底部反弹已3倍,Lighter怎么就起飞了?

- 核心观点:去中心化永续合约交易所 Lighter(LIT)近三个月币价上涨超 3 倍,主要源于合规进展、与 Robinhood 的战略合作、代币经济模型重塑以及筹码结构优化等多重基本面叙事的共振。

- 关键要素:

- 合规进展:Lighter 创始人加入 CFTC 创新咨询委员会,并启动美国链上衍生品交易牌照申请,凸显其“美国本土”合规优势,区别于竞品 Hyperliquid 的离岸风险。

- 渠道拓展:与 Robinhood Wallet 深度绑定,成为其永续合约交易默认执行层和流动性引擎,Robinhood 庞大用户群可直接访问 Lighter 服务。

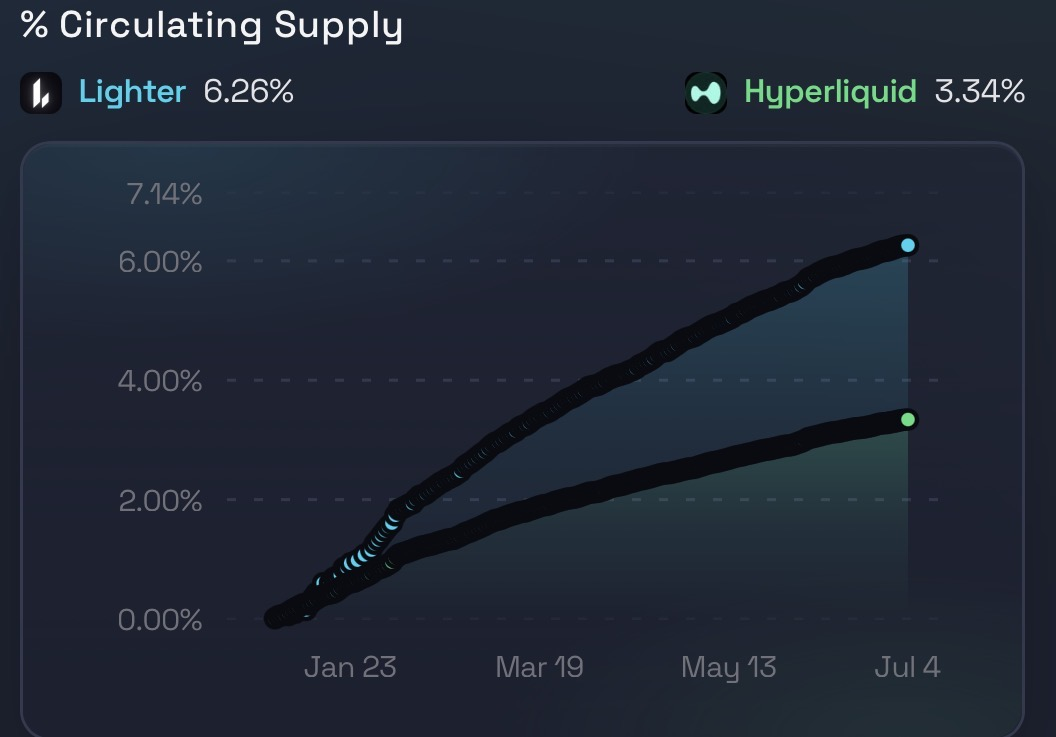

- 代币经济:协议收入全额用于回购并永久销毁 LIT,累计回购约 1550 万枚(占流通供应 6.26%),销毁力度超过 Hyperliquid;同时引入生态代币质押收益(目标年化 6%)。

- 筹码结构:前期持续下跌中完成底部换手,筹码从松散分布转向集中沉淀,市场结构从抛压主导切换至增量资金定价,空头回补放大价格弹性。

- 市场表现:LIT 暂报 2.65 USDT,24 小时涨幅 19.4%,近三个月从低点 0.78 USDT 反弹超 3 倍。

Original: Odaily (@OdailyChina)

Author: Azuma (@azuma_eth)

The decentralized Perp DEX project Lighter (LIT) has demonstrated a notably strong price performance recently.

According to OKX data, as of 14:30 today, LIT was quoted at 2.65 USDT, marking a 24-hour increase of 19.4%. Calculated from its historical low of 0.78 USDT in early April, LIT has achieved a robust rebound of over 3x in the past three months.

Considering Lighter's recent developments in regulation, products, and tokenomics, LIT's strong price performance can be attributed to the simultaneous resonance of multiple fundamental narratives.

Regulatory Progress: The Narrative Advantage of a "US-based" Exchange

The first major driver behind Lighter's recent strength is the rapid clarification of its regulatory pathway.

This is particularly evident when comparing Lighter with its biggest competitor, Hyperliquid (HYPE). While HYPE has long held the leading position in the on-chain Perp DEX sector, its offshore nature is often viewed as a potential regulatory liability. This is especially true against the backdrop of a tightening US regulatory framework, implying persistent policy uncertainty.

In contrast, Lighter positions itself more as a "trading infrastructure born within the US regulatory system." As a US-based project, Lighter is proactively embedding itself within the regulatory framework, thereby gaining a new "compliance premium."

During the Q1 investor conference call in early April, Lighter founder and CEO Vladimir Novakovski explicitly stated that the company has initiated the application process for an on-chain derivatives trading license in the United States. Vladimir commented bluntly: "To serve traditional financial institutions like Citadel, having a license is not optional."

