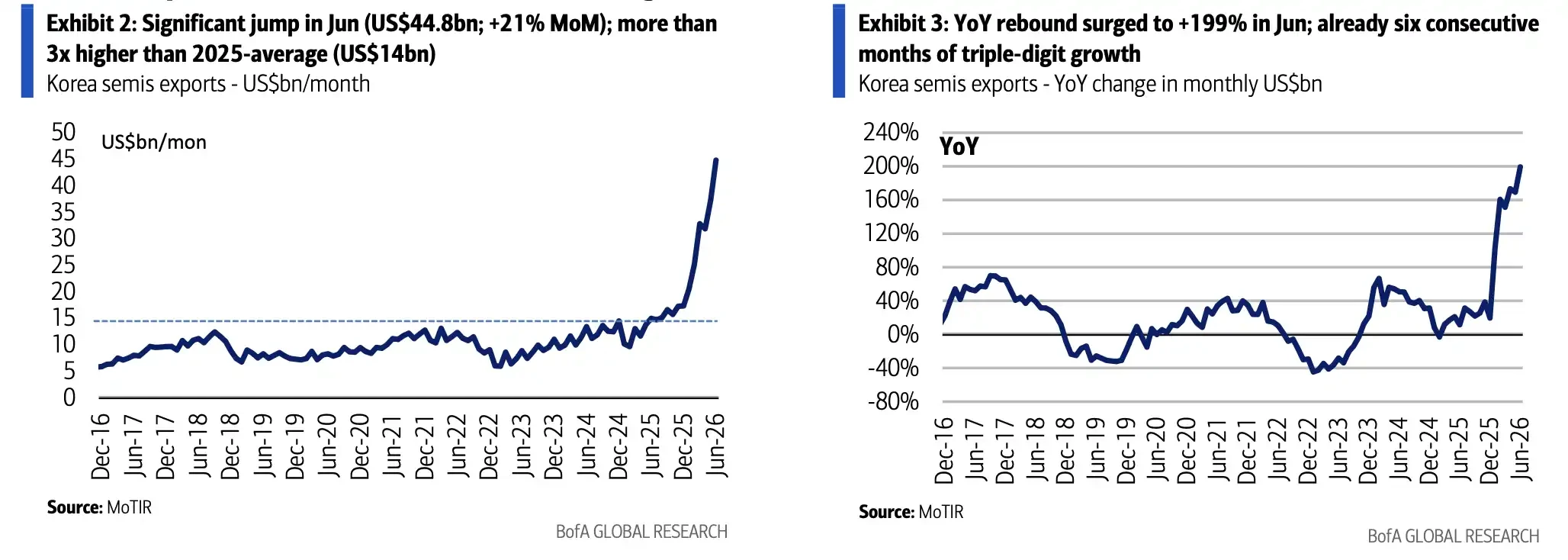

- 当前短期数据仍偏强:6月韩国半导体出口同比增长199.5%,2026年三季度DRAM价格预期上调至环比增长13%-18%,现货价创新高。

- 三星二季度初步业绩(7月7日发布)将成为检验内存景气度的重要窗口,若内存部门表现超预期,将缓解市场对周期见顶的担忧。

- AI需求能否在2027年后持续兑现,以及地缘政治和中国本土化进程对供应链的影响,是未来市场长期关注的核心分歧点。

TL;DR

- After a collective pullback in memory stocks on July 2nd, the market began questioning whether the AI-driven memory pricing cycle is nearing its peak.

- Bank of America believes that Meta's AI computing rental plans, CXMT's potential entry into the iPhone supply chain, and South Korea's 800 trillion won investment plan have not yet altered the short-term supply-demand dynamics.

- South Korean export data, price forecasts, and cloud capex remain relatively strong, but the key divergence point lies in whether AI demand will materialize as expected post-2027.

