a16z pours $500 million in one month, while small funds are shutting down in droves: Where is crypto VC money flowing?

- Core Thesis: While the book value (TVPI) of the current venture capital market has significantly recovered, actual cash returns to investors (DPI) remain extremely low, making liquidity the dominant contradiction. This phenomenon is even more extreme in the crypto VC space, characterized by a power-law distribution and capital concentration towards top-tier players.

- Key Elements:

- As of Q1 2026, the median TVPI of funds tracked by Carta has rebounded for six consecutive quarters, primarily driven by top-tier projects in the AI sector, but the recovery is not universal.

- The median DPI for vintage year 2019 and 2020 funds is only slightly above zero, with over half having not returned any cash to LPs; less than 20% of vintage 2017/2018 funds have achieved a DPI of 1x.

- VC returns follow a power-law distribution. The net IRR of funds at the 90th percentile generally exceeds 20%, a stark gap from the 15.5% at the 75th percentile, while the median fund performs modestly.

- Capital is concentrating towards top-tier funds. Funds larger than $100 million absorbed 57% of all VC capital in 2025, compared to just 31% eight years ago, with mid-tier funds facing significant fundraising challenges.

- The largest crypto funding rounds in June included a $355 million strategic round for Digital Asset (led by a16z, with participation from Wall Street institutions) and a $175 million DeFi lending round for Morpho, indicating institutional capital is accelerating its influx into infrastructure tracks.

Original author: Ben Lakoff, CFA

Original compilation: TechFlow

TechFlow Summary: The title of Carta's latest report is "VC is back," but the recovery is only in paper valuations (TVPI); real money (DPI) has yet to return to LPs. This monthly funding report breaks down the respective situations of GPs and LPs in 2H26: who is making money, who is just holding on, and what this logic looks like when applied to crypto VC. The author, Ben Lakoff, is a licensed CFA specializing in early-stage crypto investments, offering direct insights with high data density. The end includes all crypto funding transactions and hackathon results from June.

GM!

Welcome to the June Deal Flow Digest, a snapshot of all the crypto funding I tracked last month.

This month's feature article dives into VC fund performance. Carta released its Q1 2026 VC Fund Performance Report with the headline "VC is back." But paper returns are coming back much faster than cash. Let's break down what TVPI and DPI really mean, what GPs and LPs will face in 2H26, who the real winners are, and what this logic looks like specifically for crypto VC.

Don't forget to check the table at the end for all June deals, plus the latest hackathon and Demo Day results (linked).

Carta tracked 2,775 funds holding approximately $119.3 billion in assets. The data shows that median fund valuations for almost every recent vintage are up, fundraising pace is accelerating, and the overall outlook for venture capital has improved significantly.

