高盛半导体财报季前瞻:SOX暴涨后,AMD和AMAT还能涨吗?

- 核心观点:高盛认为半导体二季度盈利仍有上调空间,但板块已大幅上涨(SOX单季涨87.8%),不再适合普涨;AI资本开支、DRAM/HBM、先进封装和EDA工具是核心主线,而个股分化将加剧。

- 关键要素:

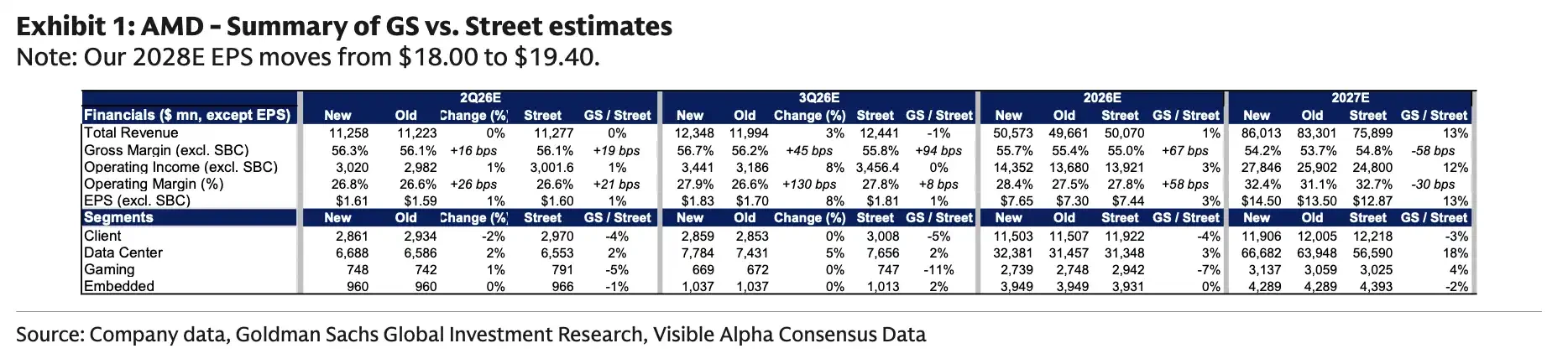

- AI资本开支驱动计算领域:AI服务器CPU、云厂商ASIC项目和AI加速卡支撑AMD等公司数据中心收入,AMD 2027年EPS预测被上调至14.50美元,高于市场预期13%。

- 内存与设备受益中期需求:DRAM/HBM供需偏紧、HDD定价改善;设备公司订单可见度延伸至2028年,应用材料被上调目标价至645美元,基于DRAM投资推动2026年增长。

- 模拟半导体分化明显:高盛偏好工业、航空国防和数据中心敞口高的公司(如安森美),对依赖智能手机或传统汽车周期的标的更谨慎。

- ARM与科磊需谨慎:ARM面临智能手机疲软和高运营费用压力,维持卖出评级;科磊受WFE支出向DRAM倾斜影响,可能跑输同行。

- EDA与高通受益AI扩散:Cadence受agentic AI工具和EDA需求推动,收入指引可能上调;高通数据中心业务被纳入增长叙事,FY27-28收入模型设50-82亿美元。

TL;DR

- Goldman Sachs expects most semiconductor sub-sectors to have room for upward revisions in Q2, but the SOX index has already surged approximately 87.8% in a single quarter.

- AI capital expenditure, DRAM/HBM, advanced packaging, and EDA tools are the primary drivers of this round of earnings upgrades.

- Goldman Sachs prefers AMD, AMAT, and ON, is more cautious on ARM and KLAC, and maintains a limited view on Qnity after its price increase.