On July 2nd, AI and semiconductor stocks faced a concentrated sell-off, dragging the memory sector down with them. Stocks like SK Hynix, Samsung, Micron, Kioxia, and Western Digital saw notable declines. The trigger wasn't a single earnings report but three bearish signals appearing simultaneously: Meta reportedly planning to rent out its AI computing power externally, ChangXin Memory Technologies (CXMT) potentially entering Apple's iPhone supply chain, and South Korea announcing a massive ~800 trillion won semiconductor and memory investment plan. According to a recent Bank of America memory industry report, while these developments are worth monitoring, they are not yet sufficient evidence to suggest a reversal in the AI memory cycle.

The main driver of this memory market cycle isn't traditional PC or smartphone inventory restocking, but the continuous pull from AI data centers for high-end memory like HBM, LPDDR5, and enterprise SSDs. For the market, the question behind the stock price correction is straightforward: Is AI demand being disproven, and could supply suddenly surge? Bank of America's answer leans towards cautious optimism. Short-term price and export data still support an upward memory cycle, but investors are no longer just watching prices rise; they are beginning to question how long this uptrend can last.

Meta's AI Computing Rental Does Not Equal Reduced AI Orders

The market's most immediate concern stems from Meta. According to a report by Bloomberg Law, Meta is planning a cloud infrastructure business to sell AI computing power and model access to external clients. Media outlets like Tom's Hardware subsequently interpreted this as a potential source of "excess computing capacity." If Meta were indeed cutting long-term chip and component orders due to an oversupply of AI servers, demand for HBM, LPDDR5, and enterprise SSDs would be negatively impacted.

However, feedback Bank of America received from the chip supply chain does not support this inference. The report states that Meta's AI data centers are still more aggressively adopting advanced memory, with long-term chip and component orders strengthening. There is no evidence of order cuts due to server oversupply. At least from the current supply chain perspective, Meta appears to be continuing its expansion of AI infrastructure rather than scaling back prematurely.

This explains why memory stocks are so sensitive to rumors about a single client. AI servers consume significantly more memory than traditional servers. HBM is used for GPU acceleration, while LPDDR5 and enterprise SSDs also require higher bandwidth, lower power consumption, and greater storage performance. If major cloud providers cut capital expenditure, expectations for high-end memory prices and orders would come under pressure quickly. Conversely, as long as hyperscale cloud providers continue to ramp up spending, the short-term supply-demand tightness is hard to resolve quickly.

CXMT Entering iPhone: More of Apple's Bargaining Chip in the Short Term

The second concern is CXMT potentially entering Apple's iPhone supply chain. If Apple were to adopt CXMT's DRAM on a large scale, the pricing power of Korean and US memory giants in the mobile DRAM market could be weakened, reinforcing expectations of accelerated local substitution in China.

However, this impact has clear short-term limitations. Public reports primarily cite Bank of America's view that for CXMT to enter the iPhone supply chain, it needs to simultaneously overcome US semiconductor restrictions against China, pass Apple's quality and specification certifications, and navigate potential intellectual property litigation risks. The relevant low-power DRAM must also meet stringent speed, power consumption, and ECC requirements, while Korean and US giants still hold significant technological and patent barriers in advanced mobile DRAM.

Even if Apple makes small trial use of CXMT chips in lower-end models like the iPhone 18e, the actual order volume could be limited. Bank of America believes that demand for lower-end models in the Chinese market is relatively constrained, limiting the procurement scale. A more realistic impact is that Apple uses this to strengthen its negotiating position with Korean and US memory giants for contract prices in the second half of 2026 or 2027, rather than immediately changing the global mobile DRAM supply-demand structure.

CXMT's long-term impact cannot be ignored. China's localization efforts will continue to change some clients' procurement choices. But for the current cycle, it is not yet evidence of a "sudden supply influx." What the market truly cares about is whether CXMT can stably pass Apple's quality certifications, how US restrictions will be enforced, and whether its capacity can expand from low-end models to higher-specification products.