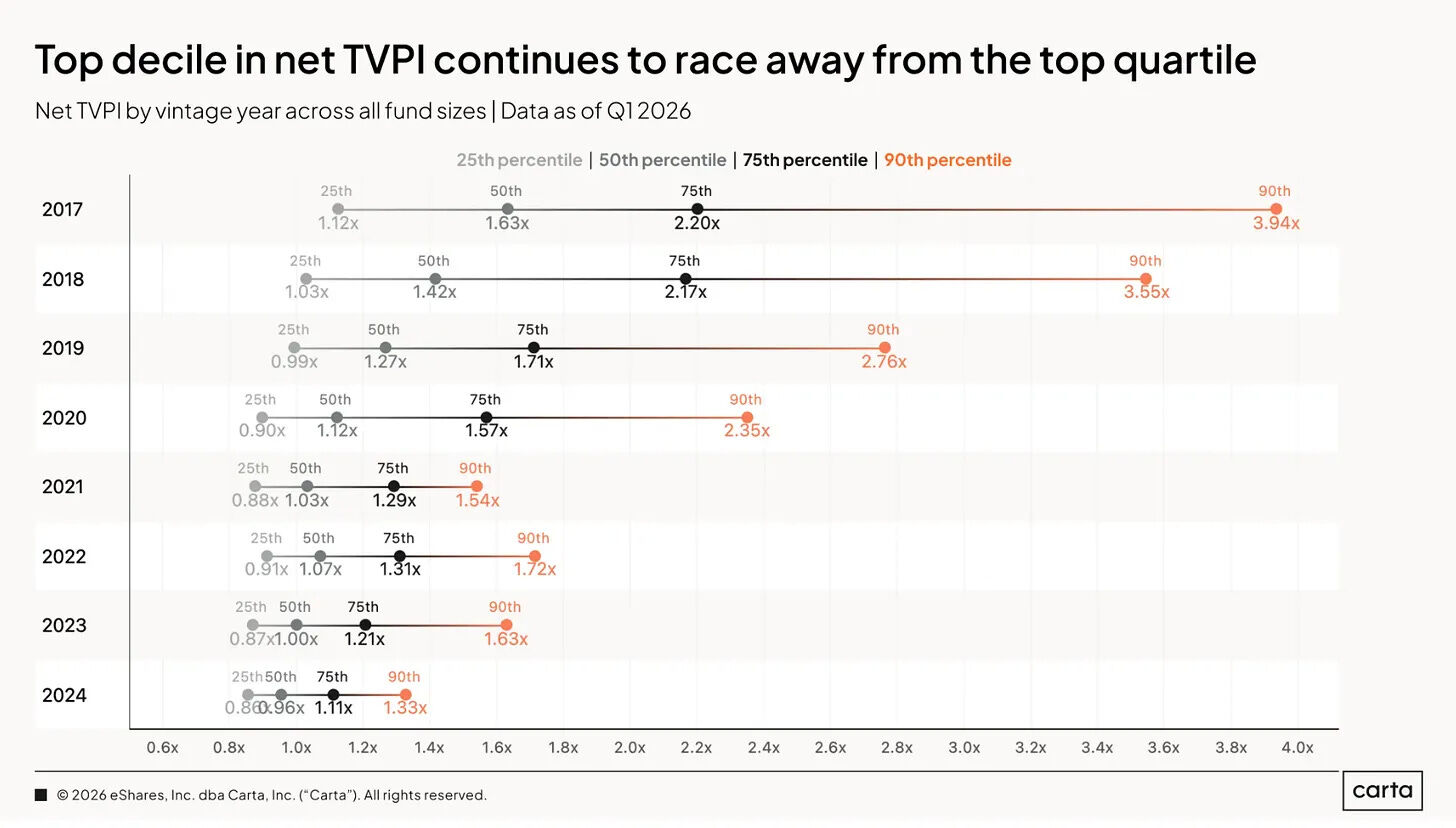

From 2017 to 2024, median TVPI has been climbing for almost every vintage, and for six consecutive quarters. TVPI (Total Value to Paid-In) measures what a fund is worth now, including unrealized paper value. The valuation reset from 2022 and 2023 that wiped out everyone's books is essentially over.

That's the good news. But the key part of the story is: paper is back, but cash is not.

VC is Recovering, but Only Unrealized Paper Value (TVPI) is Up

Let's start with the truly positive aspect. The median TVPI for the sample is moving up and to the right again for basically every recent vintage. Valuations stopped falling first, then started recovering, and the funds holding these assets mechanically became more valuable.

Note: Median TVPI for funds by vintage year has been recovering for six consecutive quarters

Source: Carta Q1 2026 Report

Who's driving this? Mainly the top tier.

90th percentile valuations across all stages are soaring, and much of this comes from one sector. Carta's companion Private Markets Report shows that AI consumed a record share of every venture dollar invested. If your fund has AI exposure, your books are healthy. If you're in the infrastructure "picks and shovels" business or betting on narratives outside AI, your "recovery" will be much weaker.

So, this rising tide isn't lifting all boats. It's basically (and significantly) only lifting the boats carrying foundation models. Not surprising.

This determines how you should read that headline number. High TVPI doesn't equal a good fund. It's a snapshot reflecting what someone, somewhere, would theoretically be willing to pay, not the cash actually hitting LP accounts.

No One is Actually Getting Cash (DPI)