Before the semiconductor earnings season, stock prices had already run up significantly. The Nasdaq Q2 review shows the PHLX Semiconductor Index rose 87.8% in the second quarter, the best quarterly performance since its inception in 1994, far outpacing the broader US stock market. In a Q2 semiconductor outlook, Goldman Sachs stated that while fundamentals still have room for upward revision, the sector post-rally is no longer suitable for buying across the board. AI servers, memory, advanced packaging, and design software remain the strongest themes, while weak smartphone demand, shifts in equipment spending structure, and export restrictions will amplify individual stock divergence.

Semiconductors Still Have Room for Upgrades, but the AI Chain is Beginning to Stratify

Goldman Sachs reports that Q2 results or future guidance for computing, memory storage, semiconductor equipment, and some analog chip companies could still exceed market expectations.

The main theme in the computing sector remains AI servers. Server CPU demand, cloud providers' ASIC projects, and the ramp-up of AI accelerators continue to support the data center revenue outlook for companies like AMD. Memory and storage benefit from tight DRAM/HBM supply-demand dynamics, improved HDD pricing, and favorable NAND cycle expectations, with limited near-term new supply pressure.

The equipment chain's outlook is more mid-term focused. AI servers require more HBM and advanced packaging, and memory manufacturers' capacity expansion and technology upgrades will drive demand for deposition, etching, and other process steps. Some equipment companies' order visibility has already extended to 2028.

The analog semiconductor recovery is not broad-based. Goldman Sachs prefers companies with higher exposure to industrial, aerospace & defense, and data center end markets, and is more cautious on names more reliant on smartphones or traditional automotive cycles.

This divergence is also reflected in Goldman Sachs' tactical choices. The report prefers Applied Materials, AMD, and ON Semiconductor, while being more cautious on ARM and KLA Corp. For semiconductor materials and electronic solutions company Qnity, Goldman Sachs remains positive on improving wafer fab utilization and execution but sees a more balanced risk-reward profile after the stock price increase, a judgment primarily derived from the report's tone.

AMD and Applied Materials are Goldman Sachs' Two Most Explicit Long Picks

AMD is one of Goldman Sachs' clearest long cases in the computing chain. The Goldman Sachs model shows the 2027 EPS estimate for AMD has been raised to $14.50, approximately 13% above the consensus estimate. The 2027 data center revenue forecast is $66.682 billion, about 18% higher than market expectations.

Supporting this view are robust server CPU demand, improving gross margins in the data center business, and operating leverage from the subsequent ramp-up of AI chips. AMD has previously announced its Advancing AI 2026 event will be held and live-streamed in San Francisco on July 23, 2026. Beyond the earnings season, the market will focus on whether AMD can provide a clearer AI server roadmap, customer progress, and revenue trajectory during this event.

Goldman Sachs model shows AMD 2027E EPS of $14.50, higher than the market consensus of $12.87. 2027E data center revenue is $66.682 billion, surpassing the market estimate of $56.590 billion, with server CPU and MI450 ramp-up as key drivers.

Applied Materials represents the end of the equipment chain with stronger order visibility. Goldman Sachs raised its price target for Applied Materials from $520 to $645, based on a 32x multiple on a normalized EPS estimate of $20. The key assumption in the report is that robust DRAM investment will drive best-in-class growth for the company in 2026, with WFE demand visibility extending to 2028.

DRAM is the focal point here. Rising demand for HBM and high-performance memory from AI servers will drive memory manufacturers' capacity expansion and process upgrades. The advantage for equipment companies lies in longer order cycles and higher revenue visibility. The risk is also direct: if cloud providers or memory manufacturers slow down capital expenditure, market expectations for mid-term revenue would be quickly revised downwards.

Goldman Sachs model shows AMAT CY2027E total revenue of $45.972 billion, a 25% year-over-year increase. The DRAM segment is expected to be $12.4 billion, up 41% year-over-year, serving as the primary source of equipment upside.

ON Semiconductor is placed in a relatively positive portfolio context, not based on significant upward revisions, but because near-term expectations have already been lowered. The company announced on June 25 its intention to acquire Synaptics in an all-stock transaction valued at approximately $7 billion, expected to close by mid-2027, subject to approvals including Synaptics shareholders'. Goldman Sachs believes that with investor expectations reset downwards, ON Semiconductor's potential for slightly better-than-expected quarterly performance warrants more attention.