South Korea's 800 Trillion Won Plan: Not New Supply for the Next Two Years

The third concern stems from the massive semiconductor and memory investment plan announced by the South Korean government. According to information released by South Korea in late June, the plan is sized at approximately 800 trillion won (~$520 billion), involving Samsung, SK Hynix, new fabs, and HBM capacity expansion. Such a large figure is easily interpreted by the market as a signal for a new round of major capacity expansion.

But Bank of America believes this is not a direct supply signal for the current cycle. The report states that the relevant new clusters and supporting infrastructure are more aligned with long-term industrial planning. Some projects still have a long way to go before mass production and are unlikely to unleash a large amount of new capacity abruptly in the next two to three years.

Past experience in the memory industry, where "capex peaks often correspond to cycle peaks," has made any large-scale fab construction plan trigger caution. However, current enterprise demand is concentrated in AI-related products like HBM, SOCAMM, and enterprise SSDs. Constraints related to advanced process nodes, packaging, yield rates, and customer certifications are much stronger than in traditional DRAM. Long-term investment plans do not equate to short-term effective supply, especially when high-end memory capacity remains constrained.

Exports and Prices Still Rising; Market Begins Asking How Long It Can Last

Short-term data remains on the side of the bulls. Official data from South Korea shows that semiconductor exports in June reached approximately $44.8 billion, up 199.5% year-over-year, with total exports reaching about $102.25 billion, up 70.9% year-over-year. This data corroborates the continued upward trend in memory prices.

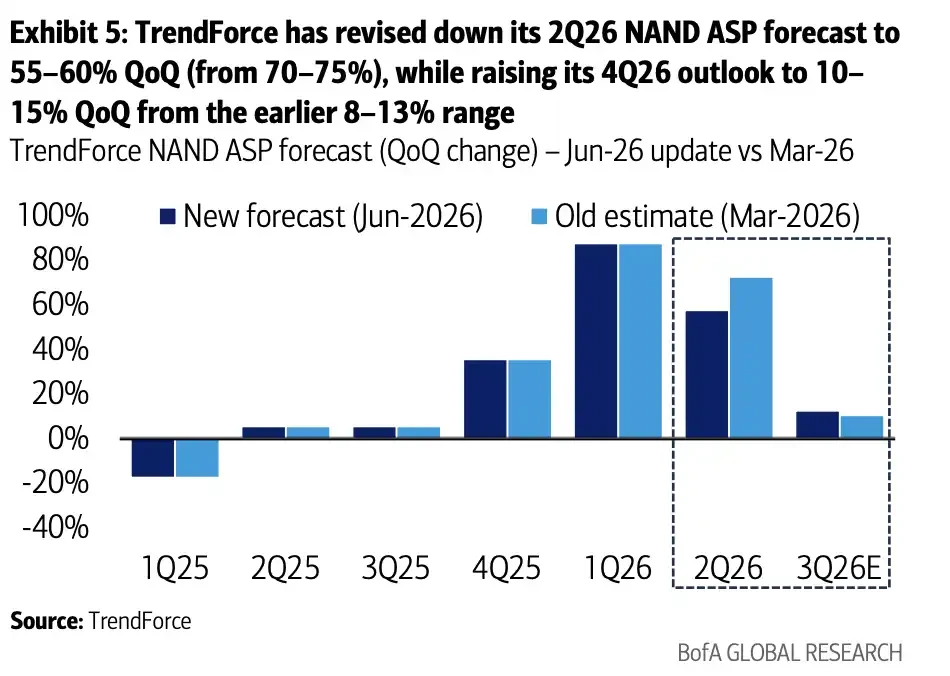

Price forecasts are also relatively strong. In its June update, TrendForce raised its forecast for DRAM average selling price in the third quarter of 2026 to a sequential increase of 13%-18%, up from a previous estimate of 3%-8%. Bank of America's report estimates DRAM price sequential growth for Q2, Q3, and Q4 of 2026 at 5.3%, 17%, and 7% respectively, and NAND price growth at 6.5%, 13%, and 1% during the same period. The two sets of forecasts are broadly aligned for Q3 and Q4, with differences mainly in the Q2 pace and some NAND price assumptions.