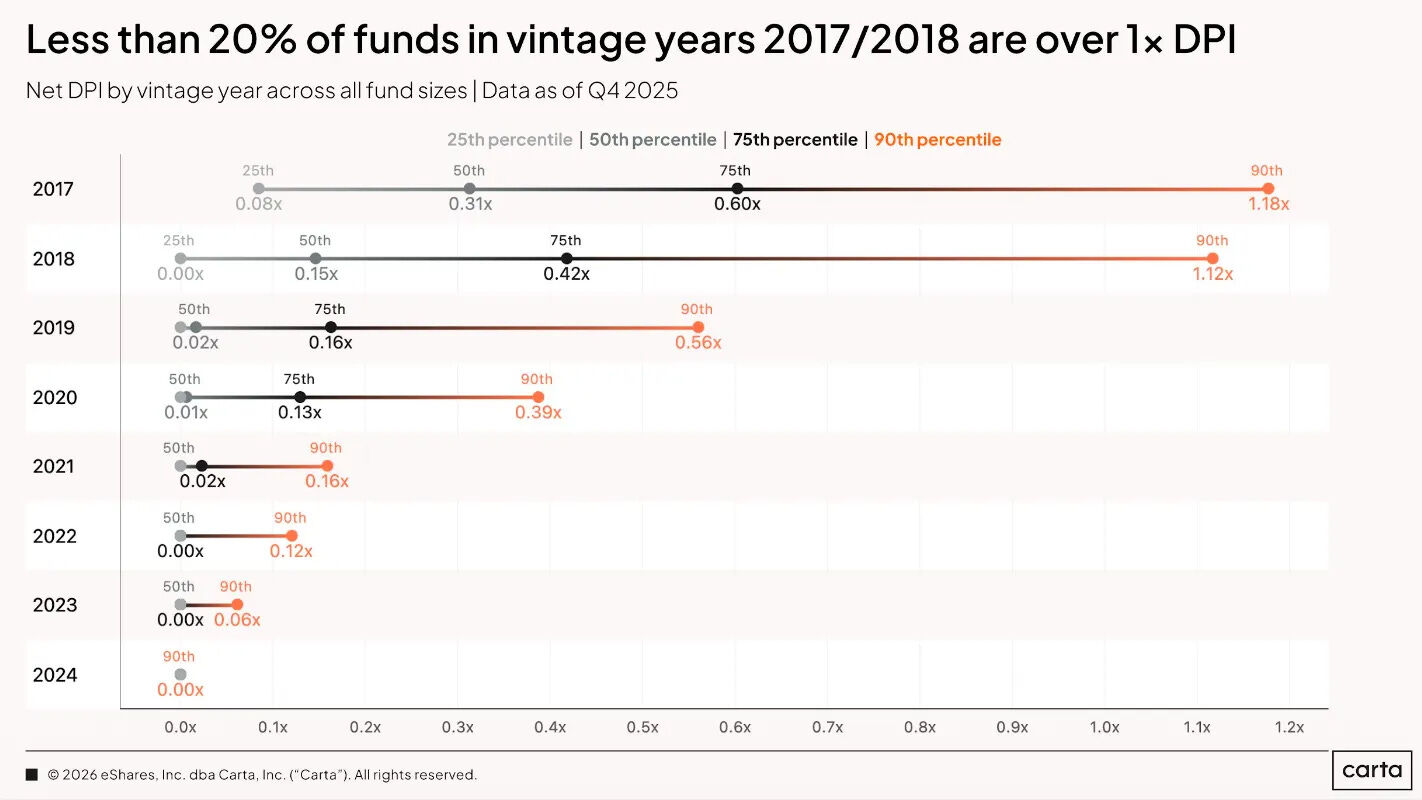

This is the part the recovery story skips. DPI (Distributions to Paid-In), the cash a fund actually returns to LPs, remains very low.

For 2019 and 2020 vintage funds, the median DPI is only slightly above zero. Over half of these funds haven't returned a single dollar to LPs. These are funds that are five to six years old.

Note: Median DPI for 2019 and 2020 vintage funds is only slightly above zero, with over half yet to return any cash

Source: Carta Q1 2026 Report

Older vintages should be better, but are actually worse. Funds from 2017 and 2018 are nearly ten years old, in the latter half of their lives, when distributions should be materializing. Yet, less than 20% of these funds have reached a 1x DPI, meaning they've returned the LPs' initial capital.

The problem is the J-curve refusing to complete its upward swing. Early on, funds go negative IRR as they invest capital. Then, as valuations rise and exits occur, the curve should bend upwards. Now, valuations are rising (as TVPI proves), but exits aren't happening. The IPO window is only slightly ajar for a select few names, M&A is selective, and everything else is stuck at high prices, unable to move.

PitchBook, Preqin, NVCA, Wellington – all point to the same conclusion for 2026: liquidity is the bottleneck. Simple as that. The widely considered antidote is the secondary market: continuation vehicles, GP-led transactions, and LPs selling their stakes for cash instead of waiting for traditional exits. This is moving from niche to common practice quickly.