ARM and KLA Corp Show: The Bigger the Rally, the Harder to Ignore Earnings Flaws

Goldman Sachs maintains a Sell rating on ARM with a 12-month price target of $150, based on 50x a normalized EPS estimate of $3. Pressure stems from two main areas: persistently weak smartphone demand and higher-than-expected operating expenses.

ARM is still perceived by the market as a potential beneficiary of AI and high-performance computing. However, the more direct revenue and profit pressures visible in near-term earnings still come from mobile-side licensing revenue and cost expansion. For stocks already priced high on the AI narrative, the market pays more attention to whether recent revenue, margins, and guidance can be delivered.

KLA Corp's pressure comes from the structure of equipment spending. Goldman Sachs expects its quarterly results and guidance to be slightly positive but still potentially underperform peers, as WFE spending shifts towards DRAM. Compared to logic chips and foundries, DRAM requires less intensity for inspection and metrology equipment. An overall upward trend in the equipment cycle does not mean all equipment segments benefit equally.

Qnity's situation falls in between. The company's Q1 announcement showed net sales of $1.315 billion for the first quarter of 2026 and raised its full-year guidance. Goldman Sachs remains positive on improving wafer fab utilization and the company's execution but believes the upside potential versus downside risk now appears more balanced after the stock price increase. For stocks that have already priced in a recovery, earnings reports need to deliver not just good results, but also provide sufficiently strong forward guidance.

EDA and Qualcomm Also Brought into the Earnings Spotlight by AI

AI expectations are not limited to the GPU, CPU, and memory chains but are also spreading to chip design software and data center chips.

Cadence is one of the companies Goldman Sachs favors in the EDA chain. Public filings show the company revised its 2026 revenue outlook up to approximately 17% year-over-year growth after Q1, and it launched an engineering solution for agentic AI chip and system design with NVIDIA. Goldman Sachs further expects the company's 2026 revenue guidance could still be raised, driven by monetization of agentic AI tools, the IP business, and core EDA demand.

Qualcomm's data center business is also back in focus. The company mentioned in its recent Investor Day materials that its data center business will begin contributing billions of dollars in revenue from fiscal year 2027. The Goldman Sachs model sets Qualcomm's data center revenue at $5 billion and $8.2 billion for FY27 and FY28, respectively. For Qualcomm, this represents a growth narrative shifting from smartphone chips to data centers, but orders, customers, and margins still need to be consistently delivered.

The question this earnings season needs to answer is straightforward: Can AI capital expenditure continue to drive upward earnings revisions for semiconductor companies? Over the past quarter, stock prices have already priced in an optimistic outlook. Going forward, the strength of server CPUs, ASICs, HBM, EDA, and equipment orders must be factored into revenue and profit models for 2026 and 2027 to sustain valuations after the rally.

Whether Upgrades Can Catch Up with Stock Prices Will Determine the Degree of Divergence This Earnings Season

The key point for the Q2 semiconductor earnings season is not whether there are still upside expectations for the market, but whether the magnitude of the upside can cover the stock prices that have already risen.

Goldman Sachs' preview points to a more divergent answer. AI capital expenditure, DRAM/HBM, advanced packaging, and the monetization of EDA tools are still pushing up earnings expectations for some companies. After the SOX index has significantly outperformed the broader market, the market's tolerance for flaws is decreasing.

Weak smartphone demand will weigh on ARM, the shift of WFE towards DRAM will diminish KLA Corp's relative advantage, and supply chain constraints, export restrictions, and geopolitical risks could also impact order fulfillment. Companies like AMD and Applied Materials, which still have room for model upgrades, will face scrutiny on the pace of execution. Companies that have already rallied significantly but have limited short-term fundamental flexibility are more likely to face pressure during the earnings season if their guidance lacks strength.