Yesterday, Novakovski announced on X that he has become a member of the Commodity Futures Trading Commission (CFTC) Innovation Advisory Committee. The significance of this in the market context far outweighs the title itself. The CFTC's Innovation Advisory Committee essentially serves as an "institutional buffer layer" between regulators and market participants, tasked with providing policy advice to the CFTC on the intersection of technology, law, and finance. Under current regulatory trends, Vladimir's new role means Lighter is not just "adapting to regulations" but can participate in the early stages of rulemaking.

Furthermore, another noteworthy piece of information is that new Federal Reserve Chairman Kevin Warsh disclosed holding some LIT in his pre-appointment financial disclosure. While this doesn't imply Warsh will use his position for any specific purpose, this "potential policy network connection" still reinforces the market's perception of Lighter's compliance resource advantage.

New Channel Unlocked: Deep Integration with Robinhood

Beyond regulatory progress, the second key variable for Lighter's recent breakout is the opening of new distribution channels, particularly its deep integration with Robinhood.

Last week, Robinhood and Lighter jointly announced that Robinhood Wallet now supports a native Perp trading entry powered by Lighter, allowing users to trade perpetual contracts and tokenized stock assets directly within the wallet, using USDG as the quote asset.

As an investor in Lighter, the market had previously anticipated some form of collaboration between Robinhood and Lighter. However, some users also worried that Robinhood might choose to build its own Perp product, creating competition with Lighter. The latest announcement confirms that Robinhood ultimately chose to integrate perpetual contract trading capabilities through Lighter.

For Lighter, this signifies a qualitative shift in its role — it is no longer just an independent DEX but is progressively becoming the default execution layer and liquidity engine within the Robinhood Wallet ecosystem, making its services more accessible to Robinhood's vast user base.

Ansem, a well-known trader recently gaining attention due to the surge of his own Meme token, gave this development a highly positive assessment: "The collaboration between Lighter and Robinhood looks like they're aiming for something big."

Reshaping Tokenomics: All Buyback Tokens Burned

Another key move by Lighter recently was the announcement on July 1st of updates to its tokenomics model, further solidifying LIT's pricing logic as a "cash flow-driven asset."

In this update, Lighter explicitly committed to using all protocol revenue to repurchase LIT, upgrading the buyback mechanism from "programmatic buying" to "permanent burning." As of that time, Lighter had repurchased approximately 15.5 million LIT, representing about 6.26% of the circulating supply, with the first on-chain burn scheduled after the end of Q2.

Simultaneously, LIT's staking mechanism was redesigned. After an initial phase subsidized by pre-TGE revenue, the team announced a gradual transition to using ecosystem tokens for staking rewards, targeting an annualized yield of approximately 6%. With the current staking volume of around 125 million LIT, this corresponds to an annual distribution of approximately 7.5 million tokens.

Within this framework, LIT's economic model begins to present a relatively clear structure: on one end, sustained protocol revenue ➡️ full repurchase and burn ➡️ contraction of circulating supply; on the other end, staking rewards for long-term holders ➡️ directed distribution in the form of ecosystem tokens.

Data analyst ajey.lit, who tracks the Perp DEX sector, posted a comparison of buyback data between LIT and HYPE, with quite surprising results. Compared to HYPE, which has always emphasized revenue and buybacks, LIT's repurchase intensity appears relatively stronger — as of now, Lighter's repurchased tokens account for approximately 6.26% of the circulating supply, significantly higher than Hyperliquid's (HYPE) approximately 3.34%; calculated by the ratio of buyback amount to market cap, Lighter's buyback accounts for about 4%, also higher than HYPE's approximately 1.8%.

Shift in Token Distribution: Handover Complete, Lighter Setup for Rally

Looking at the three threads of compliance, distribution, and economic model together, LIT's rise doesn't appear driven by a single catalyst but rather by a typical process of "delayed pricing + collective revaluation."

The prerequisite for all this is that LIT's bottom-level tokens had undergone sufficient washout during the prior continuous decline.

Since LIT's TGE, factors like the overall sluggish crypto market, intense competition in the Perp DEX sector, and the continuous exit of early airdrop users created a typical downward selling pressure structure for LIT. Meanwhile, market makers and long-term capital completed sustained accumulation at low levels, causing tokens to gradually shift from "scattered distribution" to "concentrated holding." This process can essentially be understood as a bottom-handover event.

As Lighter's fundamentals gradually improved, LIT's market structure also shifted from being "dominated by supply overhang and selling pressure" to being "dominated by incremental capital pricing." Under this structural change, marginal improvements in fundamentals began to be truly amplified. Furthermore, this structure was compounded by concentrated short positions. During the prolonged consolidation and bearish expectations, some short positions accumulated. When the price broke through key ranges, market liquidity became distinctly asymmetric — selling pressure from above was insufficient, while short covering provided a new source of buy orders, amplifying price elasticity.

In summary, LIT's current rally should not be understood as a single-factor event but as the combined effect of three levels: First, fundamentals shifted from uncertainty to verifiability; second, the token structure shifted from being dominated by selling pressure to a completed handover; third, shorts and liquidity structure inversely amplified elasticity.

LIT did not "suddenly become stronger"; it is simply "being progressively repriced."