For GPs, the signal is uncomfortable but straightforward. A fund with great TVPI and near-zero DPI will start getting difficult questions in the next 12 to 18 months. LPs have been very patient throughout the reset. Before they recommit, they want to see cash. GPs who can proactively manage a liquidity path (partial exits, secondaries, continuation funds) will have an advantage over those who just keep reporting healthy paper numbers.

VC is a Power Law Game, and the Dispersion is Massive

Regardless of the recovery, dispersion is the permanent characteristic of VC.

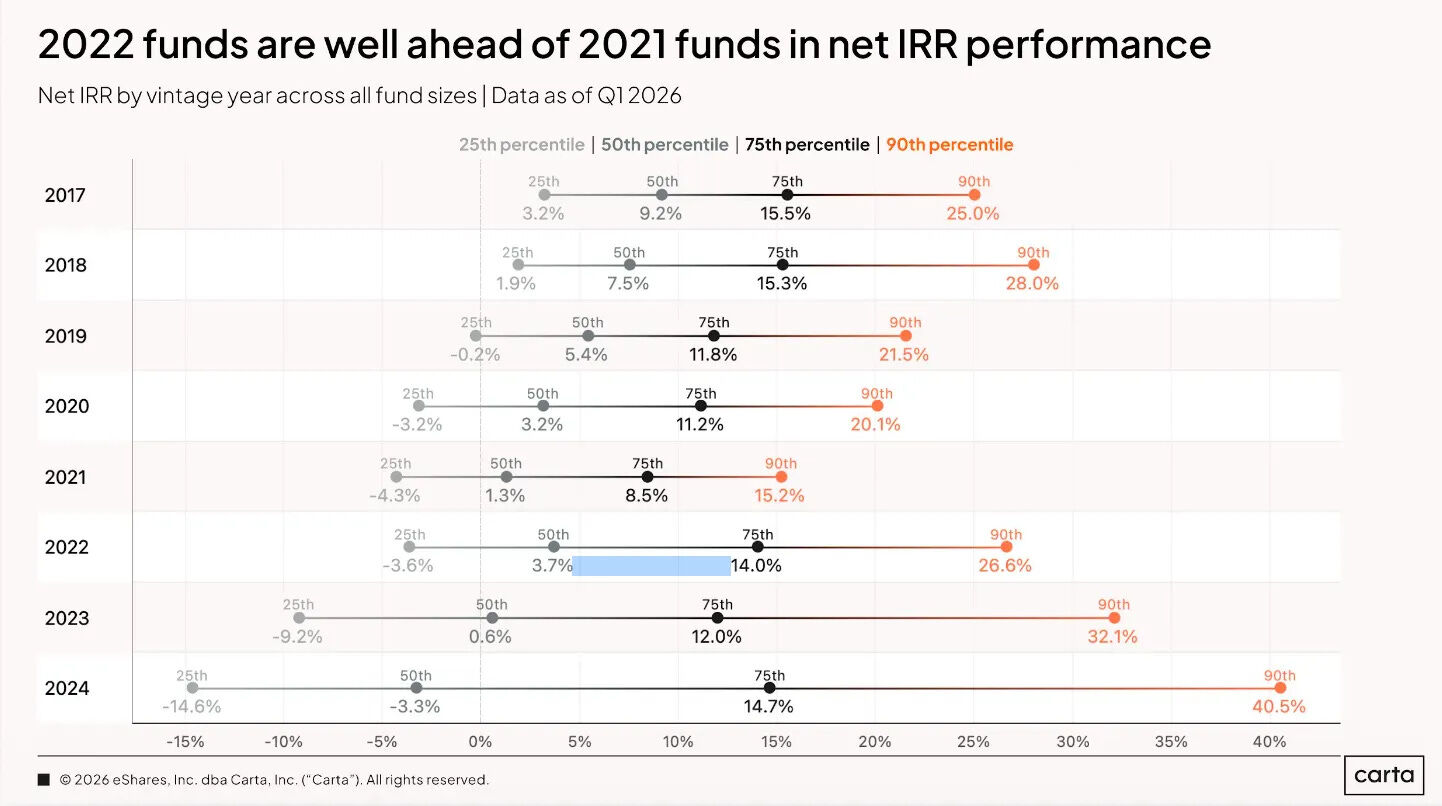

Across nearly every vintage, the 90th percentile net IRR is above 20%, while the 75th percentile is still below 15.5%. The gap between being in the "top quartile" and the "top decile" is enormous. Most funds are clustered in the "okay" tier.