June semiconductor exports reached approximately $44.8 billion, up 199.5% year-over-year

Q3 2026 DRAM price expectations were raised to sequential growth of 13%-18%

The spot market also indicates continued supply tightness. According to Bank of America's report, in early July, the spot price of 16Gb DDR5 reached a new high of $4.7, 16Gb DDR4 was around $7.5, and 512Gb NAND wafers were near $2.0. Prices saw a pullback from April to May but rebounded in June. DRAM manufacturers' prioritization of HBM production further squeezes the supply of traditional DRAM.

The higher the prices go, the more the market worries about a cycle reversal. The current divergence isn't about whether the memory market is strong in the short term, but whether this strength is already fully priced into stocks, and whether AI demand can continue to absorb these higher prices.

Samsung's Q2 Preliminary Earnings: A Proximity Test for the Memory Market

Samsung is expected to release its preliminary Q2 results on July 7th, which will serve as a short-term test for market sentiment regarding the memory cycle. According to Moneycontrol citing Bloomberg, the market will focus on whether its operating profit can alleviate pressure from the cooling AI trade.

Overall profit may be impacted by factors like special bonuses booked in Q1 and margin pressure from the smartphone business, potentially coming in below some optimistic expectations. However, Bank of America believes that memory division operating profit could exceed market consensus, primarily benefiting from rising average selling prices.

This highlights the delicate situation for memory stocks currently. Overall company profit might be muddied by factors like mobile phones and bonuses, but the memory business itself remains in an upward pricing phase. If Samsung's memory division performance significantly beats expectations, it would strengthen the view that the July 2nd correction was more a release of concentrated sentiment and worry. If price transmission or margins disappoint, concerns about a cyclical peak will intensify.

Valuation does not entirely eliminate risk. Despite significant earnings expansion in memory stocks, P/E ratios remain relatively moderate, and ROE has improved markedly. However, the sector has already seen substantial gains since the beginning of 2026, and the July 2nd correction indicates that investors are becoming more sensitive to any potential negative news.