And this gap compounds. For context: 20% annualized growth over 10 years is a 6.2x return, while 10% annualized growth is 2.6x.

Note: Net IRR distribution for funds by vintage year. The 90th percentile generally exceeds 20%, a significant gap from the 75th percentile.

Source: Carta Q1 2026 Report

VC isn't just the asset class with the highest returns; it's also the one with the highest dispersion.

Translation for LPs: Manager selection isn't just one of many inputs; it is the input. Indexing the entire asset class gets you the median, and the median VC fund is, at best, a slow, illiquid 2.6x return.

The Middle Ground is Being Squeezed Out

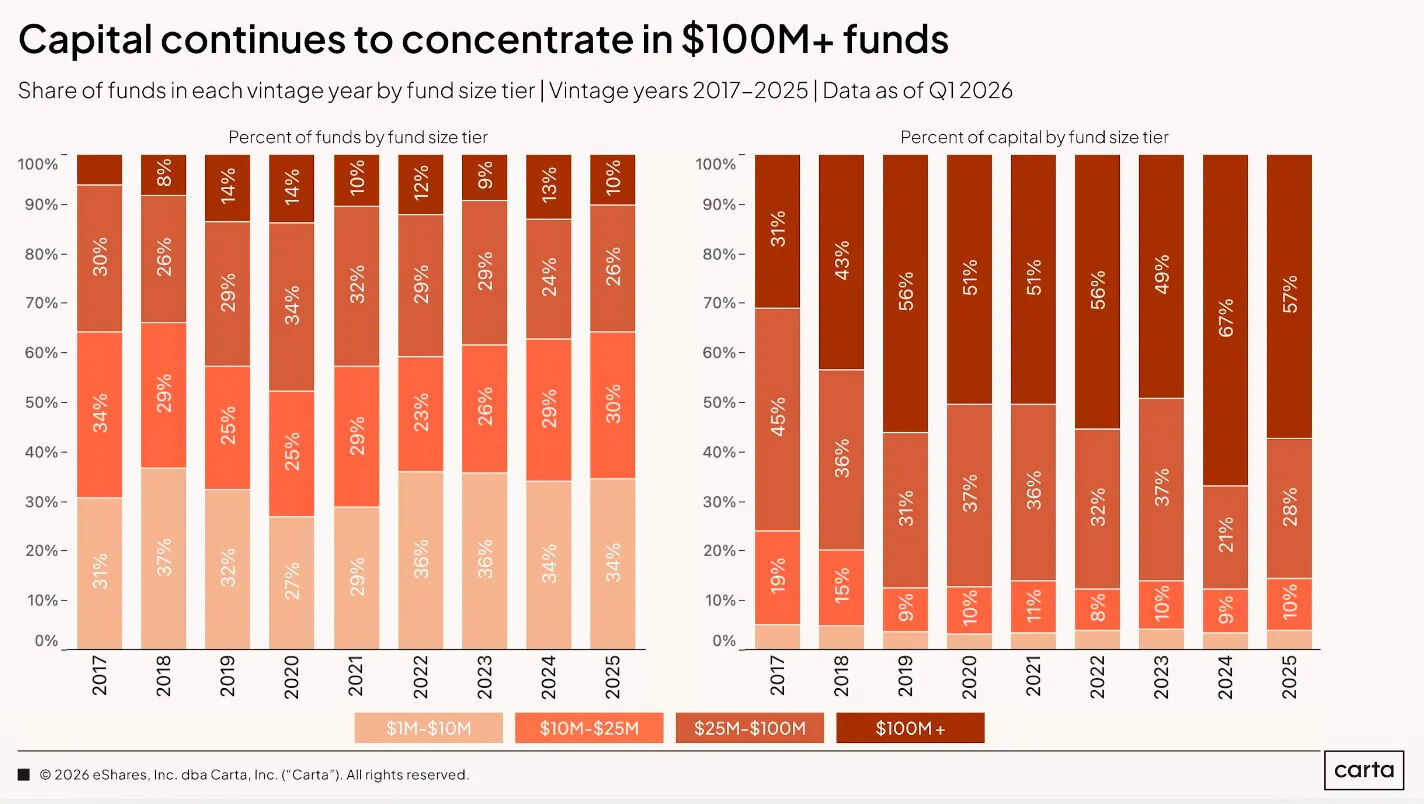

The final piece, perhaps the most structural one, and a recurring theme in my recent articles: money is concentrating.