Ultimate Debate Centers on AI Capex Post-2027

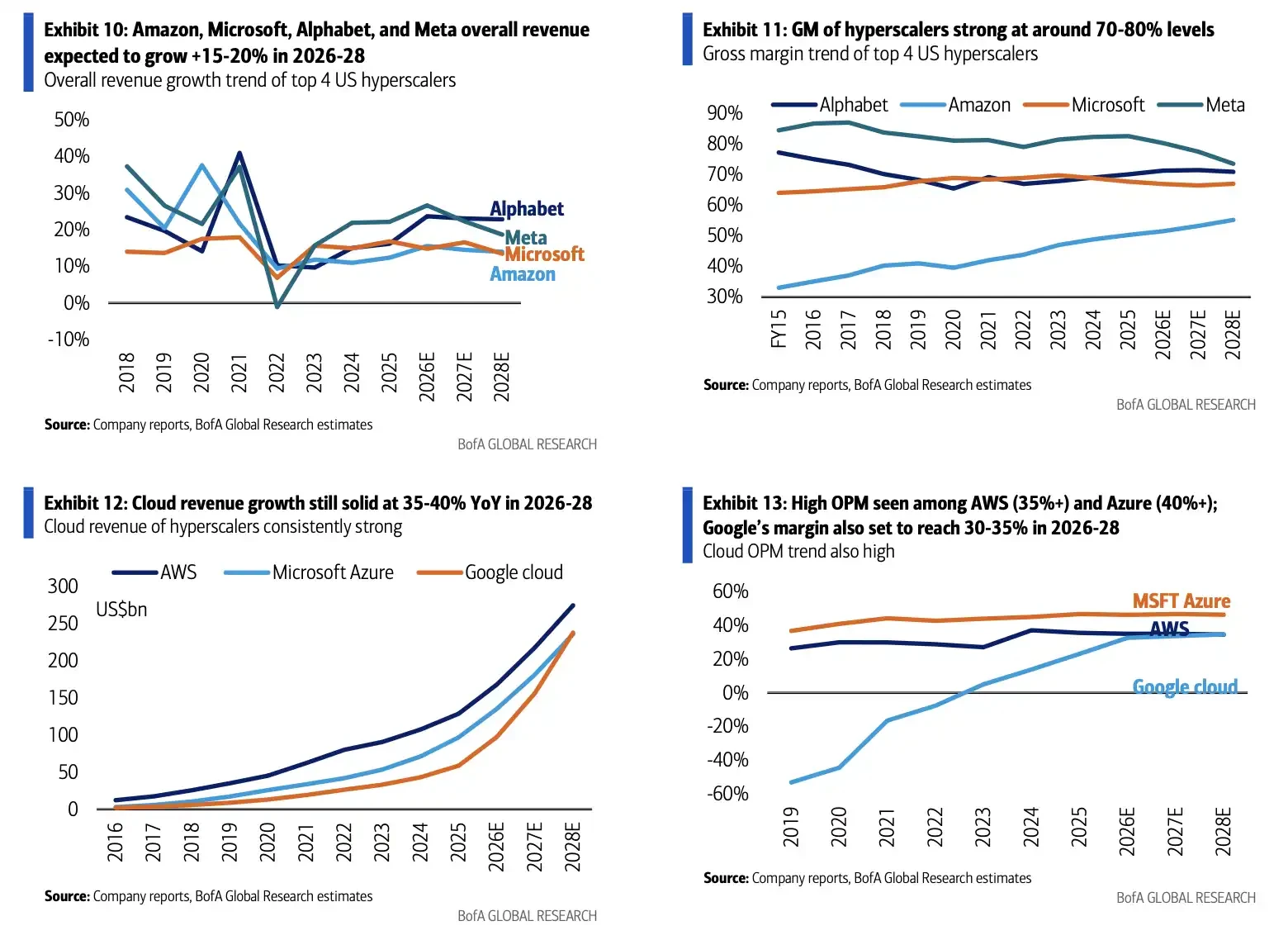

The broader context supporting memory demand is the ongoing expansion of capital expenditure by cloud giants. According to media compilations and analyst estimates, major cloud providers like Amazon, Microsoft, Alphabet, and Meta could see AI-related capex reach approximately $700 billion in 2026, a significant increase over the previous year, potentially remaining high through 2027-2028. This figure is not an official combined guidance from the four companies, and different compilations including companies like Oracle may yield different results.

Trends in major cloud provider capital expenditure, cloud revenue, and profit margins. 2026 capex is expected to be in the ~$700 billion range, a crucial support for sustained high-end memory demand.

Therefore, this pullback in memory stocks feels more like the market preemptively testing three questions: Is Meta actually cutting back on AI infrastructure investment? Can CXMT move from token entry into Apple's supply chain to large-scale substitution? Will South Korea's long-term investment plan eventually translate into a new wave of supply pressure?

Currently, these questions haven't yielded answers sufficient to overturn the cycle. Export data, spot prices, price forecasts, and cloud provider capex still point to strong demand. However, risks remain. AI capex needs to continue materializing beyond 2027. Geopolitical restrictions may alter supply chain choices, and China's localization process will continue to influence negotiations between Korean/US memory giants and their clients.

Whether the memory cycle has peaked is currently not a conclusion confirmed by data. More accurately, the market has moved from a phase of "only watching price increases" to a phase of "verifying how long the price increases can last."