Note: Capital is concentrating towards top-tier funds

Source: Carta Q1 2026 Report

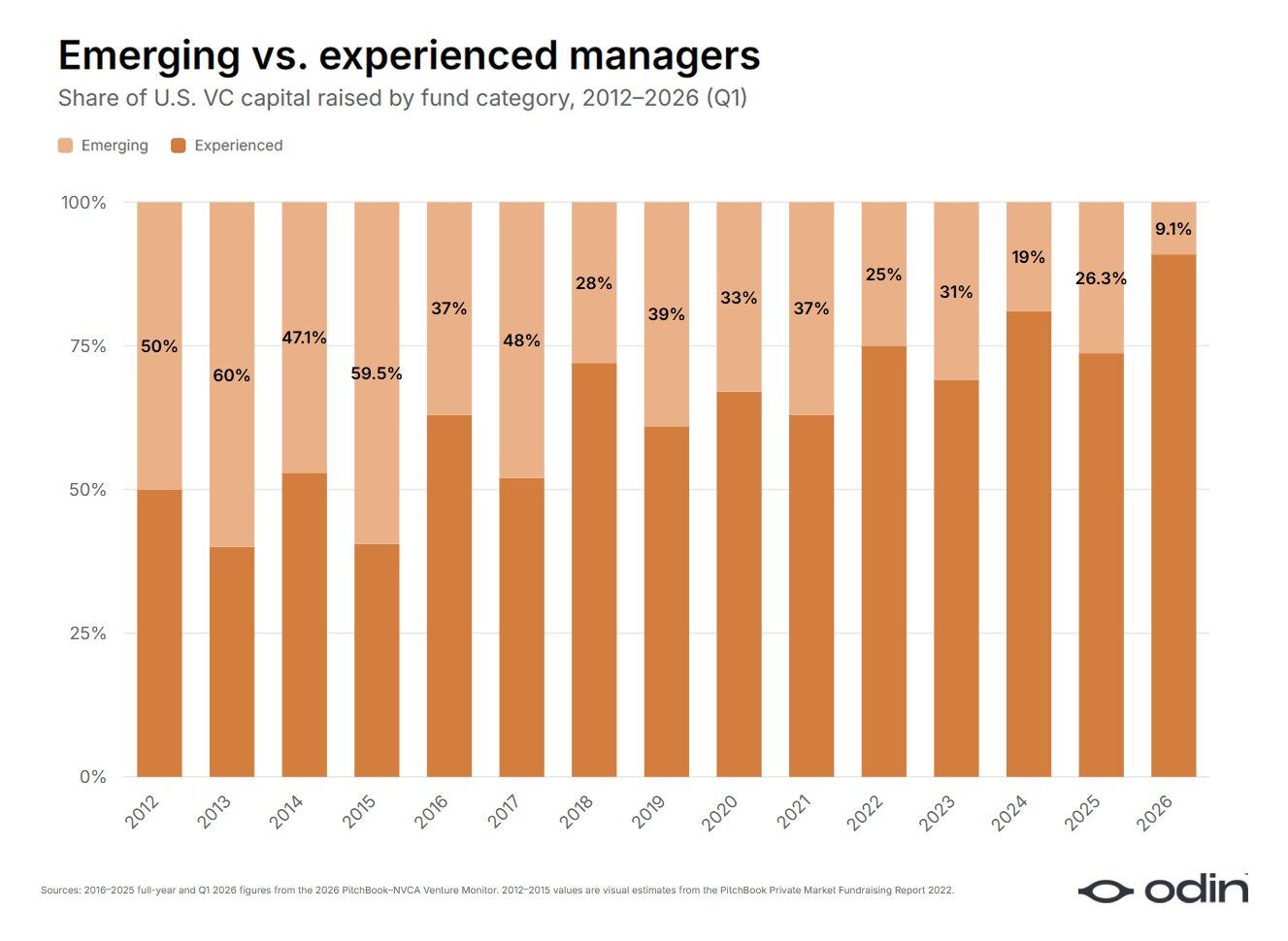

Funds over $100 million captured 57% of all VC fundraising in 2025. Eight years ago, that number was 31%. Most newly formed funds are still small, under $25 million, but large funds are absorbing an increasing share each year.

Note: Small funds under $25 million still represent the majority in number, but total fundraising volume is skewed towards larger funds

Source: Carta Q1 2026 Report

This is a barbell structure. Mega-funds raise capital on their balance sheets and brands. Truly differentiated micro-funds raise capital on their niche strategies. The undifferentiated middle is where fundraising goes to die. Part-time VC managers are heading back. The crossover capital and generalist funds that flooded into private tech during the 2021 highs are retreating to their core businesses.

Overall fundraising is stabilizing (Carta recorded 86 new funds and $3.9 billion in Q1, the strongest start since 2022), but "stabilizing" doesn't mean "evenly distributed." This capital is flowing toward those with track records and leaving everyone else behind.

My Key Takeaways

Boiled down to four points:

Paper is back, cash is not. TVPI is a story about sentiment; DPI is the only number LPs can actually spend.

The power law is alive. A few funds win big, most are mediocre, and the distance between them is the entire game.

Liquidity is the next dominant logic. Funds that can generate distributions, not just report paper gains, will win the next fundraising cycle.

Capital concentration is the trend. Be big, be sharp, or don't be stuck in the middle.

Carta doesn't break out crypto separately, so these aren't "our" numbers. But the physical laws are the same, just louder in crypto.

Crypto VC is more dispersed, more concentrated, and more reflexive than the broader market. Part-timers fled here earliest and hardest. This suits me fine: in the pre-seed stage, the only lasting advantage is picking the right person before the crowd arrives. The data consistently confirms this; the median is a trap, the action is in the tails.

Alright, now for the rest of the June crypto and web3 funding :)

Top 10 Crypto Funding Rounds in June

Securitize | SPAC Merger / PIPE | RWA Tokenization | ~$400M | 2026-06-26

This BlackRock-backed tokenization leader is going public on the NYSE (ticker: SECZ) via a merger with Cantor Equity Partners II, aiming for gross proceeds of ~$400M, including an oversubscribed $225M PIPE. Clients include Apollo, KKR, Hamilton Lane, and VanEck. Securitize is also building the NYSE's own tokenized securities platform. This is a public listing, not a private VC round, so it gets the asterisk at the top, but it's also the cleanest milestone this year for "tokenization going mainstream." The deal is expected to close around July 1st.

Digital Asset | Strategic Round | Institutional Infrastructure / L1 | $355M | 2026-06-11

a16z crypto led what is arguably the largest true crypto funding round this month, at a $2B valuation. The follow-on list reads like a Wall Street roll call: Citadel Securities, an Abu Dhabi Investment Authority entity, BNP Paribas, HSBC, Apollo, Optiver, Tradeweb, CME Ventures, S&P Global, SBI, SoFi, Coinbase Ventures, and Polychain. Digital Asset builds Canton, a privacy-enhanced public L1 blockchain for regulated capital markets, already supporting ~$6 trillion in tokenized asset issuance. Users include JPMorgan, DTCC, and Visa. If you need a data point for "TradFi is choosing its rails," this is it.

Morpho | Strategic Round | DeFi Lending | $175M | 2026-06-09

Co-led by Paradigm, Ribbit Capital, and a16z crypto, with participation from Apollo Funds, Circle’s venture arm, and VanEck, at a valuation of up to $2B. Reportedly the largest DeFi round ever. Morpho allows anyone to "build their own Aave" – customizable lending markets. Its client list (Coinbase, Kraken, Anchorage, Galaxy) explains why institutional capital is suddenly comfortable underwriting on-chain credit. The thesis "DeFi is the backend of fintech" just got funded.

Fomo | Series B | Consumer Trading | $75M | 2026-06-22

Index Ventures led the $75M round at a $550M valuation, with participation from Union Square Ventures and angels like Mark Pincus, Kevin Hartz, and Humam Sakhnini. Fomo is a non-custodial social trading app that abstracts away wallets, gas, and bridging. It takes about 30 seconds to onboard, fund, and buy a token, layered with leaderboards and social features. With 625k+ users and $4B in volume, it's the brightest consumer-focused raise this month.

SignalPlus | Series B | Institutional Derivatives